This earnings season will be unlike any other, as travel restrictions and lockdowns related to COVID-19 have impacted results dramatically.The biggest economic hits came in mid-March, however, and won’t be fully captured in first quarter results. This makes company guidance particularly important as market participants look for clues into what earnings may look like for the rest of the year.

EARNINGS SEASON UNLIKE ANY OTHER

It goes without saying that this will be a reporting season unlike any other. For some companies less impacted by the COVID-19 pandemic, the numbers may appear normal. For others, the focus will be on balance sheet strength and survival. The separation between winners and losers is widening in this environment.

Turning to the numbers, with 41 S&P 500 Index companies having reported results (mostly with quarters ending in February), index earnings are tracking to a 14% year-over-year decline, down from the 4% increase expected on January 1 and 5% decrease expected as of March 31. We think even these lowered estimates may be tough to achieve, given heightened uncertainty during the pandemic, the significant number of companies that have withdrawn their guidance for analysts, and lingering stale estimates.

WHAT TO WATCH

We highlight four main themes for this earnings season:

Don’t count on a low bar. The bar has been lowered significantly, which is typically a recipe for better-than- expected results. According to Bespoke Investment Group, analysts have raised estimates for only 88 companies in the S&P 1500 Index over the past four weeks, while 1,236 companies have seen estimate cuts, the most since at least 2008. However, with so many companies having pulled their guidance, and the dramatic changes in economic conditions over the last few weeks of the quarter, misses may be more prevalent than they typically might have been, even in a recession.

There will be winners. This environment may also provide opportunities for some well-positioned companies:

· So-called “stay-at-home stocks,” many of them in internet, digital media, and e-commerce, have performed well recently in anticipation of strong results.

· Many consumer staples companies are helping us stock our shelves and eat all of our meals at home.

· Even before COVID-19, healthcare companies enjoyed perhaps the best visibility into their near-term earnings prospects. They’re playing a key role in testing and treatment and are big stimulus recipients.

· Results for the technology sector may surprise to the upside, based on the relative resilience of the sector’s estimates in recent weeks and current mobility and work-from-home trends.

Finding the floor. For companies most impacted by COVID-19, the focus will be on survival more than anything else. It will be about balance sheets and cash piles. Some of the hardest hit areas will include travel- related businesses, such as airlines and hotels, and certain brick-and-mortar retailers, restaurants, and entertainment companies that are deemed non-essential and depend on public gatherings. With oil prices having fallen more than 60% in the first quarter, earnings in the energy sector may be extremely challenged.

All about guidance and scenarios. With so many companies pulling their outlooks, analysts and strategists forecasting in this environment have had to do some guessing. Given the uncertainty, investors will be looking for help developing credible scenarios depending on how long the stay-at-home orders remain in place. Every country and state is in a different place, increasing forecasting difficulty.

WHAT WE KNOW ABOUT 2020

While forecasting in this environment is very difficult, we now know more than we did a month ago:

Recession almost certainly began in March. We have sufficient evidence to say with confidence that a recession began in late March. The contraction in US economic activity, measured by gross domestic product, may approach 10% during the second quarter (not annualized). The unemployment rate is at its highest level since the Great Depression, possibly in the low-to-mid teens.

Containment efforts are working. In terms of beating this virus, social distancing is working, and the outbreak already may have passed its peak in the United States. The progress has opened the door to easing some lockdown restrictions and a gradual reopening of many state economies in the United States beginning as soon as this week. The Trump administration’s guidelines for reopening, released April 16, likely contributed to April 17’s stock market rally by shoring up confidence in the recovery. Some promising treatments in development also helped.

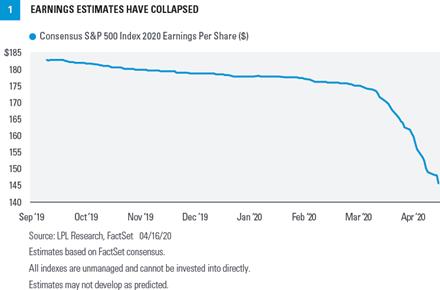

Estimates have collapsed. Finally, we also know that consensus 2020 earnings estimates for the S&P 500 have fallen precipitously in recent weeks to around $145, according to FactSet, suggesting that our prior base case earnings forecast for the S&P 500 of $158–162 may be overly optimistic [FIGURE 1].

ADJUSTING 2020 ESTIMATES

Based on containment progress and prospects for recovery, we think $138–142 in S&P 500 earnings per share (EPS) for 2020 (previously our bear case) is a reasonable target. That’s about a 15% drop from 2019 and in the range of declines observed in prior short-lived recessions not accompanied by a full-blown financial crisis. We expect a strong second-half economic rebound, supported by massive fiscal and monetary stimulus, to help support a recovery in corporate profits. We also acknowledge uncertainty introduces downside risk.ADJUSTING 2020 ESTIMATES

PLAYBOOK SUGGESTS NEAR-TERM CAUTION

We continue to follow our Road to Recovery Playbook to evaluate the market’s bottoming process. We made two changes to our playbook last week [Figure 2].

One was to Signal #1, “Confidence in the timing of a peak in new COVID-19 cases in the United States,” which we upgraded from “monitoring daily” to “almost there.” We hope to be able to declare the peak in new cases with confidence this week. The second was to Signal #4, “Sentiment and technical analysis indicate limited number of sellers remaining.” Recent gains have removed oversold conditions, with the percentage of stocks in the S&P 500 above their 200-day moving average having crossed above 20% last week, after falling below 5% in late March, suggesting significant technical improvement taking place under the surface.

Two signals remain checked off. Job losses have given investors visibility into the severity of a US recession (#2), while massive policy responses from Washington, DC, and the Federal Reserve have helped shore up investor confidence and cushioned the economic blow (#5). The last signal, Signal #3, remains unchecked, with the S&P 500 now only 15% off of its February 19 high and no longer pricing in a recession.

For tactical investors, we believe patience is prudent here. We believe stocks have come too far, too fast and that a 5–10% pullback may be likely. Historically, patterns following prior bear market lows support this view.

For long-term investors, we continue to believe stocks may be more attractive than bonds at current valuations, and we would recommend overweight allocations to stocks, and a corresponding underweight to fixed income for suitable investors.

Our year-end 2020 fair value target range for the S&P 500 remains 3,150–3,200, less than 10% from April 17’s close at the low end of the range.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

S&P 1500 Index: A broad-based capitalization-weighted index of 1500 U.S. companies and is comprised of the S&P 400, S&P 500, and the S&P 600.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

© LPL Financial

Read more commentaries by LPL Financial