Curb Your Enthusiasm

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar is light and provides little post-COVID19 data. Continuing jobless claims takes on a new importance, and we may get some useful information from the components of the University of Michigan sentiment survey. 96 companies in the S&P 500 will report earnings. The depth of the employment decline and curtailment of normal activity has turned the national debate to how and when the restrictions will end. Investors, encouraged by these apparent plans, are trying to look beyond the recession. This is a good concept but represents a huge emotional swing from just a few weeks ago. Mr. Market is noted for emotion, but sound analysis is more important.

Investors, curb your enthusiasm.

I am not as grouchy as the character created by award winning Larry David, and certainly not as funny. I am concerned that investors are expecting too much, too fast.

Last Week Recap

In my last installment of WTWA, I emphasized the lack of data and intellectual rigor needed to answer the many important questions raised by investors. This was an accurate observation. Speculation replaced analysis for much of the week, resulting in items like these:

JPM: The Worst Might Be Over for Stocks.

While there are the requisite conditions to the forecast, the conclusion is that “most so-called risk assets (typically stocks) have seen their lows and should move higher in the second quarter.”

The Worst is Yet to Come, Says Gundlach, who expects the March low to be taken out, compares the current situation to the 1929 crash, and warns against a “V” recovery.

There was plenty of other discussion about which letter was the best economic description. Thanks to readers who played along with acronym suggestions!

The uninformed commentary led me to post about

The Irrelevance of Financial News and offer a few tips for discovering what is worth your attention.

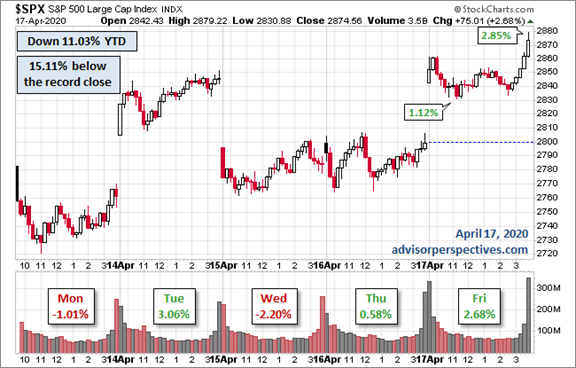

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski’s version, an excellent combination of the most important information.

The market gained 3.0% on the week. The trading range was 5.8%, a big reduction also reflected in actual volatility and implied volatility. You can monitor these along with historical comparisons in my weekly Indicator Snapshot (below).

Noteworthy

When my friend and former colleague Prof. Marty Finkler cites a member of my dissertation committee, Prof. John Kingdon, it attracts my attention. Both have appeared in prior posts, but the combination of their work shows what can happen when you think beyond the immediate crisis. I know that many readers will be ideologically opposed to the suggested policy change, but I urge you to read the well-developed argument and consider the evidence.

Replace Employer Health Insurance: If Not Now, When?

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators have always been a valuable part of my economic review. As we watch for signs of the eventual economic rebound, NDD’s three time frames will be especially helpful. Here is his (very wise) conclusion:

Both the nowcast and the short-term forecast remain awful. The long-term forecast, buoyed by lower interest rates and Fed money supply intervention improved to positive, laying the groundwork for the eventual recovery. In the meantime, unless a miracle treatment or vaccine appears, public policy decisions made at the very top in Washington, or failing that by the various consortiums of state governments that have formed, will determine the shape of the economic response to the pandemic.

The Good

Until we have more relevant data, I will just hit the highlights and provide some interpretation.

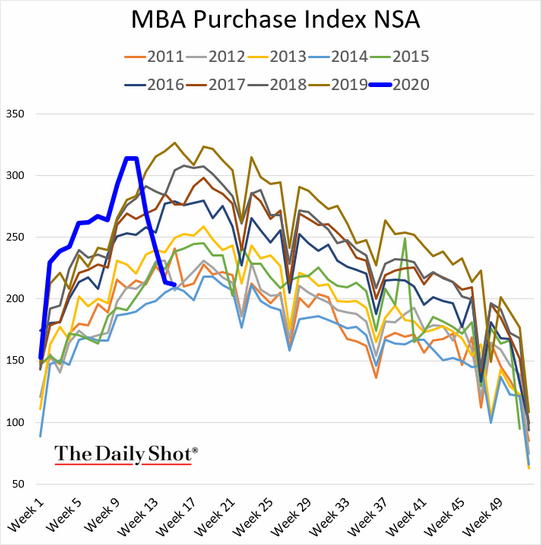

- Mortgage applications rebounded by 7.3% from the prior drop of 17.9%. The series is now tracking levels from some prior years rather than setting records.

- Building permits for March registered 1353K (SAAR), lower than February’s 1452K but beating expectations of 1297K.

The Bad

Everything else declined significantly. Some of the March data still does not reflect the entire coronavirus effect.

- Retail sales dropped 8.7% in March versus a 0.4% decline in February. I am not scoring this as “good” even though it beat expectations for a 10% decline. The expectations are not very meaningful.

- Industrial production declined 5.4% in March, compared to a 0.5% gain in February.

- Unemployment and revenue effects are hitting city budgets. (WSJ). (Chicago Tribune).

- Early earnings reports, covering 9% of the S&P 500, show companies reports missing expectations by 8.3%, although sales are up more than usual as is the revenue beat rate (70%). (FactSet). Brian Gilmartin tracks the decline in forward earnings

- Rail traffic continued to decline, over 20% on a year-over-year basis. (Steven Hansen).

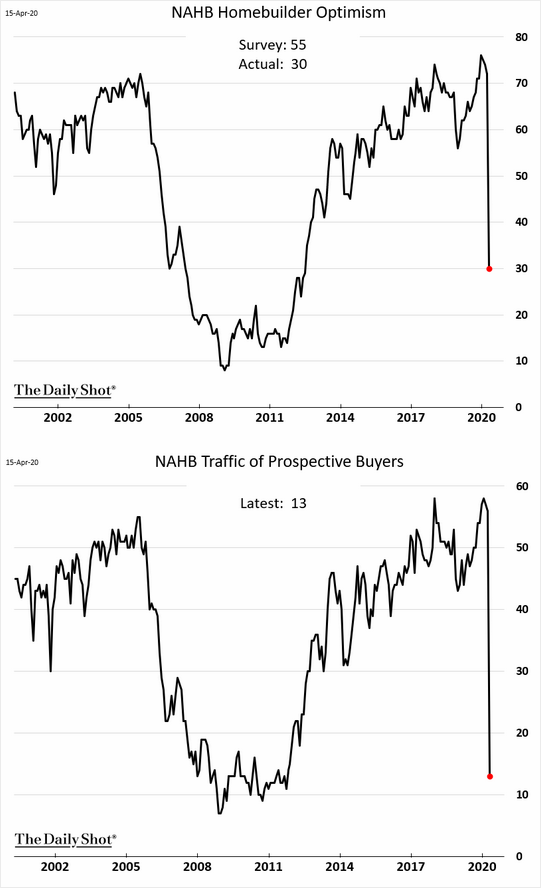

- The NAHB housing market index dropped to 30 in April, from March’s 72 and missing expectations of 57.

- The Beige Book, which provides information from all 12 Federal Reserve Districts for the FOMC meetings, describes a sharp and abrupt contraction in economic activity. Steven Hansen (GEI) has a helpful summary with quotes from each region.

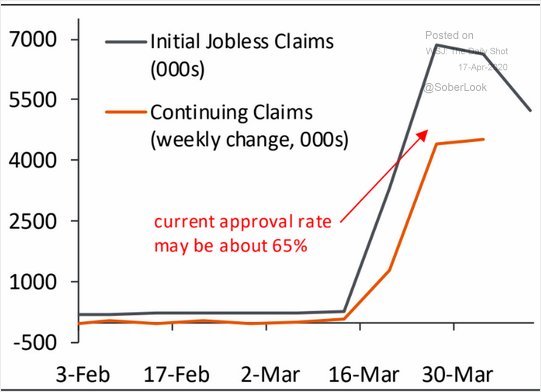

- Initial jobless claims were 5.245M, lower than the prior week’s 6.615M — another “less bad” number. It is probably better to switch our attention to –

- Continuing jobless claims (two weeks old) of 11.976M versus the prior week’s 7.446M.

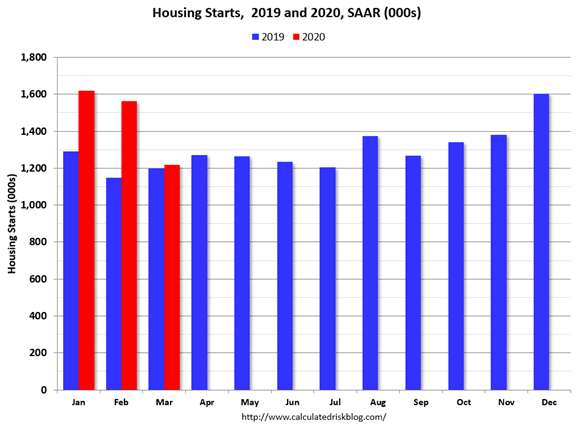

- Housing starts dropped to 1216K (SAAR) in March from February’s 1564K. Calculated Risk observes that the numbers are partially pre-crisis. The level is still a year-over-year increase. Since residential construction is deemed essential, it might not decline as much as other sectors.

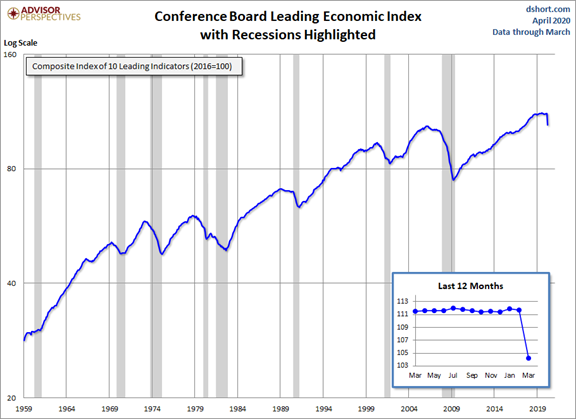

- Leading economic indicators declined 6.7%, the largest in its history (Jill Mislinski).

The Ugly

The need for speed leads to inefficiencies and waste. Trying to avoid this would leave no hope of meeting key deadlines.

U.S. Pays High Prices for Masks From Unproven Vendors in Coronavirus Fight

Stimulus cash is being sent to dead people. Their loved ones can probably keep it.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

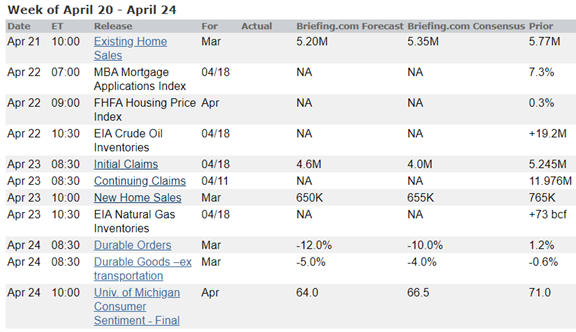

The Calendar

The economic calendar is light. There are several housing reports, but the time period covered does not completely reflect the COVID19 impact. I am especially interested in Michigan consumer sentiment and continuing unemployment claims.

96 companies in the S&P 500 will report earnings. We are all interested in the management outlook, but that is likely to be guarded.

Most important will be the ongoing stories tracking the pandemic and the prospects for reopening at least part of the economy.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

The economic calendar is not very interesting. Old reports are ignored. Current reports are read to see just how bad it is. Market participants want to look ahead so traditional economic analysis is not helpful. Earnings reports will provide some information, but it will be vague and sketchy.

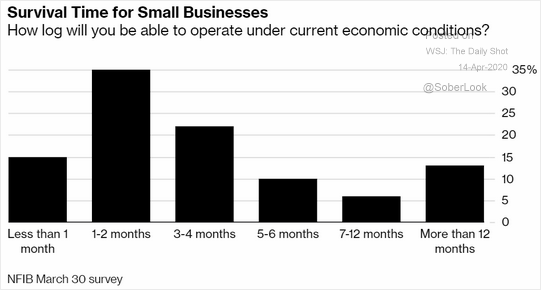

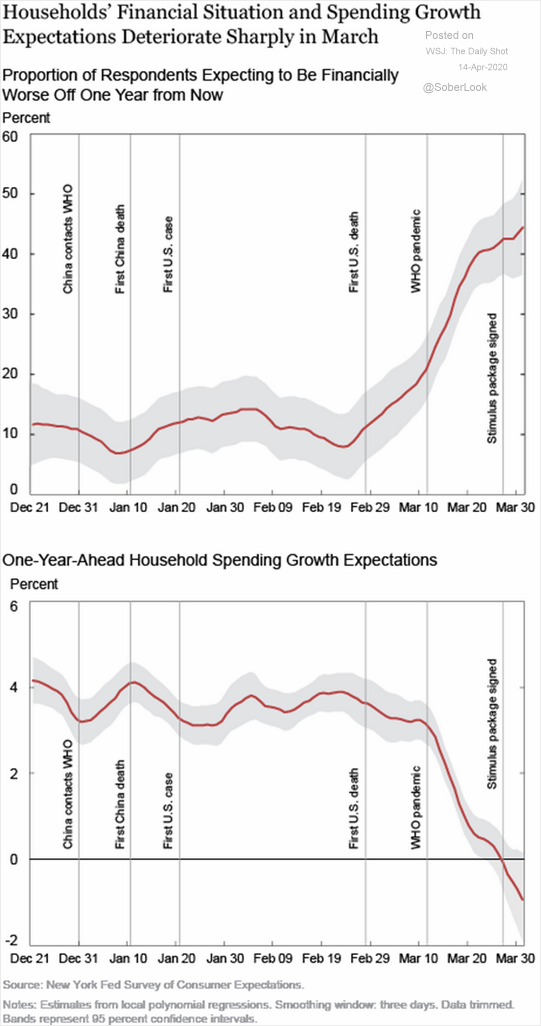

The economic stress is very great and gets worse as time passes. Many small businesses can last only for a month or two.

Households also are in poor shape. Since this affects spending, it has a ripple effect.

It is no wonder that everyone wants this to be over and is encouraged by optimistic statements about a return to normal. The emotional side of the markets is outracing the analytical side. Investors should be wondering if the message should be:

Curb Your Enthuisiasm!

Background

The return to normalcy has taken on a political cast. Many of our leaders (mostly Republicans) are looking at the facts right in front of them and conclude that the problem is over-stated. Several of my respected economic sources are describing the economic shutdown as a costly waste. The cost is definitely great. The consequences of the alternative are the result of controversial estimates.

The opponents of this viewpoint (mostly Democrats) place more emphasis on the pubic safety issue and have more confidence in the scientific analyses.

A third group is happy to step into the financial gap, but especially worried about mounting debt.

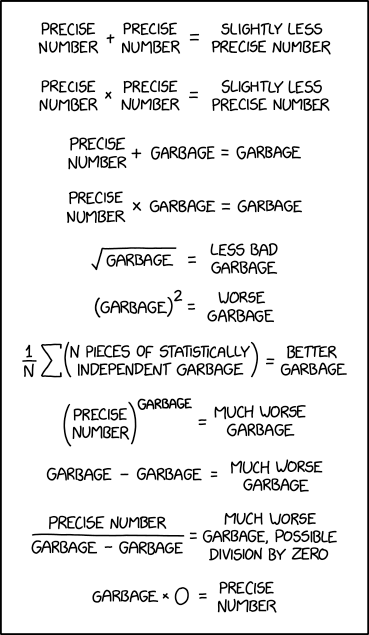

Weeks ago, I concluded that this was not a time to listen to everyone, treating all opinions as equal. Sticking with the tradition of my work, I am seeking out the best experts on several important questions. This means creating four different models and finding a way to link them together– Pandemic, Economy, Corporate Earnings, and only then, Stock Prices. There is no sound way to skip ahead in the chain. As is often the case, xkcd’s analysis is on point. Go to the original source to see the extra commentary when you mouse over the individual items, e.g. for the final precise number, “Garbage in, Garbage out” should not be taken to imply any sort of conservation law limiting of the amount of garbage produced.

We cannot make any solid conclusions with some estimate of the spread of the virus in the absence of any policy and the consequences of various alternatives. Each can and should have an error band. If we do not know much, at least we can try to be aware of that.

There are hundreds of articles on the themes each week. I am including a sample of the best on WTWA and a more extensive list on my blog. Eventually it will shed enough light to yield some specific conclusions. Meanwhile, please be patient!

This week’s focus is on the roadblocks to a quick return to normal.

Scientific developments

It all starts with counting the cases. Sources use different definitions and processes. Some of the reporting countries have been wildly inaccurate. Others have not done enough testing to provide meaningful results. (WSJ).

We cannot reopen without better data. This means at least two or three times the current testing level. (NBC). Only about 1% of the US population has been tested.

Without diagnostic testing on a massive scale, federal and state officials and private companies will lack a clear picture of who has been infected, who can safely return to work, how the virus is spreading and when stay-at-home orders can be eased, public health experts say.

Similar reports from Barron’s and Bloomberg.

Good news on the Gilead data on a trial for Remdesivir (STAT). While we all hunger for good news, this was not a controlled study and the patients did not represent the complete range of virus sufferers. The China study, which has a control arm, has not yet been reported. The reporters announcing the results from an internal University of Chicago video presentation write, “The same trials are being run concurrently at other institutions, and it’s impossible to determine the full study results with any certainty. Still, no other clinical data from the Gilead studies have been released to date, and excitement is high.”

A vaccine could take longer than investors expect (Barron’s). Some believe that the 18-month estimate is optimistic. The New York Times has a similarly pessimistic take based on interviews with 20 experts in public health, medicine, epidemiology, and history.

Resolve to Save Lives, a public health advocacy group run by Dr. Thomas R. Frieden, the former director of the C.D.C., has published detailed and strict criteria for when the economy can reopen and when it must be closed.

Reopening requires declining cases for 14 days, the tracing of 90 percent of contacts, an end to health care worker infections, recuperation places for mild cases and many other hard-to-reach goals.

And also…

Even though limited human trials of three candidates — two here and one in China — have already begun, Dr. Fauci has repeatedly said that any effort to make a vaccine will take at least a year to 18 months.

All the experts familiar with vaccine production agreed that even that timeline was optimistic. Dr. Paul Offit, a vaccinologist at the Children’s Hospital of Philadelphia, noted that the record is four years, for the mumps vaccine.

Economic news

The theme has shifted to various scenarios for reopening and the consequences of each. This is a standard economics approach, but the assumptions for the (wide-ranging) scenarios are often doubtful. Here are some leading examples.

Here are four criteria for determining the ability to reopen: hospital capacity, testing all with symptoms, monitoring of confirmed cases and contacts, and a sustained reduction in cases for at least 14 days.

About 37% of jobs can be done at home (NBER).

Ezra Klein (VOX) compares three different plans for reopening. “There’s one from the right-leaning American Enterprise Institute, the left-leaning Center for American Progress, Harvard University’s Safra Center for Ethics, and Nobel Prize-winning economist Paul Romer.”

He finds similarities in the approaches and raises important practical questions. All require monitoring. Should it be mass surveillance or mass testing? 22 million tests a day in one plan.

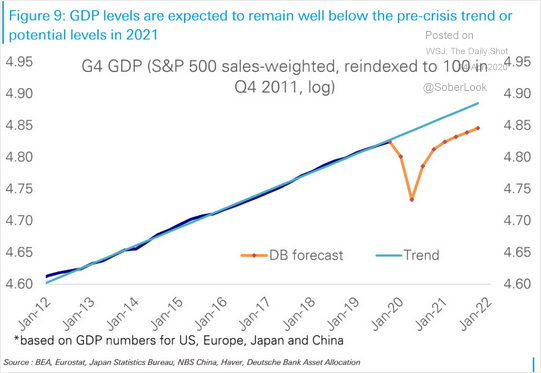

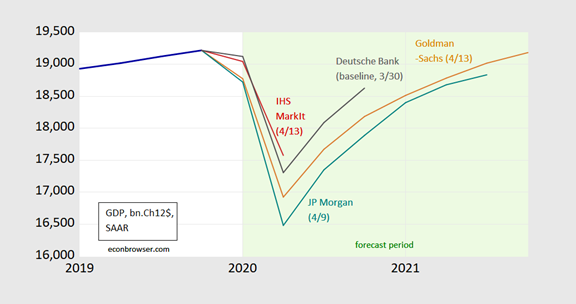

Gregory Mankiw sees two possible recovery paths. His interesting format is like the typical two-handed economist—an optimist and a pessimist.

Policy choices

When Ignorant Bureaucrats Make Your Decisions for You

considers decisions at a county level.

Job losses are putting pressure on the President (AP).

But conservative economist Steven Moore, a Trump ally, said there will be 30 million people out of work in the country if the economy doesn’t open back up soon. “And that is a catastrophic outcome for our country. Period,” he said.

The early push to sign up businesses is running into some hurdles (Washington Post).

Investors should be objective in evaluating this evidence before risking their money!

Stock Prices

Menzie Chinn addresses the outlook from various economic groups, citing the problems from the same factors I have been hammering on. It is reassuring to have some agreement from a strong source. I mention this is the “stock price” analysis is that we cannot come close to an estimate of earnings or stock prices without economic analysis.

Quant Corner and Risk Analysis

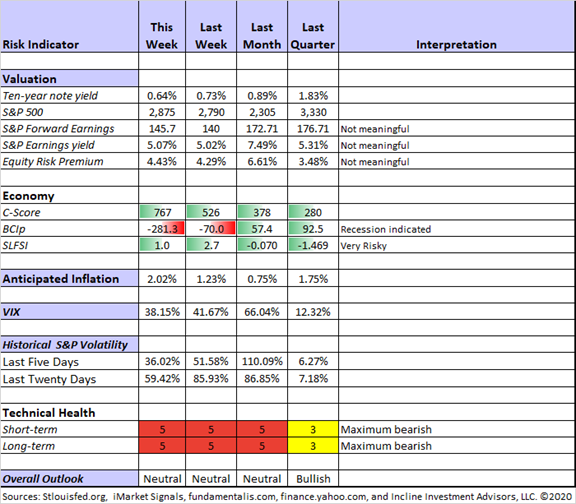

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

For a description of these sources, check here.

Both long-term and short-term technical indicators continued at the worst reading. The C-Score improved significantly. It will now have a new purpose. It put us on recession warning last May, but the confirming coincident indicators never pushed us beyond the tossup level. Conditions are sufficiently clear that I expect an “official” recession call from the NBER that will set the starting date some time this year. It will not be March, which will probably not the dating criteria. It takes a large and prolonged decine across the economy. It is certainly going to be a large decline, but prolonged will be a matter of judgement. We also might escape the traditional two negative quarters, say some economists. For our purposes, none of this really matters. We will reset our thinking and let the C-Score work at helping us forecast the next cycle bottom.

I am treating forward earnings and the resulting measures as not meaningful until we get more clarity.

I contine my rating of “Neutral” in the overall outlook for long-term investors. I am not trying to guess what will happen in the next week or two. As an investor, I would be neither a buyer nor a seller at this point.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

Georg Vrba: Business cycle indicator and market timing tools. Georg’s business cycle index continues its steep decline.

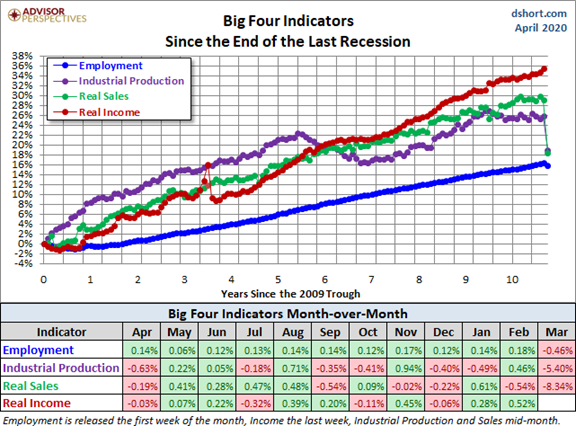

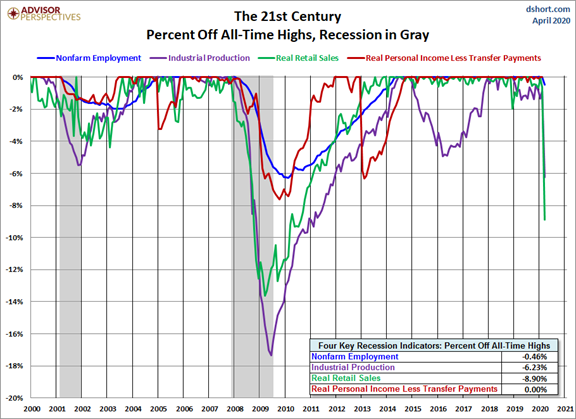

Doug Short and Jill Mislinski: Regular updating of an array of indicators. It is time for an update of the Big Four indicators used by the NBER for recession dating. We can also look at the size of the declines compared to the two last recessions.

Insight for Investors

Investors should understand and embrace volatility. They should join my delight in a well-documented list of worries. As the worries are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely.

Best of the Week

I am taking a different approach to this week’s selection of the “best.” Since I have been complaining about the irrelevance of most sources, I want to highlight approaches that deserve investor attention. This week I have three that are clear, accessible, and free. (Well one of them costs a few bucks).

- As a fan of Abnormal Returns from the site’s inception, I am a subscriber and daily reader. The Saturday post is the basis for “non-finance related stuff.” It is often an absorbing distraction from my Saturday writing. This week it is quite different, and clearly “finance stuff.” Tadas has included links to several different sectors, including autos, the environment, air travel, nature, and cities. Each of these topics forces the reader to think beyond the daily market stories and focus on major changes in various sectors and industries. This is exactly what we should be doing.

- I am a long-time reader of Barron’s. It is an establishment take and often bearish but includes a range of ideas. This week’s edition looked at the COVID19 impact on digital medicine, autos, steel, and banks. It is a start.

- Seeking Alpha has an important feature that is especially relevant right now. We want to know how companies feel about the pandemic and the effects on their business, but no one has time to listen to all of the calls. Here is the answer. Go to the author page for SA Transcripts. Click on the link for recent calls (upper right corner). You will now see a search box with fairly powerful capabilities. For starters, just enter “coronavirus.” You can also quickly find sectors or stocks that you own or are considering.

These are all valuable tools, and I wanted to highlight them.

Stock Ideas

Here are a few ideas to consider, keeping in mind the companies and sectors that will be viable on “the other side.”

Chuck Carnevale provides an excellent update on his analysis of Cardinal Health (CAH). There is an important lesson for income investors. He is not disappointed by the lower stock price since his purchase was based on the dividend and dividend growth potential. This is a key conclusion:

In contrast to the very nervous looking price action, Cardinal Health’s earnings have advanced nicely and so have their dividend. The orange line on the above graph depicts earnings, and the white line the dividend. Clearly, these are both more consistent and more predictable than trying to guess where the price might go over the short run.

And of course, be sure to watch the video!

Barron’s Andrew Bary analyzes three former United Technologies stocks. Now in different business, each shows promise. Did you know that about 1/3 of the 16 million elevators around the world are at least 20 years old? This is the sort of fact that helps to identify the stability of earnings.

Dividend Sensei analyzes the 13 Best Dividend Aristocrats. Near the end of the article you will find a discussion of criteria and tables of stocks that make it through the screening process. Some of these ideas will seem controversial, but I think they all are worth a look. I own several of them.

Rida Morwa likes Royal Dutch Shell (RDS.A). Valuation, balance sheet, and financial strength are all factors.

In a Pandemic, Pharma’s Strengths Emerge: Pipelines With Essential Drugs

Wells Fargo (WFC) gets a thumb-up from Stone Fox Capital. While profit was down, the company managed a profit in the face of building reserves against future losses. A key? Enough capital to thrive during the economic weakness.

The Great Rotation – Now the Great Reset

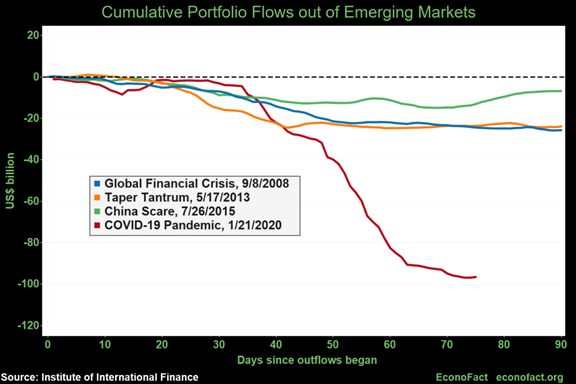

Emerging markets, on of the Great Rotation themes, are especially hard-hit by the coronavirus pandemic. Megan Greene and Michael Klein (Econofact) write as follows:

The worldwide coronavirus pandemic is likely to hit these economies harder than economies in richer countries. Not only are their public health systems under-resourced to deal with the outbreak, making the containment and treatment of the disease more difficult, but their economies are already being battered by the way in which the pandemic is impacting global demand and financial markets. The economic and financial vulnerabilities of these countries at the beginning of this year, as well as the way the economic effects of this pandemic are unfolding, suggest that many less-developed countries are facing a very rough road ahead.

Some are looking ahead to a rebound in value stocks. I am a believer, but that rotation will not come until after the recession. That is the reason to focus on The Great Reset first. Could It Be Value Stocks’ Time to Shine? One Long-Skeptical Strategist Thinks So.

Watch out for

Kirk Spano warns about 4 Oil Stocks About To Be Kicked Off The S&P 500. He explains the inclusion criteria and the implications for companies added or removed.

The Stanford Chemist warns about CLO equity funds, comparing the potential unfavorably with preferred shares. Bloomberg cites upcoming ratings cuts from Moody’s in their own warning about the CLO sector. “…as the underlying debt gets downgraded at a record pace.”

Final Thought

I am optimistic by nature. I expect a good resolution to this crisis. Eventually. For now, my enthusiasm is curbed. Here’s why.

- I have more confidence in the scientists on scientific issues. In addition, my own background in modeling and data analysis allows me to evaluate the work. (Mrs. OldProf is butting in to say, “Just like Peter Navarro?”) Well, not exactly! My working conclusion is that we are not yet close to meeting the conditions for a safe reopening of the economy.

-

- Modern DNA and RNA testing allows faster identification of candidates and easier design of alternative vaccines.

- The FDA will be somewhat more tolerant of studies and provide a fast track. Moderna’s (MRNA) candidate could be available for health workers in a few months. Various treatments will be offered on a compassionate use basis.

- Vaccine production can be expedited and increased. The history of past efforts is of little relevance.

- I am concerned about false starts. Moving too soon will revive the virus and represent a big setback. Some political leaders seem poised for this action. Those in the more cautious states cannot escape the effects.

- I expect a phased process that will slowly identify those who qualify as immune (a complex question), the safer parts of the country, and groups who are less susceptible.

- I expect a long-term application of (slightly relaxed) social distancing, along with temperature tests when you enter a large facility.

- I expect plenty of innovation with a new look to the economy. Sectors will rise and others will collapse. This should be the focus for long-term investors.

These are working conclusions, changing when I get more evidence. To summarize:

Be optimistic about science, cautious about politics, suspicious of economic forecasts, and open-minded about the future economy.

[Interested readers can get complimentary information about my most recent conclusions and papers by emailing info at inclineia dot com].

And by the way, Larry David favors social distancing (Deadline).

I basically want to address the idiots out there — and you know who you are,” David said in a video shared by the Office of the Governor of California. “You’re going out — I don’t know what you’re doing. You’re socializing too close, it’s not good.”

“You’re hurting old people like me — well, not me. I have nothing to do with you. I’ll never see you. But, you know, other — let’s say, other old people who might be your relatives! Who the hell knows.”

David went on to say that those who venture forth are “passing up” on a “fantastic opportunity, a once-in-a-lifetime opportunity” to “sit on the couch, and watch TV. I don’t know how you’re passing that up!” David said. “Well… maybe…’cause you’re not that bright. But here it is: go home! Watch TV! That’s my advice to you.

He concluded that those who have seen his show should know “nothing good ever happens going out of the house,” adding “it’s just trouble out there” and that it’s “not a good place to be.”

“So stay home and, you know, don’t see anyone except maybe if there’s a plumbing emergency, let the plumber in and then, you know, wipe everything down after he leaves… but that’s it. OK,” David concluded.

I’m more worried about

- Additional waves of the virus.

- Growing public pressure about reopening the economy too soon. Many governors will be in a tough position.

I’m less worried about

- Scary numbers, especially the GDP report. People forget that it is annualized, so a big number will seem much bigger. Investors can divide by four to get a rough estimate for the current quarter. Why is this the convention? Trends usually last for more than a year and it facilitates comparisons (Barron’s).

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits