Like much else, fixed income markets were dominated by the coronavirus pandemic in the first quarter. While the COVID-19 crisis is far from over, we expect that second-quarter bond market performance will be dominated as much by the path of central bank and government policies around the world as by the path of the coronavirus.

During the first quarter, as the coronavirus spread around the globe and containment efforts partly shut down economic activity, investors rushed into U.S. Treasuries at the expense of nearly every other asset class. Prices rose and yields fell sharply, with one- and three-month Treasury bill yields sinking below zero at times. In contrast, prices of many other bonds dropped. The riskier the bond, the larger the price drop.

Treasury bond returns were strong in Q1, but returns for riskier bonds declined

Source: Bloomberg. Q1 2020 returns are from 12/31/2019 through 3/31/2020, while 2019 returns are from 12/31/2018 through 12/31/2019. Returns assume reinvestment of interest and capital gains. See disclosures for indexes used. Indexes representing the investment types are: Treasury Bonds = Bloomberg Barclays U.S. Treasury Index; Core Bonds = Bloomberg Barclays U.S. Aggregate Index; Securitized Bonds = Bloomberg Barclays Securitized Bond Index; TIPS = Bloomberg Barclays U.S. Treasury Inflation-Protected Securities; Municipals = Bloomberg Barclays Municipal Bond Index; Int’l Developed Bonds (x-USD) = Bloomberg Barclays Global Aggregate ex-USD Bond Index; IG Corporate Bonds = Bloomberg Barclays U.S. Corporate Bond Index; Emerging Market Bonds = Bloomberg Barclays EM USD Aggregate Bond Index; Preferred Securities = ICE BofAML Fixed Rate Preferred Securities Index; Bank Loans = S&P/LSTA Leveraged Loan 100 Index; HY Corporate Bonds = Bloomberg Barclays VLI High Yield Index. Past performance is no guarantee of future results.

The mixed performance in the fixed income markets in Q1 underscores some important lessons for investors:

1. The benefits of holding Treasuries for diversification from stocks. Highly rated government bonds posted positive returns, providing a valuable offset to the 20% decline in the S&P 500® index. Longer-term Treasuries produced the largest returns, which has historically been true during stock market declines. In contrast, riskier, more aggressive investments, like high-yield and emerging-market bonds, tend to be correlated with stocks and therefore don’t provide as much diversification.

2. The value of liquidity in times of market stress. Steep price declines for preferred securities and municipal bonds were, to a large extent, the result of low liquidity. Because these are smaller markets driven by individual investors, when there are significant outflows from mutual funds, it can exaggerate the drop in prices.

3. The importance of a risk premium. When investing in more aggressive fixed income asset classes, investors should earn extra yield compared to Treasuries of similar maturity to compensate for the added risk. For example, investing in bonds with higher credit risk—that is, the risk that the borrower will default on the debt by failing to make required payments—means that the higher the risk, the more yield an investor should receive as compensation. Prior to the selloff, yields for most asset classes were very low relative to Treasuries and long-term averages. This offered little compensation to investors for the risk, resulting in steeper losses than might otherwise have been the case.

Q2: Coronavirus vs. central banks

So far, it appears that the efforts of the Federal Reserve, which recently increased its lending capacity by $2.3 trillion, including $500 billion to support state and local municipalities, along with the $2.2 trillion CARES Act, have helped to stabilize markets.

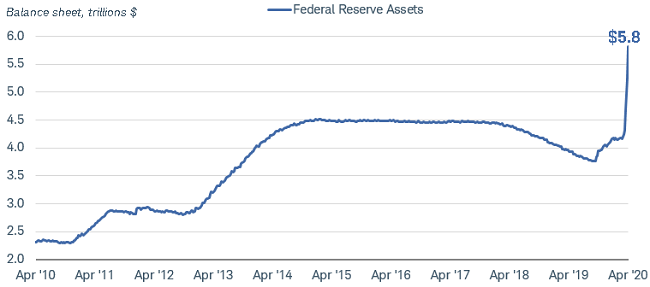

The Federal Reserve has been early and aggressive in its actions. In addition to lowering its benchmark federal funds rate to near zero, the Fed has taken several steps to help increase liquidity in financial markets and support the economy. These have included increasing its balance sheet to more than $5 trillion, introducing a special-purpose vehicle to buy investment-grade corporate bonds to unfreeze the credit markets, opening up swap lines with a wide range of central banks to increase the supply of dollars to the global economy, and easing restrictions on banks to free up lending capacity. All of these moves are intended to make sure the financial system is functioning and that credit is flowing to households and businesses.

The Federal Reserve has purchased securities, injecting liquidity into markets

Source: All Federal Reserve Banks: Total Assets, Trillions of Dollars, seasonally adjusted. Weekly data as of 4/1/2020.

Central banks in other major countries also have taken steps to cushion the blow from the spread of COVID-19. Most have cut interest rates, increased their bond-buying programs and widened the types of assets they will hold. These moves should mean that financial markets function more smoothly. When combined with expansive fiscal policies, they can help cushion the downturn in the global economy.

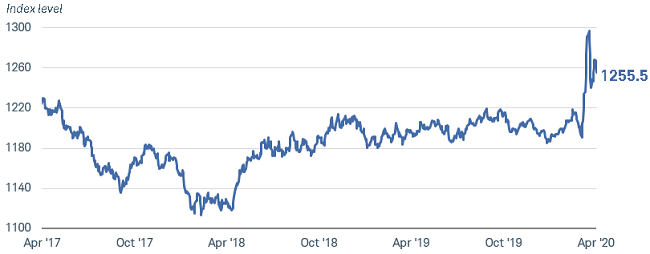

In determining whether these moves are successful, one of the important indicators we’re watching is the U.S. dollar. Strong demand for the dollar has taken it to record highs in the past month. A strong dollar is a sign of tightening financial conditions, and tends to weigh on global growth—especially in emerging-market countries that have high levels of U.S. dollar-denominated debt. With the Fed easing policy aggressively, the dollar has eased off its highs, but it is still elevated.

The value of the U.S. dollar has eased a bit, but it is still high

Source: Bloomberg. Bloomberg U.S. Dollar Index (BBDXY). Daily data as of 4/7/2020. Past performance is no guarantee of future results.

We don’t see these moves as an “all-clear” signal for investors to take on significantly more risk. The COVID-19 pandemic is forcing countries to halt economic and social activity on a scale we’ve never seen before. The depth of the unfolding downturn in the global economy is expected to be far deeper than most previous recessions. All governments and central banks can do is push against this force with the tools available. Consequently, we are still cautious, even though we expect volatility to be somewhat lower than at the peak levels of mid-March.

As fiscal and monetary policy work to limit some of the downside risk, interest rates are likely to remain very low across the yield curve. Short-term Treasury bill yields dipped below zero on safe-haven buying in March and are likely to remain near zero for at least a year, but more likely two years. Federal Reserve Chair Jerome Powell indicated that the range for the fed funds rate will be held near zero until the Fed reaches its mandate of full employment and inflation near the 2% target, and it’s confident that the economy has weathered the recent events. Neither of the mandates are likely to be met any time soon given the magnitude of the recession in front of us.

While we don’t anticipate that the fed funds rate will be set in negative territory, there is a risk that intermediate-term yields could dip below zero in a scenario of a very deep recession and investor flight to safety. However, the Treasury will be issuing record amounts of Treasury bills and bonds to pay for the sharp increase in government spending to stimulate the economy. With the budget deficit projected to expand by $2 trillion in 2020, there will a lot of supply for the market to absorb. Barring another round of panic buying, we see Treasury yields staying low – but positive.

Where to find potential value

Despite the grim economic outlook, we do see the potential for investors to find pockets of opportunity in the fixed income markets. With yields for many bonds rising relative to Treasuries, the entry point for investing is better than it was at the beginning of the year. However, there are tradeoffs. There is likely to be more credit risk, more interest rate risk due to longer maturities, and/or more liquidity risk. We suggest when looking to add more interest income to a portfolio outside of core bonds, that investors keep the allocation small because of the potential for wide price swings.

Here are some segments of the market where we see potential value:

1. Investment-grade municipal bonds

Yields have risen relative to Treasuries in the municipal bond market. The yield ratio of munis to bonds for 10-year maturities (MOB spread) is well above its five-year average, making valuation more attractive than it has been for many months. We suggest focusing on higher-rated issuers – those rated AA or above. Generally these municipalities are in a better financial position to manage through an economic downturn. We would also focus on those that are less reliant on sales taxes, as the shuttering of businesses is causing sales tax revenue to drop in most places.

2. Investment-grade corporate bonds

Volatility has settled down in the investment-grade corporate bond market, although yield spreads relative to Treasuries remain elevated. We continue to suggest investors stay in bonds rated A or above. While the new Fed facilities meant to buy investment-grade corporate bonds (and exchange-traded funds) should help provide support for the market, we still believe many downgrades are likely. The large amount of BBB rated bonds still poses a risk to the market as we expect the number of “fallen angels”—formerly investment-grade issuers whose credit rating has been downgraded to speculative grade—to increase.

3. Preferred securities

Prices for preferred securities have fallen sharply since the onset of the COVID-19 crisis. Low liquidity and uncertainty about how the curtailment in economic activity would affect issuers contributed to the steep price declines. We believe for investors looking for higher income, preferreds may present an opportunity at current prices.

There is the risk of dividend suspensions, especially in non-rated preferreds. That risk appears lower for large U.S. financial institutions, however, because most are well capitalized.

In general, allocations to more-aggressive income investments should be made cautiously. Volatility is likely to remain high for quite a while. We suggesting keeping the size of any allocation to riskier investments small. Make sure you have a long time horizon and the capacity to ride out the ups and downs of the market, which means having enough liquidity elsewhere in the portfolio if you need access to funds in the short run.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market or economic conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Tax-exempt bonds are not necessarily suitable for all investors. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and Schwab does not guarantee its accuracy. Tax-exempt income may be subject to the alternative minimum tax. Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

Preferred securities are often callable, meaning the issuing company may redeem the security at a certain price after a certain date. Such call features may affect yield. Preferred securities generally have lower credit ratings and a lower claim to assets than the issuer's individual bonds. Like bonds, prices of preferred securities tend to move inversely with interest rates, so they are subject to increased loss of principal during periods of rising interest rates. Investment value will fluctuate, and preferred securities, when sold before maturity, may be worth more or less than original cost. Preferred securities are subject to various other risks including changes in interest rates and credit quality, default risks, market valuations, liquidity, prepayments, early redemption, deferral risk, corporate events, tax ramifications, and other factors.

Investing involves risk including loss of principal. International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Treasury Inflation Protected Securities (TIPS) are inflation-linked securities issued by the US Government whose principal value is adjusted periodically in accordance with the rise and fall in the inflation rate. Thus, the dividend amount payable is also impacted by variations in the inflation rate, as it is based upon the principal value of the bond. It may fluctuate up or down. Repayment at maturity is guaranteed by the US Government and may be adjusted for inflation to become the greater of the original face amount at issuance or that face amount plus an adjustment for inflation.

Correlation is a statistical measure of how two investments have historically moved in relation to each other, and ranges from -1 to +1. A correlation of 1 indicates a perfect positive correlation, while a correlation of -1 indicates a perfect negative correlation. A correlation of zero means the assets are not correlated.

Currencies are speculative, very volatile and are not suitable for all investors.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(0420-0F75)

© Charles Schwab & Co.

© Charles Schwab

More Volatility/Downside Protection Topics >