Navigating the Maze of Models

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsOnce again, no one cares about the economic calendar. There are a few items with recent data – jobless claims, mortgage applications, and Michigan sentiment – but most reports are old news. Everyone is focused on the increase in coronavirus cases and deaths. There are plenty of predictions, each based on model from a reputable source. The variation is wide.

The question that needs an answer:

How can we navigate the maze of models?

Last Week Recap

In my last installment of WTWA, two weeks ago, I interrupted my vacation plans to provide some perspective on the need for clarity in determining what information was both relevant and important. Sadly, we have seen little of that. The headline-driven market gets plenty of fresh material every day. There is little information on how to figure out what current market prices reflect, but plenty of unsupported guesses about what will happen next.

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski’s version, an excellent combination of key variables.

The market lost 2.0% on the week, erasing the early end-of quarter gains. The trading range was 7.9% — very high and generally unpredictable. You can monitor volatility, implied volatility, and historical comparisons in my weekly Indicator Snapshot in the Quant Corner below.

Personal Note

Allocating my time during my semi-retirement (!?) is a challenge. I want to focus my time on the most important information for the individual investor. A challenge is that the most popular investment sources are not very good at figuring out what is important. They want to run eye-catching stories. They want to provide investment advice on specific stocks. Those are not the most helpful themes at this juncture.

How can investment writers and publishers do more? How about stories like honing investment skill and critical thinking. There is no other way to interpret today’s investment news. Finding the right sources to improve your knowledge would also be helpful.

These are not topics of great interest since most want shortcuts to success, not knowledge. It is a personal frustration since the bias against investment education limits my “reach.” The best I can do is to write what I think is important and publish it on my own blog. My first installment using this approach applied critical thinking to the seriously flawed analysis of a big-time interviewee on CNBC. I am trying to craft a good approach for such pieces, so I am especially eager to get comments and suggestions.

Noteworthy

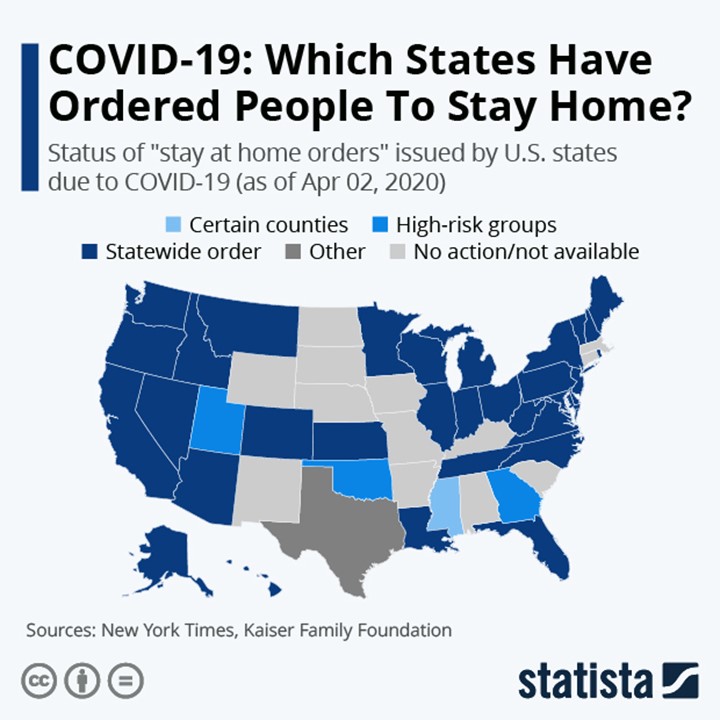

These are the states that have issued “stay at home” orders. (Statista)

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators have always been a valuable part of my economic review. Eventually our focus will be on a turn in the economy. This source will be helpful for that purpose, as it was in identifying potential weaknesses going into the recession. In the short leading and coincident indicators, “the bottom fell out.” Long leader indicators are very slightly positive. Here is NDD’s overall conclusion:

We know that over the next month or two, conditions are going to be awful. Whether there will be a V-shaped rebound or whether lasting damage is done to the economy depends most of all on political decisions in Washington that result in enough public health progress being made – or not – to create the conditions for the near-nationwide lockdown to end soon; whether short-term severe disruption becomes a credit and liquidity crisis, and whether a wage deflationary spiral begins to take root.

The Good

Until we have more relevant data, I will just hit the highlights and provide some interpretation. The pre-COVID19 reports continued to show strength. These included housing data and consumer confidence. The ISM manufacturing report registered 49.1, beating expectations of 43.3, but this was mostly because of an inventory build. This stockpiling is unlikely to continue.

For the moment, consumer confidence remains at historically high levels.

The Bad

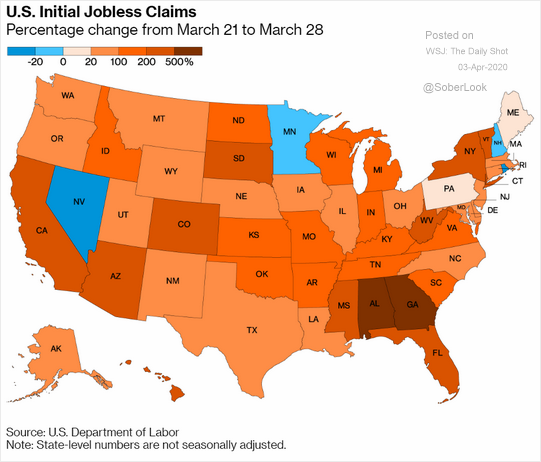

Employment news was dreadful. Initial jobless claims totaled ten million over the last two weeks. The number is understated because of the difficulty in state employment offices in handling the applications. This is an interesting state-by-state look at the spike in jobless claims.

Payroll employment dropped a net of over 700K jobs, breaking a 113-month streak of gains. This report is also an understatement because the survey period was in mid-March. We can expect much worse data next month.

The unemployment rate moved to 4.4%, also not an adequate reflection of reality. This will also be much worse when the survey period more accurately reflects conditions. The conventional U3 rate will not be as useful as those showing detached workers. U3 requires that people are actively seeking work, an unlikely condition in current circumstances.

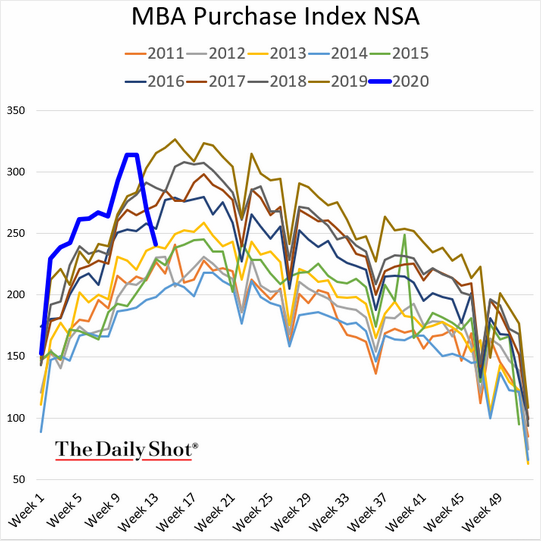

Mortgage applications are now tracking a lower path for the year.

The Ugly

Program implementation SNAFU’s. (Yes, I taught that class, too. The one about implementation – SNAFU’s were just a part of it). You can have a great idea but getting it to work is another matter. An example I often use is a professional football play. It requires many repetitions in practice before game day. Even then there are errors. You can have a great idea, but you can’t just draw the play in the dirt and expect it to work. (Mrs. OldProf likes this example).

Complex organizations provide the same challenges for first-time ideas. Here are a few we see right now.

- Individual checks are going to be delayed for many people without established banks and tax records.

- The small business loan program is so popular that it was overwhelmed on the first day. Banks complained that the regulations and instructions were inadequate. The best case is now a delay of a week or so. And the program may be only 15% of the needed size. (NPR)

- Getting companies to shift production to medical necessities. Manufacturing requires plans, tooling, experienced workers, delivery logistics, and many other items. It can be done, but not instantly.

- Adjusting production and supply chains to match shifts in demand. (Will Oremus, Marker). The aggregate demand for toilet paper has not changed, but it is now needed at home, not in a commercial setting. The products, paper mills, and supply chains are different for the two markets. (This explains why a local restaurant is offering a roll of toilet paper along with a take-out dinner!)

- Establishing criteria and procedures for rapidly constructed temporary hospital facilities. The beds are there, but the patient qualification was an early bottleneck.

It is difficult to do big things quickly, even when the need is urgent. Small Businesses Will Be Crucial to Recovery. Many Can’t Survive More Than 6 Months.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

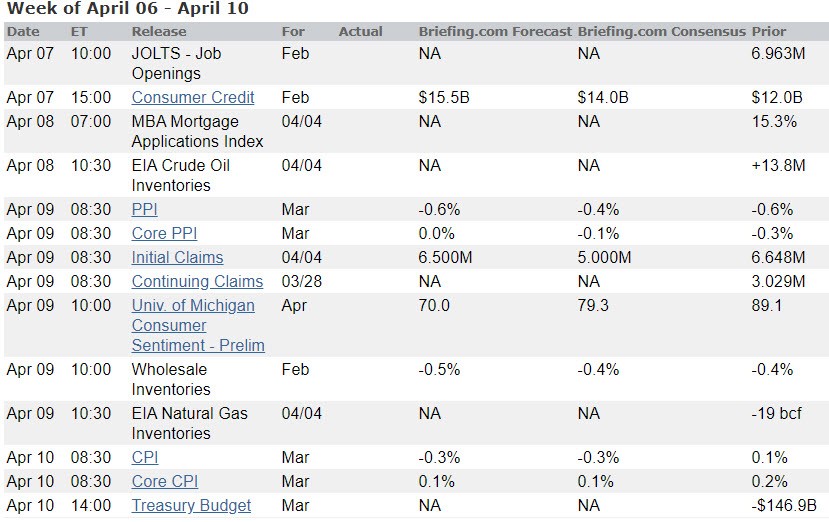

The Calendar

The economic calendar once again features “old news” from the pre-virus period. I will keep running the calendar, but (as I have been emphasizing for weeks) we must remain conscious of the collection dates for data rather than the release dates. The relevant items this week are initial jobless claims, mortgage applications, and Michigan sentiment.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

Once again, the economic data is mostly from the pre-virus period. Few will find the news to be interesting. The spread of COVID19 and the responses rightly command our attention. The news is confusing. The possible outcomes cover a wide range. They all seem to come from reputable sources. What should we believe?

The key question to be answered is:

How should we navigate the maze of models?

Don’t expect to see this explained on TV! I’ll do my best to shed some light, but I cannot manage it in one post.

Background

Modeling has a poor reputation in financial media and the blogosphere. A typical discussion finds a single point estimate that proved wrong and scoffs at it. The author then might take one line of the George Box quote out of context to emphasize modeling error. Not surprisingly these assessments come from those who never studied the subject or built any models themselves. When your business model does not include this expertise, it is natural to treat it as irrelevant.

The current circumstances require a dramatic change. Financial firms and advisors without the ability to interpret models, much less develop them, are going to be several steps behind the action. It has become an essential skill in analyzing the current data – at least for advisors who plan to help clients with adjustments.

As one who studied the topic fifty years ago, taught the class to graduate courses at a Big Ten university, and built hundreds of models, I know what to look for. My challenge is to present the essence of the problem in the space of a WTWA post. I’ll do my best.

The most important aspects of modeling are the following, none of which is a single point forecast of an outcome!

- Carefully reviewing all of the factors involved. Decide whether something is relevant and whether it fits into the model. This keeps you focused on the right problems.

- Making reasonable assumptions for each factor. This requires study.

- Providing the ability to adjust assumptions to test sensitivity of the results. If an input has little effect, you can give it less study. If it has a big impact, you know where to focus.

Briefly put, a good model forces you to think about the problem in a disciplined fashion, consider the relevant assumptions, and identify the range of possible outcomes.

Part of the current confusion is that amateurs seize upon a “model result” without considering any of the relevant elements. It is no wonder that model developers are amazed at finding themselves quoted concerning very specific predictions about fatalities.

Investment Opportunities

Investors want to know at least three things:

- Where is the market bottom?

- Is this a good time to start buying?

- Which stocks are most attractive.

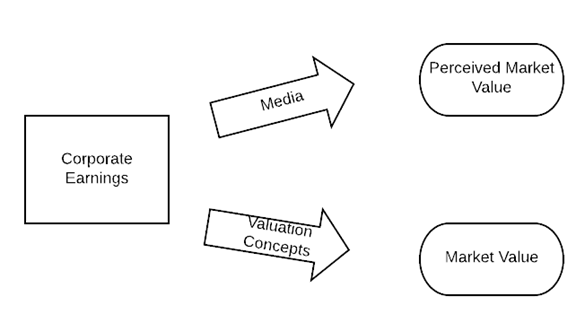

Here is the causal model followed by some comments.

Even better knowledge about corporate earnings will not provide a complete answer. Many will be skeptical of this news. Media interpretation will influence the perceived growth and quality of earnings. This will determine the perceived market value.

The intrinsic market value is somewhat more objective, but still subject to one’s choice of valuation model.

Overall corporate earnings information is not really helpful in stock selection, although earnings reports may help to identify survivors.

Economic Rebound

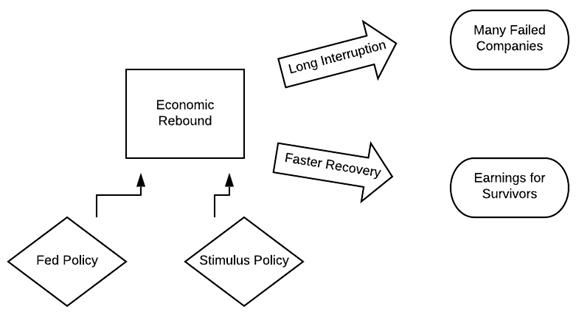

The needed information about corporate earnings depends upon the economic rebound. My chart of this causal model again includes only the basics.

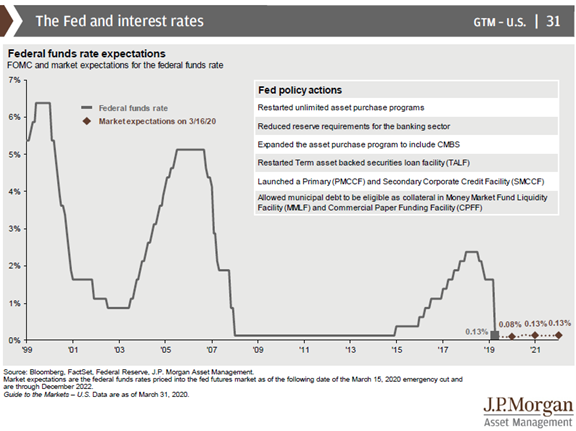

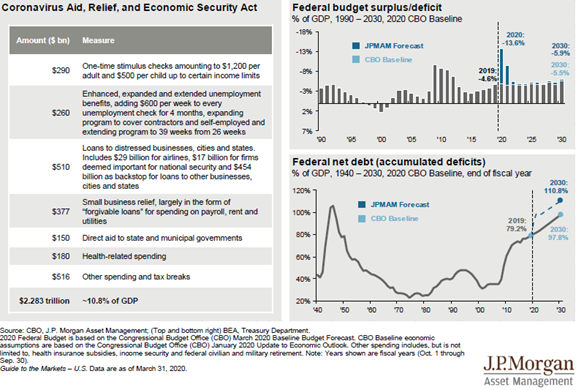

The arrows dealing with the length of a recovery (and the time until it starts) are a consequence of the severity and duration of the pandemic. This diagram illustrates the impact of mitigating policies. These are generally underweighted. Many, and especially those in finance, are skeptical of government intervention. The actions include big numbers but not very tangible examples, except for program confusion. The crisis itself is much more dramatic. The government stimulus will take time to implement and more time to show up in the data. Some companies will fail along the way. J.P Morgan’s newest guide to the markets has a nice summary of government actions. Keep in mind that most thought the Fed interest rate policy changes left them with “no ammunition.” Many were skeptical that the government could rise above partisanship to reach a stimulus agreement.

And there could be more.

Trump Calls for New $2 Trillion Infrastructure Bill

The Pandemic Effect

Determining the pandemic effects requires information of at least five types:

-

How intense will the peak effect be? (Cases, fatalities, pace of the spread). The impact can be limited by adding contact tracing to the current lockdown requirements. How US can keep death toll far below the 100,000 projection

-

How long before the peak arrives? Testing delays have foiled our ability to estimate this. Test makers are moving fast, but the coronavirus may be moving faster

and also The coronavirus outbreak won’t peak in every state at once. And how to improve testing ‘We’re racing against the clock’: Researchers test wearables as an early warning system for Covid-19.

- How successful will social distancing prove to be? NYT on the importance. And Time Magazine regular updates on flattening the curve. And also see this estimate of peak resource use.

- When will a successful treatment and/or vaccine be found? COVID-19: 3 Reasons For Some Optimism

Johnson & Johnson Says Its Coronavirus Vaccine Could Be Ready Early Next Year

- Can a safe and effective return to work plan be developed? How Covid-19 immunity testing can help people get back to work. This is not an off-the-cuff pick of a target date, but a constructive plan.

Modeling these characteristics is an incredible challenge. This is the main reason for the wide variation in model results. Math modellers say lack of data makes curve flattening difficult to predict. This will improve with more testing data. None of the key parameters can be estimated without that information.

Modeling Summary

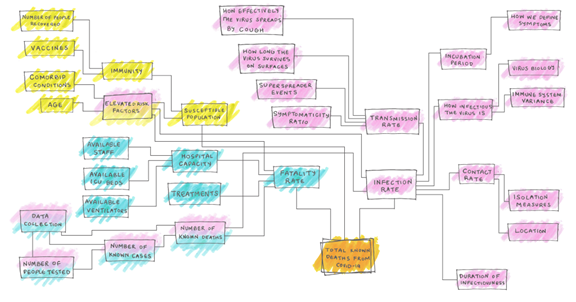

I have tried to organize and explain the key questions and problems. FiveThirtyEight takes up the question: Why It’s So Freaking Hard To Make A Good COVID-19 Model .

This is a first-rate analysis of the final step in my analysis, including several more relevant problems. If you read it carefully you will understand the complexity of the problem. The article begins with a simple causal model and then adds in the problems and ambiguities. There is a series of charts, each of which adds a problem. Here is the final version:

And here is the conclusion:

Think of it like making a pie. If you have a normal recipe, you can do it pretty easily and expect a predictable result that makes sense. But if the recipe contains instructions like “add three to 15 chopped apples, or steaks, or brussels sprouts, depending on what you have on hand” … well, that’s going to affect how tasty this pie is, isn’t it? You can make assumptions about the correct ingredients and their quantity. But those are assumptions — not absolute facts. And if you make too many assumptions in your pie-baking process, you might very well end up with something entirely different than what you were meant to be making. And you wouldn’t necessarily know you got it wrong.

Over the next few months, you are going to see many different predictions about COVID-19 outcomes. They won’t all agree. But just because they’re based on assumptions doesn’t mean they’re worthless.

“All models are wrong, it’s striving to make them less wrong and useful in the moment,” Weir said.

We’re hungry, so somebody has to do some baking. But be sure to ask what ingredients went into that pie and in what quantities.

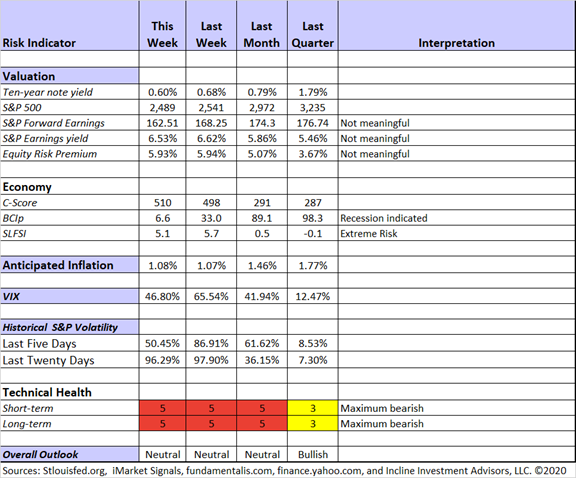

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

Both long-term and short-term technical indicators continued at the lowest reading. The C-Score improved slightly, but it will now be used for a different purpose. It put us on recession warning last May, but the confirming coincident indicators never pushed us beyond the tossup level. Conditions are sufficiently clear that I expect an “official” recession call from the NBER that will set the starting date some time this year. It will not be March, since the March data do not really meet the dating criteria. It takes a large and prolonged decine across the economy. It is certainly going to be a large decline, but prolonged will be a matter of judgement. We also might escape the traditional two negative quarters, say some economists. For our purposes, none of this really matters. We will reset our thinking and let the C-Score work at helping us forecast the next cycle bottom.

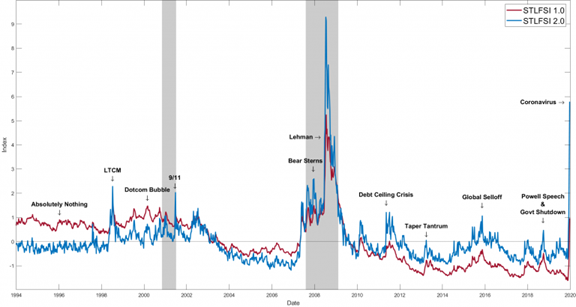

The St. Louis Fed’s Financial Stress Index

has been changed to Version 2.0. The effect is shown in the chart below. It can be annoying when a method is altered, but it can be necessary to capture real-world changes. The chart shows that the new indicator, while still in the safe zone, would have been less comforting than the former version over the last few years.

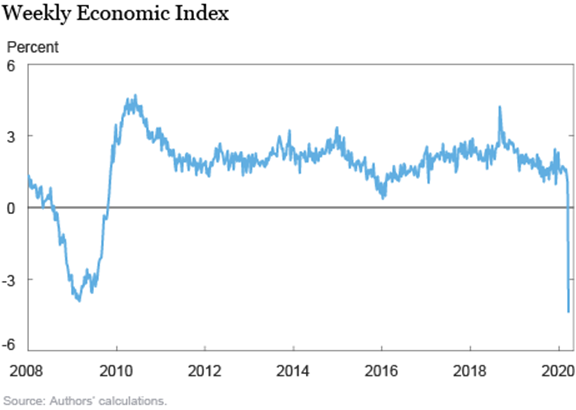

I am considering the addition of the NY Fed’s Weekly Economic Index (WEI) to the Indicator Snapshot. It combines sound methodology with frequent data. This is not like the SLFSI.

Economists are well-practiced at assessing real activity based on familiar aggregate time series, like the unemployment rate, industrial production, or GDP growth. However, these series represent monthly or quarterly averages of economic conditions, and are only available at a considerable lag, after the month or quarter ends. When the economy hits sudden headwinds, like the COVID-19 pandemic, conditions can evolve rapidly. How can we monitor the high-frequency evolution of the economy in “real time”?

To address this challenge, we compute a Weekly Economic Index (WEI) to measure real economic activity at a weekly frequency. Few of the government agency data releases macroeconomists often work with are available at weekly or higher frequency. While financial data, like stock market prices and interest rates, are available at high frequency, we are particularly interested in real activity, not financial conditions. For our purpose, most weekly series come from private sources like industry groups, which collect data for the use of their members, or from commercial polling companies.

Here is a current look at the index.

I am treating forward earnings and the resulting measures as not meaningful until we get more clarity. (Barron’s, Brian Gilmartin).

I contine my rating of “Neutral” in the overall outlook since I would be neither a buyer nor a seller at this point.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

Doug Short and Jill Mislinski: Regular updating of an array of indicators.

Georg Vrba: Business cycle indicator and market timing tools. The most recent update of Georg’s business cycle index has now signaled the recession, as has his unemployment rate method.

Insight for Investors

Investors should understand and embrace volatility. They should join my delight in a well-documented list of worries. As the worries are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely.

Best of the Week

As occasionally happens, there is a tie in my recommendation for “best of the week.” Both provide important ideas about valuing stocks at this crucial juncture.

Chuck Carnevale does his usual combination of stock ideas with a course in how to analyze them. He starts with a screen for high-quality dividend growth stocks that have sound credit ratings and low long-term debt. Choosing five examples from the original list of 20, he shows how to use the price and earnings history to analyze the company characteristics and attractive entry points. Importantly, he includes two less attractive examples in the group of five. To appreciate this work, you must take the time to watch the video provided.

In a note to his users, Chuck points out another important feature of the FAST Graphs tool. He first explains the fast and frequent updates for the database. He elaborates as follows:

However, we must also realistically recognize that the estimate data we are currently seeing was likely, or at least for the most part, issued prior to the coronavirus crisis. Clearly, there is going to be near term to intermediate term fallout as a result of the mandated shutdown of most businesses and industries. We would further suggest that no one, and certainly this applies to analysts, can currently provide any clear guidance or information as to what the extent of the economic damage might be. However, we are confident that analysts everywhere are doing their best to update their forecasts as quickly as possible.

We should also recognize that until the situation clarifies, we should not be making decisions based on estimates that were made prior to the crisis. However, FAST Graphs’ subscribers do have the option of utilizing the “Custom” calculator where they can manually input their own estimates. Understanding that many of you may not feel confident that you can make accurate forecasts, you at least can apply rough estimates that would allow you to run different “what if” scenarios.

This is excellent for those of us who want to build in different earnings assumptions and see if the stock is still attractive.

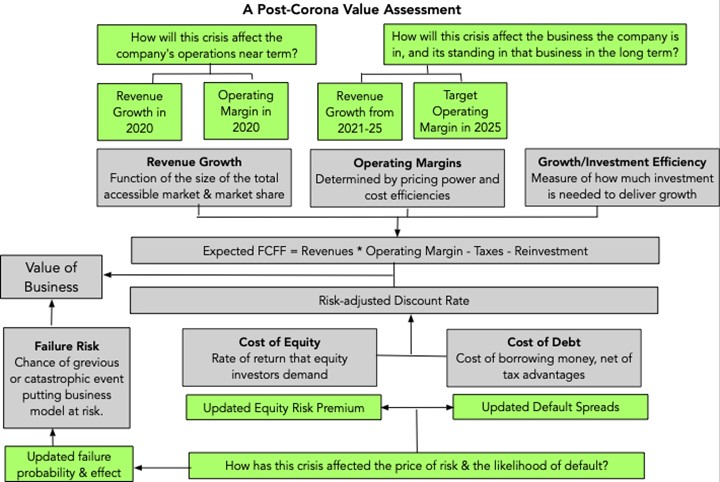

The second winner this week is from Prof. Aswath Damodaran, who graciously shares the tools used in his Stern School of Business MBA classes. I recommend his entire “Viral Market Meltdown” series, but my focus today is on part V, Back to Basics. After an overview of current prices and events, he writes:

While many investors have put their valuation tools away, using the argument that there is too much uncertainty now to even try, I will argue that this is exactly the time to go back to basics and try valuing companies, uncertainty notwithstanding.

The Dark Side beckons..

If your concept of valuation is downloading last year’s financials for a company into a spread sheet and then using historical growth rates, with some mean reversion thrown in, to forecast future numbers, you are probably feeling lost right now, and with good reason. Specifically, the last six weeks have upended almost all of the assumptions, explicit and implicit, that justified this practice.

Historical data may be recent, but it is already dated: For most companies globally, the most recent financial statements are for 2019, and in calendar time, these financials are only a few weeks old. As the global economy shuts down, though, the one thing we know with certainty is that the revenues and earnings numbers reported in those recent financial statements are almost useless, a reflection of a different economic setting. The same can be said about equity risk premiums and default spreads, as I am painfully aware, since the numbers that I updated on January 1, 2020, are so completely out of sync with where the market is today that I plan to do a full update at the end of today. (March 31, 2020).

This year will deliver bad news: There is almost no doubt that 2020 will be a bad year for all companies, with the key questions being how much of a drop in revenues companies will see this year, and how this will translate into earnings shocks. It is true that there are a handful of companies, like Zoom, Slack and Instacart, to name just three, that may actually benefit from the global quarantine, but they are the exceptions.

Survival has become a central question: The magnitude of the shock to corporate bottom lines and the speed with which it has happened has put companies at risk, leaving debt-burdened and young companies exposed to default and distress. While some of the largest may get help from governments to make it through this crisis, their smaller and lower-profile peers may have to shut down or let themselves be acquired.

The post-virus economy will be different from the pre-crisis version: Every major crisis creates changes in business environment, regulations and business models that reshapes the economy and resets competitive games, setting the stage for new winners and losers. Thus, for some companies, the bad news on revenues and earnings this year may be a precursor to superior operating performance in the post-virus economy, as their competition fades.

Here is a chart of his method for a post-Corona valuation.

He invites all of us to use a valuation spreadsheet he developed. You should also watch his video guide for using the spreadsheet.

This is an excellent tool. While it may seem intimidating on your first try, it gets easier. As with the Carnevale approach, you are able to adjust crucial assumptions to fit your expectations for a range of outcomes.

Stock Ideas

Here are a few ideas to consider, but do not skip my recommended analytical process!

Yelp: Lockdown Survivor

notes that there is a large decline in current business. Stone Fox Capital suggests that the low estimates for 2021 are too aggressive given the potential for vaccines and treatments. They note the Starbucks rebound “…in the Hubei Province about two months after closing the province is a strong indication of how quickly the retail sector can rebound. Where Yelp has a leg up on surviving the economic lockdown is a strong balance sheet. The company had $434 million in cash at the end of December.”

The same source provides a similar analysis of American Airlines Group (AAL).

What is the big difference between the valuation of housing REITs and mortgage REITs? This is important if you are interested in either market.

Double Dividend Stocks likes Dupont (DD) because of new management and guidance and the attractive opportunity from selling near-term options. [Jeff: That is one of our positions.]

And for contrast, here is a recommendation I don’t care for. See if you can figure out why. Twitter Has Suffered Enough. It’s Time to Buy the Stock, 2 Analysts Say.

The Great Rotation – Now the Great Reset

The current recession scare has halted (postponed?) the value portion of the Great Rotation. It has also affected small cap stocks which are generally perceived as more vulnerable financially.

The open-minded investor will change course when there is vital new information. My current best idea is to emphasize a Great Reset, a focus on the best sectors and stocks for the post-pandemic era. I will elaborate on these ideas as they make it through my testing process

Watch out for

Zoom Video (ZM). Stone Fox Capital suggests that the stock’s current price reflects “a virtual only world where users never return to normal trends.”

Exchange traded notes and possible liquidations. (CNBC).

Your dividend program since S&P 500 Dividends Will Fall 25% This Year, Analysts Say.

Final Thought

This is a special time and requires special care.

What Will Not Work

- Did you think you had an “all weather” portfolio? You probably missed a chance to lighten up as recession odds increased. This will limit your chances to take advantage of the eventual rebound. Rebalancing your allocation will help, especially if you target purchases with the right stocks.

- ETFs. Many stocks will not survive. Do you want to own them? An ETF combines the bad with the good.

- Market timing the bottom. Someone will guess right of course, but we don’t know who it will be.

What Will Work

- Will the company survive? Verify the balance sheet, cash flow, and the Altman Z score.

- Use an earnings model like FAST Graphs. Check the valuation sensitivity of a near-term earnings hit.

- Use a revenue model like Prof. Damodaran’s to check out discounted FCF. This will provide another sensitivity test using different inputs and assumptions.

This means doing your homework on each stock. It takes time but avoids costly mistakes and finds the best opportunities. If you are sheltering in place you have time to do some extra study of stock valuation!

What Other Actions Might Investors Consider

Following the principle of taking what the market is giving us, the most attractive trade is selling options and collecting the highly elevated premium. I do this through my Enhanced Yield program where we begin with a stock that meets our tests and then sell a short-dated out of the money call. This is geared to income investors.

Another attractive approach is selling cash-secured puts. This is good for investors who want to establish a position in a stock and are not fussy about the exact timing.

I have been using these approaches for many years, but it is nice to see Barron’s join in with Dividends Are Under Siege. Here’s How to Rebuild the Income That Came From Them.

Do not waste time on investment news. It is only a distraction.

Mrs. OldProf is turning off the news, reading good books, playing Words with Friends, and watching some movies. It is a good plan, once you have finished your daily stock homework!

[I hope readers will consider writing to “info at inclineia dot com”. Get information on our Enhanced Yield income program, dependable even in declining markets. Join our Great Reset email list for progress and ideas on that topic. Or request a portfolio consultation. The stakes are higher right now and professional help is quite affordable.]

I’m more worried about

- Increased fighting in existing hot spots. The world has enough worries.

- Adequate numbers of respirators and protective equipment. Life should not be based upon which hospital got a shipment. Workers on the front lines deserve protection.

I’m less worried about

- Another Great Depression or Great Recession. In a recent update, JP Morgan’s Dr. David Kelly cited a crucial difference. This time we know there will be an end. It may not come until someone has an effective vaccine, but the economic weakness will not drag on indefinitely with no end in sight. I also like his fall, stall, and surge description for market action.

- Whether we are in a bear market and/or when it started. This dichotomy matters much less than the fundamental economic and earnings outlook.

- Scary economic forecasts. GDP estimates are annualized, so a Q2 decline of 10% shows up as 40%. Unlike past economic crises, we are seeing the impacts very quickly. Like Dr. Kelly, I do not expect a prolonged continuation of a decline.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits