Coronavirus Risks for U.S. Consumers and India

summary

- Contagion and Consumers

- India’s Battle to Maintain Economic Health

Comedian George Carlin once quipped that “Consumption is the new national pastime.” Well, if he was right, no one is having much fun these days. Mandated closures and social distancing have had an immediate and dramatic effect on American spending, which is critical to global economic growth. Substantial fiscal and monetary policy support should help many consumers survive this difficult interval without lasting financial damage. But for some consumers, any income disruption may be too much to bear.

Consumers have been the focus of several stimulus bills passed by Congress this year. The Families First Coronavirus Response Act, ratified March 18, includes job protections and paid leave for certain workers battling COVID-19 or tending to family members, including parents looking after children whose schools have closed. The Act also increases funding for unemployment programs and lowered the eligibility requirements for food assistance. These measures provide only basic relief for people in greatest need.

The larger Coronavirus Aid, Relief, and Economic Security (CARES) Act, signed into law March 27, went much further. Under the Act, all taxpayers with earnings up to $75,000 (doubled for a household filing jointly) on their most recently filed tax returns will receive a payment of $1,200. Each child in the household earns an additional $500. Higher earners receive a means-tested partial payment, with the incentive scaling down to zero for individuals earning over $99,000.

The prospect of receiving cash is enticing, but the payments will only go so far. The one-time checks will only cover one month of rent or mortgage payments for households in most parts of the U.S. The payments are meant only to help households carry on through a temporary suspension of economic activity, not something more permanent. And it may take several months for all of the payments to be distributed.

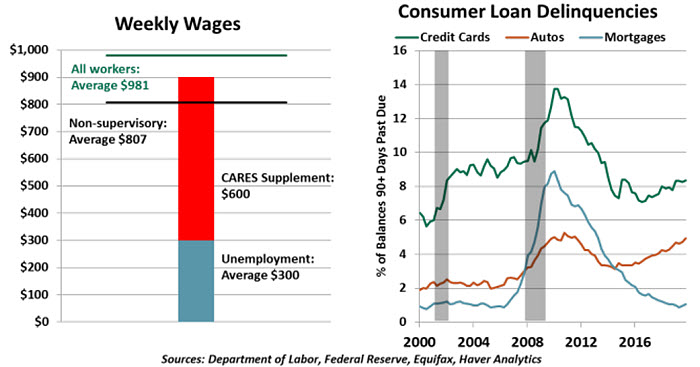

Sidelined workers will also benefit from CARES’ enhancement to unemployment insurance (UI) benefits. UI is not a generous system, by design: Small payouts keep employers’ insurance premiums lower and encourage unemployed workers to seek work aggressively. Benefits vary depending on the worker’s income and state of residence, but average around $300 per week. The CARES supplement of $600 per month brings UI payments up to a more typical level of income.

“Larger unemployment benefits will be a big help to a growing number of workers.”

CARES also extends UI to populations that never had the benefit before, including self-employed and gig workers. The Bureau of Labor Statistics estimates there were 1.6 million contingent workers in the U.S. as of 2017, comprising about 1% of the workforce. Any of them who cannot work due to COVID-19’s effects now qualify for benefits and the CARES supplement. The Act also supplements wages for workers whose hours have been reduced due to the COVID-19 slowdown.

The CARES Act also provides money for small business loans, which will be forgiven if the loan is used to sustain payrolls. This benefit may have been too little, too late; astonishing levels of initial unemployment claims show that layoffs have taken hold. Employers may choose to terminate workers in order to let them collect more generous UI, rather than continue paying them and then applying for debt forgiveness.

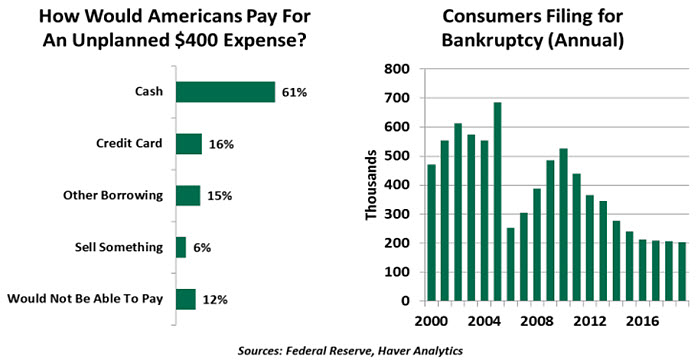

Whether paid through wages or UI, many households need every dollar that comes in. Too many Americans live on the margin: an estimated 39% of them would be unable to pay for an unplanned $400 expense, even during good times. An abrupt loss of income will hurt these workers badly.

U.S. consumers are entering the coming recession with high debt burdens. In good times, employed consumers have both the confidence to borrow and the income to handle it. Mortgage balances on one-to-four family homes are nearly equal to their 2007 peak. Auto loans and leases, credit card balances, student loans and unsecured personal loans grew for years. With unemployment rising rapidly, however, indebtedness may become much more difficult to handle. And the credit models that lenders rely on may struggle to appreciate increasing risk.

Strain on consumer credit quality will challenge the banks that underwrite the credit. At this time, there is no national policy of debt forbearance: The U.S. Federal Reserve issued guidance that “financial institutions should work constructively with borrowers and other customers in affected communities.” Some banks are offering piecemeal accommodations for borrowers affected by COVID-19. But these policies are temporary and will grant no reprieves for routine expenses like rent and insurance.

The rapid downturn we are experiencing today will do minimal damage if it is short-lived. Until recently, the consensus had been that the U.S. will experience a recession that is sharp, but brief. Based on COVID-19’s patterns of contagion in other countries that have dealt with an outbreak, it is reasonable to assume the spread of new cases will decline, allowing commerce to recover relatively quickly.

“Unemployment rates rise quickly and fall gradually.”

But recent readings from the U.S. job market have been sobering, and raise the possibility of a deeper downturn and a slower recovery. Cessation of local lockdown policies could take some time, and consumers will then need time to overcome their own safety concerns and resume normal patterns of activity. Many households’ budgets will be stretched, limiting how quickly consumption and employment will rebound. Impaired American consumption is a global problem: it hurts both domestic producers and those in every country that exports to the U.S.

The stimulus measures implemented to date are largely aligned with expectations for a temporary setback. (For example, the UI supplement in the CARES Act is funded only through July 31.) Steps taken so far are not designed to be a lasting survival mechanism for businesses or individuals. Conversations in Washington have consequently shifted to “Phase 4” of fiscal stimulus, which would provide more enduring support. But new legislation will take time.

Though the recent global financial crisis ended in 2009, employment was slow to recover and bankruptcies were elevated for years afterward. If we want to avoid a similar outcome, we will need more support for American consumption. And that is no laughing matter.