A Pundit’s Paradise – Anyone Can Play

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWe have a full economic calendar. Only the FOMC decision will get major market attention. Initial jobless claims provide a post-virus look at the job market. Housing data remains interesting.

Despite this, the media focus will remain on the coronavirus crisis. In the absence of any solid economic data, and in the spirit of the new populism, everyone’s opinion is equal. Stating the obvious passes for great wisdom. Any deeper look seems silly.

It is what I call:

A Pundit’s Paradise. Anyone can play.

Last Week Recap

In my last installment of WTWA, I predicted little attention to the economic news. That expectation was certainly accurate! I emphasized the need for investors to decide upon and emphasize the time frame that fit their purposes. I also pooh-poohed [OldProf technical term for “scorned”] the ongoing efforts to “explain” market moves.

More such stories dominated the week. Markets had a knee-jerk and bogus reaction to falling oil prices. The increase in coronavirus cases, even though expected, was treated as some sort of inverse stock futures contract. I confess to some frustration. I have been accurate on the spread of the virus, the analysis of economic effects, and the government policy response. It would be nice to predict how the market would react to expected news. As I say every week, “Good luck with that.”

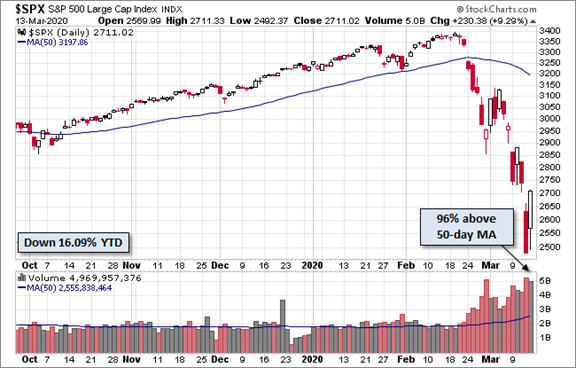

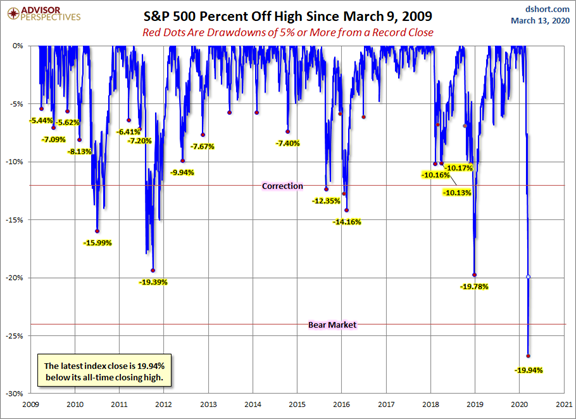

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski’s version, an excellent combination of key variables.

The market lost 8.8% on the week and the trading range was a mammoth 16.3%. Monday reflected a gap lower from Friday’s close of 2972. This reflected the start of the oil price war. The Friday end-of-day rally came with news of policy action from the Administration and the hope for fiscal stimulus. Every day of the week included moves of 1000 points or more in the DJIA. You can monitor volatility, implied volatility, and historical comparisons in my weekly Indicator Snapshot in the Quant Corner below.

For additional context, here are charts showing the decline since mid-February and the total drawdown.

See the full post for even more great charts and analysis.

Personal Note

My long-planned vacation for the next two weekends has been canceled along with many other events. The North American Bridge Championships attract players from around the world, put a lot of older folks in close quarters, and involves sharing cards from table to table. It was a disappointing but wise decision. Local tournaments and clubs have followed suit. For the first time in my life there is no live competitive bridge, although one can play online.

This does not reduce my need for some time off. Nothing distracts me as much as the demand for focus from competing against the best players in the world. I’ll catch up on some good books, I guess. I always monitor positions and client accounts but writing WTWA is a massive addition of work. If things calm down a little, I plan to dial back for the next week or two. I hope readers will understand. [Mrs. OldProf approves this message.]

Noteworthy

The modeling effort to show how we might mitigate coronavirus effects has a very interesting backstory. Please read to the very end and look at the simple GIF which explains a crucial point.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators are a valuable part of my economic review. His approach divides indicators into three time frames. Currently, the long leading indicators remain positive, but the short-term forecast has dropped to neutral. The nowcast declined to negative. NDD warns, “To reiterate, I expect the news to outrun even the high frequency indicators.”

The Good

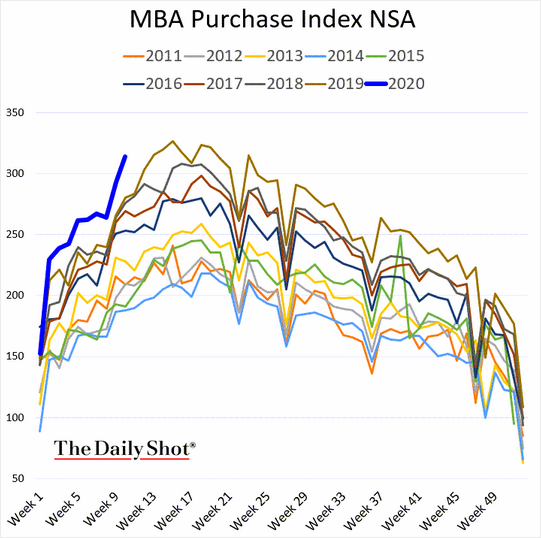

- Mortgage applications increased by 55.4% versus the prior week’s 15.%.

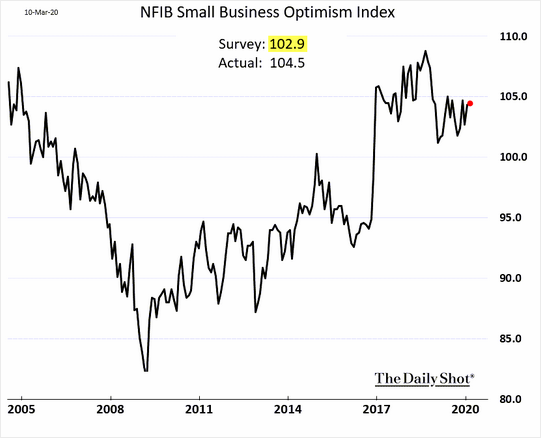

- NFIB Small Business Optimism remained high and beat expectations. Most of the punditry expects it to move lower.

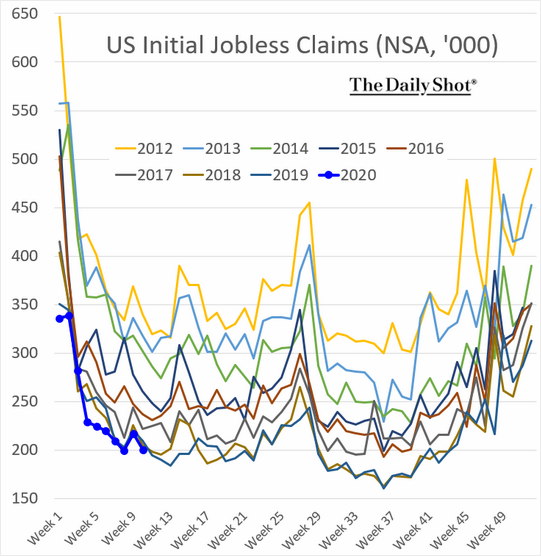

- Initial jobless claims of 211K beat expectations of 218K and was a slight improvement over last week’s (downwardly revised) 215K. This is the most current economic report, in the range of coronavirus major effects. The WSJ reports on the significance of the data.

- Inflation data from the PPI (-0.6%) missed expectations of a decline of 0.2%. I see low inflation as relieving pressure on the Fed. The CPI was in line with expectations.

- Movie Box Office reports are also weekly. So far, so good reports Calculated Risk. AMC is reporting a plan for sanitizing after each showing, limiting the audience, and separating seats. Gross sales are tracking near the minimum of the last four years, and some blockbusters have been delayed.

The Bad

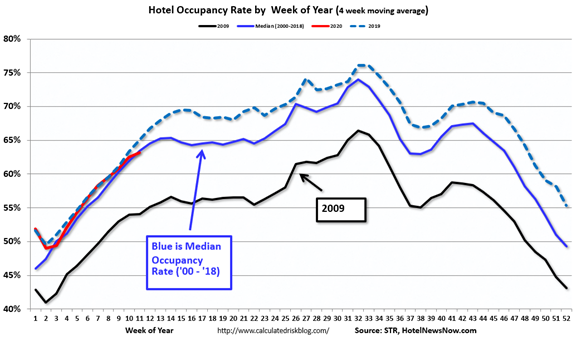

- Hotel occupancy is down -7.3% YoY. (Calculated Risk)

- University of Michigan sentiment, another up-to-date indicator, registered 95.9 in line with expectations but lower than last month’s 101. I am scoring it as “bad” for this report because of the decline. It bears close watching as a possible signal of consumer weakness.

The Ugly

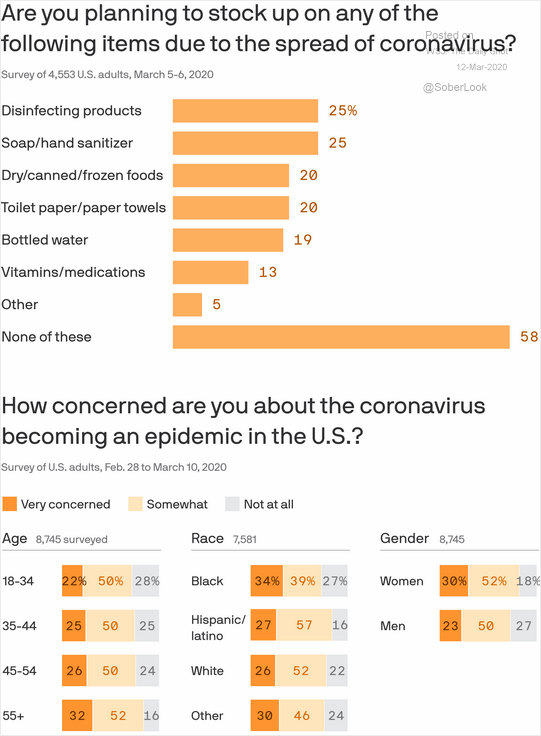

Price gouging. Or is it “retail arbitrage?” He Has 17,700 Bottles of Hand Sanitizer and nowhere to Sell Them.

And a survey confirming the stories most have already heard. Panic?

In my never-ending quest for accuracy and verification, I made a late-afternoon trip to Safeway. Many shelves were empty and checkout lines were long. One possible indicator is that they were out of bags! You could check out with loose items in your cart or pay a dollar for a bag. I told the cashier that I had a few bags to return in my car and I would be happy to sell them for fifty cents. She replied that this would take the involvement of a manager, but those in line behind me were amused at this effort at “retail arbitrage.” (See Ugly below).

An Important Comment on Data Interpretation

Regular reporting of data releases makes it easy to forget that the “news” is often weeks old. When events are breaking fast and markets responding to headlines, this is important to keep in mind. We may still be two months away, or even longer, before we begin to get data which we can treat as important. I plan to continue the economic reports and emphasize those that have more recent data.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

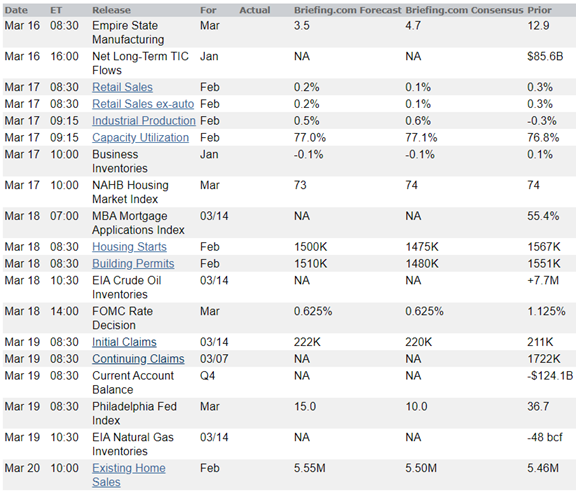

The economic calendar is important, but once again few reports will get any attention. The FOMC rate decision on Wednesday is the highlight, with market expectations calling for at least a 50 bps reduction (and perhaps much more) in addition to the emergency intra-meeting cut. Housing starts and building permits are important for those of us interested in housing. Retail sales and industrial production will be part of the history, but not reflecting the coronavirus panic. Initial jobless claims are the most current read on labor and reflect the week that is the basis for next month’s employment report.

Some will view the regional Fed surveys as fresh data, but the survey periods may not be late enough to be meaningful.

The audience-free Democratic debate on Sunday night and the subsequent Tuesday primaries are important, but pobably not market-moving. FedSpeak is in the quiet period until after the meeting but expect Fed-related tweets to continue unabated.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

Given the backward-looking nature of most economic reports, few will care about the results. The FOMC decision is the feature for the week. As always, Fed decisions invite pundit speculation.

In the absence of data, all opinions are equal. It is the era of populism, so actual knowledge, experience, or training is irrelevant.

It is a Pundit’s Paradise, where anyone can play!

Background

In each of the last few posts I have provided a framework for interpreting events and breaking news. I am trying to adhere to that educational mission, but it is a challenge. Even committed investors really want the reassurance of Mr. Market.

I will not emphasize any of the posts of those who “called the crash.” At some point I will do a review of the underlying wisdom, but not just yet. I am emphasizing what I see as most important for investors – right now! It may be difficult to recognize a time of opportunity amidst the market turmoil, but that is when the rewards are the greatest.

As I did last week, I’ll discuss current knowledge about the virus, the economic effects, the market reactions, and the policy response. I hope I can provide a few suggestions about how investors of different stripes might use this information.

Virus spread

-

NYTThe Hill

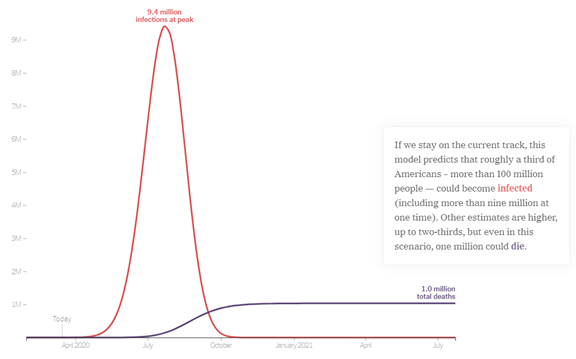

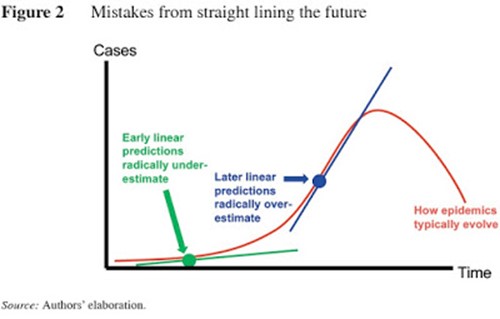

The C.D.C.’s scenarios were depicted in terms of percentages of the population. Translated into absolute numbers by independent experts using simple models of how viruses spread, the worst-case figures would be staggering if no actions were taken to slow transmission.

Between 160 million and 214 million people in the United States could be infected over the course of the epidemic, according to one projection. That could last months or even over a year, with infections concentrated in shorter periods, staggered across time in different communities, experts said. As many as 200,000 to 1.7 million people could die.

These estimates do not include the various responses to the threat.

“When people change their behavior,” said Lauren Gardner, an associate professor at the Johns Hopkins Whiting School of Engineering who models epidemics, “those model parameters are no longer applicable,” so short-term forecasts are likely to be more accurate. “There is a lot of room for improvement if we act appropriately.”

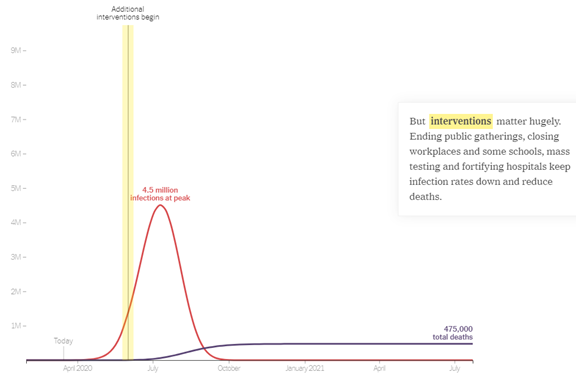

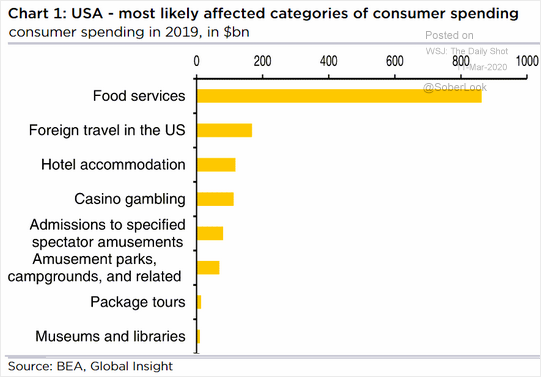

- Mitigating factors. If you read only one article on the potential coronavirus effects, it should be this one: How Much Worse the Coronavirus Could Get, in Charts. The story illustrates the best features of modeling, providing a rough idea of the impact of key variables. Here is one case.

Interventions matter – a lot!

The start time for interventions is also very important. I cannot do justice to this tool without the interactive features. Please try adjusting the factors yourself. The bottom line is that aggressive testing and response is the right track, even if the initial delay was costly.

Economic Effect

-

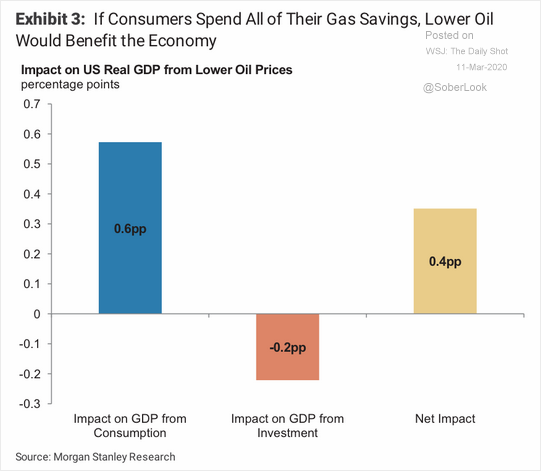

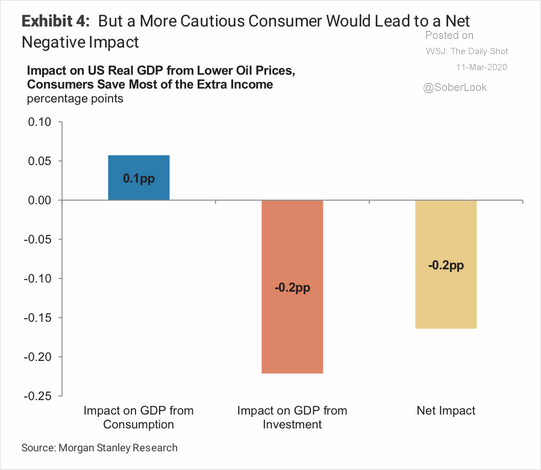

This analysis is wrong on several counts. The price weakness on this occasion has far more to do with expanded supply that lower demand (although that contributes). Many more oil companies are hedged against falling prices. Banks that provided the hedges do hedging of their own. The break-even prices are lower than before. But most importantly, these reports scoff at the effect of lower gas prices. It does depend somewhat on whether people spend the savings. Even if they do not, the GDP effect is only about 0.2%.

-

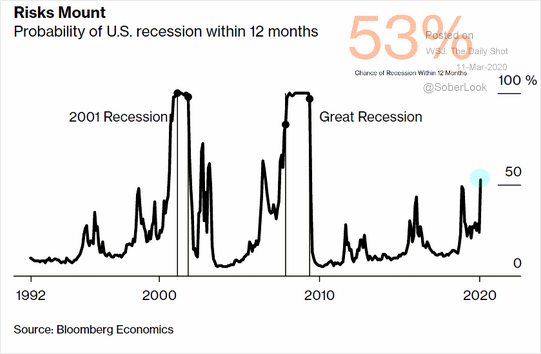

- Recession odds. The average person I speak with believes we are already in a recession or that it is inevitable later this year. By contrast the economic forecasters are more in the 50-50 range, where I have been for some months. This is important because stocks are already pricing in a recession which may or may not occur. More on that in today’s Final Thought.

Timothy Taylor shows the possible range of economic effects, explaining the variables involved.

Policy

- New information. One of the biggest weaknesses in Wall Street analysts is giving short shrift to government actions. It is so easy to use the Fed as a punching bag and critique the actions of leadership. As a result, most conclude that government policies will not help. We now have signs of Fed support for the financial system, Trump Administration policy releasing emergency funds, and initiatives for some kind of overall stimulus. It will make a difference which we saw in an initial reaction on Friday.

- Markets have been disappointed with the official policy responses, including both the Fed rate cut and President Trump’s evening speech. Joe Weisenthal explains that it is more than a “Fed put.” The early US response has been confused and politicized. The slow implementation of testing will prove costly. The dismantling of agencies that were skilled in providing support and predictive analytics was a serious mistake. The debate over economic stimulus demands compromise – and fast. The President’s Friday announcement was on the right track but included some diversions. Cutting off flights from the UK, which he said was contemplated, might add to the blindside effect of shutting down trips from Europe. The reality is that the virus is already in the US and is spreading. The suggestion of adding to the Strategic Petroleum Reserve was also a surprise. Let’s see if that affects oil markets.

Stock Prices

- New information. There really was little relevant new information last week. My take is that the oil price effect was exaggerated. The “signal” from the bond market, which I disparaged last week, reversed course. There were solid reports of forced selling by some hedge funds with leveraged positions. The behind-the-scenes trading is hidden from the average investor, even though the evidence is there if you know how to look.

- Rebound timing. There are many viewpoints, but most cite the conditions for some bottoming. But note well, these signs were there on Monday and markets moved even lower. No method is guaranteed. Here is an interesting collection of indicators and ideas.

Considering signs of when to buy. James Mackintosh (WSJ) looks at three relevant factors – political, stability of the financial system, and timing.

D.M. Martins Research does not recommend immediate buys but takes note of some positive developments including apparent containment of COVID-19 in the Far East and the reopening of Apple stores. Can the recovery curve be replicated in other countries?

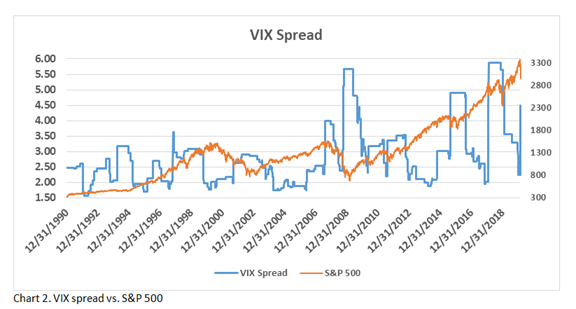

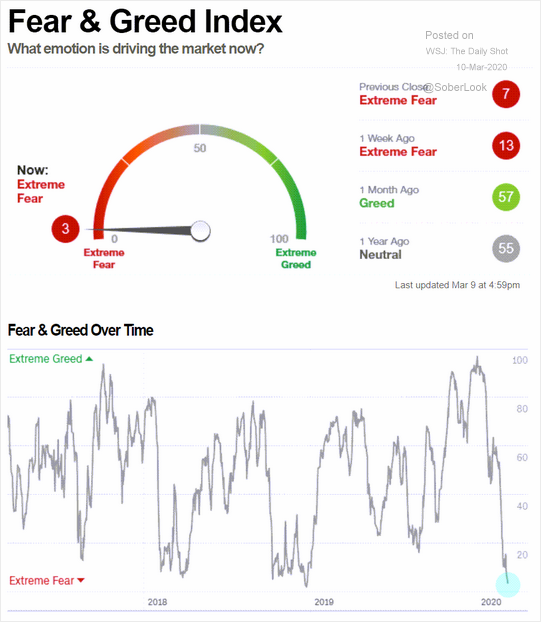

Analysis of the VIX Spread, the ratio between the 52-week high and low is an interesting measure from Leo Chen, Ph.D. via David Kotok. The chart below shows the history of this indicator. It read 4.93 on 3/7 where a level of “5” indicates extreme fear.

And the popular Fear & Greed Index.

The Put/Call ratio (a contrarian indicator where high ratings show fear) is at a multi-year high.

What Actions Might Investors Consider

I must start by underscoring that I provide investment advice to clients. I provide information to readers – information that I hope will be helpful in making their own decisions. With clients I can determine their personal situations and needs and discuss issues with them when needed. My readers cover a very wide range of circumstances. My challenge is to be helpful in my posts without crossing the line into advice.

With that in mind, here is what I was doing last week – for clients and for myself.

For the basic stock program, I neither bought nor sold, maintaining about 25% cash. (Please remember that this is only the equity portion of portfolios. If someone’s allocation is normally 60-40, they are now 45-40 with 15% cash).

There is not a rush to go all in with available cash. It may be time to adjust your sector allocation. I am including the Investment Ideas section with that in mind. If you “predicted” the crash, take a pat on the back and a fresh look at the current opportunities.

The best opportunity right now involves taking advantage of elevated volatility in option prices. In my Enhanced Yield Income program, I added to positions with more covered calls on solid value stocks with reasonable dividends. These include (especially) sectors where we do not expect a fast rebound. You can collect the high call premium, take some income, and reinvest the rest at current low stock prices. This is designed for investors who need reliable income regardless of market moves.

As usual, I’ll describe more of my own conclusions in today’s Final Thought.

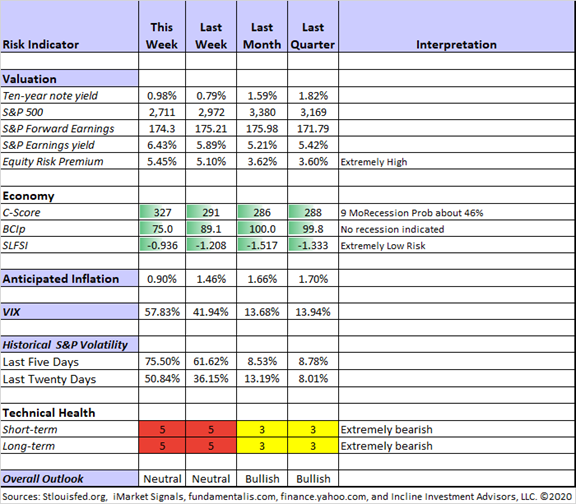

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

Both long-term and short-term technical indicators continued at the lowest reading. The C-Score improved slightly. The St. Louis Financial Stress Index is published on Thursday, using data from the prior Friday. We can expect another move higher next week, although we remain solidly in the safe zone.

I continue my rating of “Neutral” in the overall outlook despite attractive valuations. It reflects the increased risk and the continuing need for patience in either buying or selling. Some have asked about the likely decline in the forward earnings estimates. Brian Gilmartin is covering this evolving story and describes the likely volatility in corporate outlook “with a downside bias.” Even if I make a major reduction in expected earnings, the stock/bond comparison shows a large difference in valuation.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

Doug Short and Jill Mislinski: Regular updating of an array of indicators.

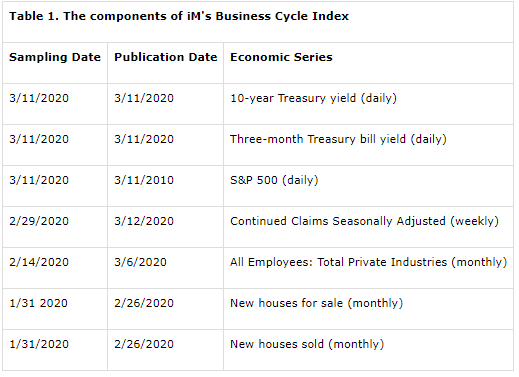

Georg Vrba: Business cycle indicator and market timing tools. The most recent update of Georg’s business cycle index does not signal recession. This week he reminds us of the historically effective components of his indicator, emphasizing “…that the full effect of the COVID-19 pandemic on the BCI will only manifest itself after the April housing data is published end of May.”

Guest Sources

Insight for Investors

Investors should understand and embrace volatility. They should join my delight in a well-documented list of worries. As the worries are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely. The drawback this week is that there is a lot of uncertainty surrounding when and how current worries will be resolved.

Best of the Week

If I had to recommend a single, must-read article for this week, it would be my friend Vitaliy Katsenelson’s, What Would Ben Graham Do in Today’s Market?

With shared credit with Jason Zweig, whom he cites.

Beginning with Zweig:

First, determine whether you are an investor or a speculator. “The investor’s primary interest lies in acquiring and holding suitable securities at suitable prices,” Graham wrote. The speculator, on the other hand, cares mainly about “anticipating and profiting from market fluctuations.”

If you’re an investor, “price fluctuations have only one significant meaning,” according to Graham: “an opportunity to buy wisely when prices fall sharply and to sell wisely when they advance a great deal.”

And also…

“The investor who permits himself to be stampeded or unduly worried by unjustified market declines in his holdings is perversely transforming his basic advantage into a basic disadvantage,” warned Graham. He “would be better off if his stocks had no market quotation at all, for he would then be spared the mental anguish caused him by other persons’ mistakes of judgment.” (The italics are Graham’s.)

Vitaliy adds wonderfully to this analysis, making it come to life with current pricing. His thoughts were the same as mine while watching the massive one-day moves:

The prices you see on your screen today are the transitory manic depressive opinions of the often mentally unstable Mr. Market. (If I have offended Mr. Market, my apologies). Mr. Market did not carefully value your companies today and decided that they are now worth less. No, he woke up in a grumpy mood and indiscriminately marked them down as if they were overripe bananas at the grocery store. (You cannot have enough metaphors here.)

The stock prices on your screen say nothing about what these companies are worth. Nothing at all. But that is all that is going to matter in the long run. I promise you one thing: The value of your companies doesn’t change 8% a day, day after day.

These are valuable articles for true investors. Keep a copy handy and look back at it a year from now. More on this topic in today’s Final Thought.

Stock Ideas

How about Adobe: Another Potential Winner Out Of The Bear Market.

Dick’s Sporting Goods (DKS) has low exposure to the coronavirus risks. Stone Fox Capital describes the strategic shift reducing the hunt department and increases other lines.

Sports such as basketball, soccer and volleyball are no longer seasonal. Soccer moms shopping alongside hunters buying a rifle never fit into the store concept.

What investors should care about are the actual results of the business. Shifting the hunt store space to more premium products in footwear and sports-related experiences is lifting the business.

Stone Fox Capital has another “fear trade” value stock with a strategy shift, Camping World Holdings (CWH).

Here’s Why Mortgage REITs Plunged 10% To 25% Today combines an explanation of highly unusual price activity with ideas about finding value. Hint: Study the price to book value ratios.

Bret Jensen suggests a simple covered call strategy for Exxon Mobil. He describes the strengths of the company, including the strong balance sheet and history of dividend increases. [Jeff – This basic approach is similar to what I do in my “Enhanced Yield” strategy, except that a user shorter-dated calls to capture rapid time decay. My emphasis is on regular income without the need for a stock price increase].

Blue Harbinger suggests a very similar, selling put options, on Phillips 66 (PSX). This is an acceptable alternative to my approach if your account is authorized for cash-secured puts. Be sure you are willing to buy the stock at the indicated price.

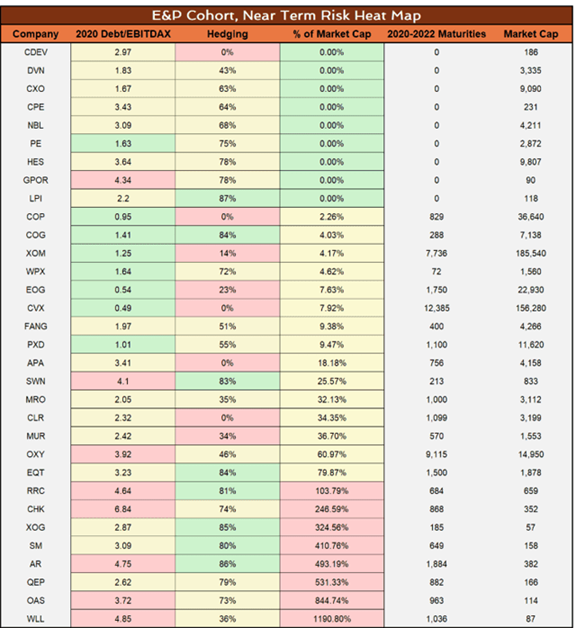

Is there a safe way to invest in an eventual energy rebound? Brad Thomas highlights the “historic opportunity for safe yield for brave income investors.” How brave need you be? The article provides background on the Russian and Saudi ability to continue the price war, and their breakeven price points. I especially like this heat map of the E&P cohort and near term risk; it includes both leverage and hedging. But Brad’s emphasis is on the safest mid-stream names. While the emphasis in on REITs, anyone with an interest in the sector will learn from this article.

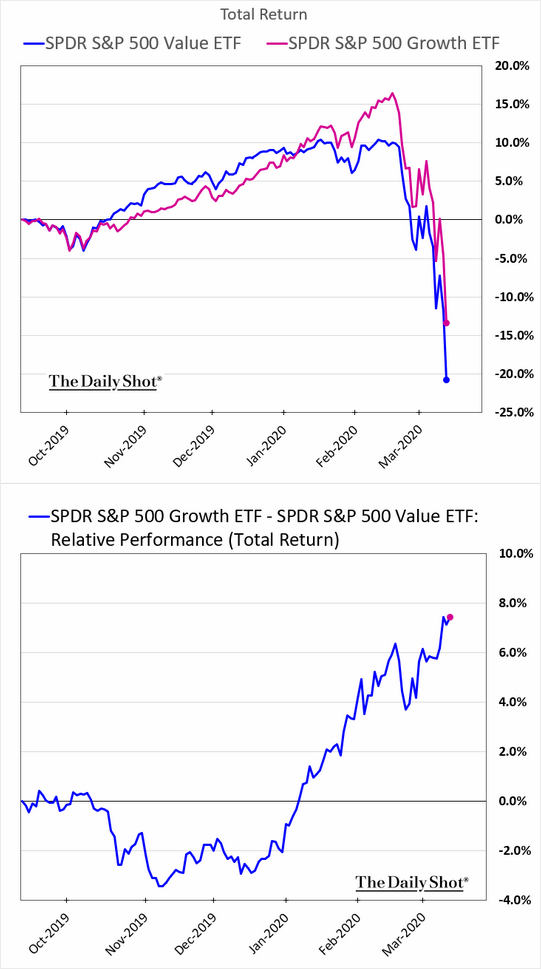

The Great Rotation

The current recession scare has halted (postponed?) the value portion of the Great Rotation. It has also affected small cap stocks which are generally perceived as more vulnerable financially. While I am using financial strength is a stock selection criterion, even the good stocks get caught up with the general selling of an ETF. While my own definition of “value” is a bit different from the popular charts, they do provide an indication of what is happening. In the face of this, I continue to proceed slowly on this theme.

Watch out for

The SIM hack – and how to protect yourself from unauthorized account withdrawals. (CNN Business).

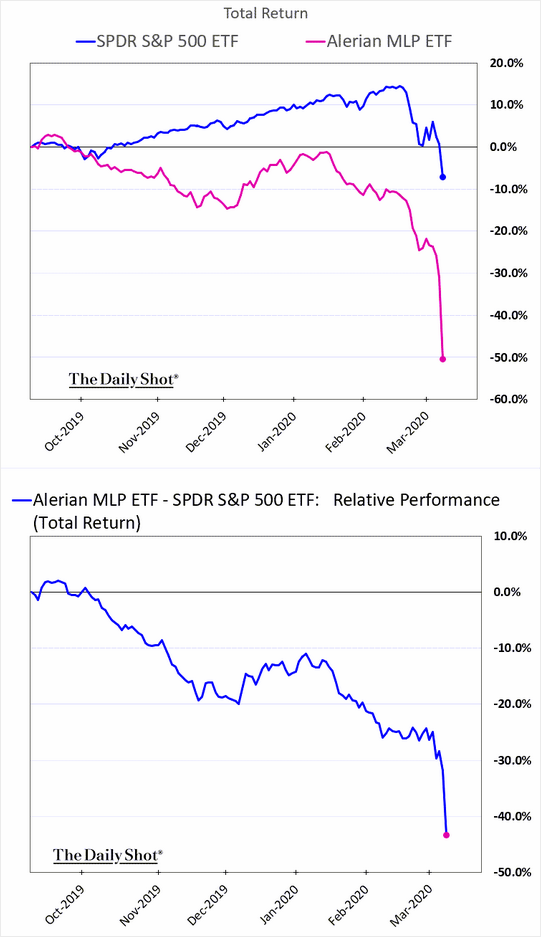

MLP’s, already weak before the price war.

Final Thought

In my last few posts, I have covered most of the current issues in great detail. If you missed any of them, I hope you will check them out. They provide valuable background for the current market.

The many variables have differing time frames. Some believe that government should immediately put money in the pockets of those who will spend it. Greg Mankiw recommends $1000 per person as well as giving Dr. Fauci “anything he asks for.” He does not like a payroll tax cut, which does not help those who can’t work. And “There are times to worry about the growing government debt. This is not one of them.”

The economic effects of new policies involve a lag. Market effects reflect approval or disapproval, often by specific subsets of participants, or even computers. It is a tricky test for the individual investor. Many of my very intelligent friends believe that a recession is inevitable or that one has already begun. This is a direct result of the easy narrative of cancelations and “nesting.” These effects are easy to see. Only those who place the impacts in the context of the overall economy can judge the impact.

How much of spending and production continues? Look at your own budget. Will your spending move a lot lower? Will those working from home continue to be paid? Will they provide productive services? What services will attract the revenue lost by restaurants and travel? Even if some sectors have an immediate hit, how much does that mean for the overall economy? How long will it last? Can policy actions mitigate the impact?

These more difficult questions are not asked by most observers. It helps to explain why economists do not view these events as a “light switch” that turns off the economy.

My favorite investment sector remains the homebuilders. None of the demographic fundamentals have changed. Mortgage rates have improved affordability. Companies are catering to the lower-price market. There is no sign of an effect on the jobs of potential buyers. Despite this, Mr. Market reduced stock prices in this group by about 30% in four days. As Vitaliy observed in my “best of the week section,” the price changes simply make no sense.

Panic is not a plan. Difficult times are crucial for investment decisions.

[Readers interested in what I am doing to generate dependable income in a declining market should request our Enhanced Yield information. I also welcome readers wanting to join our Great Rotation email list. You can opt-in to an email list which describes our progress with the design of the program, provides detail on the themes, and analyzes a specific stock we have already purchased. There is no charge and no obligation for participants, and we will not use your email for any other purpose. You can opt-out whenever you wish, but I hope you don’t! Comments and reactions are an important part of my investment process. I welcome your participation. Just write to “info at inclineia dot com”. There has been a lot of interest. If we have missed you, please try again].

I’m more worried about

- More panic. The expectation of a growth in cases and deaths should be firmly established. Nonetheless, fresh news sparks another round of knee-jerk selling. This frightens those who think Mr. Market knows all.

- Politicized government action. This should not be about claiming credit nor casting blame. Government can get there by spending enough money on any policy, but cooperation would make it easier and more effective.

I’m less worried about

- Epidemic containment. In the last week there has been a major move in the right direction.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits