Want to read more by Smead Capital Management? Visit their Featured Firm page here

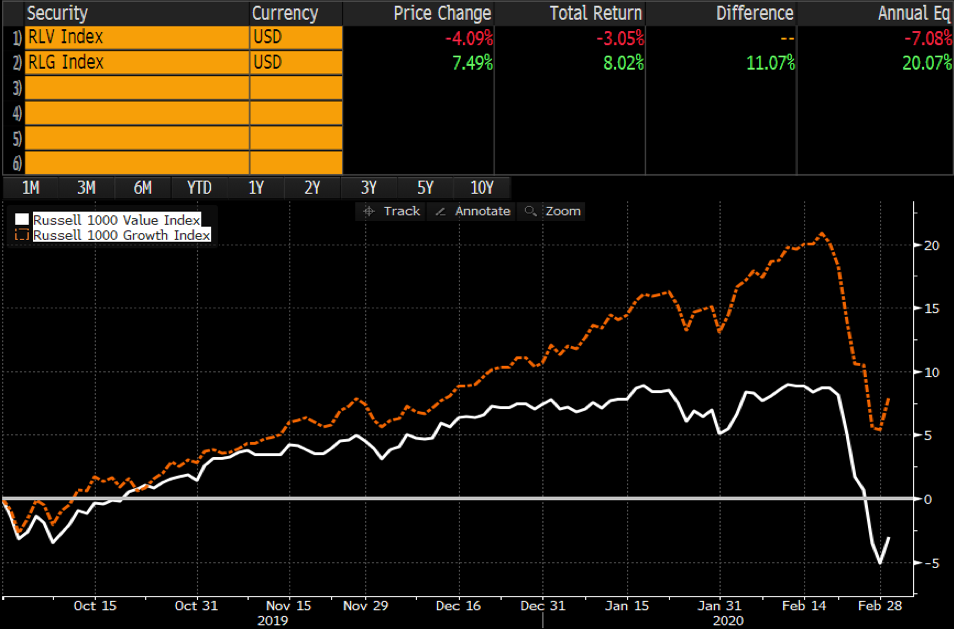

Those of you who have been with us recently know that we are calling the recent decline in value stocks a capitulation in a value investing depression. The coronavirus has sucked all the economic optimism out of a market which has hugged tightly to large growth companies providing reliable sales or earnings momentum. Index and ETF investors are also gripping tightly to low-vol stability stocks with slower, more consistent growth at very high price-to-earnings ratios (P/E). Here is how the Russell 1000 Value Index has done recently in comparison to the Russell 1000 Growth:

Source: Bloomberg.

What is the likely outcome of this race to safety and wholesale capitulation in economically sensitive stocks?

We believe over the next five to ten years, economic growth will be driven by a variety of factors including input prices, interest rates, household finances and demographics. When it comes to input prices, the recent capitulation in value has been led by the price of energy. For as long as the eye can see, automobiles will be fueled by gasoline. To us, this means that gasoline is automobile, airplane and long/short haul truck cocaine. The users are addicted to the product for years until a critical mass of cars, planes and trucks are run on batteries or something else. The S&P 500 Index has 3.51% of its assets (as of March 2, 2020) in the energy sector. This seems odd for one of the most important ingredients of our economy.

Interest rates are currently below one percent all the way out past five -year Treasury bond maturities and mortgage rates are working their way below three percent as they catch up to the ten-year Treasury bond rate near one percent. The Federal Reserve Board just cut fed fund interest rates 50 basis points as we go to press. Every week, we ask ourselves why today’s young families are so blessed to borrow money this cheaply to get their household up and running. We believe everyone will look back at this the way folks did in the late 1960s, after the early 1960s when mortgage rates were like today.

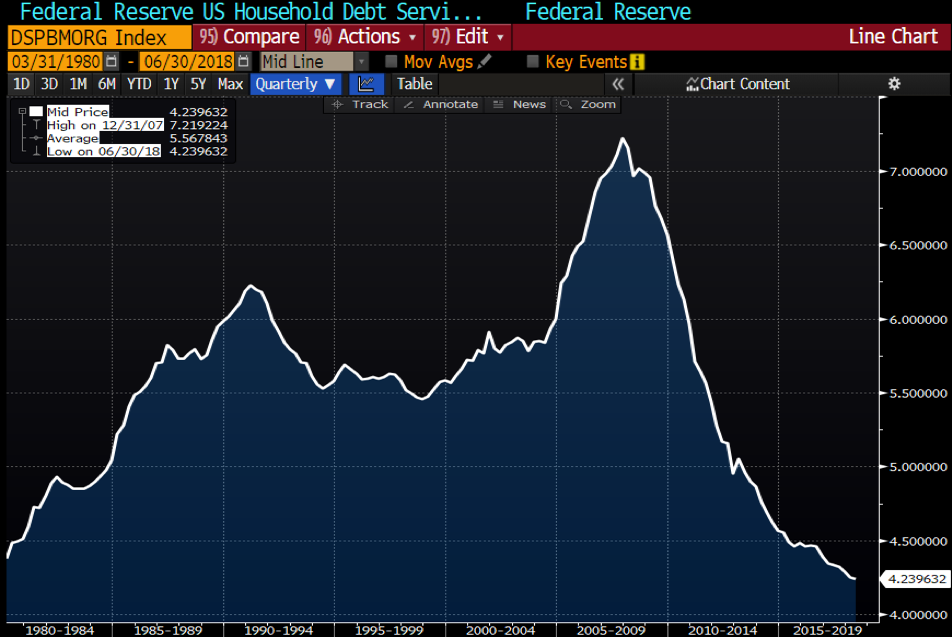

Household finances in the U.S. are in the best shape they have been in in the last 40 years (see the chart below).

The savings rate in the U.S. is the highest in a non-recession year in decades. All the money that would be needed to promote a dramatically better economy is available.

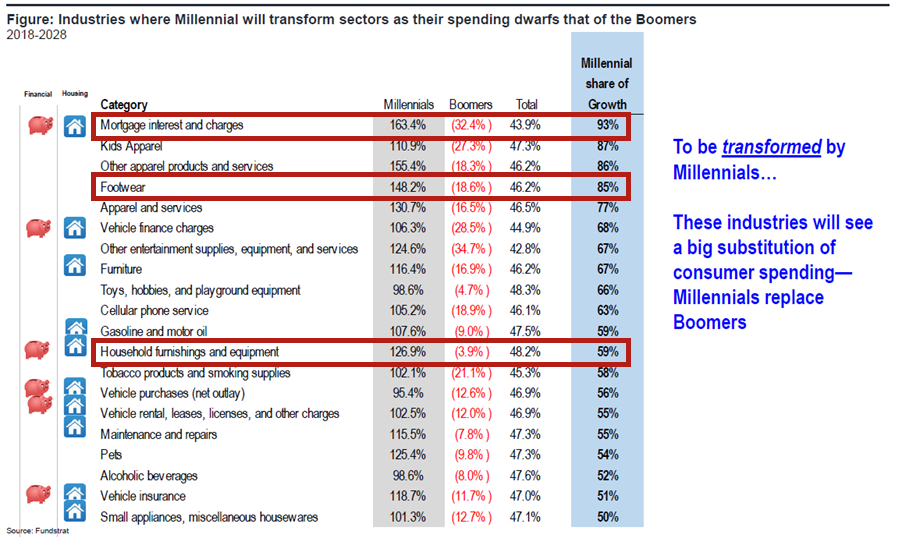

Demographically, 90 million millennials are about to take over the 30-45-year-old age group, replacing 65.8 million Gen X folks over the next ten years. This means that 36% more people will be forming households. Household formation is classic high economic multiplier effect living. We like to think of it as necessity spending on car buying, home buying, home furnishing and landscaping, etc.

We expect the swing will be huge because in the last ten years those same millennials were paying rent, eating fast food, drinking lots of alcohol and buying the latest Apple device. The landlord, burrito wrapper, bartender and iPhone assembler created very little in multiplier effect. Ask your landlord how many cars or houses they own, what your burrito wrapper spends money on, where your bartender lives and where the Apple devices are assembled (outside the U.S.).

Therefore, the most important list for the next ten years is the chart below. The chart shows where millennials will increase their spending the most.

The categories are very closely tied to home ownership, children, automobile transportation and family entertainment. In the current virus-led decline, this is the list of the poorest performing common stocks. We like stocks which have been battered by the collapse in economic optimism like Lennar (LEN), Target (TGT), Disney (DIS) and Occidental Petroleum (OXY). Regardless of how long the virus wreaks havoc, won’t these underlying fundamentals ultimately assert a stronghold over long-term stock price performance? Remember, time is the friend of the long-term investor and like Warren Buffett always likes to say, “Money moves from the hands of the impatient investors to the patient investors.” Economic optimism looks very cheap to us in these circumstances.

Warm regards,

William Smead

The information contained in this missive represents Smead Capital Management's opinions and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Bill Smead, CIO wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

© 2020 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com

Follow us on Twitter @SmeadCap