There are tangible signs economies in the MENA region have reformed and evolved over the past decade, according to Franklin Templeton Global Sukuk and MENA Fixed Income’s Dino Kronfol, and Franklin Templeton Emerging Markets Equity’s Bassel Khatoun and Salah Shamma. They outline the opportunities they see in the year ahead.

In the Middle East and North Africa (MENA) region, we’ve seen signs that many of these economies have adjusted, reformed and evolved to tackle the headwinds that have come their way over the past decade or so. In recent months, new challenges have arisen.

As we move into a new decade, we’ve seen evidence of growth in a number of MENA economies, across both fixed income and equity markets.

A WORD ON OIL PRICES

Before the novel coronavirus outbreak, we thought an oil price range of US$60-80 per barrel with a commitment from OPEC+ would be sufficient to support the global economy. Now we are seeing a potential slowdown in global economic growth and a dip in demand for oil as the virus spreads. We will continue to monitor the next OPEC+ meeting in March and see if members make supply cuts.1 We expect global growth to bounce back in the long term, and see oil prices rebound from current levels of about US$50-55 per barrel back to the range we anticipated before the virus outbreak.

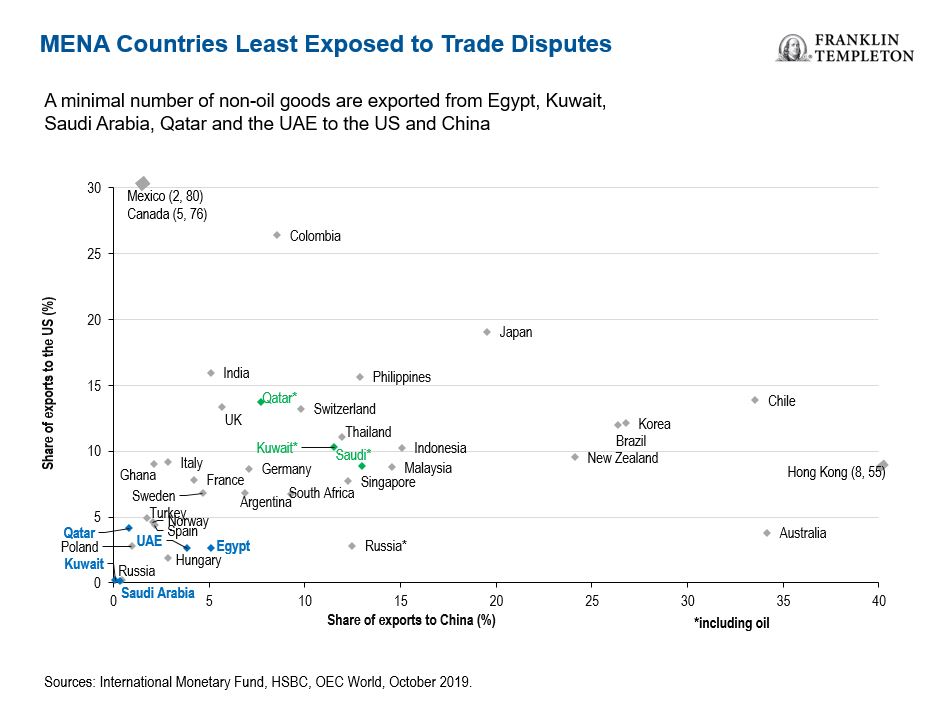

The world continues to focus on the potential market impact from ongoing US-China trade disputes. As most investors expected, US President Donald Trump recently signed a “phase one” trade deal with China which should likely cool off any further retaliatory action from either side—at least for now. While we continue to monitor global trade tensions, we think it’s unlikely the MENA region will feel a major impact from disputes between the United States, China and/or Europe.

MENA countries, for example, export a low number of non-oil goods to the United States and China, as seen in the chart below. MENA equities are also pegged to the US dollar, while GCC debt indexes exhibit a third of the volatility of the J.P. Morgan Emerging Markets Bond Index (EMBI),2 meaning that they are broadly lowly correlated to spikes in global tensions like trade wars, geopolitics or sudden oil price movements. And yet despite these favorable characteristics, we think MENA equities and fixed income asset classes continue to be underappreciated by investors.

MENA Region Increasingly Prominent in Emerging Markets Universe

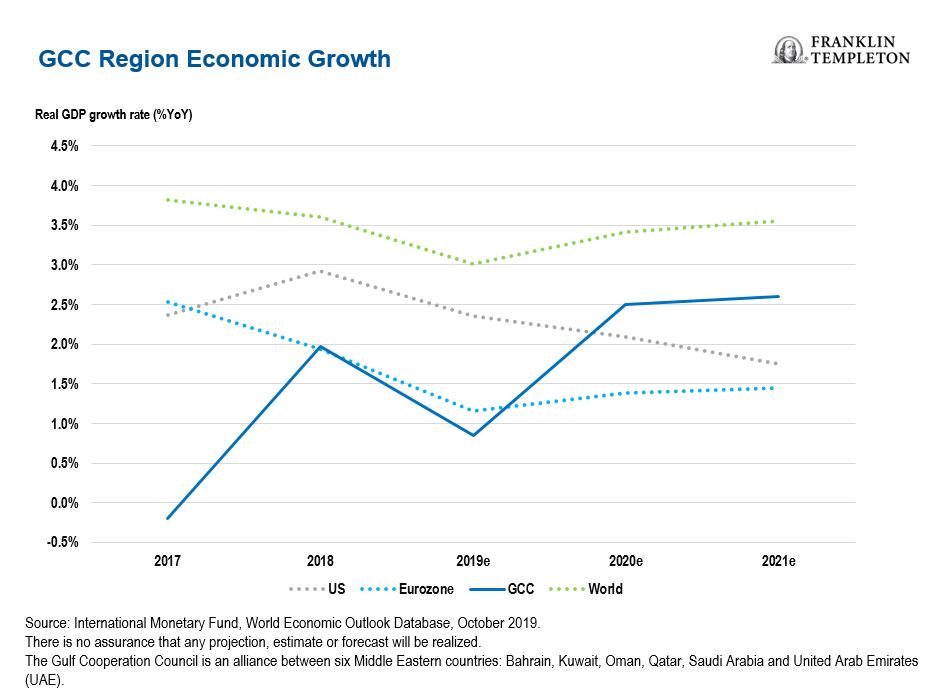

Our on-the-ground presence in the MENA region allows us to see the full effects of meaningful social and economic reforms that governments have implemented over the past couple of years. We’ve observed some encouraging signs these reforms have had a material impact on the overall sentiment towards regional economies—with growth in the Gulf Cooperation Council (GCC) region set to outpace advanced economies in 2020 and beyond.3

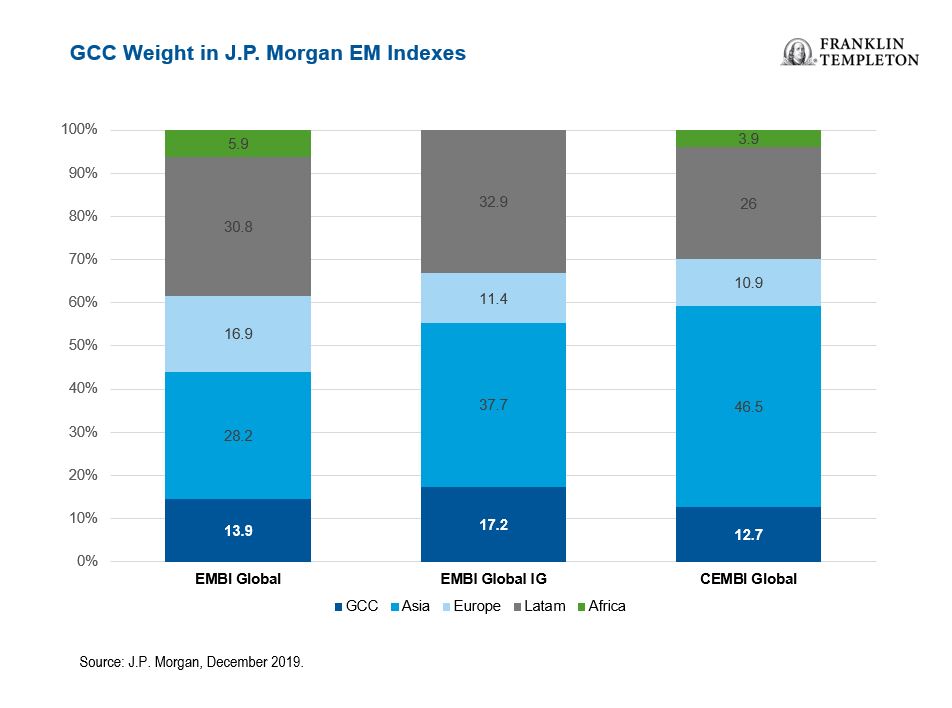

On the MENA fixed income side, we also started to see crossover investors from other emerging markets, following the GCC’s inclusion into J.P. Morgan’s EMBI in 2019, which now accounts for 18% of the index. Standing at close to US$500 billion in total outstanding debt,4 the GCC bond market is unrecognizable from a decade ago, and sovereign credit ratings for four of the six GCC countries are now rated “A1” or higher from a global credit ratings agency.

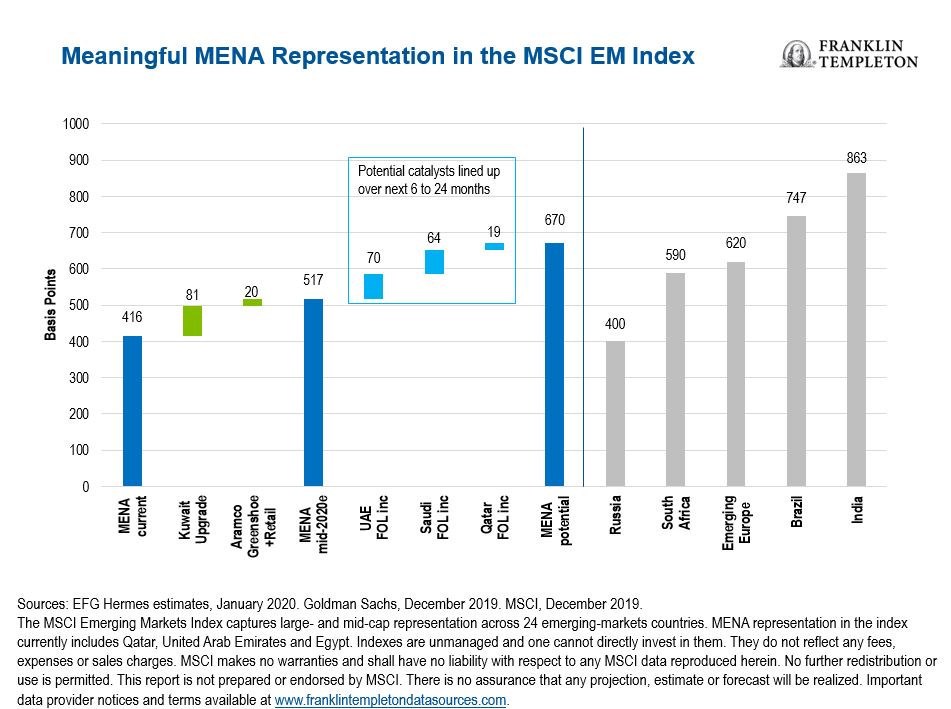

MENA equities are also becoming increasingly prominent within the emerging-market universe. With Saudi Arabia’s recent inclusion in the MSCI Emerging Markets Index5 and Kuwait’s slated for June 2020, in addition to several other smaller, liquidity catalysts lined up over the course of the next two years, the MENA region’s overall weight in the index could potentially increase to almost 7%.6 This would put it on par with the likes of South Africa, Emerging Europe and Brazil. And in Saudi Arabia alone, we’ve seen foreign inflows into the market of approximately US$21 billion this past year because of its recent inclusions in the MSCI and FTSE Emerging Markets Index.7

We think major, liquidity events like these make MENA increasingly hard to ignore from an investment perspective, as it continues to become more prominent within the wider emerging-market universe.

Distinct Pockets of Opportunity Across MENA

Economic growth in the MENA region is picking up at a time when we’ve seen a general loosening of monetary policies. A global shift to more accommodative monetary policy has provided a positive backdrop for MENA countries, as looser monetary policies support overall demand. As such, we see distinct pockets of opportunity in certain markets.

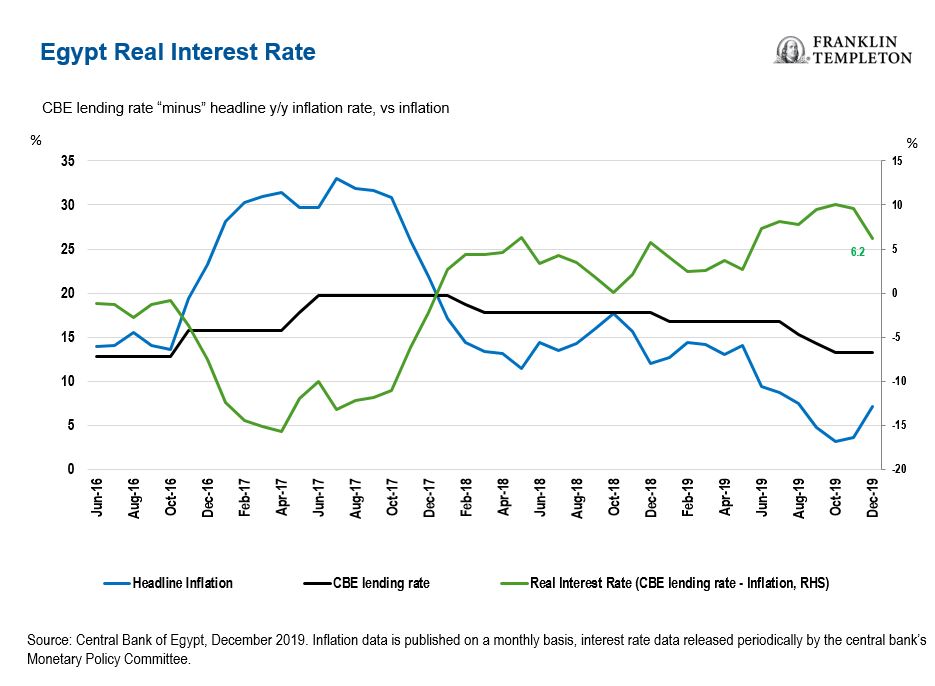

In the case of Egypt, we’ve seen significant shifts in the economy. Inflation which has historically been stubbornly high has come off significantly over the last two years, and allowed the country’s central bank to reduce interest rates by 450 basis points in 2019.8 We think lower rates could kick off long-awaited growth in consumption and credit that in turn creates a positive backdrop for equities.

It is also important to note that Egypt is primarily a secular growth story. Real gross domestic product (GDP) growth is estimated to pick up to 5.9% for the fiscal year ending in June 2020, versus 5.6% for the fiscal year 2019.9 It’s a country that has come a long way through a three-year International Monetary Fund (IMF) program that involved a US$12 billion loan and a sharp devaluation in the Egyptian pound. By the time the program concluded in 2019, it had steadied Egypt’s economy and left unassuming equity valuations, at a price-to-earning (P/E) multiple of 8.98 in Egypt’s benchmark equity index, despite a 22% projected earnings growth rate, all of which are bullish factors that are attractive to us.10

We’re also seeing some notable opportunities in the United Arab Emirates (UAE), which has implemented proactive reforms to increase foreign ownership across multiple sectors, drive the trade and tourism economy, relax rules on property ownership and extend visas to encourage expatriates to stay in the country longer-term. Expo 2020, a six-month-long fair starting in October 2020, is also expected to drive tourism, create jobs and will likely leave a legacy via the transformation of the Dubai South district.

From a valuations point of view, we consider UAE equities to be quite inexpensive at the moment, with a P/E multiple of 9.4 for its equity benchmark, relative to high P/E ratios across the globe. If we look at the bigger picture, emerging markets currently trade on a P/E multiple of 13.4, placing the UAE on the lower end of the valuation scale.11 As a result, we believe a combination of mass reforms, positive growth measures and attractive valuations present us with some untold opportunities for the country.

We’ve also seen some progressive developments in the pension sector, particularly for expatriates. The Dubai International Financial Centre (DIFC) has launched its Employee Workplace Saving Scheme this year—a mandatory program for all DIFC employers, which will restructure the current defined gratuity plan, an end of service benefit paid out to an employee upon departure from the company, based on existing salary and number of years worked. We think the new model has the potential to be replicated across the UAE and wider GCC, and that the region’s pension funds could reach US$40 billion over the next five years.

Saudi Arabia is another market we can’t overlook. The initial public offering (IPO) of Saudi Aramco in December 2019, a pillar of the Kingdom’s wider 2030 Vision Program, was the largest listing in history, peaking at a valuation of over US$2 trillion. The company also issued its first bond ever, which sparked massive global interest and attracted more than US$100 billion in demand. Deals like these lend credibility to the wider reform agenda inside the country, and we are excited about its future growth prospects.

Furthermore, the ongoing transformation in Saudi Arabia cannot be overstated. Far-reaching reforms have already started to change the socioeconomic landscape. Major strides have been taken to liberalize women’s rights and improve female workforce participation. Similarly, we’ve seen a significant effort to rein in wasteful spending, increase fiscal transparency and promote new industries in the kingdom.

Moving forward, sparking growth in Saudi Arabia’s private sector will continue to be a cornerstone of the government’s program, which is prioritizing privitization and aims to raise as much as US$200 billion in the coming years. And while we think the Saudi Aramco listing on the local stock exchange, the Tadawul, should contribute to kick-starting the country’s IPO pipeline, the broader privatization push is part of the government’s broader vision to diversify its economy and decrease dependence on oil revenues. We expect four more companies to also list on the Tadawul throughout this year, barring any deterioration in market conditions.

Looking ahead, we think there are many opportunities to be found across the MENA region, and that investors shouldn’t discount it as a potential investment case.

To get insights from Franklin Templeton delivered to your inbox, subscribe to the Investment Adventures in Emerging Markets blog.

For timely investing tidbits, follow us on Twitter @FTI_emerging and on LinkedIn.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of publication date (or specific date in some cases) and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FTI affiliates and/or their distributors as local laws and regulation permits. Please consult your own professional adviser or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton Investments’ U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

1. OPEC+ is an alliance of oil producers, including members and non-members of the Organization of the Petroleum Exporting Countries.

2. Source: Franklin Templeton calculation based on Bloomberg data, December 2019. The J.P. Morgan Emerging Markets Bond Index tracks bonds in emerging markets. Indices are unmanaged and one cannot directly invest in them. They do not include fees, expenses and sales charges.

3. Source: International Monetary Fund, October 2019. The Gulf Cooperation Council is an alliance between six Middle Eastern countries: Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates (UAE). There is no assurance that any projection, estimate or forecast will be realized. Important data provider notices and terms available at www.franklintempletondatasources.com.

4. Bloomberg, as of December 31, 2019.

5. The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging-markets countries. Indexes are unmanaged and one cannot directly invest in them. They do not reflect any fees, expenses or sales charges. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI. Important data provider notices and terms available at www.franklintempletondatasources.com.

6. Franklin Templeton’s own estimates.

7.The FTSE Emerging Markets Index includes large- and mid-cap securities from advanced and secondary emerging markets. Indexes are unmanaged and one cannot directly invest in them. They do not reflect any fees, expenses or sales charges. Important data provider notices and terms available at www.franklintempletondatasources.com.

8. A basis point is a unit of measurement. One basis point is equal to 0.01%.

9. Sources: International Monetary Fund, October 2019, World Bank, October 2019. There is no assurance that any projection, estimate or forecast will be realized. Important data provider notices and terms available at www.franklintempletondatasources.com.

10. Sources: Egyptian Exchange EGX 30 Index, October 2019. Bloomberg, Franklin Templeton calculations, October 2019. Price-to-earnings ratio is the ratio for valuing a company that measures its current share price over its per-share earnings. There is no assurance that any estimate, forecast or projection will be realized. Indexes are unmanaged and one cannot directly invest in them. They do not reflect any fees, expenses or sales charges. Important data provider notices and terms available at www.franklintempletondatasources.com.

11. Source: MSCI via Bloomberg. Note: Emerging Markets are represented by the MSCI Emerging Markets Index. Indexes are unmanaged and one cannot directly invest in them. They do not reflect any fees, expenses or sales charges. Important data provider notices and terms available at www.franklintempletondatasources.com.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments