February was quite the wake-up call for investors with the S&P 500 falling 13% from it’s all-time high over the course of only 7 trading days^….with not a single one of those days ending positive. As the coronavirus (COVID-19) continued to spread the markets largely ignored it until one day, out of the blue, it appeared to take notice.

While the speed of the most recent correction has been unusual, so far the depth of the fall has been quite ordinary. In fact, in terms of depth, the current episode looks a lot like the Zika virus about 4 years ago when the market fell 12% over the course of about a month and a half (between 12/29/15 - 2/12/16).

It is also very reminiscent of another coronavirus outbreak, SARS, in 2003. In that episode the S&P 500 fell 14% in a little less than 2 months (between 1/14/03 - 3/11/03).

Ongoing Unknowns

Economically, what is quite different about this episode as opposed to SARS in 2003 (which also started in China) is that China now makes up about 19% of global GDP....Compared to only about 4% in 2003.

While everyone focuses on the role of China in manufacturing, the sole focus on manufacturing is a pretty outdated view. What is often overlooked is the pivotal role the Chinese consumer plays for US companies. In fact, Starbucks has over 4,100 stores in China1…. More than twice the number of any other country outside of the US. General Motors sells more cars in China than in the US2. From a big picture lens, China is the third largest market for US goods and service exports3 and one of the most important markets for many US companies as it relates to meeting their growth assumptions.

The ripple effects on supply chains and global tourism from the unprecedented efforts China took in locking down cities, factories and airports is simply unknowable. Compounding this is the ongoing spread to other countries which has resulted in additional unprecedented measures. Cases in the US have likely been largely under-reported up to this point due to the shortage of functional test kits4. It is this uncertainty that is hard to calculate. Has the market over-reacted? Will the market recover relatively quickly as in other outbreaks? Only time can tell.

Your Objectives Are Knowable, The Future Is Not

Over the course of executing any long-term investment plan, there is nothing you should expect more than the unexpected….eventually. That is why we cannot talk enough about diversification, centered around your goals, time horizon and objectives. Not a plan centered around trade policies, Federal Reserve interest rate adjustments, disaster responses or elections.

The reality is that every market correction seems different while you are living it. However, after-the-fact parallels are easy to come by (hindsight is 20-20). As the saying goes, history doesn’t repeat itself but it often rhymes.

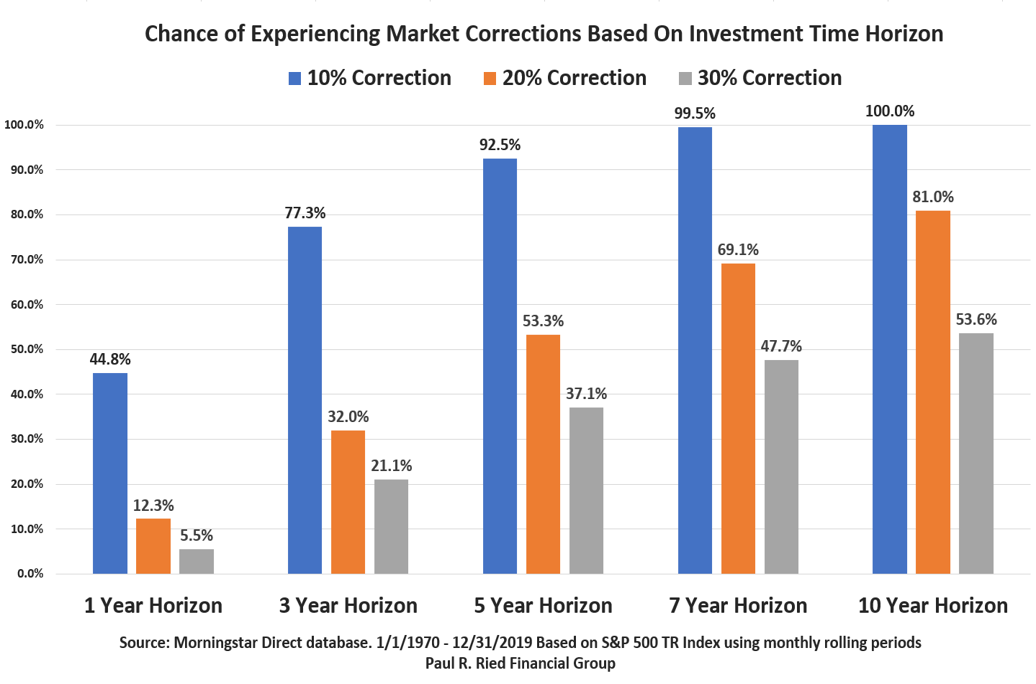

As the below chart illustrates, experiencing corrections in the stock market is inevitable, especially as you extend your time horizon. However, the timing is unpredictable and that is the reason for diversification. This chart shows you the chance of experiencing stock market corrections of varying sizes over the last 50 years (1/1/1970 - 12/30/2019).

As you can see, corrections like the one we have experienced so far are definitely to be expected. Over any 1-year time period your chance of going through a correction of at least 10% has been nearly a coin flip over the last 50 years.

A Tale of Two Decades

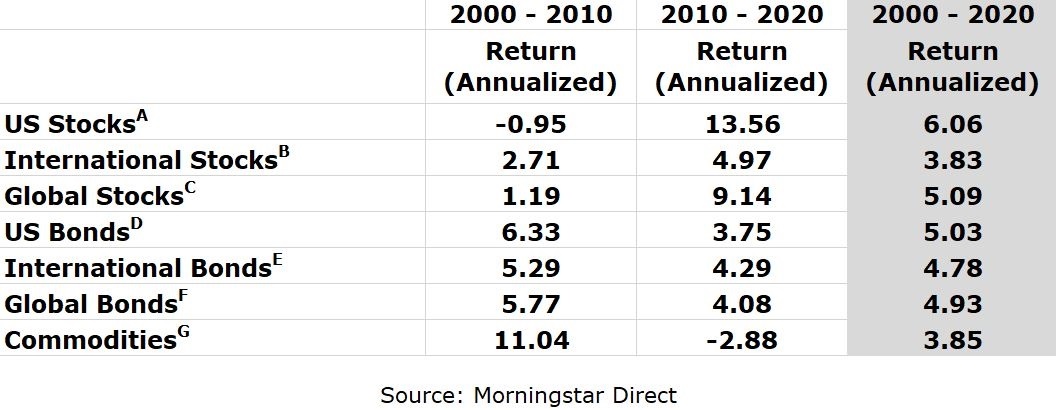

As we embark on a new decade it can be useful to look at where we have come from. The last two decades had some stark contrasts, particularly as it relates to US stocks. US stocks started 2000 at the lofty valuations that were a hallmark of the Dot-Com Boom and ended the decade at depressed valuations as a result of the 2008-2009 global financial crisis. The end result for US stocks over the 2000-2010 period was a lost decade in terms of return for investors.

The subsequent period was quite the opposite, US Stocks started at depressed levels and ended 2019 at historically high levels by most measures of valuation. While not as expensive as the Dot-Com boom...still quite expensive.

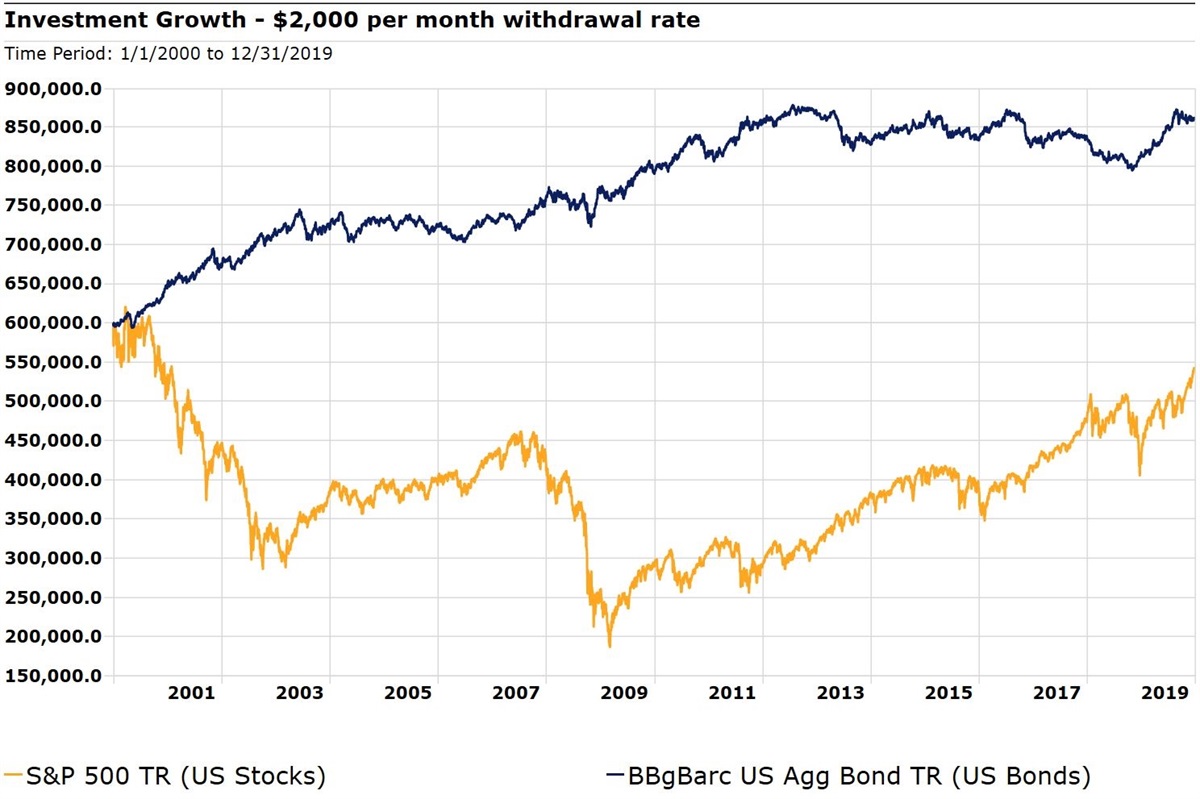

Over this complete 20-year period US Stocks had the highest return of about 6% per year. Although, an investor taking monthly income of about 4% per year would have been better off during this particular snapshot in time investing in US or Global Bonds due to their lower volatility. The below chart shows two hypothetical investors starting with $600,000 and taking $2,000/mo from their account (representing a 4% annual withdrawal rate based on the starting value).

Disclosure: This example is for illustration purposes only and does not represent the actual performance of any particular investment or investment strategy. Past performance does not guarantee future results. The S&P 500 TR index is an unmanaged group of securities considered representative of the US stock market in general. The BBgBarc US Agg Bond TR index is an unmanaged group of securities considered representative of the US bond market in general. You cannot invest directly in an index. Data Source: Morningstar Direct

___________________________________________________________________________________________________

However, had the decades been flipped with US Stocks performing well the first decade and poorly in the second decade then the results would likely have been dramatically different. This is what is often referred to as sequence of return risk. For an investor that is not taking from or adding to their investments, sequence of return matters little. Although, for everyone else it can make significant impacts on their outcome. The purpose of diversification is to strike a balance between stability and return to make the ride smoother. This helps reduce sequence of return risk as well as helps manage the emotional rollercoaster volatility can cause which might lead to an investor abandoning their strategy at the worst time.

The Decade Ahead

What will the decade ahead look like? Only time will tell but we think it would be prudent to expect returns that more closely resemble a combination of the last 2 decades rather than our most recent decade in isolation. However, given the low interest rate environment, the last 10 years for bonds may represent more of a goal than an expectation. In addition, US Stocks entered this decade at high valuations and international stocks are relatively undervalued, so we don’t think now is the time to count out international stocks for the long-term.

What does this all mean in practice? Your investment portfolios are designed for a marathon, not a sprint. And in reality, it’s not even a race. The goal is not to beat somebody else....The purpose is to meet your objectives.

Using the principles of asset allocation and utilizing professional active money managers we have developed customized portfolios consistent with each of your objectives. If your objectives have not changed, we recommend staying the course through these current challenges with the understanding that these wild market swings (and worse) are to be expected during the course of any long-term investment horizon.

As always, should you have any questions or concerns, don’t hesitate to e-mail or call our office.

Paul R. Ried, MBA, CFP®

President / CEO

Registered Principal*

Timothy R. Kimmel, CFP®

Chief Financial Advisor

Registered Representative*

Adam Jordan, CIMA®, AAMS®

Director of Investments / CCO

Registered Principal*

Kelly Kolstad, JD, CFP®

Personal Financial Advisor

Registered Representative*

^ - Source: Morningstar Direct as of 2/28/20

1 - https://finance.yahoo.com/news/starbucks-update-on-china-store-reopening-amid-coronavirus-162021454.html

2 - https://www.cnbc.com/2020/01/07/gm-warns-of-ongoing-challenges-in-china-as-sales-fall-15percent-in-2019.html

3- https://oec.world/en/profile/country/usa/#Exports 4 -https://www.sciencemag.org/news/2020/02/united-states-badly-bungled-coronavirus-testing-things-may-soon-improve

A – S&P 500 TR B – MSCI EAFE NR C – DJ Global TR D – BbgBarc US Agg Bond TR

E – BbgBarc Global Agg ex USD TR Hedged F – BbgBarc Global Agg TR Hedged

Opinions expressed are not intended as investment advice or to predict future performance. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. All economic and performance information is historical and not indicative of future results. Asset Allocation, which is driven by complex mathematical models, should not be confused with the much simpler concept of diversification. No investment strategy can ensure profits or protect against loss. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability,and differences in accounting standards. Past performance does not guarantee future results.

© Paul R. Ried Financial Group

More Mutual Funds Topics >