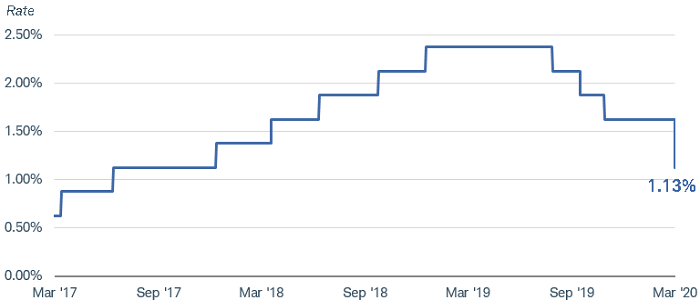

In a surprise move, the Federal Reserve on Tuesday lowered the target range for the federal funds rate, its key benchmark interest rate, by 50 basis points,or half a percentage point, to a new range of 1% to 1.25%. The reasoning behind the move was concern about the “evolving risks” to the economy posed by the coronavirus.

The cut came after a meeting of Group of Seven (G7) finance ministers and central bankers issued a statement reaffirming their commitment to support the global economy. The 50-basis-point cut was the first move of more than 25 basis points since December 2008.

The federal funds rate is now in the 1% to 1.25% range

Source: Bloomberg. Federal Funds Target Rate Mid Point of Range (FDTRMID Index). Daily data as of 3/3/2020.

The federal funds rate is the interest rate banks charge each other to lend Federal Reserve funds overnight. It’s also a key tool the central bank uses to moderate or stimulate U.S. economic growth.

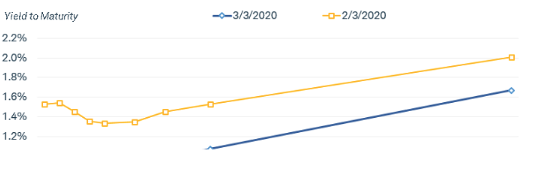

Treasury yields of all maturities dropped after the decision. Two-year Treasury yields dropped below 0.8%, indicating that markets may be expecting even more cuts down the road. Meanwhile, 10-year Treasury yields hit another new all-time low of 1.04%.

Source: Bloomberg, data as of 3/3/2020 and 2/3/2020. Past performance is no guarantee of future results.

While monetary policy cannot directly address many of the problems that the virus poses (only a vaccine can do that), it can help mitigate some of the second-order risks to the economy. With growth slowing around the globe as businesses struggle with broken supply chains and financial conditions tightening, the Fed clearly wanted to signal that it was acting to offset some of the risks. In a press conference Tuesday, Fed Chair Jerome Powell described it as a preventative measure. Powell said that risk to the Fed’s outlook had changed materially, and these measures were meant to keep the U.S. economy strong.

Having lowered rates by 50 basis points, the Fed has used up a fair amount of its “ammunition.” Should the economy fall into recession, it’s likely the federal funds rate could go back to zero and the Fed would likely re-start its quantitative easing program. It’s too soon to say if that will happen, but it is a possibility longer term.

On the other hand, if the economy is resilient in the face of the coronavirus and growth improves, then the Fed may face a difficult decision later this year about reversing this emergency rate cut. Financial conditions will likely help determine Fed policy as this situation progresses. While the Bloomberg U.S. Financial Conditions Index rebounded slightly from its end-of-February low, conditions are still “tight.”

Financial conditions tightened as coronavirus fears spread

Note: The Bloomberg U.S. Financial Conditions Index tracks the overall level of financial stress in the U.S. money, bond, and equity markets to help assess the availability and cost of credit. A positive value indicates accommodative financial conditions, while a negative value indicates tighter financial conditions relative to pre-crisis norms.

Source: Bloomberg. Bloomberg U.S. Financial Conditions Index (BFCIUS Index), daily data as of 3/3/2020.

We expect Treasury yields to remain low and perhaps fall even lower. The yield curve should steepen as short-term rates fall faster than long-term rates. Even though interest rates are already low, there is room for them to fall further. U.S. 10-year Treasury yields are still significantly above those in Europe and Japan, which implies that rates could converge longer-term.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market or economic conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

Investing involves risk including loss of principal. International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(0320-0FC3)

© Charles Schwab & Co.

© Charles Schwab

More Alternative Investments Topics >