"Reversion to the mean is one of the most common stories in history. It is the main character in economies, markets, countries, companies, careers – everything." Morgan Housel, The Collaborative Fund"

Lesson #2: Reversion to the mean occurs because people persuasive enough to make something grow don’t have the kind of personalities that allow them to stop before pushing too far.

The five lessons, continued

I finished last month’s Absolute Return Letter – the first in this series – arguing that wealth in society cannot outgrow nominal GDP forever. Over the long run, the two must grow 1:1. The fact that wealth, particularly US wealth, has grown much faster than GDP since the Global Financial Crisis, implies that the ratio of wealth-to-GDP must mean revert at some point, and mean reversion is precisely what this month’s Absolute Return Letter is about.

Morgan Housel, the author of “Five Lessons from History” opens his thoughts on Lesson #2 with the following words:

What kind of person makes their way to the top of a successful company or a big country?

Someone who is determined, optimistic, doesn’t take “no” for an answer, and is relentlessly confident in their own abilities.

What kind of person is likely to go overboard, bite off more than they can chew, and discount risks that are blindingly obvious to others?

Someone who is determined, optimistic, doesn’t take “no” for an answer, and is relentlessly confident in their own abilities.

I am sure you know one or two people in your circles who fit this bill quite well, but I cannot think of anyone better than Elon Musk of Tesla (who is also mentioned by Morgan Housel). Elon Musk is admittedly a genius, but he is also an accident waiting to happen. Taking on VW, GM, Ford and Toyota at the same time as he plans to colonise planet Mars, should be enough to raise your eyebrows. This month’s Absolute Return Letter is not about Elon Musk, though, but about the little, greedy devil that grows in most of us; the devil that tells us to buy when we ought to sell.

Mean reversion in its simplest form

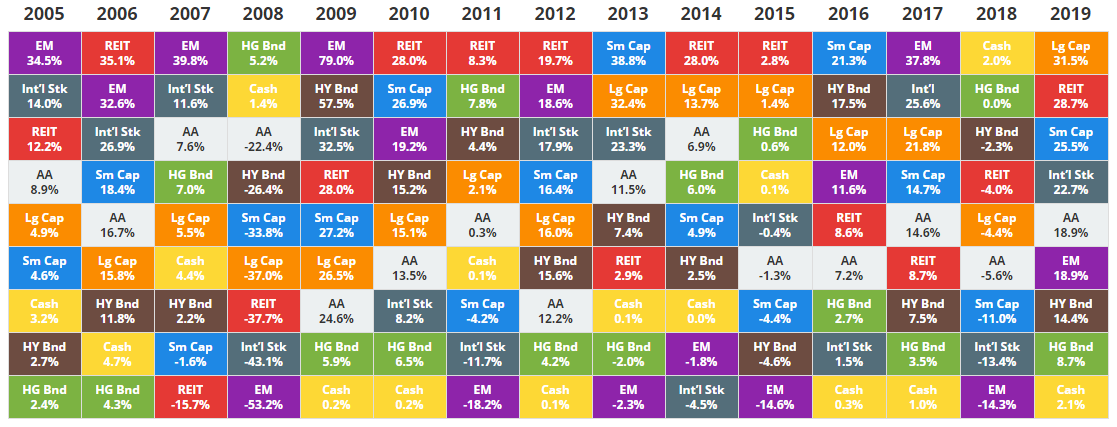

Mean reversion in its most simple form is easy to understand. What does very well one year, rarely does so well the next. Investors have learned that lesson many times over the years but still manage to forget the logic behind it (or at least some of us do) every now and then. The rule is not set in stone, though. Take a quick look at Exhibit 1 below and look at the 2010-15 period during which one asset class did outstandingly well – REITs.

Exhibit 1: Asset class returns, 2005-19 Source: Novel Investor

Another asset class that stands out as an exceptional performer more recently is Large Cap, which is most likely explained by the outstanding performance of many big technology companies.

What REITs did from 2010 to 2015, and what Large Cap has done since 2013 is the exception rather than the rule, though. Generally, asset class returns tend to vary quite dramatically from one year to the next, and the reason is quite simple. A change in fundamentals will cause an asset class to perform very well (or very poorly) for a while, but the momentum this creates often causes the asset class in question to overshoot (undershoot) the price that can be justified from a fundamental point-of-view. Hence, at some point, mean reversion will kick in.

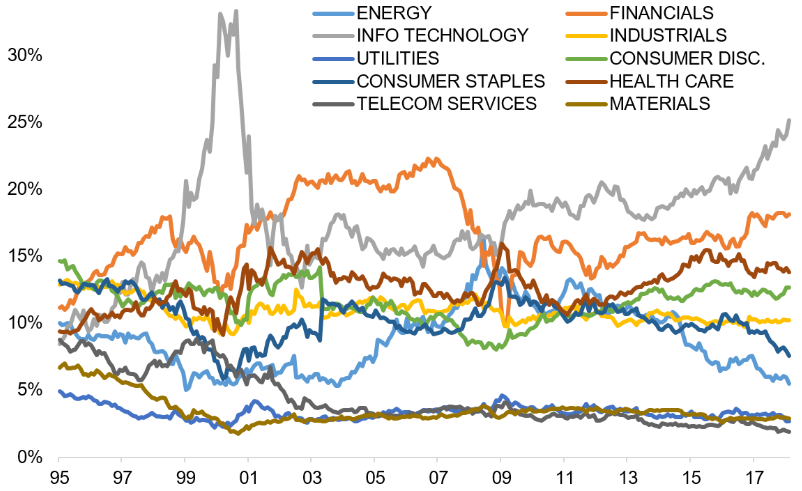

The obvious example of that would be Information Technology during the dotcom boom and bust (Exhibit 2). As you can see, IT did exceptionally well in the second half of the 1990s, only to come straight back in the early 2000s. Although IT is now elevated again, it gives me some comfort that the gains appear to be more modest this time, although I am pretty sure mean reversion will spoil the party at some point – at least temporarily – if it hasn’t already started.

The ultimate version of mean reversion

Wealth growth is an important driver of the feel-good factor in society, and that explains why populists like Donald Trump and Boris Johnson have risen to the pinnacle of the political arena more recently. As a significant percentage of the electorate in both countries have gone through years of negative wealth growth, by choosing a rather controversial leader, ordinary people are begging for a better life. In the context of mean reversion, let me explain why that is relevant.

Although many Americans and even more Brits (when measured in percentage terms) have experienced a decline in living standards in recent years, total wealth in both countries is higher than ever, and that is because the wealth of the wealthiest 0.1% has risen absurdly, which is why one of our megatrends is called The Rising Gap between Rich and Poor.

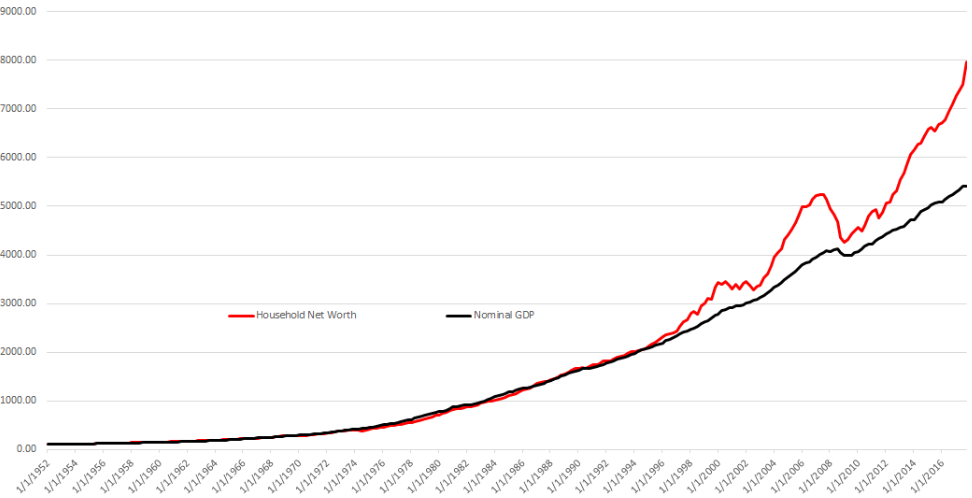

In the long run, total wealth in society cannot grow faster than GDP. That said, in the mid-1990s, wealth began to grow significantly faster than nominal GDP and has done so ever since (Exhibit 3).

Exhibit 3: US household net worth vs. nominal GDP Source: Zero Hedge

There are some very technical, mathematical reasons why one cannot outgrow the other forever but, for now, let’s just apply some simple logic and say that GDP growth drives wealth growth in society. Hence, over time, the two must grow hand in hand; however, it doesn’t always do so in the short to medium term.

Every single country around the world has a well-established mean value when you measure wealth relative to GDP, and every county reverts to that mean regularly. In the biggest economy of them all, the United States of America, the long-term mean value is 380% and, at present, wealth-to-GDP is no less than 520%. In other words, mean reversion will destroy plenty of wealth at some point. It is only a question of time.

Central bankers (governments?) know this and desperately try to prevent the system from clearing itself. By injecting ever more capital into the system (via QE or otherwise) they have managed to postpone D-Day for a number of years, but the system will eventually clear itself. There are no two ways about it. Think of it as central banks pushing a snowball in front of themselves. The only problem is that the snowball gets bigger and bigger.

Another snowball or two

The mood amongst average Americans is better than it has been for many years (conveniently ignoring the coronavirus-related setback over the past few weeks). US real wages are rising again, and many have forgotten that the stock market can also go down every now and then. Given that the average American is more exposed to equities than the average European, no wonder he feels good, but I can spot a snowball or two. Allow me to explain.

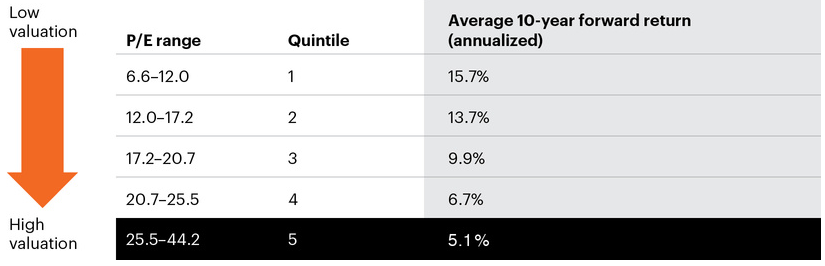

Exhibit 4: 10-year annualised returns on US equities based on stock market valuation (CAPE) at entry point (1950-2018) Source: FS Investments

Problem #1: US equities are relatively expensive and will mean-revert at some point.

Long-term returns on equities (when annualised) are almost always the highest when P/E levels at the entry point are the lowest. As you can see from Exhibit 4 above, over the last 70 years, if you have entered the market at valuation levels of 12 or less, 10-year returns (when annualised) have been no less than 15.7%, but that number drops as the entry P/E-level rises. Unfortunately, right now we are in the fifth quintile, meaning that, if history provides any guidance, you shouldn’t expect more than c. 5% annually on US equities over the next ten years.

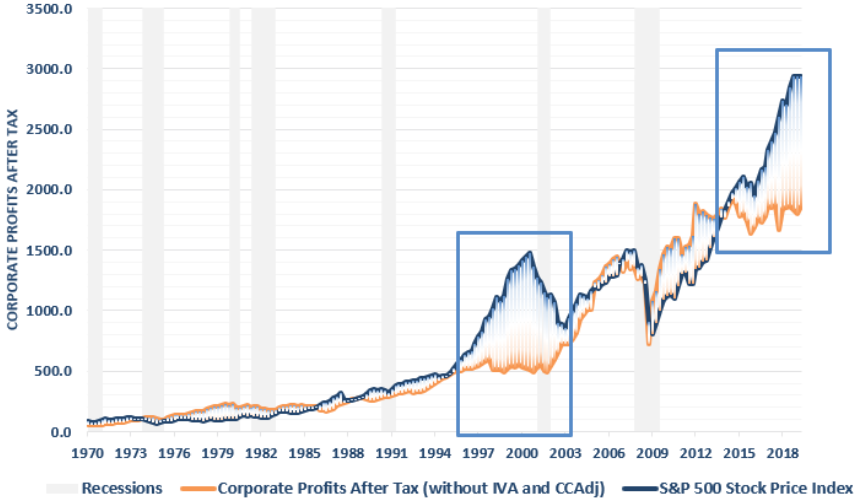

Problem #2: US corporate profits are not as strong as the stock market suggests, meaning that US equities will mean-revert at some point.

Just like central bankers are fighting tooth and nail to prevent the system from clearing, so do corporates, and that has led to a massive spread between US corporate profits and the performance of the S&P 500. As you can see from Exhibit 5 below, the two used to move more or less in parallel lines but not anymore.

Listed equities react to surprises in reported earnings, particularly to surprises in operating earnings. When operating earnings are good, investors reward the company in question, but operating earnings can be manipulated. By making the numbers look better than they really are, the CFO of the company in question effectively pushes a snowball in front of him, and that system will also have to be cleared one day, just like central bankers cannot continue to avoid D-Day.

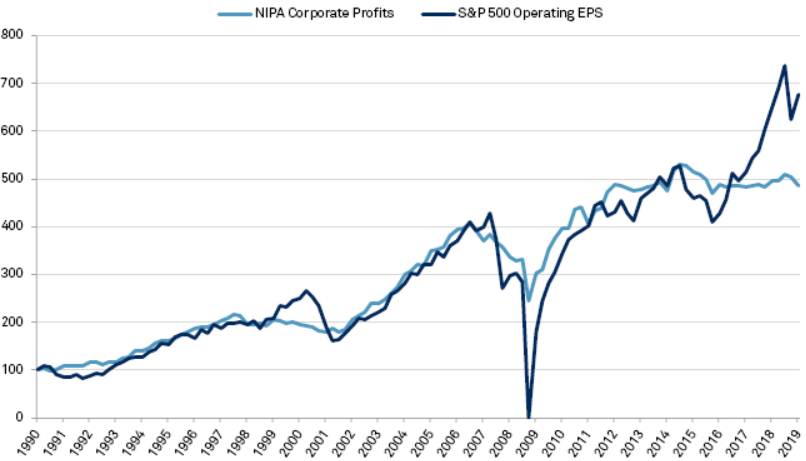

Problem #3: S&P 500 operating profits are out of sync with NIPA profits, meaning that US equities will mean-revert at some point. (NIPA stands for National Income and Products accounts and include corp. profits from non-financial companies.)

In the US, there is something called NIPA profits with the underlying data originating from the national accounts. As you can see from Exhibit 6 below, S&P 500 operating profits and NIPA profits used to move hand in hand, but companies have figured out a way (don’t ask me how they do it) to ‘cheat’ the system. Longer term, the two measures of corporate profits must grow more or less 1:1, so the current situation is unsustainable. At some point in the not so distant future, a mean reversion will spoil the party and bring misery to investors in US equities.

Exhibit 6: S&P 500 operating EPS vs. NIPA corporate profits Source: Standard & Poors Global Market Intelligence

Investment implications

The investment implications are obviously quite dramatic. When US equities are as expensive as they currently are, when US equity prices are elevated relative to underlying corporate profits, and when those corporate profits are unsustainably high compared to NIPA profits, how can I expect anything else but for US equities to mean-revert at some point in the not so distant future?

It actually reminds me of the days leading up to the collapse of the Japanese equity market in 1990 when, in the mid to late-1980s, Japanese investors chose to ignore some simple facts that were blatantly obvious to the rest of us. For quite a while, we all looked stupid as the equity party in Japan lasted longer than we all predicted – quite similar to the current situation in the US, where you are deemed almost non-patriotic if you are not gung-ho on US equities.

I mentioned earlier that US wealth is bound to mean-revert at some point. Total US wealth adding up to 520% of GDP is not sustainable, and equity holdings account for a significant share of total US wealth. In other words, the anticipated (and inevitable) mean reversion of wealth could go hand in hand with the forthcoming mean reversion in US equity markets.

As far as the rest of the world is concerned, don’t expect other markets around the world to detach themselves from US markets. Although wealth-to-GDP is not nearly as much out of sync elsewhere, I would expect a bear market in the US to have at least some impact on other equity markets, hence our recommendation to keep the equity beta to a minimum until further notice, but that doesn’t mean there is nothing to invest in.

I have recently identified two investment opportunities both of which you’ll find on ARP+, namely shipping and uranium (my paper on uranium will only go live in the next week or two).

Both of those opportunities are big mean-reversion opportunities. The shipping industry is in its 13th bear market year, and uranium prices have struggled ever since the Fukushima disaster in 2011.

That is about as much as I plan to say about mean reversion. Next month, when I discuss Lesson #3 – “Unsustainable things can last longer than you anticipate.” – I will return to the Japanese experience of the late 1980s, I will look at similar examples from other parts of the world, and I will explain why investors are sometimes unprepared to apply simple logic when investing.