As 2020 began, market expectations were positive. We expected longer-term interest rates to rise and that the upside momentum in stocks would continue—barring a catalyst to spark a reversal in overly optimistic investor sentiment.

Well, the coronavirus epidemic did just that, resulting in a quick sell-off in stocks in late January. Although stocks quickly reversed and surged to new highs—amid expectations that the outbreak would peak and central banks would step in to support growth—10-year Treasury yields fell and have only marginally recovered. We have since reduced our upside outlook for rates, which is an important component of our Sector Views research process.

However, at this point we believe the global recovery simply may be on hold until later in the year, if the historical pattern of market response to epidemics holds true. Typically, stocks have experienced a short-term dip followed by the continuation of the market’s upward trend.

Meanwhile, the Democratic primary, where the moderates are pitted against the liberals, is affecting the relative performance of the health care sector. All candidates have endorsed the idea of the federal government taking a larger role in health care, whether by building on the Affordable Care Act or instituting a single-payer, national health insurance program.

Bottom line, we’re monitoring the impact of the ongoing uncertainty, but the fundamental underpinnings of our sector calls remain in place. At least for the time being, we’re not making any changes to our sector ratings. However, here are some of the issues that are affecting sectors:

Coronavirus may have an impact on sector performance

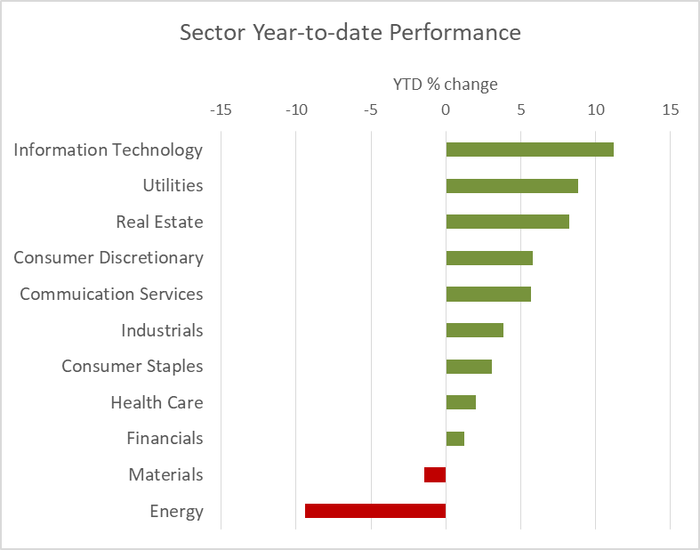

Many companies potentially could be affected by coronavirus (COVID-19), whose epicenter is an important manufacturing region of China. However, with the exception of the Materials and Energy sectors—which have seen sharp market declines year to date—the market impact so far has been mostly limited to industries within sectors that source their inputs from or sell their goods and services to China.

For example, we haven’t seen a broad impact on the Information Technology sector. However, within the Technology sector, industries such as electronic equipment and components, communications and some of the semiconductor companies have seen sharp market weakness. Integrated circuits, liquid-crystal display (LCD) components, automotive components, industrial machinery, air freight, luxury goods, oil and gas and chemicals are among the list of products and services flowing into and out of China that are likely to be affected the most.

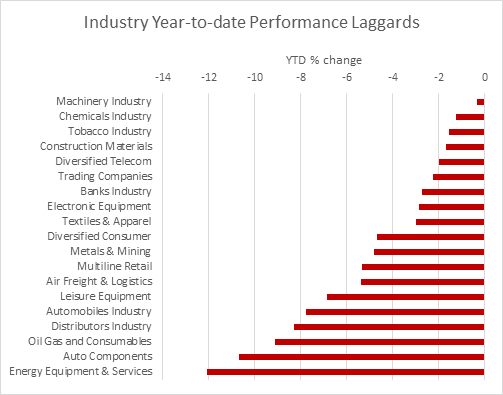

Industries including energy equipment/services and auto components have lagged this year

Source: SCFR, Bloomberg, as of 2/17/2020 Past performance is no guarantee of future results.

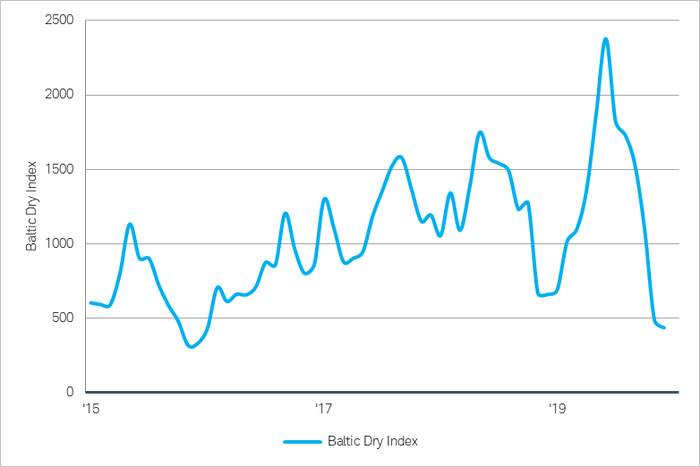

Besides the sharp market weakness in the Energy and Materials sectors, signs of the slowdown in trade have been seen in some economic indicators. For example, the Baltic Exchange Dry Index, which reflects the shipping rates for various dry bulk commodities like industrial metals, coal and grain, has fallen to its lowest level since 2016 as shipping to and from China has ground to a halt. We are monitoring other high-frequency data for signs that the global economy is being affected by the epidemic.

The Baltic Exchange Dry Index has dropped as shipping to and from China slowed

Source: SCFR, Bloomberg, as of 2/17/2020. The Baltic Dry Index (BDI) is issued daily by the London-based Baltic Exchange. The BDI is a composite of the Capesize, Panamax and Supramax Timecharter Averages. It is reported around the world as a proxy for dry bulk shipping stocks as well as a general shipping market bellwether. Past performance is no guarantee of future results.

Coronavirus has had an indirect impact on other sectors

Other sectors, such as the Financials, Real Estate and Utilities sectors, have been indirectly affected by the epidemic and by concerns about its potential influence on global growth. One of the factors that has felt an outsized impact is interest rates.

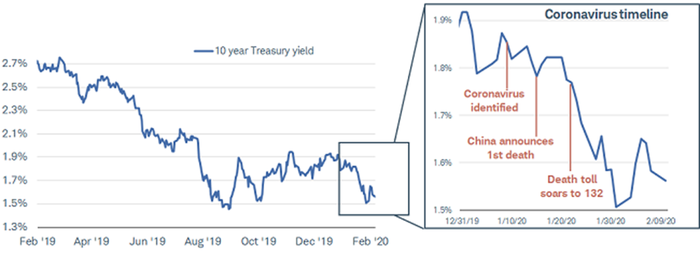

10-year Treasury yields are still well below pre-coronavirus levels

Source: SCFR Bloomberg. Daily data as of 2/10/2020. Past performance is no guarantee of future results.

While stocks rebounded quickly, interest rates did not. After trending higher in Q4 2019, rates began slipping at the start of the year, just as the coronavirus was identified (see chart above). To a large extent, that’s because the U.S. economy is likely the best positioned to withstand the impact of the epidemic compared to other economies around the globe—particularly China. The shock to China’s economy—the second-largest in the world—is reverberating around the globe, sending investors fleeing to the safety of Treasuries, driving the value of the U.S. dollar higher and U.S. bond yields lower.

This has had an outsized impact on the relative performance of Financials (which tend to underperform when interest rates fall) and Utilities (which tend to outperform when interest rates fall). And with stocks rising at the same time that yields have fallen, real estate investment trusts (REITs) have had a double tailwind. This is very similar to what we saw in mid-2019, when both cyclical and defensive sectors outperformed the broader market.

Energy and Materials have underperformed year to date

Source: SCFR, Bloomberg, as of 2/17/2020 Past performance is no guarantee of future results.

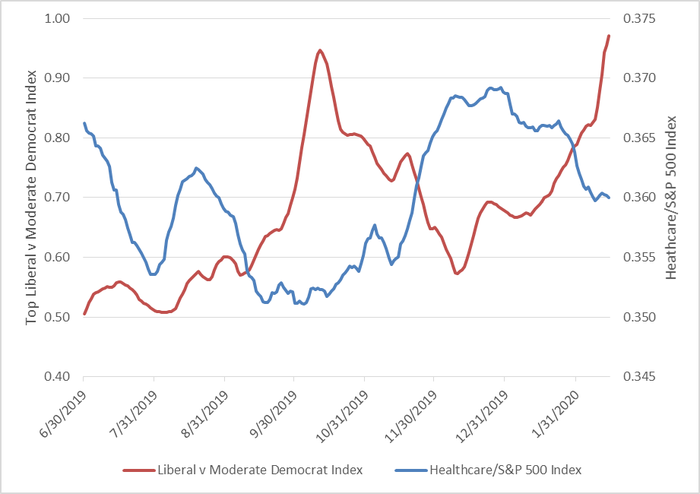

Meanwhile, Democratic primaries have raised uncertainty about health care

As we move through the Democratic presidential primary season, we’ve seen a change in leadership in the polls, and that has affected the relative performance of the sector. In the national average of polls tallied by RealClearPolitics, Sen. Bernie Sanders (a liberal Democrat) has taken over leadership from former Vice President Joe Biden (a moderate Democrat). We can see a clear relationship to the relative performance of the health care sector. In the chart below, a rising red line reflects the top liberal Democrat rising in the national average poll relative to that for the top moderate Democrat over the past eight months. In the last couple of months, the health care sector (blue line) has underperformed the broader market amid the rising popularity of Sanders and slide in Biden’s polling numbers. However, the recent rapid rise in Bloomberg CEO Michael Bloomberg’s poll numbers could reverse this trend, as he closes in on Biden for the top moderate spot.

Health Care sector relative performance has declined as liberal candidates have risen in polls

Source: Charles Schwab as of 2/17/20 Top Past performance is no guarantee of future results.

We are maintaining our current views

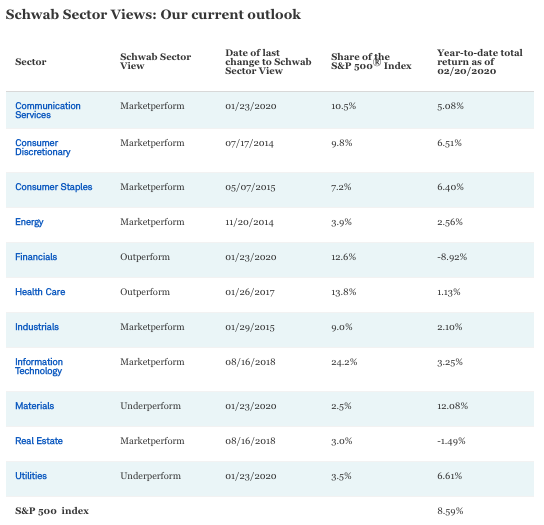

As we’ve penned in previous Schwab Sector Views, we have a process for making our sector calls. (You can read more about this process in the footnotes of the table below.) An important pillar of the process involves our economic outlook, which includes our outlook for interest rates. Amid growing signs of a global economic rebound, we recently initiated an “outperform” rating to Financials and “underperform” ratings on Utilities—which was consistent with our expectations for a rise in interest rates.

However, with the threat of the coronavirus becoming a pandemic, there are questions as to whether global economic stabilization or recovery is sustainable. We think that it could simply be delayed until later in the year. In this environment, we’ve lowered our expectations for the 10-year Treasury. At the current rate of about 1.6%, we don’t expect a significant interest rate headwind or tailwind for the interest-rate-sensitive sectors, including Financials and Utilities.

As a result of the current uncertainties, we’re not taking a particularly bullish or bearish macroeconomic view. So, as part of our weight-of-the-evidence approach, we are looking to the fundamental and valuation factors that we track for each of the sectors. Currently, they argue for maintaining our current views.

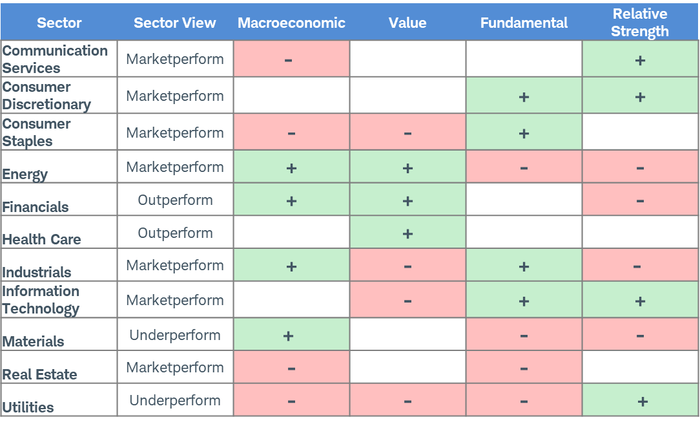

Sectors overview

Note: Each of the sector lenses shown above—Macroeconomic, Value, Fundamental and Relative Strength—is both intuitive and evidenced-based in nature. Within each, there are a varying number of factors. The Macroeconomic lens includes sector sensitivities to interest rates, stocks and the value of the U.S. dollar; the outlook for each of these is determined by the Schwab Center for Financial Research (SCFR)’s Asset Allocation Working Group, which uses a mosaic approach of quantitative and qualitative considerations. Value includes six different valuation metrics that provide a holistic perspective on current valuations relative to each of the sectors’ own historical valuations, as well as relative to the other sectors. Fundamental provides insight as to how efficiently the companies within each sector use invested capital to produce earnings; this historically has been informative as to future relative performance of the sectors. Finally, Relative Strength measures momentum of the individual sectors against all of the other sectors. We also consider the data in the context of factors outside the scope of these indicators—for example, geopolitical risk or central bank policy changes.

Source: Charles Schwab, as of 2/17/2020.

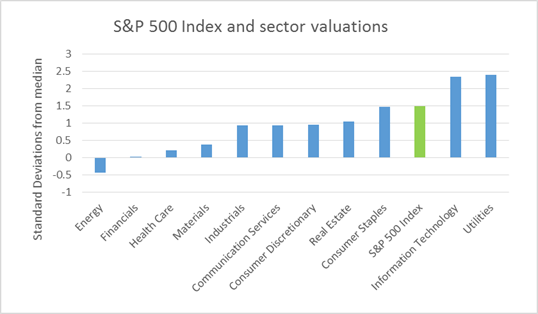

The Financials and Health Care sectors have average fundamentals, but both have among the most attractive relative valuations (Energy has the best, but we think that could be a value trap – it looks cheap but is unlikely to sustainably outperform).

Energy, Financials and Health Care have relatively low valuations

Source: Charles Schwab, as of 2/17/2020 Valuations include six different valuation metrics that provide a holistic perspective on current valuations relative to each of the sectors’ own historical valuations, as well as relative to the other sectors. Standard Deviation is a quantity calculated to indicate the extent of deviation for a group as a whole.

For the Materials sector, even if growth picks up later this year, still-tepid global growth is not expected to provide an enduring tailwind to industrial metals or demand for chemicals. Relative valuations are okay, but fundamentals remain poor. While revenue growth is expected to recover from a deep drawdown in 2019, only modest growth is expected over the next two years.

As for Utilities, while their defensive nature of utilities can be attractive in uncertain times, we are increasingly concerned about valuations, which have risen to well above historical levels, and any recovery in interest rates could be a significant headwind.

A final word

Keep in mind that no matter what our view is on any of the sectors, remaining diversified is very important. Concentrating in too few sectors can dramatically affect the risk profile and performance of your portfolio. So if you do make any sector tilts in your portfolio, keeping them small is a good way to maintain appropriate diversification and potentially enhance the performance of your portfolio.

Source: Schwab Center for Financial Research, FactSet (for YTD total returns) and S&P Dow Jones Indices (for S&P 500 sector weightings). Sector performance data is based on total return for each S&P 500 sector subindex (see “Important Disclosures” for index definitions). Sector weighting data is as of 1/31/2020; data is rounded to the nearest tenth of a percent, so the aggregate weights for the index may not equal 100%.

Past performance is no guarantee of future results.

Important Disclosures:

Schwab Sector Views do not represent a personalized recommendation of a particular investment strategy to you. You should not buy or sell an investment without first considering whether it is appropriate for you and your portfolio. Additionally, you should review and consider any recent market news. Supporting documentation for any claims or statistical information is available upon request.

All expressions of opinion are subject to change without notice in reaction to shifting market or other conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Diversification and asset allocation do not ensure a profit and do not protect against losses in declining markets.

Market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

The policy analysis provided by Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

Risks of the REITs are similar to those associated with direct ownership of real estate, such as changes in real estate values and property taxes, interest rates, cash flow of underlying real estate assets, supply and demand, and the management skill and credit worthiness of the issuer.© Schwab Charitable

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

The Schwab Center for Financial Research (SCFR) is a division of Charles Schwab & Co., Inc.

© Charles Schwab & Co.

© Charles Schwab

More Alternative Investments Topics >