NewsLetter - February 2020

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsCAVEAT EMPTOR

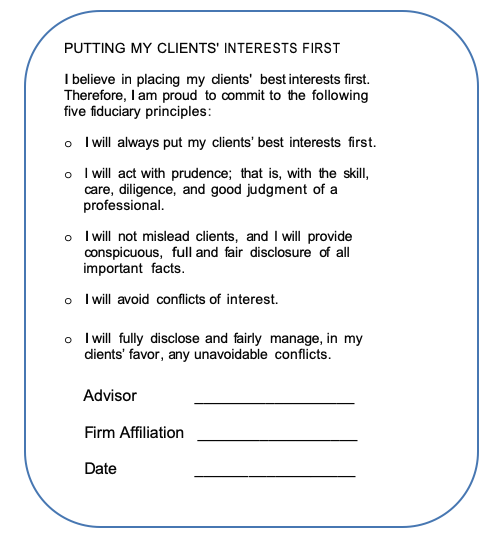

I’m not sure how comfortable this would make me feel if I were a client; however, as Barbara Roper notes at the end, it is an impressive effort to meet the new CFP Board standards.

“Northwestern’s CFP disclosures put industry’s fraught questions in focus” – Financial Planning

“More than 1,000 CFPs affiliated with Northwestern Mutual now have to make their conflicts of interest abundantly clear and explain how they manage them in clients’ best interests.

“The insurer and broker-dealer has created a disclosure document intended to comply with the CFP Board's new code of ethics and standards of conduct. In the document, advisors tell planning clients outright that they’re incentivized to ‘sell Northwestern Mutual insurance products to a client often’ – and for the highest possible commissions.

“The CFPs at Northwestern also have a financial interest in selling permanent life insurance with higher initial premiums than term products. They’re encouraged ‘to sell more expensive products and services to you which will have the effect of increasing my compensation,’ the document states. They can be paid on an ongoing basis for selling a Northwestern variable annuity in a brokerage account with less than $50,000, but not for selling a mutual fund, the brochure says.

“‘I know that in the long run, I will benefit most by serving you well,’ it says later. ‘Your interests and my interests align in this respect because I rely heavily on the referrals I receive from satisfied clients. This in itself helps to mitigate the material conflicts of interest described above.’”

Financial Planning obtained the remarkable 8-page template, which is entitled “My commitment to you as a CFP professional.” The traditional brokerage and insurance incentives don’t stand out as much as the firm’s “sincere effort to explain those conflicts clearly,” according to Barbara Roper, director of investor protection for the Consumer Federation of America.

“I’ve read a lot of these types of documents over the years, and this is clearer than most, Roper said in an email.”

STAR SPANGLED BANNER AS YOU’VE NEVER HEARD IT

And my friend Freddie said they left out the last two words: “Play ball!”

He also added some background… https://www.smithsonianmag.com/history/the-story-behind-the-star-spangled-banner-149220970/

CREDIT SCORE MYTHS

From the Wall Street Journal:

“Some common myths include: checking credit scores can hurt the credit score (a ‘hard inquiry’ where a financial firm is evaluating a potential loan so you can have an impact, but a ‘soft inquiry’ like an employer conducting a background check does not, nor does a soft inquiry of checking your own credit score); paying bills on time is all you need to worry about (it’s not, as ‘credit utilization’ also matters, because paying on time but always being maxed out is a negative compared to ‘just’ using 30% of your available credit each month, which can be remedied by spending less or simply asking for a credit limit increase); carrying a balance helps boost the credit score (it doesn’t; it just racks up interest charges!); closing an old card with a high interest rate will help (it doesn’t, and closing a long-standing card can actually reduce the score by reducing the average age of your credit accounts); opening a new retail card at a 0% rate is good for your score (it’s not; it’s a hard inquiry that’s more likely to reduce the score); shopping for a mortgage/auto/student loan hurts the credit score (hard inquiries matter, but if multiple hard inquiries come together, they’re bundled together as a single query and recognized as a single transaction that reflects the borrower is likely just shopping around); and assuming credit reports are accurate in the first place (the FTC found in 2012 that 21% of consumers had errors, with 5% of the cases so serious it impaired their credit… which means it really is important to monitor your credit score to ensure credit events are being reported properly!)”

https://www.wsj.com/articles/9-myths-about-credit-scores-11571623800

SMILE FOR THE DAY

From my friend Bill

EXCLUSIVE: CALPERS FIRES MOST OF ITS EQUITY MANAGERS

Excerpts from Chief Investment Officer

Better late than never?

In a major investment move, the California Public Employees’ Retirement System (CalPERS) has terminated most of its external equity managers, slashing their allocation to $5.5 billion from $33.6 billion. Only three of 17 external equity managers have been spared in the reduction …

The memo, which has not been publicly discussed, says the moves are necessary because of long-term underperformance. The memo obtained by CIO says that Meng is putting a “renewed focus on performance and our ability to achieve our 7% assumed rate.”

Meng, who took over as CalPERS’s CIO in January, has repeatedly expressed concerns, not only about CalPERS achieving the 7% assumed rate of return …

“Over the last five years, traditional managers have underperformed their benchmarks by 48 bps and emerging mangers by 126 [bps],” the memo says…

Over the last decade, CalPERS has moved to managing most of its $187 billion in equities in-house, the majority of the strategies index-based [my emphasis]…

Good luck on the 7% assumed rate of return!

CAPABLE

If you or a family member is facing health issues threatening their ability to remain in their home, you might check CAPABLE. The Community Aging in Place—Advancing Better Living for Elders (CAPABLE) project addresses both function and cost. CAPABLE is a program developed at the Johns Hopkins School of Nursing for low-income seniors to safely age in place. The approach teams a nurse, an occupational therapist, and a handyman to address the home environment and uses the strengths of the older adults themselves to improve safety and independence.

https://nursing.jhu.edu/faculty_research/research/projects/capable/

SOME INTERESTING TID BITS

From my longtime friend David:

THE RISK OF JUST ONE STOCK: 56 individual stocks within the S&P 500 are up at least +50% YTD through the close of trading last Friday, 11/29/19, including 11 stocks that are up at least +75% YTD. There are also 13 stocks that are down at least 30% YTD, including 4 stocks down at least 50% (source: BTN Research).

NEVER BEFORE: The USA exported more barrels of crude oil and petroleum products in both September and October this year than it imported, the first time that our nation's oil exports have exceeded its imports based upon monthly records maintained since 1949; i.e., the last 70 years (source: Energy Information Administration).

THE KIDS INHERIT AND THEN THEY SELL: There are 79.5 million owner-occupied homes in the United States as of 9/30/19. By the year 2037, 21 million of the 79.5 million homes (26% of all current homes) are projected to have a change of ownership as the "Baby Boomer" generation dies. (source: Zillow).

HEALTH INSURANCE: In 2018, the average American employee paid $453 per month for his/her family's health insurance coverage through an employer-sponsored plan. That $453 amount represented 28% of the total cost of the insurance coverage; i.e., the employer paid $1,164 per month (source: Commonwealth Fund).

LONG-TERM GUESS: When President Franklin D. Roosevelt proposed the Social Security retirement program in 1935, FDR's financial people projected that total Social Security expenditure would reach $1.3 billion in 1980, or 45 years into the future. The actual Social Security outlays in 1980 were $149 billion. Thus, the analysts' 1935 estimate represented less than 1% of actual 1980 Social Security expenditures (source: Social Security).

SAME SONG, SECOND VERSE

From the S&P Persistence Scorecard

For funds categorized as top performers in September 2017, 47% maintained their top-quartile performance the subsequent year. However, there was a dramatic fall in persistence afterward—just 8% of domestic equity funds remained in the top quartile in the three-year period ending September 2019. This result (8%) is consistent with the notion that historical performance is only randomly associated with future performance.

An inverse relationship exists between the time horizon length and the ability of top-performing funds to maintain their success. Less than 3% of equity funds in all categories maintained their top-quartile status at the end of the five-year measurement period. In fact, no large-cap fund was able to consistently deliver top-quartile performance by the end of the fifth year.

DOESN’T MATTER WHERE YOU LIVE

From the S&P Persistence Scorecard – Latin America

Brazil…regardless of size focus, by the fourth year, no fund remained in the top quartile. Fixed income painted a slightly different picture than equities.

Chile…just 27% of top-performing funds in the first 12-month period repeated their outperformance in the subsequent period. This rate dropped to 9% in the third period and to 0% in the fourth and fifth periods.

Mexico … After one year, just 18% of managers remained in the top quartile, and by year two, the percentage dropped to zero… Top-quartile managers in the first five-year period were more likely to move to the bottom quartile (38% of managers) in the second five-year period than to any other quartile.

INDEX FUNDS BREAK THROUGH $10 TRILLION IN ASSETS MARK AMID ACTIVE EXODUS

Financial Times

HOW ABOUT CHASING “WINNING” COUNTRIES?

From Dimensional Fund Advisor’s “Hindsight is 20/20. Foresight Isn’t.”

The moral? Stop chasing “winners”; it’s a losing strategy.

WHO’S RICH?

From my friend Monty:

Who are the top one percent by income?

The cutoff for a top 1% household income in the United States in 2019 is $475,116.

Full story at https://dqydj.com/top-one-percent-united-states/

WHY I DON’T MAKE NEW YEAR’S RESOLUTIONS

From Parade

80% – That’s the percentage of New Year’s resolutions that fail by February.

MY BIGGEST INVESTMENT LESSONS

https://finance.yahoo.com/news/biggest-investment-lessons-102600254.html?guccounter=1

Excerpts from Christine Benz, one of my favorite commentators. Christine is director of personal finance at Morningstar.

Investing is Overrated …

I'm not saying you shouldn't invest. You absolutely should. It's essential. End of story. What I am saying, however, is that investing is the attention hog in many discussions about how to reach financial goals. It's sexy, there's often a current-events hook to explain why the market is behaving as it is, and hitting it big with an investment doesn't usually require any sort of sacrifice. But, ultimately, your boring pre-investing choices – like your savings rate and how you balance debt paydown with investing in the market – will have a bigger impact than your investment selections on whether you amass enough money to pay for retirement or college. (I call these types of pre-investment decisions your "primordial asset allocation.") If your savings rate is high enough and you start early enough, that can make up for some lackluster asset-allocation and investment-selection choices. The flip side is also true: If you haven't saved enough, great investment picks probably won't be enough to save you.

Beware the Latest Fad …

In a related vein, I've seen enough to conclude that many new products that come to market don't actually help improve investor outcomes. Rather, they're an effort to help investment firms capitalize on what's hot and generate fees on new assets.

Get Some Help in Retirement …

Most people approaching or already in retirement could benefit from another set of eyes on their plans, to help ensure that their withdrawal rate system is sustainable, that they're being tax-efficient with their withdrawals, and so on. Having a financial adviser who knows what's going on in your financial life and portfolio is also the gold standard for helping ensure that nothing falls through the cracks if you become incapacitated or die.

While the traditional investment advice model requires investors to pay a percentage of their assets year in, year out, soon-to-retire and retired investors who are confident in their abilities can pay for advice on an hourly or per-engagement basis. That will be more economical than paying for ongoing advice or oversight; the downside is that the hourly or per-engagement advisor won't be looking over your portfolio unless you ask for help. So, it's a trade-off.

S&P HINDSIGHT DASHBOARD

- In sharp contrast to last year, US equities triumphed in 2019, with the S&P 500® up 31%, its biggest annual gain since 2013. Easing trade tensions and Fed accommodation renewed optimism about the economic outlook. Mega-caps dominated as gains for the S&P MidCap 400® and the S&P SmallCap 600®, 26% and 23% respectively, lagged the S&P 500.

- International markets also gained, with the S&P Developed Ex-US BMI up 23% and the S&P Emerging BMI up 20%.

High Beta was the best performing factor, followed by Quality; not unrelatedly, Information Technology was the best performing sector, up a remarkable 50%. Meanwhile, Value outperformed Growth for the first time in three years.

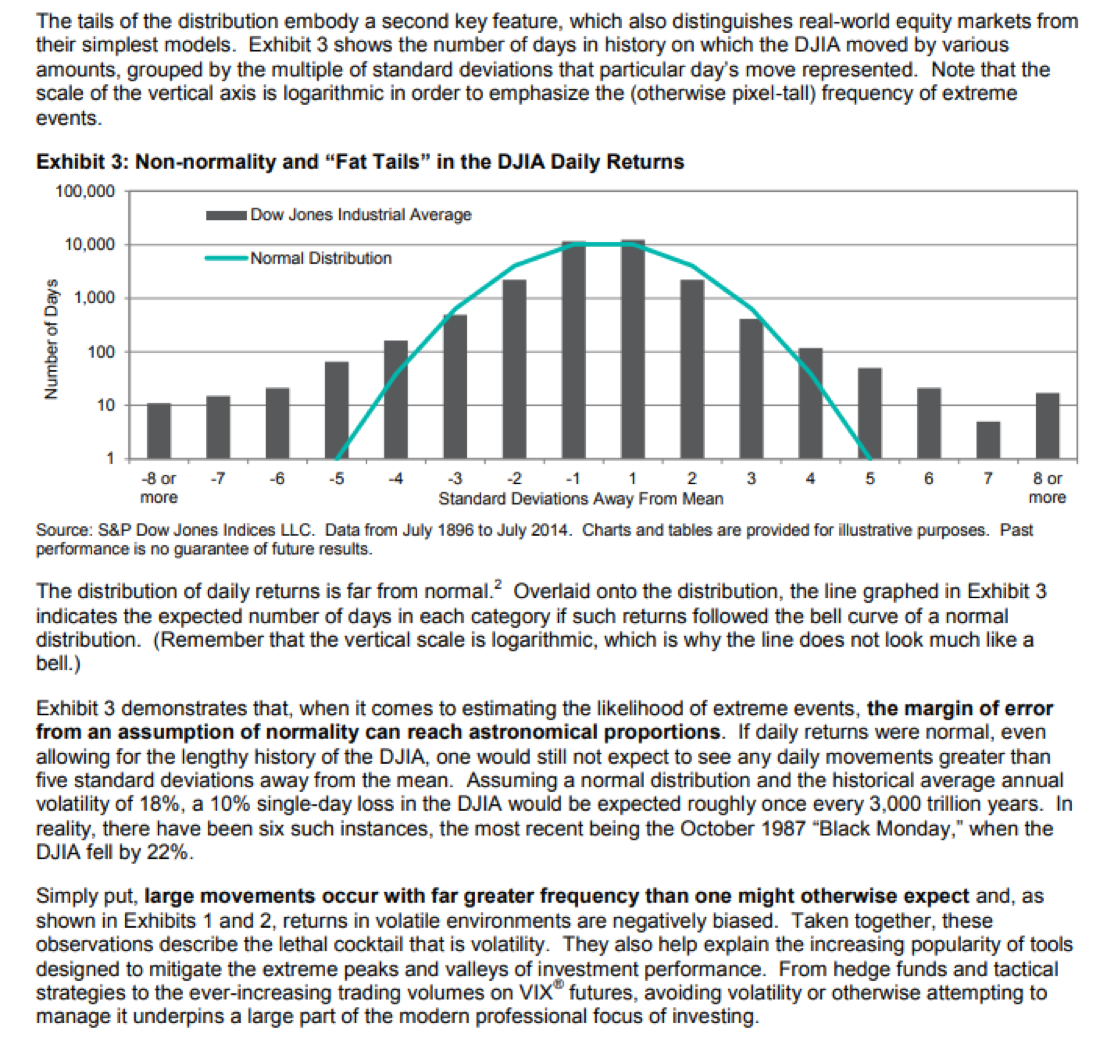

FAT TAILS

Why markets can be far more volatile than simple statistics might suggest.

- – From S&P DOW Jones Indices: The Landscape of Risk

https://us.spindices.com/documents/research/research-the-landscape-of-risk.pdf

MORE CAVEAT EMPTOR

“It’s 2020, and the chase for big commissions is back” – Investment News

“As 2020 opens a new year and decade, the broad financial advice industry is working to make it easier for brokers and financial advisers to sell high-priced, high-commission, complex products to clients, with the focus on tapping retirement accounts that hold trillions of dollars in investor savings.”

https://www.investmentnews.com/its-2020-and-the-chase-for-big-commissions-is-back-176057

THE MORAL? PROTECT YOURSELF WITH THE FIDUCIARY OATH

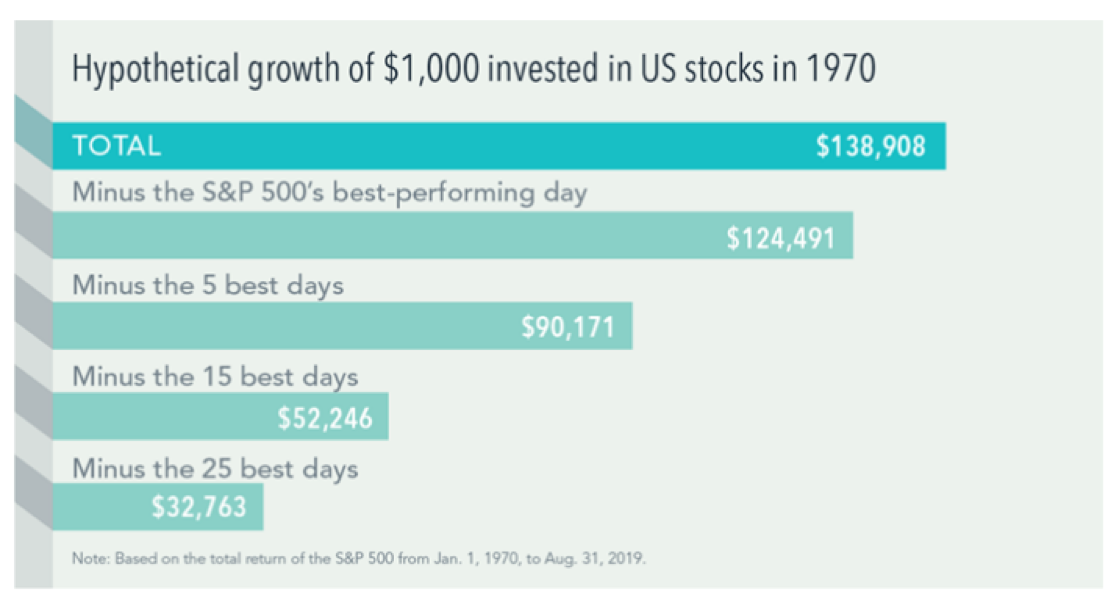

TIME IN THE MARKET, NOT MARKET TIMING

An update of a classic study from DFA.

https://www.mydimensional.com/what-happens-when-you-fail-at-market-timing

MORE TIME IN THE MARKET, NOT MARKET TIMING

From a study by Wayne Thorpe, senior financial analyst at the American Association of Individual Investors Journal, via my friend Clark Blackman’s most excellent client letter.

How painful is it if you don’t market time and have to live through a market downturn?

Since 1871, market downturns have recovered as follows:

- 3% of market downturns recover within a month

- 50% of market downturns recover within 2 months

- 80% of market downturns recover within 1 year

- 95% of the time those big "once or twice in a lifetime drops" return to even in 3 to 4 years.

- Collectively, since 1871, the time it takes for the market to recover (top to trough to top again) is a mere 7.9 months!

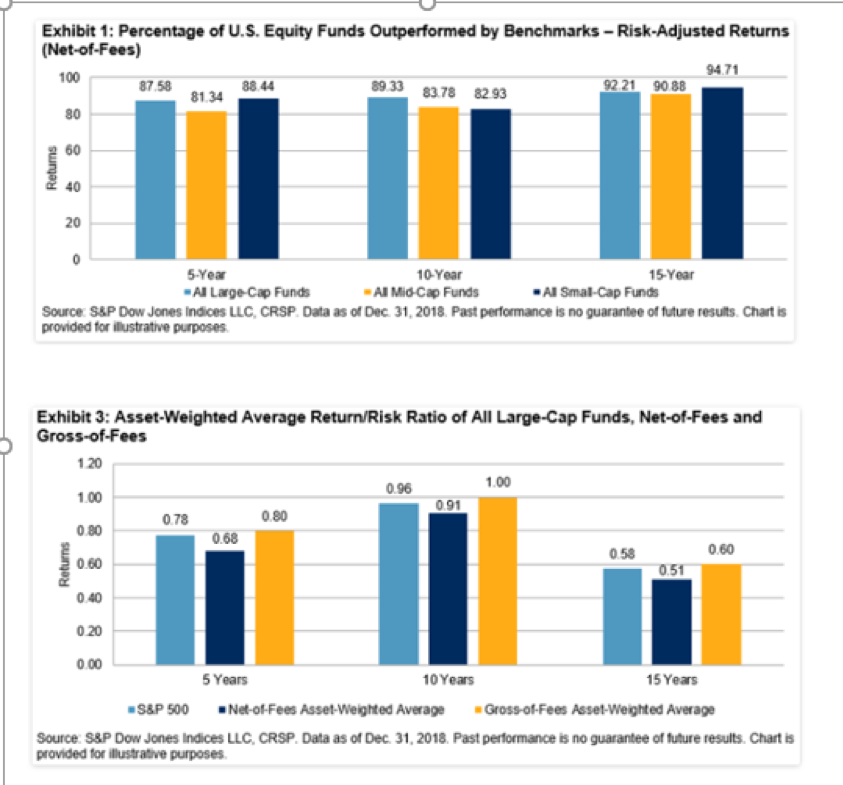

DISPELLING THE MYTH

Some interesting charts from Berlinda Liu’s (Director, Global Research & Design, S&P Dow Jones Indices) blog, “Are Active Funds Better at Managing Risk? Not Really.”

And S&P’s conclusion:

Hope you enjoyed this issue, and I look forward to “seeing you” again.

Harold Evensky

Chairman

Evensky & Katz / Foldes Financial Wealth Management

Important Disclosure

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Evensky & Katz / Foldes Financial Wealth Management (“EK-FF”), or any non-investment-related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from EK-FF. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. EK-FF is neither a law firm, nor a certified public accounting firm, and no portion of the newsletter content should be construed as legal or accounting advice. A copy of EK-FF’s current written disclosure Brochure discussing our advisory services and fees is available upon request. Please Note: If you are an EK-FF client, please remember to contact EK-FF, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. EK-FF shall continue to rely on the accuracy of information that you have provided.

© Evensky & Katz / Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management

Read more commentaries by Evensky & Katz / Foldes Financial Wealth Management

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits