Flows to private equity managers may be squeezing the illiquidity premium

Private assets are popular today as investors are reaching out on the risk spectrum for return. This behavior is always interesting to us since history shows it often leads to losses. We wanted to dig into private markets and see if excess returns are easily earned.

A brief overview

Today there are over $4.5 Trillion in private capital assets1 managed by almost 10,000 managers in the US. Twenty years ago, there were barely $500 Billion in assets, spread across 1,900 managers. Competition in these strategies has increased and the flow of money into these strategies has pushed up valuations for private businesses.

A market facilitates buyers and sellers coming together to transact. When a market is young and small, it tends to be inefficient. Skilled players can gain an edge. The outsized gains of the few attracts more competition and outside funds. At which point skilled players compete against other skilled players. Now edge is harder to come by. Increased competition drives inefficiencies out, making consistent outperformance harder. As a market matures, fees charged by the croupier (i.e. the broker) must come down.

This has already happened in public investment markets as investors learned how hard it is to outperform in this hypercompetitive arena. Michael Mauboussin’s research on the “Paradox of Skill” sums up this competitive dynamic nicely. The cost of chasing outperformance amidst high competition was the fees paid to the managers. In private markets, the cost will be higher as fees can be up to 5-6 times more.

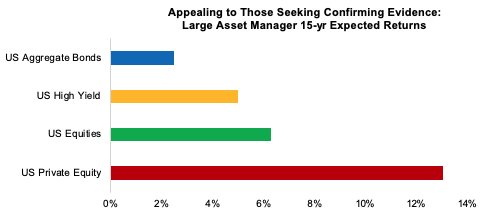

The chart below is a replication of a promotional piece we received from one of the largest asset managers in the world, indicating the prediction that private equity returns will double those of public markets over the next 15 years.

However, our anecdotal experience in talking to investors is that most have not earned outsized returns from their private asset portfolios, and the data supports their claims.

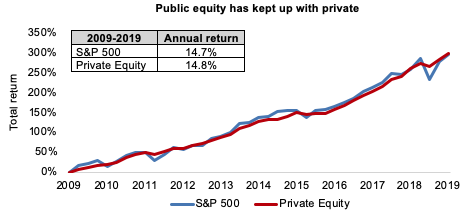

The chart below shows the performance of public versus private equity over the past decade, which was an exceptional period for all forms of equity ownership.

Source: Bloomberg. Private Equity is the Cambridge Private Equity Index. Data shown is from Q3 2009 through Q2 2019.

Interestingly, in an environment that has been favorable for all equities, especially the more leveraged ones, private equity managers in aggregate have only matched the returns of public market indices. Furthermore, such indices of private strategies ignore many inherent biases, as noted in this Financial Times article.

Academics have researched whether the increased risks of illiquidity and leverage are adequately compensated. Others have written about how private market valuations have increased, which will inevitably lead to lower returns. Could it be that too much capital has already flowed into private markets? We were curious about how much capacity private equity has and took a cut at answering this question.

How big is the investable private equity universe?

A common refrain from the private equity industry is that public equity markets are shrinking while there are hundreds of thousands of private companies. While this is true, it has no bearing on how big the investable private equity universe is. Understanding this will give more clarity on whether a capacity squeeze is happening.

It’s difficult to assess how big the private equity market is because private businesses are not required to disclose financial information unlike public companies. And just because a business exists doesn’t mean that it is investable. An owner must want to sell first for a business to be investable.

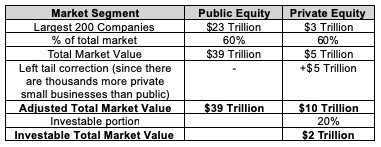

In the table below, we estimated the size of various slices of the US private equity market to comparable segments of the public equity market. We started with the Forbes list of 200 largest private businesses by revenues, estimated their total value by applying equivalent public market Price-to-Sales multiples and assumed a similar wealth distribution to public markets. We then assume 20% of these businesses could be enticed to sell to estimate the investable market size, knowing full well that this fraction is a gross overestimate. As a comparison, 4-5% of homes change hands annually in the US. Though higher prices entice more homeowners to sell, as frothy home prices caused turnover in the housing market to double prior to 2008.

In public markets, the largest 200 companies (approximately 5% of all public companies) represent 60% of total market value. Our key assumption is that this same fraction applies to private equity. For comparison, the top 5% of US households control a similar 60% of total household wealth. And this wealth distribution is likely similar to that in private equity because it will have a longer left tail than in public markets. We then take our inflated starting valuation and double it to be generous.

The result is a generous estimate of $2 Trillion dollars of private business value available for purchase. This estimate almost certainly overstates the size of private equity’s investable universe since the appropriate Price-to-Sales multiple for these companies is likely lower than their public market counterparts, and our $5 Trillion left tail correction is probably high as well. Now that we have an estimate of the investable universe, how much of that is currently invested with private equity managers?

According to a McKinsey report, this number looks to be $2 Trillion (and $5.8 Trillion in global private equity assets across equities, real estate, infrastructure and debt). But this ignores the average 1.5-2x Debt-to-Equity ratios on the average private equity deal2. Said another way, this is at least $3 Trillion in debt or $5 Trillion in total buying power. And even if our estimate of investable private business value is significantly understated, there still appears to be an excess of capital allocated to private assets.

This industry asset level versus market capacity may explain the $770 Billion in private equity capital waiting to be invested (this equates to $2 Trillion in marginal buying power). That is a lot of capital begging business owners to cash out at even higher prices.

Some of this capital will flow into public markets to take companies private. When one reason to invest in private equity is high public market valuations, will buying high and then applying a 6% fee3 deliver the promised returns?

Illiquidity premium is volatile (like any risk premium)

It is widely accepted that investors are compensated for taking the illiquidity risk of private equity. An incorrect extrapolation is that illiquidity will always pay off. This is the same reasoning people applied betting that housing prices would not fall because they never really had…until 2008.

All markets and sources of return go up and down. This is the nature of risk. When an asset is cheap or the economic environment is favorable, it will tend to deliver higher returns. When an asset is expensive its future returns tend to be lower.

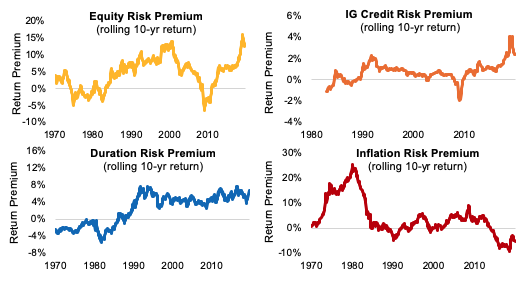

The charts below show rolling 10-year returns for various sources of risk premium – equities, credit, interest rate duration, and inflation assets (i.e. commodities). We can see each has been through multiple 10+ year periods of losing money.

Source: Bloomberg. Greenline Partners analysis

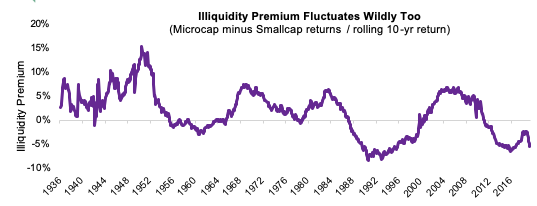

Illiquidity is no different; it is a risk with a range of outcomes.

We have proxied the illiquidity premium using micro-cap versus small-cap stocks going back to 1926. While there are certainly other methods, the important thing is seeing how this illiquidity premium has gone through multiple 10+ year periods of negative returns. We can see how this risk premium experienced a tailwind from around 1990-2010, which likely drove the current popularity of private assets.

Source: Ken French Data Library. Greenline Partners analysis

When investors fear illiquidity, the premium will tend to provide adequate compensation for the risk involved. The reverse will likely be true when investors are reaching for yield and taking illiquidity risk without regard for valuation, which may be the case today.

Implications for portfolio construction

Given the size of public versus private equity markets, what does this suggest for allocations to each asset class?

Combining public and private equity, the total equity market is worth $49 Trillion of which 20% (generously) is private equity. Capital market efficiency suggests that this is one answer to how much private equity asset owners should have out of their equity allocation. For foundations targeting 70% in total equity exposure (through equity, hedge funds and private equity), this translates to 14% of their total portfolio.

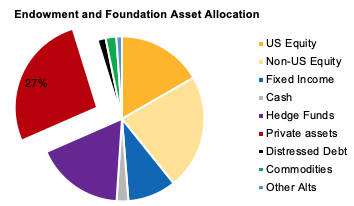

According to NACUBO studies on endowments and foundations, the average allocation to all forms of private assets is 27%, or almost triple what capital market efficiency suggests. The pie chart below shows this average asset allocation with private assets singled out.

Source: NACUBO.org

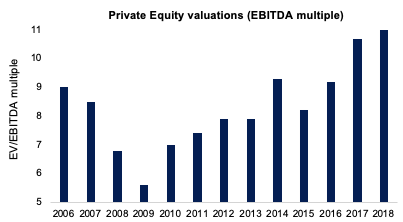

Consultants recommend increasing private asset exposure to over 40%. As more capital has moved to private assets, valuations have increased, per the chart below. Further increasing capital to this asset class will drive valuations even higher and therefore future returns lower. But in private markets, unlike in public markets, the feedback loop for informing mistakes and correcting course is decades hence there is likely to be more pain from misallocation of capital.

Source: Pitchbook

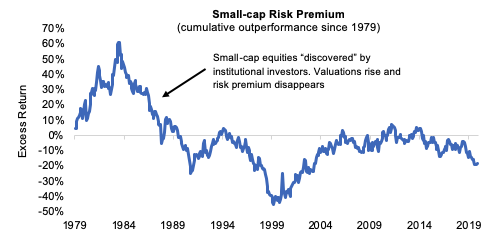

This dynamic of over-owning happened with small-cap equities when they first gained a slice of institutional portfolios in the 1980's. The chart below shows small-cap return relative to large-cap since 1979. As investors piled in, the return premium disappeared. Also, note how small-cap went through a stretch of underperformance in the 1980’s after their initial popularity.

Source: Bloomberg, Greenline Partners analysis

Markets have a way of arbitraging away excess returns. This example of small-cap may be analogous to how private equity plays out relative to public markets.

Lastly, we ask the question of whether an allocation to private equity is necessary for optimal diversification? The short answer is no.

The marginal benefits of diversification decline with each additional holding as the chart below shows. It is difficult to diversify away additional risk after the 20th holding.

We have written previously how the performance of the Dow index of 30 stocks is almost identical to that of the S&P 500 despite important differences in index construction (price weighted vs size weighted, 30 stocks vs 500, etc). Similarly, institutional investment portfolios with hedge funds, private equity and other complexities perform like simple two-asset portfolios of 70% stocks/30% bonds.

There is other real-world evidence showing that most portfolios are overdiversified. Some of our writings explore this, but we think there is much more to be learned on this topic.

Going back to private equity, our calculations show the asset management industry already controls more assets than the entire investable US private equity universe. Despite this headwind to future performance, investors seem inclined to keep allocating even more.

Usually the best opportunities in markets are those with structural headwinds, whether temporary or permanent. This begs the obvious question, has the illiquidity premium turned into a discount?

DISCLOSURES: Greenline Partners, LLC is a registered investment adviser with the US Securities and Exchange Commission. This report is not an offer to sell or the solicitation of an offer to buy any securities or instruments. Past performance is no guarantee of future performance. No part of this document or its subject matter may be reproduced, disseminated, or disclosed without the prior written approval of Greenline Partners, LLC.

The information contained herein is as of the date indicated and, to the author and Greenline Partners’ knowledge, was accurate when posted. The author and Greenline Partners LLC are under no obligation to update or remove information other than as required by applicable law or regulation.

1 Prequin

2 The Determinants of Leverage and Pricing in Buyouts, Journal of Finance 68 (6), 2223-2267.

3 Døskeland, T.M., Strömberg, P. (2018). Evaluating Investments in Unlisted Equity for the Norwegian Government Pension Fund Global (GPFG), Report for the Norwegian Ministry of Finance.

© Greenline Partners

Read more commentaries by Greenline Partners