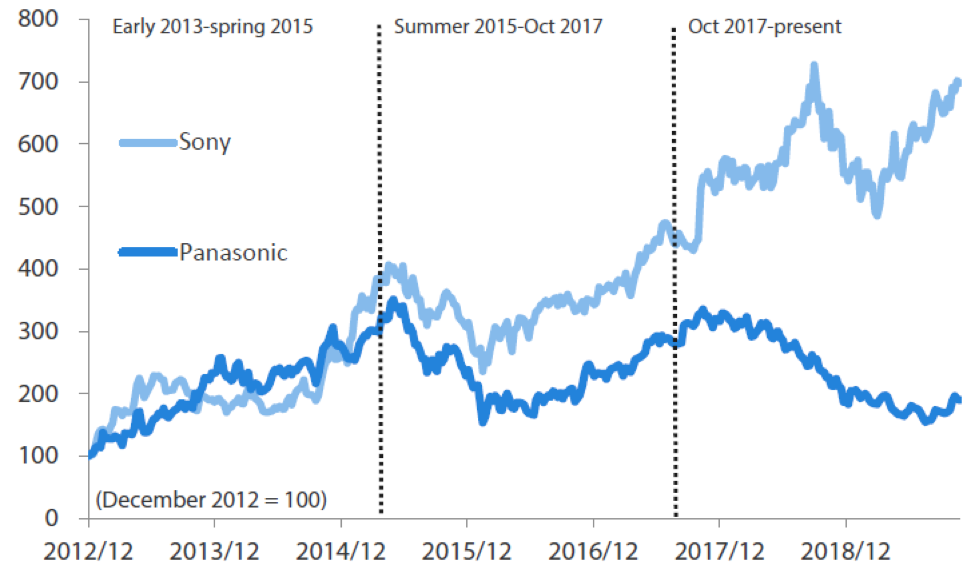

It has been seven years since the Abe administration's economic stimulus was launched. The Nikkei Stock Average has more than doubled in price since “Abenomics” started late in 2012. But, as is often the case when the market rises, not every company has benefitted from the surge that has taken place over this period. As Chart 1 shows, there have been obvious winners under Abenomics (e.g. Sony) and those that could be called losers (e.g. Panasonic)—which raises the question, how did the fortunes of these companies come to diverge so clearly?

Chart 1: Fortunes of Sony, Panasonic have diverged under Abenomics

Source: Bloomberg

Initial phase: Rising in tandem (early 2013–spring 2015)

- Both Sony and Panasonic come under new management and undertake bold restructuring

- Sony, Panasonic share prices each gain 2.5 times during this phase as financial markets applaud steps taken by the firms

In the initial phase of Abenomics, the two companies traced a similar path, as Chart 1 shows. The share prices of both Sony and Panasonic surged during this period, more than doubling at about the same rate. This is explained by the market’s positive reaction to the massive restructuring both companies initiated under new management in a bid to reform. For example, Sony sold its Vaio personal computer business, departing with a product long associated with the company. Panasonic, for its part, liquidated its massive plasma display-manufacturing plants.

Second phase: Crucial choices made (summer 2015–October 2017)

- Sony focuses on software, pours resources into CMOS optical technology

- Panasonic opts for hardware, teams up with Tesla to pursue EV battery production

While the financial markets lauded the efforts made by Sony and Panasonic during the initial phase of Abenomics, it was then time for the two companies to go on the offensive after consolidating their gains. How they approached this new phase has had lasting consequences. Sony, for its part, opted to pour resources into developing complementary metal-oxide semiconductor (CMOS) image sensors. CMOS optical technology is used in a variety of digital camera devices to process images; a recent example is the Apple iPhone 11, which uses Sony’s “only one” CMOS image sensing software to process photographs captured by the multi-lens smartphone.

Chart 2: Sony and Panasonic–Critical inflection points

Source: Bloomberg

Panasonic, on the other hand, opted to invest in electric vehicle (EV) technology. Expecting the EV market to boom, the company teamed up with Tesla. Panasonic went all out, forming a one-trillion yen strategic framework and built a factory to produce EV batteries. Prospects looked good at the time; EV technology was expected to spread rapidly around the world, and Panasonic hoped this would turn it into an undisputed winner.

Third phase: Sony pulls ahead (October 2017–present)

- Sony’s focus on CMOS optical technology pays off

- Panasonic gets mired in a EV battery price war

But as Chart 2 shows, the scenario did not turn out to be so rosy for Panasonic, whose stock price clearly began to lag that of Sony towards the end of 2017. Panasonic fell behind as it persisted its focus on EV batteries and other hardware. EV battery technology had ceased evolving for the most part, leaving little room for new innovation. The firm subsequently began to face competition from rivals, and ended up in a price war with Chinese competitors who leveraged existing technology and mass-produced EV batteries. Panasonic’s profitability slipped and its share price slumped.

In contrast, Sony, which had previously gone through bitter experiences with digital cameras, televisions, personal computers and other hardware, didn’t hesitate in making a drastic shift towards software. The bold switch included investments in image sensors, games, music and movies. This paid off in October 2017, when Sony reported record earnings for the first time in two decades.

Aftermath: Panasonic recognises the need for change-based growth

Panasonic’s stock price has recently begun to rise again; company CEO Kazuhiro Tsuga said at a briefing in November that “future growth is difficult to envision if it is based on existing businesses”. He stressed the importance of constant change. At the start of Abenomics, while Panasonic withdrew from LCDs and televisions and undertook painful restructuring in an effort to change and grow, its attempt was still based on pre-existing businesses. Sony, in contrast, realised the importance of founding future growth on change. The result was the gaping chasm between the two companies’ corporate value.

Key takeaways

There are two key lessons to be learned from the story of Sony and Panasonic: the importance of keeping abreast with constantly-changing market trends (adaptation to change) and possessing “only one” technology (innovation).

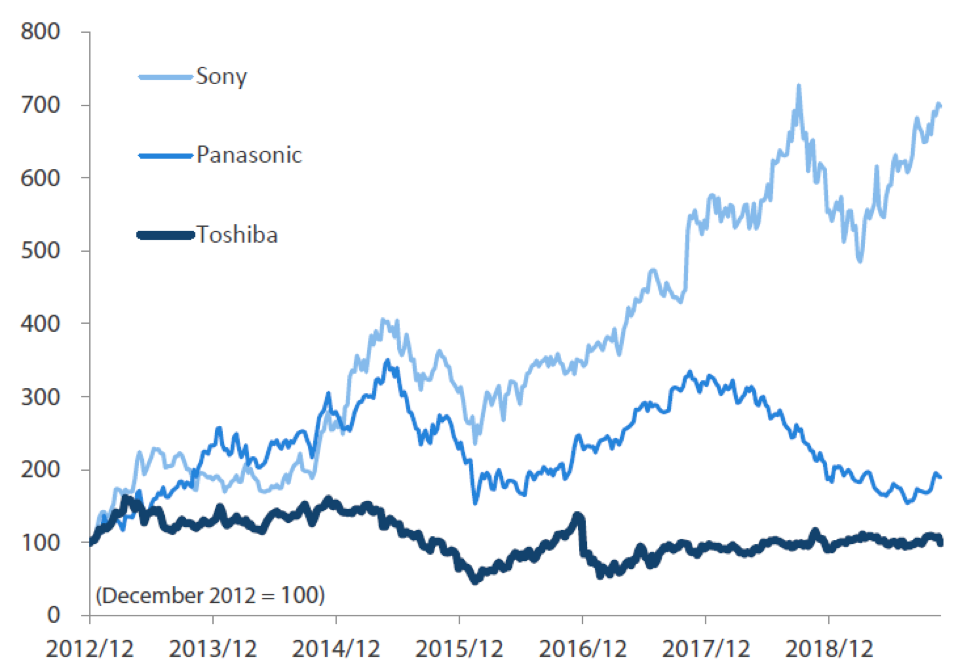

Lastly, it is worth looking at the recent fortunes of another company: Toshiba. Chart 3, which shows how the company’s share price has fared during the Abenomics era, speaks for itself. Over the past seven years, Toshiba has been mired in fraudulent accounting (May 2015), and its US nuclear unit Westinghouse suffered massive losses (December 2016). It failed to act while its electronics rivals initiated restructuring and structural reforms in the early days of Abenomics. The company was demoted to the TSE’s second section from the first section in August 2017 and ended up selling its memory chip subsidiary, Toshiba Memory, in 2018. Its performance can be summed up in one phrase: an absence of governance. “Governance”, the aforementioned “adaptation to change” and “innovation” represent key factors necessary for the sustained growth of a company, regardless of industry.

Chart 3: Toshiba–a clear laggard

Source: Bloomberg

Another lesson that can be learned from the experience of these three companies is the importance of being able to identify stocks that can produce alpha during market turbulence. In the aforementioned first phase (early 2013–spring 2015) seeing that Sony and Panasonic were headed for initial significant gains was perhaps the easy part. But when both companies’ share prices began declining at the beginning of 2015, the ability to identify that Sony’s could eventually pull out of the downturn assured future alpha. The ability to identify potential alpha requires seeing through the waxing and waning of stock prices. In short, it is about picking out the next Sony—a company whose share price may currently be at a modest level but that possesses enough potential drivers to produce future alpha.

© Nikko Asset Management

Read more commentaries by Nikko Asset Management