One of the exciting buzz words among advisors and institutional investors is ESG, which stands for Environmental, Social and Corporate Governance. This subject is almost always granted a wonderful panel reception at any conference our firm attends as it is the topic du jour. The ESG filter or screen does not have any consensus in the marketplace. The filters are chosen by each investment management organization or by the owners of the securities. In many cases, this entails not owning fossil fuel companies and avoiding other companies that meet an economic need, but are viewed as harming the future of society and the world in the eyes of specific investors. To help investors briefly understand it, it would be analogous to faith-based organizations seeking to avoid sin stocks (alcohol, firearms and tobacco) due to their personal convictions. We would like to look at ESG through an economic lens using Newton’s Third Law.

Sir Isaac Newton’s Third Law of Physics states, “For every action, there is an equal and opposite reaction.” We would like to start with the “action” first to see where ESG sits in Newton’s Third law.

The action of the last ten years is that growth stocks have stomped value stocks. The Russell 1000 Growth Index has produced a cumulative total return of 426.16% versus a 204.89% for the Russell 1000 Value (as noted by the chart below):

Source: Bloomberg

In a recent piece by noted writer, John Authers, he referred to this era as dominated by his imaginary manager which he dubbed “Hindsight Capital LLC.”

A weak global economy ensured problems for raw materials, particularly energy. The surfeit of production inspired by the panic before the financial crisis about “peak oil” and the search for alternatives would damage energy prices further. Meanwhile, the growth and power of the internet economy had much further to go.

Authers goes on to say that, “$100 in a long software/short energy trade would have turned into $1,971 by decade’s end, with dividends reinvested, and $1,783 on a price-only basis.”

The action of the last 10 years has been a bull market with growth producing an outsized portion of overall market returns. More tangible assets, like energy and the businesses related to it, have skipped this. Below is the total return of the XLE energy sector ETF versus the S&P 500 Index:

Source: Bloomberg

Now that we’ve established the “action,” let’s discuss why we believe ESG is the “equal reaction.”

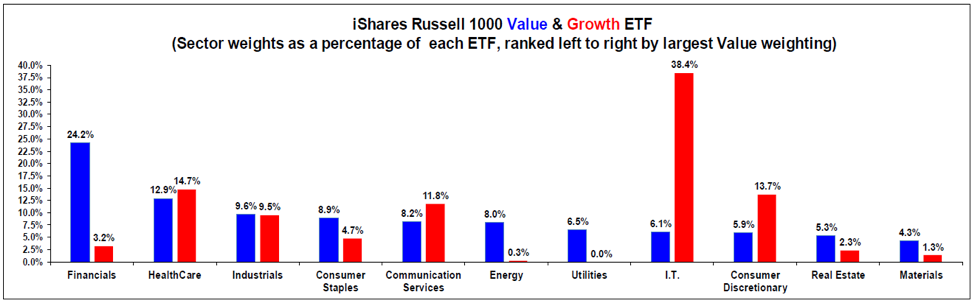

Below is a breakout of the iShares Russell 1000 Growth and Russell 100 Value ETF by sector. You’ll see there are large differences in the sector breakout, but in some places it is starker. Technology is 38.4% of the Russell 1000 Growth ETF, but this doesn’t capture all of the technology exposure. Let’s add Amazon (5.06%), Facebook (3.23%), Google in both of its share schemes (5.28%), Netflix (0.90%) and lastly the payment networks, Visa (2.11%), Mastercard (1.73%) and PayPal (0.84%), back to the information technology sector. This leaves us with an ETF that owns roughly 57.6% in technology stocks. This same number for the S&P 500 is 32.49%.

Source:iShares

The Vanguard ESG US Stock ETF is one of the largest ESG ETFs in the marketplace for investors looking to access this investing agenda. The outright technology sector in this ETF is 20.35%. If you add the same names back, you end up with 34.92%.

The “opposite reaction” is to under-own energy, particularly oil. As you can see from the chart above, the Russell 1000 Growth owns almost no energy by weight. The S&P 500 Index at year-end 2019 owned 4.35% in the energy sector. The Vanguard ESG US Stock ETF only owned 1.36%, but it’s more interesting to go beyond the sector to see what is owned in underlying stocks. Of the five largest energy stocks in the S&P 500 Index, the ESG ETF only owns one, Schlumberger. It owns no Exxon Mobil, Chevron, ConocoPhillips or EOG Resources. What does this ultimately say? If there is a better era ahead in the oil business, we believe investors seeking out this agenda will skip any benefits.

Why do we believe this is madness?

It’s not about the agenda. It’s about the economics. This is classic Wall Street. Find an era where a particular style has done well. Wall Street will then create another way to resell those same companies to a new group of people. ESG investors are buying re-branded growth portfolios that fill a non-economic agenda.

We say non-economic because investors don’t need ESG to be more growth-oriented, the Russell 1000 Growth can give you pure heroine on that, as we’ve shown. If the era ahead is not dominated by tech-oriented businesses and growth stocks, the warmth of the ESG agenda will provide no comfort. The S&P 500 Index currently owns the smallest amount of energy stocks in the last 40 years. The ESG options only compound this problem.

If the equal reaction (growth/tech stocks) do poorly and the opposite reaction (value/oil stocks) do well at the same time, we could witness value and growth reaching equilibrium. The physics of this would be shocking, or to put it as Sir Isaac Newton did long ago, “I can calculate the motion of heavenly bodies, but not the madness of people.”

Warm regards,

Cole Smead, CFA

The information contained in this missive represents Smead Capital Management's opinions, and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Cole Smead, CFA, President and Portfolio Manager, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

© 2020 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com

Follow us on Twitter @SmeadCap