Are value stocks poised for a comeback?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

For the past decade, the competition between growth and value stocks has been decidedly short on suspense — growth has consistently come out on top. But value stocks recently disrupted this storyline with a rousing rally. Was this simply a blip? Or was it a preview of a lasting rotation?

Below, Brian Levitt, Invesco’s Global Market Strategist for North America, and Talley Léger, an Invesco Investment Strategist who specializes in the equity markets, discuss whether the conditions are right for a longer-term shift to value.

Brian: The last time we wrote a blog together, I asked you if the inverted yield curve was keeping you up at night. That was back in September, and neither of us seemed to be losing sleep. We reasoned that the inverted yield curve was reflective of multiple policy mistakes — the 2018 Federal Reserve (Fed) rate hikes and the ongoing uncertainty of the trade war — and that the curve would steepen modestly amid a better policy mix. Fast forward to today: The Fed has been easing policy and there are hints of incremental progress on trade. The yield curve is no longer inverted, and US stocks have been hitting all-time highs.1

A funny thing happened on the way to those all-time highs. The markets, which had been led by growth stocks for the past decade, were briefly led by value stocks.2 Was that just a short-lived rally or a hint of a longer-term shift to come?

Talley: In my view, there are a few signposts that can help us determine whether we’re on a new road toward value outperformance — or if we simply took a short detour. You mentioned two: Fed interest rate cuts and a steepening yield curve. I believe a durable value regime depends on the outlook for both.

The yield curve (or difference between short- and long-term interest rates) is a transmission mechanism for monetary policy. The Fed manipulates the slope of the curve by either raising short-term rates to flatten the curve (2018) or lowering them to steepen it (2019). True, Fed Chair Jerome Powell has signaled no more cuts this year. However, the Fed’s own Underlying Inflation Gauge suggests core consumer price inflation should cool in 2020, giving Powell scope to reduce rates further next year.

Why is this important to your question? In a nutshell, the yield curve provides signals from the bond market on whether the economic outlook is getting better or worse. As such, it’s no coincidence that the curve is positively correlated to the performance of value stocks relative to growth stocks.

Another signpost I’m watching for is a shift in sector leadership to financials (the value heavyweight) from technology (the growth heavyweight), but that ratio hasn’t turned convincingly yet.

To answer your question, I think it’s possible that 2020 could be the year of a temporary or “mini” rotation to value. But I’m unsure it’ll last.

Brian: I’ve always been taught that value-oriented assets require a catalyst to sustain outperformance, namely a new higher level of growth in the economy. Is that possible? It seems as if we are at or near full employment, and it’s unlikely to me that a surge in productivity gains is coming our way.

You mention the Fed interest rate cuts and the steepening yield curve. Wasn’t the Fed simply unwinding the policy mistakes of 2018 — or at least what the bond market viewed to be policy mistakes? The yield curve had inverted in August, financial conditions were tight, and inflation expectations were falling. They had to respond. The Fed succeeded in normalizing the yield curve, although truth be told the spread between long rates and short rates has remained very tight and has narrowed in recent weeks.

Nonetheless, long rates (as defined by the 10-year US Treasury rate) have climbed from a very depressed and overbought condition (1.45% on Labor Day) towards 2.00% (1.95% on Nov. 8), a level that is more reflective of trend real gross domestic product.3 It’s no surprise then that value stocks would have led the market as the economy recovered and rates backed up towards 2.00%. But is that all there is to this story? Sure, the Fed could lower rates again. We could get a US-China trade deal. A better policy mix could further steepen the yield curve and support value in the near term. But aren’t we ultimately destined to return to a slow growth world with the Fed not doing much of anything for the foreseeable future?

It seems as if that is what the financials/technology ratio is telling you. So, is the idea to own value-oriented cyclicals now and then transition to growth-oriented cyclicals? Or do we continue to favor the true growth assets in what continues to be a slow-growth world?

Talley: Given population growth of less than 1% and productivity growth of less than 2%,4 I think it’s unlikely the US economy can sustain a faster pace of activity. In other words, the structural growth outlook remains modest and hasn’t changed, in my view.

That said, I’m simply talking about the cyclical growth outlook, which has received a near-term boost from easing monetary, financial and credit conditions, as well as curve steepening, diminishing recession risk, trade progress, a softer US dollar and improving global growth.

In terms of sector strategy, it’s possible that cyclical leadership could ebb and flow between growth cyclicals such as technology and consumer discretionary, and value cyclicals such as financials, energy, real estate and materials. Industrials could be seen as a “core” cyclical sector, balanced between growth and value.

However, the flow back to growth cyclicals may await a higher federal funds rate, flattening yield curve, and tighter monetary policy.

How could that sequence of events unfold? If the growth outlook has indeed improved as described above, would that eventually bring the Fed back into the game? If so, would we return to the higher funds rate/flatter curve/tighter policy regime of 2018? Such sequencing would take time, perhaps beyond our 2020 forecast horizon.

I don’t mean to over-finesse the nuances. The bottom line is I think we could be facing a value rally of playable magnitude, but ultimately insufficient duration.

Brian: “A value rally of playable magnitude, but ultimately insufficient duration.” I like that. You are a wordsmith.

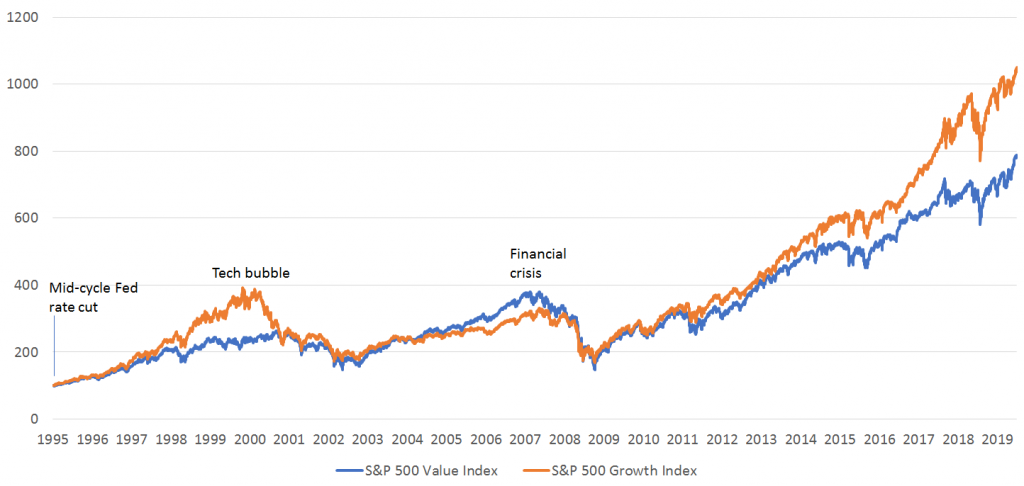

I’d like to dig more into the playable magnitude concept, particularly given how focused we are on Fed policy and the shape of the yield curve. Since the Fed lowered rates on July 31, 2019, large-cap value stocks have outperformed large-cap growth stocks (as shown in Figure 1) by 2.6% on a price-return basis (as of Nov. 26, 2019). However, consider the Alan Greenspan mid-cycle rate cut in the mid-1990s. Value stocks and growth stocks were essentially neck-and-neck for most of the next three years, only for growth stocks to outperform value stocks massively over the final 18 months of the bull market.

What’s the lesson? Scenario A: Continue to favor growth because it may keep up with value during a Fed easing cycle and outperform in the later stages of the cycle? Or Scenario B: Start building value into your portfolio because the late 1990s ended badly for growth stocks?

S&P 500 Value Index and S&P 500 Growth Index: Growth of $100 (1995-2019)

Personally, I’m in camp A for two primary reasons: 1) As the saying goes, we make hay when the sun shines, and the valuations of US-growth-oriented equities do not currently appear to be anywhere near as excessive as they were in the late 1990s, and 2) I believe that the markets will continue to favor growth in what will continue to be a slow-growth world, as they have since the global financial crisis.

Talley: In my opinion, the more cyclical Scenario A runs the risk of missing a potential, albeit tactical, value rotation. Meanwhile, the more secular Scenario B could require much patience on the part of value investors. Alternatively, there’s another option worth considering — Scenario C: Embrace an agnostic approach to style investing for the remainder of the cycle or until the cross-currents buffeting value and growth stocks sort themselves out.

In the June 2019 update of my Equity Strategy Playbook, I curbed my enthusiasm for growth and technology stocks — which served me well for the better part of three years — by adopting a blend of growth and value. At that time, valuations were one of my key reasons for downgrading growth. Specifically, the price-to-book ratio of large-cap growth relative to value had eclipsed the peak that it set in the heady days of the technology growth stock bubble of 2000.

We could debate our choice of valuation metrics, but suffice it to say your performance calculations and style benchmarks seem to support my recent change of view, at least for now. Stay tuned.

1 As of Nov. 13, the S&P 500 has hit 20 record closing highs during 2019. Source: The Financial Times, “S&P 500’s latest record high takes it past 2018’s tally,” Nov. 13, 2019

2 As measured by the S&P 500 Value Index and the S&P 500 Growth Index.

3 Source: Bloomberg, L.P.

4 Source: US Bureau of Labor Statistics

Important information

Blog header image: photo-nic.co.uk / Unsplash

The price-to-book (P/B) ratiois calculated by dividing the market price of a stock by the book value per share.

The S&P 500® Growth Index consists of stocks in the S&P 500® Index that exhibit strong growth characteristics based on three growth and four value factors.

The S&P 500® Value Index consists of stocks in the S&P 500® Index that exhibit strong value characteristics based on three measures: book value-to-price, earnings-to-price and sales-to-price.

The S&P 500® Index is an unmanaged index considered representative of the US stock market.

The opinions referenced above are those of the authors as of Dec. 11, 2019. These comments should not be construed as recommendations, but as an illustration of broader themes. Forward-looking statements are not guarantees of future results. They involve risks, uncertainties and assumptions; there can be no assurance that actual results will not differ materially from expectations.

Brian Levitt is the Global Market Strategist, North America, for Invesco. He is responsible for the development and communication of the firm’s investment outlooks and insights.

Mr. Levitt has two decades of investment experience in the asset management industry. In April 2000, he joined OppenheimerFunds, starting in fixed income product management and then transitioning into the macro and investment strategy group in 2005. Mr. Levitt co-hosted the OppenheimerFunds World Financial Podcast, which explored global long-term investing trends. He joined Invesco when the firm combined with Oppenheimer Funds in 2019.

Mr. Levitt earned a BA degree in economics from the University of Michigan and an MBA with honors in finance and international business from Fordham University. He is frequently quoted in the press, including Barron’s, Financial Times and The Wall Street Journal. He appears regularly on CNBC, Bloomberg and PBS’s Nightly Business Report.

Talley Léger is a Senior Investment Strategist for the Global Thought Leadership team. In this role, he is responsible for formulating and communicating macro and investment insights, with a focus on equities. Mr. Léger is involved with macro research, cross-market strategy, and equity strategy.

Mr. Léger joined Invesco when the firm combined with OppenheimerFunds in 2019. At OppenheimerFunds, he was an equity strategist. Prior to Oppenheimer Funds, he was the founder of Macro Vision Research and held strategist roles at Barclays Capital, ISI, Merrill Lynch, RBC Capital Markets, and Brown Brothers Harriman. Mr. Léger has been in the industry since 2001.

He is the co-author of the revised second edition of the book, From Bear to Bull with ETFs. Mr. Léger has been a guest columnist for The Big Picture and for “Data Watch” on Bloomberg Brief, as well as a contributing author on Seeking Alpha (seekingalpha.com). He has been quoted in The Associated Press, Barron’s, Bloomberg, Business Week, Dow Jones Newswires, The Financial Times, MarketWatch, Morningstar magazine, The New York Times, and The Wall Street Journal. Mr. Léger has appeared on Bloomberg TV, Canada’s BNN Bloomberg, CNBC, Reuters TV, The Street, and Yahoo! Finance, and has spoken on Bloomberg Radio.

Mr. Léger earned an MS degree in financial economics and a Bachelor of Music from Boston University. He is a member of the Global Interdependence Center (GIC) and holds the Series 7 registration.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits