The year 2019 has given us plenty of fodder for commentary. The Federal Reserve changed its outlook materially, recession worries rose, and the trade war carried on. All the while, the economy has continued to perform admirably, with steady growth, low unemployment and calm inflation. Thus far, fears of a downturn have been misplaced.

Trade uncertainty remains the greatest downside risk. Negotiations between the U.S. and China are progressing slowly, with both sides managing expectations about the timing and scope of a future trade deal. Businesses are hesitant to invest, and their reluctance is weighing on several economic indicators. But consumers remain employed and confident, and some aspects of global uncertainty like Brexit are running their course. On balance, we expect steady growth to continue through the year ahead.

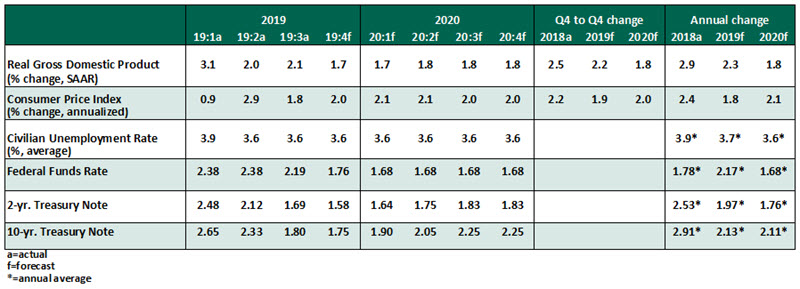

Key Economic Indicators

Influences on the Forecast

- The November employment report was remarkably favorable, with 266,000 jobs created last month. While November’s tally was boosted by the end of an automotive labor strike, upward revisions to prior months suggest the labor market is strong in all respects. Overall wages grew by 3.1% year-over-year; the inability of wages to grow more strongly suggests some slack remains in labor markets. Wage growth by production and nonsupervisory workers grew by 3.7%, a sign of the expansion benefitting all workers as it continues to run.

- At their meeting this week, Fed officials gave no reason to expect interest rate changes anytime soon. Any further cuts would be a result of economic underperformance, while hikes would first require a run of above-target inflation. Neither is our base case, and on balance, we expect a steady federal funds rate in the year ahead.

- Inflation remains benign. The deflator on personal consumption expenditures (PCE) grew by 1.3% year-over-year in October. On a core basis, excluding food and energy, it grew by 1.6%. The consumer price index (CPI) increased by 2.1% year-over-year in November, while the core CPI grew by 2.3%. All measures are pointing to an inflation environment with more structural factors holding inflation down than market pressures pushing up.

- Rumors are growing of the Fed revising its inflation targeting framework to take greater action to meet its 2% core PCE objective. While no concrete plan will be announced until next year, the persistent undershoot is meriting attention.

- In the second print of third-quarter gross domestic product, the U.S. economy grew at 2.1% at an annual rate. The trend continued from the second quarter of strong consumer spending offsetting a loss in business investment. Fixed investment has turned negative in the past without sparking a recession, and we expect this can be another such cycle as long as consumers remain buoyant.

- Manufacturing Purchasing Managers’ Index (PMI) survey readings gave a mixed picture. While the Institute for Supply Management showed a flat trend of contraction, the Markit estimate showed growth resuming. Rather than picking apart the technical differences of the two surveys, we instead take heart that even the more pessimistic reading shows a flattening trend, not a steepening decline. Non-manufacturing PMI readings fell slightly but remained expansionary.