We are drowning in information but starved for knowledge.

From megatrends to ‘fads’

From an investment point-of-view, what’s the difference between a trend and a fad? That is a very good question because, what to some people may just be a fad is to others a very investable trend.

Let me give you a simple example – cryptocurrencies. When Bitcoin was first rolled out, at least to me, it was a fad. That said, the more I have learned about the concept, the less I think it is. As traditional monetary policy tools (e.g. interest rates) become less and less effective, new policy tools shall be required, and digital currencies could come quite handy there. Only one problem: For any of the existing cryptocurrencies to work as a proper digital currency, policy makers must find a way to reduce the volatility.

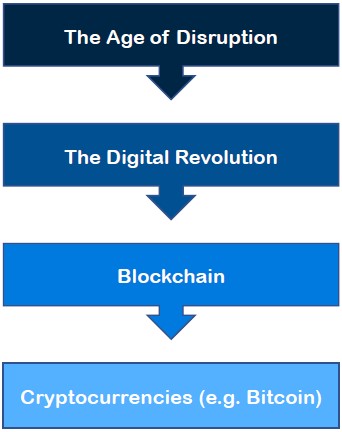

The Age of Disruption is one of the eight megatrends we have identified over the years and, ultimately, that megatrend has led us to Bitcoin. Bitcoin wouldn’t have happened without blockchain, though, and blockchain wouldn’t have happened without the digital revolution. In other words, it can be a long and winding road from megatrend to ‘fad’ (Exhibit 1).

Exhibit 1: From megatrend to ‘fad’ Source: Absolute Return Partners

Investing in megatrends

What exactly is a megatrend? A megatrend is a profound and longer-lasting change of status quo in society, be it driven by climate change, changing demographics, government policy, new technology or other fundamental socio-economic change.

Most investors, when constructing their portfolio, start by deciding how much to allocate to each asset class and then how much to allocate to each country or region. Megatrend investing is fundamentally different. If you believe, as I do, that we are in the very late stages of the current debt supercycle, but that the end could still be a few years away (debt supercycles last on average about 60 years, so this one is already long in the tooth), you will also agree that interest rates will stay low for longer than most investors believe.

Why? Because interest rates behave very similarly in all debt supercycles. In the latter stages, they are always low, and they remain low for years after the end of the cycle. In other words, adopting the debt supercycle megatrend in your portfolio construction approach implies that any investment opportunity that stands to benefit from a continuation of low interest rates should be considered, whatever the underlying asset class.

Prior beneficiaries of megatrends

As mentioned earlier, we have, over the years, identified no less than eight megatrends which will define the world in the years to come (you can read more about them here), and those megatrends define virtually everything we do at Absolute Return Partners. Having said that, the megatrend phenomenon is far from new.

The first megatrends – at least those that I am aware of – began to unfold as the industrial revolution made fundamental changes to how human beings could interact. Suddenly, steamboats allowed you to do things only the Vikings had mastered before (crossing the Atlantic), and railroads allowed you to cross entire continents in a fraction of the time it had taken on a horseback previously. It is no coincidence that the very first billionaires of this world – the Vanderbilts – made their money on transportation (Exhibit 2).

Exhibit 2: The world’s richest person in every decade Source: LoveMoney.com

The industrial revolution resulted in factories shooting up everywhere. To build those factories, and to construct all the wonderful things that would be assembled there, the world required plenty of energy (coal and oil) and ample iron and steel. Consequently, John D. Rockefeller and Andrew Carnegie shot to fame.

Seriously rich people don’t always make their money on megatrends, though. Sometimes a vanilla trend, maybe even a fad, is enough. The best example of that is the Japanese businessman, Yoshiaki Tsutsumi. Back in the 1980s, Japanese property markets reached ridiculous valuation levels which Tsutsumi took advantage of. As a result, he temporarily became the wealthiest person in the world before losing much of it again when the Japanese property market collapsed in the early 1990s. In hindsight, the Japanese property boom was clearly a fad.

Just like the early billionaires did, tech billionaires like Bill Gates and Jeff Bezos also benefitted from a very powerful trend – in this case the digital revolution. As that trend will run for many years to come (see more about that in the November Absolute Return Letter here), I think tech will hold on to its #1 spot on the rich list for years to come.

Which of ‘our’ megatrends tick the box?

There is a broader lesson to be learned here. Investing in megatrends is more likely to lead to long-term wealth than investing in the latest fad. Given the problematic outlook for the global economy (see later), I am convinced that investing in megatrends will lead to higher returns, as megatrends always survive difficult market conditions – something fads never do.

Earlier this year, BlackRock produced a white paper called Active Equity Thematic Investing and found that even a modest allocation to an array of megatrends should add meaningfully to annual returns. The obvious next question is which megatrends to pursue. In the above-mentioned paper, BlackRock lists three key criteria, two of which we would wholeheartedly agree with:

The trend in question must be enduring rather than faddish.

It must be a global theme rather than have a specific regional focus.

The third criterium that BlackRock subscribes to says that investors should be able to invest in the trend through equities. That criterium is very much dictated by their equity-focussed business model, though. We look for the best opportunities across all asset classes.

Allow me to reiterate all the megatrends that we have identified:

The End of the Debt Supercycle

Retirement of the Baby Boomers

Declining Spending Powers of the Middle Classes

Rise of the East

The Age of Disruption

Running Out of Freshwater

Electrification of Everything

Mean Reversion of Wealth-to-GDP

… with #8 effectively being the aggregate result of the other seven megatrends. Of those, five stand out as they offer a particularly good investment opportunity at present.

The End of the Debt Supercycle (which subscribers to ARP+ can read more about here) has led to a wave of downsizing of loan books amongst commercial banks all over the world. More and more corporate lending takes place away from banks these days and, going forward, bank finance will be mostly for tier one corporates. SMEs will have to look elsewhere to finance their growth. This is a trend that is highly unlikely to reverse any time soon as regulators continue to tighten demands on capital ratios in an attempt to avoid a repeat of the 2008 meltdown.

Retirement of the Baby Boomers is the megatrend that attracts the most public attention but, at the same time, it is probably one of the least well-represented megatrends in many portfolios, and the reason is obvious. This megatrend is playing out over several decades, i.e. spotting anything that is different from one day to the next is virtually impossible. That said, older people spend less money, and they spend it differently, compared to their younger peers, and therein lies the opportunity.

Rise of the East is a megatrend with major and long-lasting implications. In the short term, those implications are mostly negative as the US desperately seeks to maintain its position as the ultimate superpower of the world – both economically, politically and militarily. The ongoing trade war between China and the US is very much part of that power tussle but, longer term, it is a losing strategy for Washington not to open up to Beijing. The focus should instead be on the positive implications – rising living standards throughout Asia and how one can benefit from that.

The Age of Disruption is very much about the digital revolution. The reason why Bill Gates and Jeff Bezos have both topped the rich list more recently is quite simple – there is an awful lot of money to be made from digitisation. Even better, as AI, IoT, driverless cars, blockchain and other disruptive technologies are rolled out, even more money will be made. I am going to stick my neck out now and suggest that this is probably the megatrend that can make you the highest returns over the next ten years. Having said that, this megatrend is not only about the digital revolution. The death of fossil fuels, urbanisation and globalisation are all trends driven by the disruption megatrend, so diversifying away from technology (should you want to do that) is relatively easy.

Electrification of Everything is the final megatrend I will mention today. It is closely linked to a theme that gets plenty of media attention every day – climate change. And to all those of you who think climate change is a storm in a teacup, I suggest you take a long look at exhibit 3 below. I will say no more!

Exhibit 3: CO2 level during the last 3 glacial cycles(reconstructed from ice cores) Source: BlackRock

As governments all over the world seek to reduce the amount of greenhouse gasses, there is a drive towards electrification of all heating and transportation. In the short-term, for as long as much of that electricity is produced by coal-fired power plants, electrification will make little difference, though. In that context, it is rather disturbing how much coal still accounts for in the global fuel mix when generating electricity (Exhibit 4).

A drive towards electrifying all heating and transportation must therefore be combined with a drive away from fossil fuels, but that is already underway as renewable energy forms account for more and more in the fuel mix. In the early years of renewables, the transition was a little slow, but that was because electricity generation based on renewables did not make any economic sense and was only possible because of subsidies. That line has been crossed now, though, with more and more renewable energy projects being able to stand on their own legs.

The case for low returns

Long-term readers of the Absolute Return Letter will be aware that I have argued for a long time that returns will be disappointingly low in the years to come. There is more than one reason why that is, but nothing is more important to long-term equity returns than current valuations. The lower equities are valued today, the higher long-term returns are and vice versa.

Recent work conducted by BofA Merrill Lynch very much supports this thesis. They found that, at least in the US, the current valuation is almost all that matters as far as long-term equity returns are concerned. If you look 10 years out, the predictive power is very high. As you can see below, the R2 is 0.79%, i.e. almost 80% of 10-year equity returns in the US can be explained by normalised P/E values at the starting point (Exhibit 5).

BofA Merrill Lynch’s work is supported by work conducted by Jill Mislinski of Advisor Perspectives. Jill has found that, over the past 120 years, US equities have moved in a very well-defined channel, and that we are currently bumping against the ceiling of that channel (Exhibit 6). As you can see, we were, as of the end of November, no less than 116% above the long-term trend line.

Furthermore, Jill has found that, since 1877, we have enjoyed five secular bull markets and five secular bear markets. We are now in secular bull market no. six which is 10 ½ years old and dates back to the spring of 2009 when the recovery from the Global Financial Crisis began in earnest. A secular bull (bear) market distinguishes itself from a normal bull (bear) market in two ways. Firstly, it usually lasts for much longer and, secondly, it is characterised by rising (falling) P/E values rather than rising (falling) stock prices. You can follow Jill’s work here.

Exhibit 5: Normalised P/Es vs. 10-year returns on the S&P 500 (annualised) Source: BofA Merrill Lynch

The research done by BofA Merrill Lynch suggests that, over the next ten years, inflation-adjusted (real) equity returns will most likely be around 5% per annum - less than half the returns investors have earned in the great bull market of the last 35-40 years. Adding to that, the work conducted by Advisor Perspectives suggests that we may even be facing a new secular bear market, suggesting average returns could end up lower than the 5% suggested by BofA Merrill Lynch. Despite those indications, current equity market sentiment in the US is exceedingly upbeat.

Exhibit 6: Real returns on US equities since 1871 Source: Advisor Perspectives. Data as of 31 October 2019.

On that subject, I should point out that CNN runs the so-called Fear & Greed Index which is based on seven different momentum, strength, breadth and volatility indicators, and the current level of this index is a rather uncomfortable 75 which suggests an extreme level of greed amongst US equity investors at the moment (Exhibit 7).

All of this has led me to a simple conclusion - it is time to invest differently! If (US) equities are likely to deliver no more than 5% real returns annually and potentially worse, should we enter a new secular bear market, the portfolio construction approach that has worked so well over the last 35-40 years is very unlikely to pay off over the next ten years and maybe even longer. Obviously, this doesn’t imply that we cannot enjoy the occasional spell of rising equity prices. We certainly can, but average returns over the longer term will be disappointingly low – potentially even negative.

Exhibit 7: Fear & Greed Index Source: CNN. Data as of 2 December 2019.

What’s next?

We have been thinking along these lines for some years now and, although the relentless bull market in US equities has forced us to challenge the logic behind our thinking more than once, we arrive at the same conclusion every time. Away from the US, equities are already performing rather indifferently and, even in the US, away from various disruptive technology stocks, performance isn’t that great either. In other words, one could argue that it is not the US market per se that is doing so well. It is the disruption megatrend that is main driving force behind the extraordinary bull market.

As powerful as megatrends are, as slow they often are to unfold. I wouldn’t be at all surprised if new technologies driven by the ongoing wave of digitisation will continue to disrupt incumbents for decades to come. Moreover, some of the early disrupters could very well be disrupted themselves.

As a result, there is quite a unique investment opportunity unfolding in front of us. Even better, disruption is far from the only opportunity to be explored, and that is why we have decided to launch a family of megatrend funds over the next few years. The first one, focussing on thematic credit opportunities and linked to The End of the Debt Supercycle megatrend, should be launched early next year with a thematic equity fund (which will focus on The Age of Disruption megatrend) to be launched soon thereafter and a further two in 2021. All that is subject to regulatory approval and may change, but that is our game plan as it stands.

In a public letter like the Absolute Return Letter, I cannot be more specific than that (the lawyers won’t allow me), but drop us a note on [email protected], should you want to learn more.