summary

-

The Negativity Surrounding Interest Rates

-

Keeping Pace With Payments

-

Protests Flare up Around the Globe

Multiple medical studies have shown the power of positive thinking: People with more optimistic outlooks experience longer lifespans, lower rates of depression and stronger immune systems; those with negative perspectives can face more frequent illnesses and a lower capacity to handle stress. We fear fixed income markets may be similarly impaired, as negative yields are here to stay in a number of countries.

Negative bond yields were long thought to be possible only in theory. Conventional wisdom held that, in a market of rational actors, no buyers would exist for an investment that promises to lose money. Recent experience calls for a revision to the textbook.

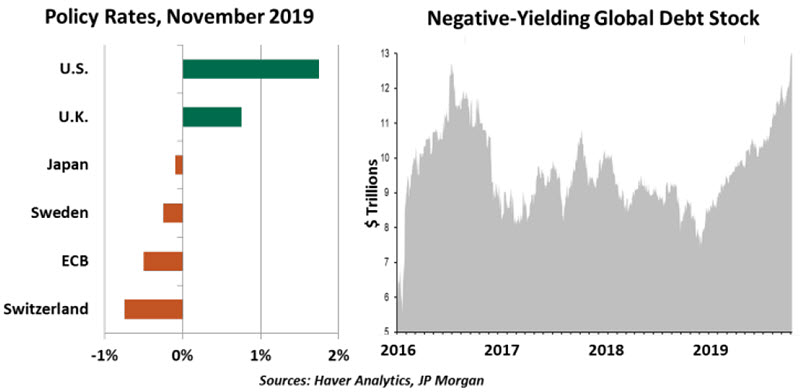

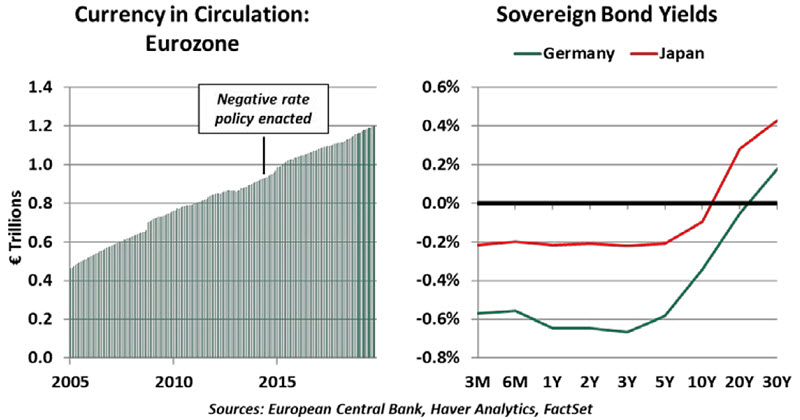

The movement toward negative yields started with short-term rates in Europe. Sweden’s Riksbank set a deposit rate of -0.25% as early as 2009 but was able to lift rates the next year. Then, as Europe struggled to recover from its double-dip recession, the European Central Bank (ECB) lowered its deposit rate to -0.10% in June 2014. The decision was criticized at the time for being an “expropriation of savers.” Former ECB President Mario Draghi defended the rate as a way to restore growth and allow interest rates to return to a higher level. More than five years later, the eurozone has avoided another recession, but the deposit rate has drifted further into negative territory.

Central banks justify negative deposit rates as a mechanism to encourage investment. With an effective tax on their accounts, depositors have a disincentive to save, and investments appear more attractive in comparison. However, commercial banks bear the burden; they are stuck losing money on their reserves but are hesitant pass the loss on to their depositors. Lower earnings may impair the ability of banks in some countries to extend credit.

At the other end of the yield curve, market dynamics are pushing longer debt yields into negative territory. Most government securities are issued with a positive yield and a fixed coupon payment. During risk-off intervals, investors seek the safety of bonds, bidding their prices up in the secondary market. As prices rise, the yield to maturity of the bond falls. Though the bond still pays its promised coupon, the buyer has paid a premium that exceeds the bond’s coupon payments, pushing the effective yield negative.

“The move toward low and negative yields continues, despite a good economy.”

When investors buy bonds that pay negative yields, they are trading yield for safety. Some of this irrationality is by policy: Many institutions and bond funds are chartered to hold a share of their assets in risk-free instruments, regardless of yield. As rates fall, governments are starting to issue short-duration securities with a zero or negative notional yield. Even Greece, a country that struggled to find bond buyers at any price just five years ago, recently auctioned €487.5 million in three-month bills that paid a negative rate.

These trends make borrowers happy, but squeeze savers and investors. Long term, investors need to reconsider their expected returns. Not long ago, all categories of savers could expect to earn a 7% return on their investments with balanced risk. This rate of return is a conventional calculation for retirement savings, but is starting to look too optimistic. As yields fall across the spectrum, only the riskiest bonds are paying such returns. This places further pressure on pension systems, many of which were struggling even before rates fell below zero.

Central banks in economies that currently hold positive yields may see a cautionary tale: Once rates fall, they do not get back up. During the last three U.S. recessions, the Federal Reserve has lowered the federal funds rate by a total of about five percentage points. With today’s rate holding near 1.55%, a reduction of similar magnitude would cause the Fed to break into deeply negative rates. In the minutes of its October meeting, the Fed made clear its reluctance to do so: “All participants judged that negative interest rates currently did not appear to be an attractive monetary policy tool in the United States.”

The Centre for Economic Policy Research found negative rates in Europe to be somewhat effective at transmitting monetary policy: When faced with negative interest rates, companies do not withdraw cash the way households might, and are somewhat encouraged to invest.

Negative-yielding bonds have natural competition from cash. While cash pays no interest, receiving nothing is still better than taking a loss. But cash has its own risks (theft, loss) and costs (transportation, storage, physical exchange), making it an impractical investment. The amount of currency in circulation did not noticeably increase even as economies entered a phase of negative rates; research suggests rates as low as -2% are possible before cash hoarding would take root.

“Hoarding cash to avoid negative interest rates is a difficult thing to do.”

And a decreasing share of the world’s money is physical. As we discuss in the next article, electronic transactions are convenient, and governments are reducing the availability of high-denomination banknotes. Most money exists electronically on reserve bank ledgers. Commercial banks can freely exchange their reserve deposits for paper currency. As outlined in an International Monetary Fund working paper, reserve banks could align cash to a negative rate by charging a rental fee or an uneven exchange rate for paper currency. The very existence of that paper is telling: Researchers are no longer exploring whether negative rates are viable, but how to enact them.

Worldwide, economies are growing and unemployment is falling, but it is not clear that negative rates were necessary to achieve this growth. Commercial lending has been steady, while governments have been slow to start debt-funded projects despite the low cost of borrowing. The burden borne by banks and savers appears to have been a net negative.

At present, over $11 trillion of bonds are trading with negative yields. This is no passing fad, and investors and central banks in some parts of the world can expect a prolonged struggle against negativity. For them, staying positive will be easier said than done.

Show Me the Money

Forty years ago, everyone was talking about money. Those conversations weren’t about personal finance or investing; the focus was on the amount of money in the economy. Inflation was raging out of control, and research blamed excessive growth in the M1 segment of the money supply (currency in circulation and checking accounts) for rapid increases in the price level. On this basis, the Federal Reserve set out to tame inflation by curbing growth in the money supply.

It took time, but the Fed was ultimately successful. Annual inflation in America is about one-tenth the peak seen in the early 1980s. Other central banks rushed to adopt strict monetary controls, with similar results. It appeared the secret to successful central banking had been found.

But the formula failed soon thereafter due to a number of external factors. The high-interest-rate environment of that era had spawned a whole new range of financial products, such as money market funds, that offered its holders access to liquidity. And credit cards, which were the province of a favored few in the 1970s, became more widespread.

This process, known as disintermediation, made it more difficult to define money and determine its effects on economic activity. It muddied the relationship between the money supply and inflation, forcing central banks to seek other paradigms for policy setting.

Central banks remain interested in the topic of money and payments, though. Efficient payment systems can foster growth and productivity, but are also vulnerable to attack. That is one reason why the Fed remains a key player in the American payment system, competing in that realm with private providers.

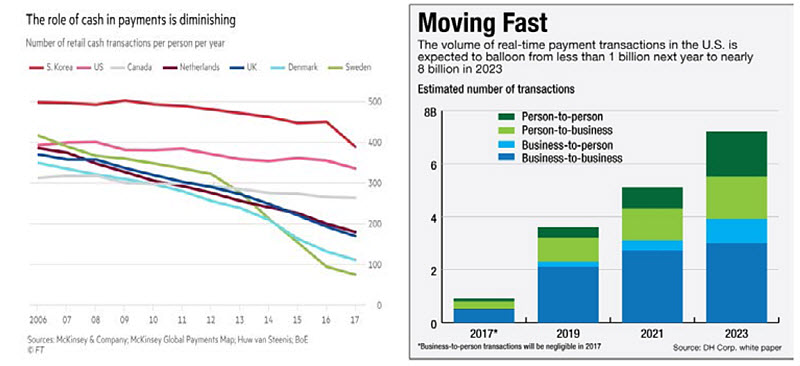

The payment system is on the cusp of massive change. As anyone who has visited a coffee shop recently knows, digital modes of payment are advancing rapidly; technology companies like Apple and Google have become important players in this area. Platforms like Venmo allow users to transfer funds to one another instantly, reducing delays and the need for paper media. To facilitate these new processes, digital currencies (which do not exist in physical form) have been proposed to reduce transactional costs.

Technology is also pressing into the realm of the financial markets. Digital ledgers like blockchain are gaining traction, reducing the time that separates trading and settling. (The Australian Stock Exchange has committed to replacing its existing clearing system with a blockchain structure over the next two years.) It used to take days for a security to change hands, but it will soon happen almost instantaneously.

The scale of change (or some would call it disruption) on the horizon is mind-boggling. But as it advances, it will create both benefits and risks. The benefits of speed, efficiency and cost are clear. The risks arise primarily from security; there are concerns the new platforms are more vulnerable to cybercrime, and require careful monitoring.

“When it comes to payment methods, cash is no longer king.”

To provide assurance and to keep their fingers on the pulse of payments, central banks have been forging ahead with their own digital transformations. The Fed recently announced plans for a real-time interbank payments service called FedNow, which it hopes to have available within the next five years. The Fed (along with other central banks) is considering creating its own digital currency, whose value it would guarantee. The public trust of monetary authorities may give central banks an advantage in these arenas.

The pace of commerce is increasing, and participants in the payment system are going to have to adapt quickly. The patrons at my coffee shop are getting tired of me paying with the spare change found between couch cushions.

Taking It to the Streets

Those trying to follow global developments closely are probably finding it hard to keep up. A series of uprisings around the world have complicated the outlook for many countries.

In recent months, a number of protests have broken out in different parts of the world, reminiscent of the protests of the late 1960s. Bolivia, Britain, Spain, Chile, France, Hong Kong and Lebanon have all seen mass demonstrations.

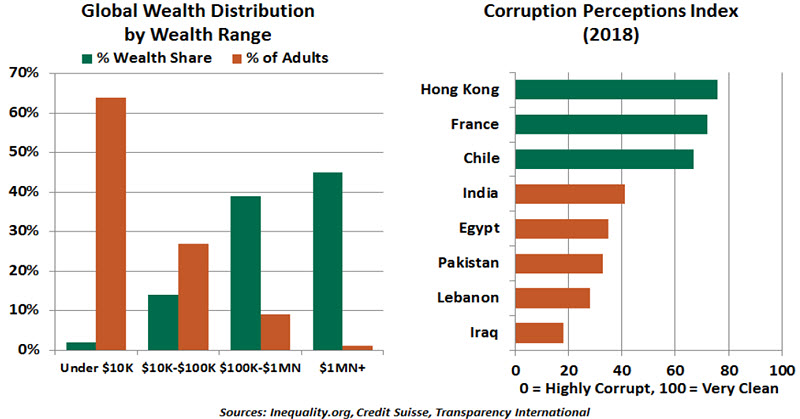

In Lebanon, a proposed tax on a popular messaging platform prompted people to take to the streets, while in Chile, it was a hike in subway fares. Concerns over fuel and onion prices contributed to the protests in France and India, respectively. Lebanon is not only among the world’s most unequal economies but also stands among the most indebted countries of the world. On the other hand, Chile, though relatively stable and wealthy for its region, has a high level of post-tax income inequality.

“Several protests around the globe bring back memories of protests of the late 1960s.”

While globalization and technological progress have been immensely beneficial to the global economy, popular sentiment is turning against the high income and wealth disparities that stem from economic shifts. Slowing economic growth, particularly in Latin America, and lower fiscal capacity have impaired governments’ ability to offer programs to support the disenfranchised. On the other hand, the high tax burden in many countries, notably in Europe, has fueled discontent. Governance issues, like corruption and poor services, are also at the heart some of the protests.

Poorer individual fortunes aren’t the only motivator; some objections are linked to the environment and climate concerns. Anger over new policies (such as in Hong Kong, Catalonia and Brexit) is also a factor. Greater awareness about issues and easier communication through social media have made it harder to placate dissenters and easier to organize rallies.

Social unrest is a growing economic worry because it undermines the delicate balance between ensuring macroeconomic stability and tackling growth challenges. It is a call for policymakers to act on reforms that not only improve growth but also benefit even the weakest sections of society.

© Northern Trust

www.northerntrust.com

© Northern Trust

More Fixed Income Topics >