Introduction

Index funds are increasingly embraced by investors seeking market-based returns at relatively lower costs than actively managed funds. As a means for everyday investors to access market returns while mitigating the risks of significant underperformance, index funds are a compelling investment option. Furthermore, for investors wanting to integrate their values into their investment portfolio, socially responsible investing (SRI) index funds provide a foundation on which to make a constructive difference in the world.

SRI index funds are created using several different approaches, but one type that provides the unique opportunity for investors to obtain the benefits of market index funds while making a positive impact, is called optimized index funds. Optimized index funds seek to track the returns of a public benchmark index within a narrow range, called tracking error, while not using all the constituents of the index. In the case of an SRI fund, this is typically done by applying a set of exclusionary screens. Some examples of exclusionary value screens include companies that are affiliated with gambling, tobacco, or weapons production and support. Fund managers may also exclude companies on the basis of environmental, social, and governance (ESG) factors.

Optimized index funds also offer a platform on which to advocate for better corporate behavior through engaging company management teams. Importantly, they seek to deliver the consistent performance relative to market indexes that allows investors and their financial advisors to focus on the decisions and behaviors that make a meaningful difference in whether investors meet their long-term goals.

No need to choose between impact and performance

Optimized index funds recognize that there are real people behind the shareholder accounts. Investors attracted to SRI funds tell us they want to invest in products that reflect their desire to avoid investments in certain companies and to make a positive impact on the world, but they also need these investment products to help them prepare for the future. Whether building a nest egg for retirement, saving for college tuition, or planning for unanticipated expenses, investors rely on sound financial plans and products that deliver results.

Investment products that seek to change the world, but fall short in delivering the financial results shareholders need, fail to deliver on their promise to investors.

Screened optimized index funds are a pragmatic response to a complex investment landscape where many investors want to invest with their values, but also want predictable performance relative to public benchmarks.

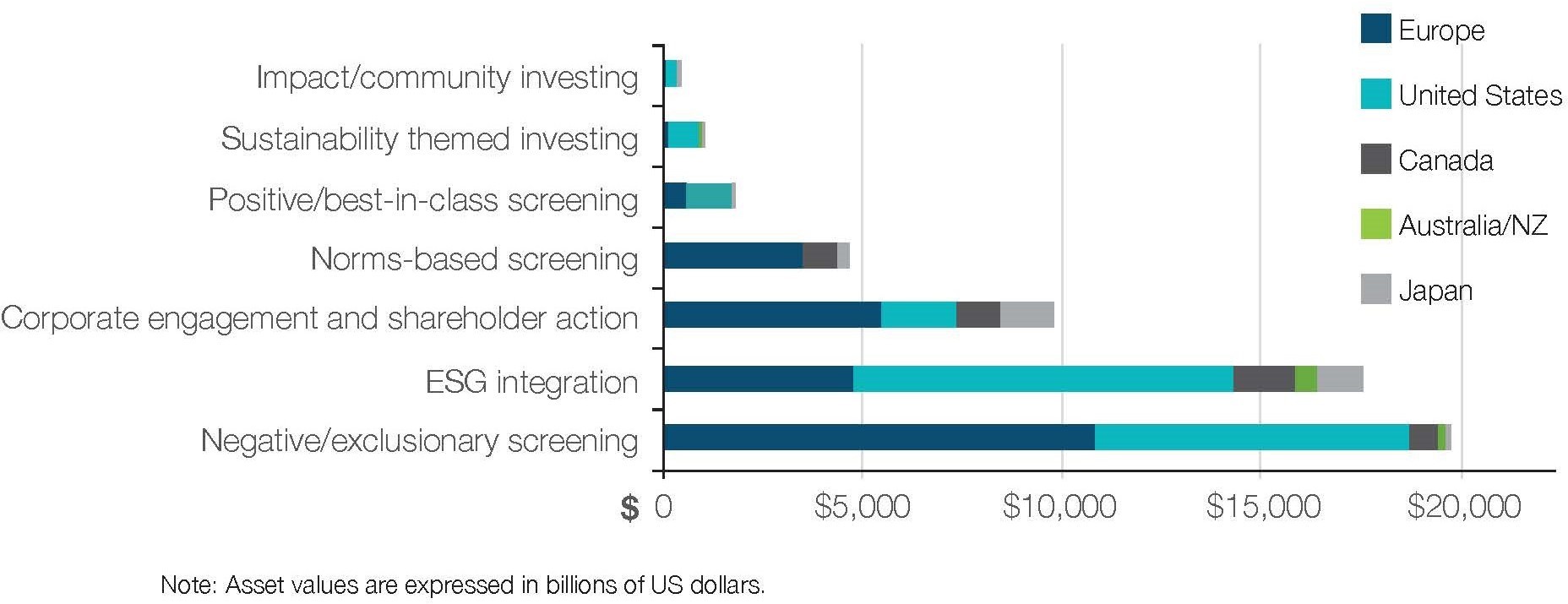

For SRI optimized index funds, stable ownership of a range of companies and industries provides a platform for helping investors integrate their values into their investment decisions. Exclusionary screening is the foundation for many SRI strategies, but the best funds also actively advocate for change in the companies in which they invest. (See Figure 1). Active proxy voting, investing to bolster underserved communities, and shareholder advocacy can all be accomplished in optimized index funds.

Shareholder advocacy done well often takes years to accomplish, beginning with research on a topic and the target company’s connection to it. Building rapport with company management teams also takes time. And sometimes shareholder advocates need the leverage of an annual shareholder meeting or two to move atopic forward with a corporate management team. While an active strategy may be a reasonable platform for advocating for change at a company, many active managers have very short holding periods not conducive to long- term discussions with corporate management teams. Optimized index strategies afford shareholder advocates with long, stable holding periods that allow for a measured, strategic approach to advocating for corporate change.

It is our view that this prophetic part of investing – encouraging corporate change – is enhanced through SRI optimized index strategies, especially for investors who are also hungry for consistent, potentially predictable performance.

Figure 1: Sustainable investing assets by strategy and region 2018

Performance

Evidence continues to mount that active investment strategies, particularly in U.S. equity markets, have failed to beat broad market indexes on average. This inconvenient fact is often ignored by investors, though many are getting the message as they move billions of assets to index strategies. It is also minimized by active managers who have an objective to beat their chosen benchmarks, but who on average often don’t.

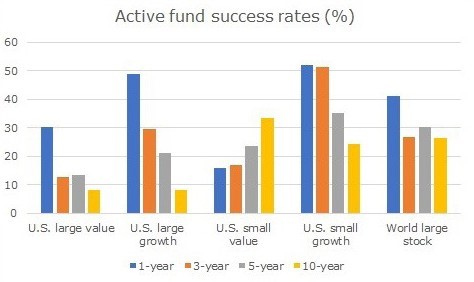

According to Morningstar analysis, just 24% of active funds have beaten their passive peers in the past 10 years. That may sound discouraging enough, but some subcategories are even worse.

Just over 8% of large cap value and large cap growth stock funds beat their average passive peer funds in the last 10 years ending in December 2018. (See Figure 2). The small growth category was slightly better with 24% of active funds outperforming their passive peers and small value was even better at 33% of funds outperforming over the past 10years. Regardless of the market cap size of the strategy, many active funds have under¬¬performed their passive peers over market cycles.

While some investors may actively choose to sacrifice potential return to express a moral view through their investments, many investors want to be productive and responsible with the impacts of their investments. And it’s not just that the evidence is overwhelming that the average active investment manager under- performs market indexes, it’s that variable performance often induces investors to make detrimental choices with respect to the timing of their investment decisions.

These decisions lead investors in funds with highly variable returns – far above and far below the public benchmarks they seek to exceed – to experience returns that are sometimes far below the performance of the fund itself.

Figure 2: Active fund success rates (%)

Investor behavior in the face of variable returns

Investors in active funds are tempted to chase performance, often experiencing performance that is lower than the funds in which they invest. This concept of “investor returns” captures the self-harming decisions that many investors are tempted to make. Most of us can empathize with this feeling. We are tempted to buy a fund or stock after we are convinced by recent past outperformance and we capitulate by selling only after our investment has failed. In effect, we “buy high” and “sell low”- exactly the opposite of the optimal investment strategy.

By their very design, optimized index strategies are expected to deliver performance that tracks markets within a forecasted range, which is almost always much narrower than the range delivered by actively managed strategies. Because of this, investors can buy into optimized index funds knowing that performance is unlikely to exceed or trail the benchmark returns by a wide margin, making them less prone to trade into and out of the fund. By contrast, investors in active funds are often tempted to trade more, exposing themselves to a greater number of detrimental decisions. Even if the active fund performs well versus its market benchmark over time, which we’ve shown is quite rare, a typical investor’s behavior results in trading into and out of the fund that results in lower realized returns.

Morningstar has attempted to quantify the investor gap between investor returns and fund returns in its “Mind the Gap” study, and the results are illuminating. Investors in active funds tend to experience larger shortfalls between the investor return they receive versus the returns of the funds in which they are investing. In contrast, investors in broad market index funds tend to have very low shortfalls between investor return and fund return.

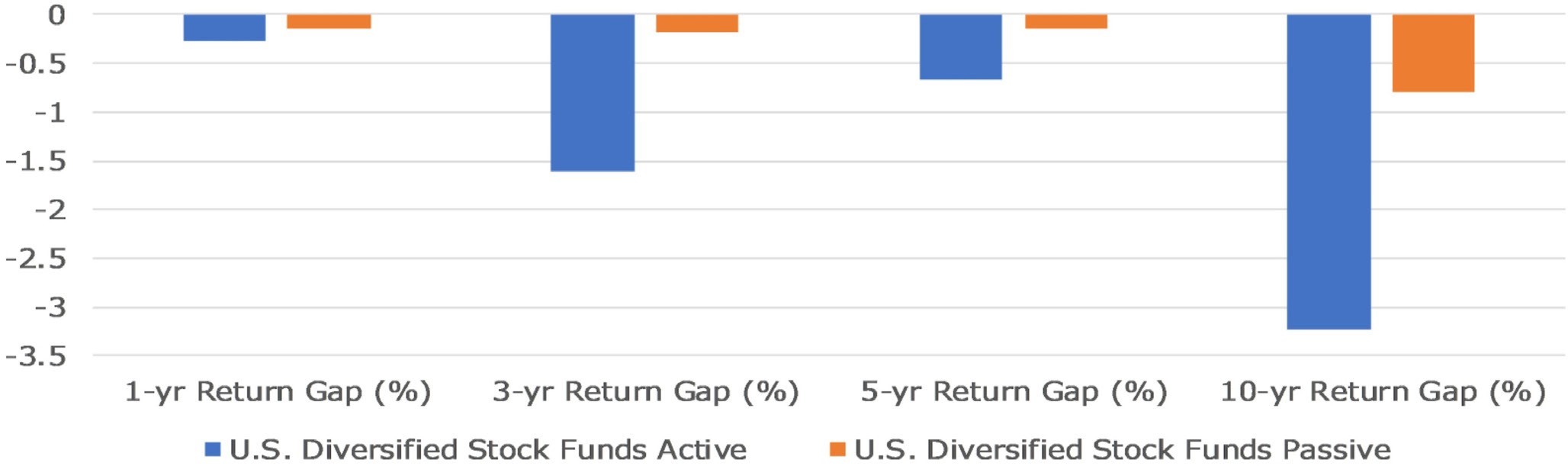

Figure 3: U.S. stock funds: Investor gap over time

Morningstar analyzed U.S. Diversified Stock Funds and compared active versus passive investor returns. Over the prior one year from March 31, 2018, passive funds had a -0.15% investor gap versus active funds with a -0.27%. (See Figure 3). Over three years, the gap widened as passive funds had a -0.18% investor gap while active funds had a -1.61% investor gap for a 1.43% difference in the shortfall suffered by investors in active funds versus passive funds. The difference fell to 0.52% investor gap positive difference between passive and active funds over five years and a 2.44% difference over 10 years. In all periods, there is a better investor return for passive fund investors versus active fund investors and it is very substantial in most periods.

Why is this? Probably because investors in index funds experience the return they expect, which is likely to be slightly below market benchmarks after taking fees into account. The data suggest that index investors are satisfied with the returns they experience and therefore don’t react as much as investors in active strategies do. Investors in active funds, on the other hand, are constantly faced with the decision to buy, hold, or sell based on their assessment of the skill of the active manager. They are faced with the daunting task of distinguishing between the skill and luck of the manager – a feat that is exceedingly difficult to do on a consistent basis.

Helping advisors help their clients

For financial advisors, the consistent performance delivered by optimized indexes provides a platform for stable assets under management and easier conversations with clients. Advisors can focus on helping clients act on the things they can control like their rate of savings, objectives, and their tolerance for risk, rather than defending the latest quarterly performance report from an underperforming manager.

And by using optimized SRI index funds, advisors help clients integrate their values into their investment portfolios while not compromising on expected performance.

At Praxis Mutual Funds, we incorporate both the pragmatic and the prophetic as we seek to deliver predictable performance through a series of optimized equity index funds. For additional resources on stewardship investing and more information, visit praxismutualfunds.com.

-------

A Fund’s stewardship investing strategy could cause the fund to sell or avoid securities that may subsequently perform well, and the application of social screens may cause the fund to lag the performance of its index.

Consider the fund’s investment objectives, risks, charges and expenses carefully before you invest. The fund’s prospectus and summary prospectus contain this and other information. Call 800-977-2947 or visit praxismutualfunds.com for a prospectus, which you should read carefully before you invest. Praxis Mutual Funds are advised by Everence Capital Management and distributed through Foreside Financial Services, LLC, member FINRA. Investment products offered are not FDIC insured, may lose value, and have no bank guarantee.

2191060

Read more commentaries by Praxis Mutual Funds