Tactical Asset Allocation Views – Q4 2019

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Macro outlook and tactical asset allocation

Global growth below trend and decelerating

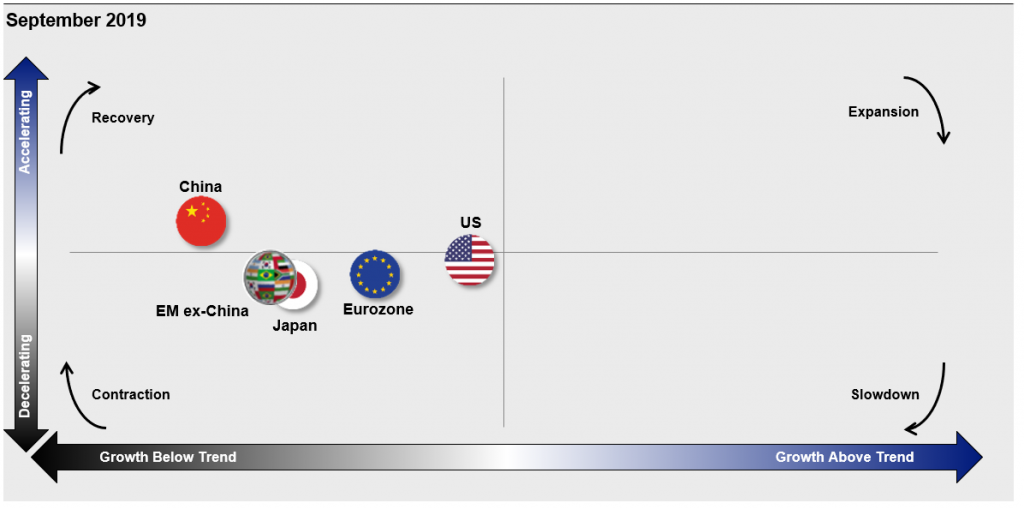

The global economy is rapidly decelerating, and we expect all major regions and countries around the world to grow below their trend rate of economic growth over the next few quarters, and at least through the first half of 2020. For the past six months, our macro regime framework, “Dynamic Asset Allocation through the Business Cycle”, as indicated that the global business cycle is entering a contraction, defined as growth below trend and decelerating. Our proprietary leading economic indicators (LEIs) have fallen sharply across most regions (Figure 1). This weakness has been most pronounced in the manufacturing sector, with global business surveys and industrial orders sharply deteriorating, because of tensions and uncertainty in global trade policy. In addition, business investments and capital expenditure (capex) have stalled, thereby curbing long-term growth expectations.

Figure 1: Identifying macro regimes across major regions and countries

The global economy is growing below trend as of September 2019 and still decelerating from Jan 2019 to Sept 2019

Source: Invesco Investment Solutions team proprietary research, September 2019.

Will we see a global recession in 2020? We think it’s unlikely, but we may experience a recession in some parts of the world. In our opinion, Europe exhibits the weakest cyclical dynamics, and currently runs the highest recession risks among major economies. Given its high exposures to global trade risks, the uncertainty over Brexit, and already negative interest rates, Europe has limited room to offset economic shocks. While we believe that a large and coordinated fiscal expansion would be an adequate response to private sector weakness, such a policy seems unlikely to occur before an actual recession. The recent tightening in lending standards fully justifies the renewed European Central Bank (ECB) asset purchase program, which may help avoid extreme negative downside risk. That said, we are skeptical about whether the asset purchase program can effectively boost the demand for credit in the private sector.

Across the pond, the US has been the most resilient major economy, but we are starting to see evidence that the global slowdown is affecting the world’s largest economy. The current circumstances are similar to what we experienced between 2015 and 2016, when the rest of the world led the slowdown, and the US followed. So far, the US slowdown is mostly concentrated in the industrial sector, while construction, housing activity, and consumer sentiment remained stable. Given the US economy’s relatively lower exposure to trade risk and higher exposure to domestic demand, we think the forecasts by some analysts of a recession in 2020 seem premature at this stage. However, the brief inversion of the yield curve is a headwind to future credit growth, and we believe lending standards are one of the key economic indicators to monitor going forward. Today, lending standards still seem to be very accommodating but are not yet responding to the prolonged flattening and instance of yield curve inversion (Figure 2).

Figure 2: Credit conditions respond to monetary policy with a lag

Lending standards tighten after prolonged periods of yield curve flattening and inversion

Sources: Federal Reserve, BEA, and Moody’s, from Jan 1989 to September 2019. Past performance does not guarantee future results.

As for emerging markets (EM), we are seeing tentative signs of stabilization in China after a steady deceleration over the past two years, led by improving orders in the industrial sectors. Clearly, the evolution of these cyclical indicators is strongly affected by ongoing trade policy developments, but Chinese policymakers have been successfully managing this economic transition, by and large. On the basis of our indicators, we believe it is too soon to tell whether we are at an inflection point, as the rest of the emerging markets ex-China are still decelerating across all EM regions — Asia, Latin America, and EMEA (Europe, the Middle East, and Africa).

Policy and global market sentiment

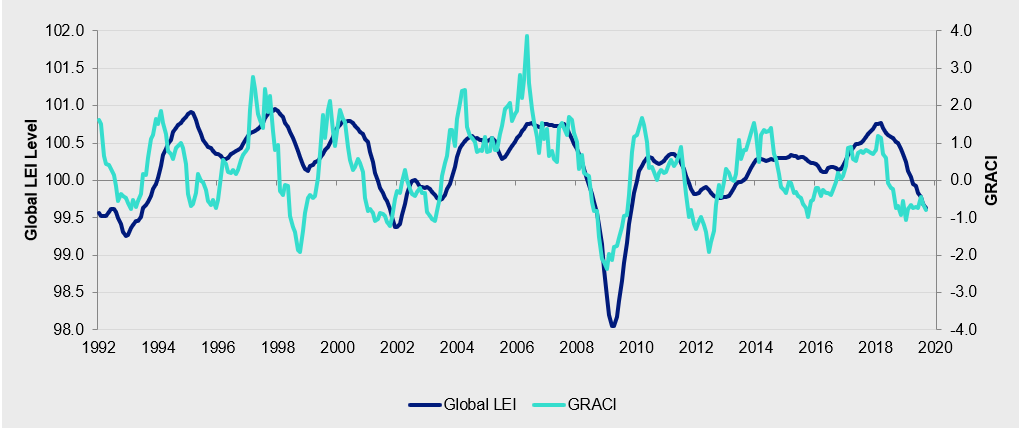

A distinguishing feature of this business cycle is the lack of inflationary pressures. This important development has allowed the US Federal Reserve (Fed) and the ECB to embark on proactive monetary policy easing in the face of slowing growth, with a combination of interest rate cuts and renewed asset purchases (effectively a Quantitative Easing program). The large decline in global bond yields has provided meaningful support to equity markets via lower discount rates and higher multiples, even while there has been a strong deceleration in earnings growth. Put another way, our analysis of market sentiment via global financial markets suggests that monetary policy has contributed to the stabilization in the global risk appetite after the steep decline in investors’ tolerance for risk that we experienced between April 2018 and June 2019 (Figure 3). As documented in our research, “Market Sentiment and the Business Cycle”, risk appetite tends to lead inflection points in the global business cycle by a few months. The stabilization of the risk appetite may, therefore, be providing an early sign that global growth may also stabilize over the next few quarters.

Figure 3: Risk appetite and the global business cycle

Sources: Bloomberg L.P., MSCI, Citi, Barclays, JPMorgan, Invesco research and calculations, from January 1992 to September 2019. The Global Leading Economic Indicator (LEI) is a proprietary, forward-looking measure of the macroeconomic trend level. The Global Risk Appetite Cycle Indicator (GRACI) is a proprietary measure of the markets’ risk sentiment.

Investment implications

Based on our research detailed in the aforementioned whitepapers, the current global macro environment we’re forecasting has historically offered limited compensation for taking additional risk in the Invesco Oppenheimer Global Allocation Fund, with riskier asset classes such as equities and credit historically matching or underperforming safe assets such as government bonds. Indeed, the past two years have aligned with this pattern, as global equities have roughly matched global government bonds while our global Leading Economic Indicators and risk appetite indicators have signaled a slowdown.1 As we enter Q4 2019, we believe a moderately defensive asset allocation is still warranted while we wait for a more significant improvement in global risk appetite and stabilization in leading economic indicators to justify increasing risk in the portfolio.

Compared with a global 60% equity / 40% bond portfolio, we remain underweight equities by about 10%, a position we have held through 2019, primarily expressed with an underweight in developed markets outside the US. We maintain a moderate overweight in US equities, with a factor tilt towards size and value, and an underweight exposure to momentum. We hold a moderate underweight in US equities, but with a pro-cyclical factor tilt towards size and value, and an underweight exposure to momentum. For the first time in 12 months, we have re-established a moderate overweight to emerging market equities, given improving risk sentiment and early signs of recovery in the Asian cycle. We remain overweight in alternative income assets, such as insurance-linked securities and event-linked bonds, which tend to offer higher long-term expected returns than core credit markets and favorable diversification properties in the late stages of the credit cycle. We continue to overweight duration in developed markets fixed income, a position we have held for the past 18 months, but we have moved from a flattening bias to a steepening bias in the US, where we expect additional rate cuts by the Fed should bring back some steepness in the yield curve. Our overall currency exposure is neutral to the benchmark, despite cheap valuations for major foreign currencies, and expensive valuations for the US dollar. We think a cyclical rebound in growth outside the US remains the primary missing catalyst for a sustained depreciation cycle for the greenback. Such a cycle would require a major reversal of private capital flows from the US to the rest of the world. Within our neutral exposure to the US dollar, we are overweight cheap and high-yielding emerging market currencies versus developed market currencies, a stance that has the potential to enable us to harvest carry and valuation premia.

Figure 4: Global allocation portfolio positioning as of October 16, 2019

Source: Invesco Ltd., 10/16/19. Portfolio allocations are displayed in terms of notional value and may exceed 100% as a result of exposure to derivatives. Notional Allocation refers to exposure gained through the use of derivative instruments when there is not an offsetting cash position. Holdings are subject to change.

Footnotes

1. For the trailing 2-year period ending September 30, 2019, the MSCI ACWI (net) returned 5.49% while the Bloomberg Barclays Global Aggregate Bond Index (USD Hedged) returned 5.62%. Past performance is not a guarantee of future results. An investment cannot be made directly in an index.

2. 60% MSCI ACWI & 40% The Bloomberg Barclays Global Aggregate Bond Index (USD Hedged)

Important Information

Blog Header Image: Denys Nevozhai / UnSplash

Duration measures interest rate sensitivity. The longer the duration, the greater the expected volatility as rates change.

The MSCI ACWI Index is an unmanaged index considered representative of large- and mid-cap stocks across developed and emerging markets. The index is computed using the net return, which withholds applicable taxes for non-resident investors.

The Bloomberg Barclays Global Aggregate Bond Index is an unmanaged index considered representative of global investment-grade, fixed-income markets.

The opinions expressed are those of Alessio de Longis as of October 21, 2019, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

Diversification does not guarantee a profit or eliminate the risk of loss.

MSCI Inc. Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent.

In general, stock values fluctuate, sometimes widely, in response to activities specific to the company as well as general market, economic and political conditions.

The risks of investing in securities of foreign issuers, including emerging market issuers, can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

Derivatives may be more volatile and less liquid than traditional investments and are subject to market, interest rate, credit, leverage, counterparty and management risks. An investment in a derivative could lose more than the cash amount invested.

Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa.

An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

Junk bonds involve a greater risk of default or price changes due to changes in the issuer’s credit quality. The values of junk bonds fluctuate more than those of high-quality bonds and can decline significantly over short time periods.

Because the Subsidiary is not registered under the Investment Company Act of 1940, as amended (1940 Act), the Fund, as the sole investor in the Subsidiary, will not have the protections offered to investors in U.S. registered investment companies.

The performance of an investment concentrated in issuers of a certain region or country is expected to be closely tied to conditions within that region and to be more volatile than more geographically diversified investments.

The Fund is subject to certain other risks. Please see the current prospectus for more information regarding the risks associated with an investment in the Fund.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds, and is an indirect, wholly owned subsidiary of Invesco Ltd.

Alessio de Longis is a Senior Portfolio Manager for the Invesco Investment Solutions team at Invesco. In this role, he leads the group’s global tactical asset allocation effort, focusing on the development, implementation and management of macro regime-based investment strategies across asset classes, risk premia and factors. Additionally, he develops and manages active currency overlay strategies and solutions for multi-asset portfolios.

Mr. de Longis joined Invesco in 2019 when the firm combined with OppenheimerFunds, where he was team leader and senior portfolio manager of the Global Multi-Asset team. Prior to joining the Multi-Asset team, he was member of the Global Debt team from 2004 to 2013, serving as currency portfolio manager and global macro strategist. He is a published author in the field of systematic currency investing using macro-based strategies, and he is regularly featured across financial media outlets.

Mr. de Longis earned an MSc in financial economics and econometrics from University of Essex, as well as MA and BA degrees in economics from the University of Rome Tor Vergata. He is a Chartered Financial Analyst® (CFA) charterholder.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits