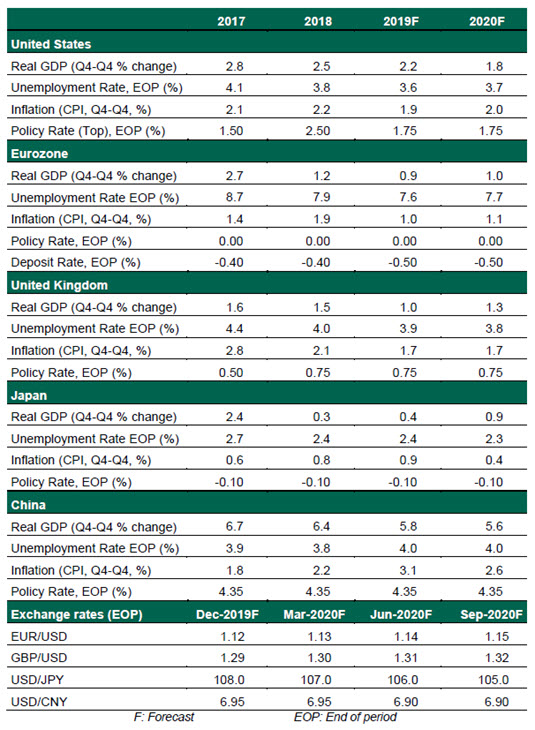

November Global Economic Outlook

SUMMARY

- Better Visibility, But No Sunshine Yet

After several quarters of gridlock, it would appear progress is finally being made on key issues clouding the global economic outlook. The U.S. and China are inching closer to signing “phase one” of a trade deal by not only pausing tariff escalation but also potentially rolling back some of the recently applied tariffs. Brexit is now a step closer to resolution, subject to the outcome of the December 12 elections. In the eurozone, there are tentative signs that the industrial sector is bottoming out.

That said, the forecast is still cloudy. U.S./China trade negotiations are far from complete, and there are a range of possible outcomes for the elections in the U.K. In our base case, economic activity will remain subdued but sustained in major economies as tariffs and trade tensions continue to sully the environment. Central banks in advanced economies are expected to be on hold for the foreseeable future.

Here are our views on the world’s major economic blocks.

United States

- At its October meeting, the Federal Open Market Committee (FOMC) lowered the federal funds target rate by 0.25%, the third reduction since the summer. In comments after the meeting, Fed Chair Jerome Powell said rates are now “in a good place,” a clear signal that more cuts are not anticipated. Further reductions would require broad economic underperformance, while a return to hikes would require sustained, above-target inflation. Our base case is a prolonged holding pattern.

- U.S. economic news has taken a generally favorable turn. Gross domestic product (GDP) grew by an annualized 1.9% in the third quarter, an outperformance driven by consumer spending. Unemployment is holding low at 3.6%, with persistent job creation and rising labor force participation. But trade tensions continue to weigh on business sentiment, as reflected in two quarters of negative fixed investment and three months of the manufacturing purchasing managers’ index showing contraction.

Eurozone

- The eurozone economy continues to remain in a weak spot but avoided contraction in the third quarter by growing at a lackluster real rate of 0.2%. Though recent German data (exports and factory orders) delivered a positive surprise, the chances of Germany experiencing recession are high. The eurozone needs a fiscal boost before external weaknesses spill over to its resilient domestic sector.

- Christine Lagarde officially took charge of the European Central Bank (ECB) at the start of the month, amid an uncertain economic outlook and a high level of internal dissent. With the ECB running out of tools and monetary policy losing potency, we believe the central bank is done for now. Lagarde is likely to press members to capitalize on low (or negative) rates by expanding fiscal policy.