”The man who moves a mountain begins by carrying away small stones.”

- Confucius

“When a long-term trend loses its momentum, short-term volatility tends to rise. It is easy to see why that should be so: the trend-following crowd is disoriented.”

- George Soros

During Q3 2019, “haven” assets were strongest among the primary asset classes.1 This followed a similar pattern from the second quarter. Long-dated US Treasury bonds led the way in the third quarter gaining 8.4%. Gold was up 4.3%. On the “risky” asset front, equities posted a modest gain of 1.8%. Commodities lost value in the third quarter, just as they did in the second quarter, down 3.8%. For the full year-to-date, all four primary assets remain positive, and meaningfully so: equities are up 20.4%, long-dated US Treasury bonds gained 19.7%, gold increased 14.5%, and commodities improved 7.4%.2

For additional benchmarking purposes, we can look at a global equity index and a broader bond index to get the most comprehensive perspective. The MSCI All Country World Index3 is up 16.4% year-to-date. The iShares Core US Aggregate Bond Index4 is up 8.3% year-to-date. A typical 60/40 mix is therefore up 13.2%.5

Equities ended the quarter positive, but it was a volatile three months. The S&P 500 made a high of 3026 on July 29 only to drop 6% in six trading days to 2847. The index then rallied back to 3022 by September 19 only to fall 5.5% to 2856 on October 3. Since then the index has continued to rally, ending the month at 3047 on October 31 and continuing to make new all-time highs as we write.

Given the significant year-to-date double-digit gains, is the recent equity market volatility a sign equity indices have come too far too fast and are at risk of a retracement? Manufacturing data in both the US and Europe show signs of a slowdown, it appears likely Q3 of 2019 will be the third quarter in a row for year-over-year declines in corporate earnings, and the “trade war” with China has clearly been distracting. On the other hand, some investors believe the Federal Reserve (along with other central banks) rate cutting will be stimulative. Our favorite gauges of market sentiment, credit spreads and Lowry’s market breadth indicators are relatively benign – supporting modest equity market increases.

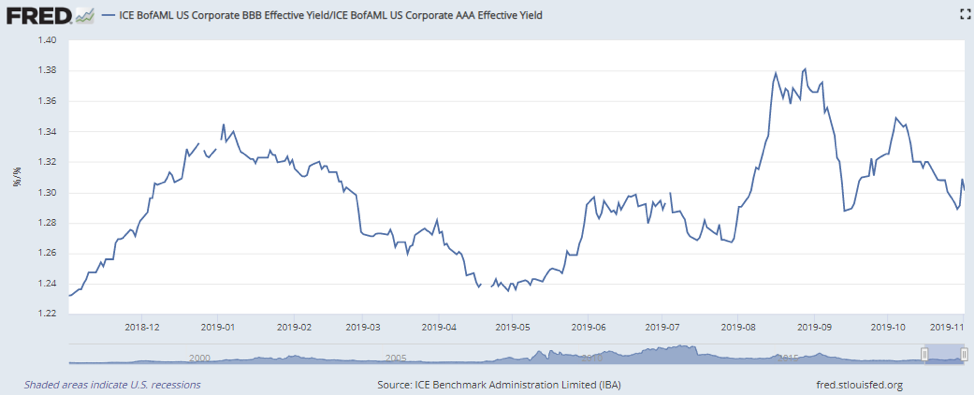

1 The ratio of BBB to AAA yields has essentially moved sideways for a year and remains well below the 150% level where HCWE & Co. suggests a recession is probable.

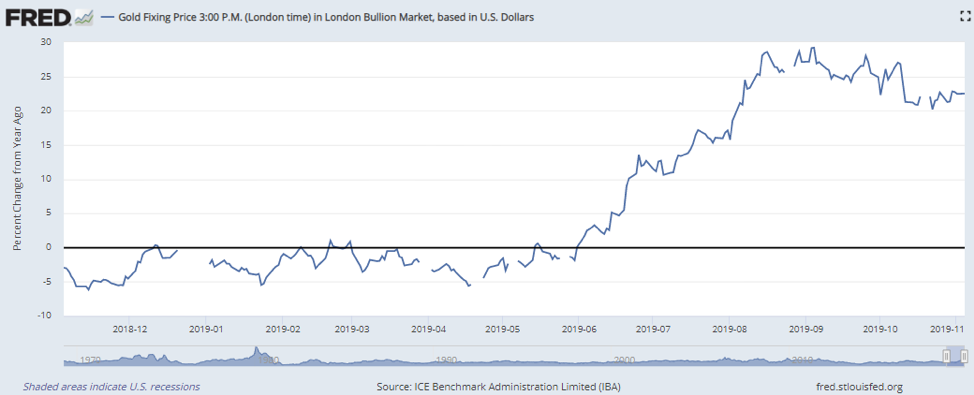

Gold, on the other hand, is indicating a significant change and a meaningful pickup in inflation. When we wrote to you last quarter, we explained how we increased portfolio exposure to gold (via GLD) in early July as gold started to show year-over-year increases.

2 On the inflation front, gold is up significantly on a year-over-year basis.

Additional (Inter-) Market Volatility: Between Equity Factors

Amidst the equity and bond market gyrations and the increase in gold, perceptive readers may note recent financial news headlines also signaling a rebirth in value investing. Some commentary explains value’s recent life as a shift away from growth and even a shift away from momentum’s outperformance. Simultaneous to the extreme positive moves in Treasury bonds and gold (“haven” assets) during the summer as the “trade war” with China developed, value began a short-term outperformance relative to growth and momentum. It began with a violent separation on September 9th when value outpaced momentum by over 3% and growth by 2.5%.6 The move has persisted. Between the market close on September 6 and the market close on October 31, value gained 4.4%, the S&P 500 is up 2.2%, growth gained just 0.4%, and momentum lost 2.1%.7

Momentum Backstory

Two years ago, the substance of our Q3 2017 letter discussed the prominent headlines of the period proclaiming the death of value investing. In that letter, we argued that despite a decade of underperformance, value investing still had merit and that cycles were both natural and typical. We pointed out that to some extent, value investing works because it subjects investors to lengthy periods of underperformance that create opportunities. Our defense of value investing aside, we also acknowledged that a decade long cycle of underperformance of any investment approach would test the patience of Job. The challenges with the “value factor,” along with our research showing momentum as an equally effective and complementary factor, led us to introduce momentum into our portfolio management process, mostly via MTUM, the iShares MSCI USA Momentum Factor ETF.

It is worth repeating that discussion of momentum from our Q3 2017 letter here:

Efforts to improve our existing investment process through question and study led us to examine what many believe is the antithesis of value investing: momentum.

Like value, momentum is an investment approach that demonstrates historical success, outperforming capitalization-weighted indices over long periods and across numerous markets and geographies. Unlike value, which is long-term oriented, momentum is essentially a short-term strategy. While the value investor buys an asset he deems cheap (either quantitatively or qualitatively) and expects over time the market will come to the same conclusion, the momentum investor buys an asset that is already performing well (with no regard for long-term value) in the expectation that the asset will continue to do well because of human behavioral/emotional traits.

Most interesting for the value investor is that while consensus wisdom holds that momentum is in direct conflict with value, it turns out momentum can be viewed as very much a complement to value. Empirical evidence shows that both value and momentum outperform the market over time and they are negatively correlated, so when combined, they enhance a portfolio. From a client’s perspective, adding momentum to a value portfolio will also smooth out periods of over/under performance and make the ride a little easier to tolerate without giving up the opportunity for outperformance.

Since that discussion, momentum has continued to outperform value. For the two-year period between September 30, 2017 and September 30, 2019 MTUM gained 28% while SPY gained 22.4%. VLUE (the iShares MSCI USA Value Factor ETF) gained just 11.5%.

Where to from Here?

Soros talks about the logical phenomenon of increased volatility around trend shifts and Confucius reminds us big actions begin with little steps. Does the recent volatility and value outperformance signal a long-term trend? From our seat, it is too early to tell, but it certainly is possible. Credit spreads and gold are highly predictive and the gold move is substantial. Increases in gold and benign or narrowing credit spreads have historically been positive for the value factor. If value does finally shine after a twelve-year hiatus, we believe our portfolios are well situated. We continue to hold significant positions in “value” securities. Jefferies (JEF), trading at around 75% of tangible book value, is a large and prominent example that we have discussed frequently. Fiesta Restaurant Group (FRGI) is another example. It trades at 6x operating earnings and near replacement cost. We purchased FRGI shares in May and September.

We continue to hold a position in the momentum ETF (MTUM) as it complements our value orientation but also because if value truly does take hold, it will, by definition, become momentum. Gold, and now to a lesser degree Treasury bonds (both via ETFs) make up the “haven” portion of client portfolios. For now, the bias is still toward risky assets but with an inflation bent. We will continue to adjust the portfolio as conditions change and opportunities present themselves.

*****

Sincerely,

Grey Owl Capital Management

Grey Owl Capital Management, LLC

This newsletter contains general information that is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. Past performance is no guarantee of future results. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock market involves the potential for gains and the risk of losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. Any information prepared by any unaffiliated third party, whether linked to this newsletter or incorporated herein, is included for informational purposes only, and no representation is made as to the accuracy, timeliness, suitability, completeness, or relevance of that information.

The stocks we elect to highlight each quarter will not always be the highest performing stocks in the portfolio, but rather will have had some reported news or event of significance or are either new purchases or significant holdings (relative to position size) for which we choose to discuss our investment tactics. They do not necessarily represent all of the securities purchased, sold or recommended by the adviser, and the reader should not assume that investments in the securities identified and discussed were or will be profitable. A complete list of recommendations by Grey Owl Capital Management, LLC may be obtained by contacting the adviser at 1-888-473-9695.

Grey Owl Capital Management, LLC (“Grey Owl”) is a Virginia registered investment adviser with its principal place of business in the Commonwealth of Virginia. Grey Owl and its representatives are in compliance with the current notice filing requirements imposed upon registered investment advisers by those states in which Grey Owl maintains clients. Grey Owl may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. This newsletter is limited to the dissemination of general information pertaining to its investment advisory services. Any subsequent, direct communication by Grey Owl with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of Grey Owl, please contact Grey Owl or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov).

For additional information about Grey Owl, including fees and services, send for our disclosure statement as set forth on Form ADV using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

1 We refer to US equities, long-dated US Treasury bonds, gold, and commodities as “primary” asset classes borrowing the language of HCWE & Company. The idea is that these four assets best capture two variables that explain a significant amount of asset price movement: global growth (explained by investor risk sentiment) and inflation. This framework is the basis for a permanent portfolio, an “all-weather” portfolio, risk-parity, etc.

2 The market (or asset class) returns are measured on a total return basis using index exchange traded funds (ETFs): SPY for the S&P 500, GSG for the S&P GSCI Commodity Index, TLT for 20+ Year Treasury Bond index (i.e. “long-dated” US Treasury bonds), and GLD for gold.

3 We use the ACWI ETF to measure the MSCI All Country World Equity Index.

4 We use the AGG ETF to measure the iShares Core US Aggregate Bond Index.

5 Technically, if one wanted to create a global 60/40 equity/bond benchmark they would use a global bond index. We are not aware of a global bond index ETF to track. We could incorporate IAGG, which is an international sibling of AGG, but that starts to get too messy and it would barely change the numbers above. IAGG is up 9.4% year-to-date.

6 This extreme one-day move is discussed in detail here: https://www.bloomberg.com/opinion/articles/2019-09-11/bond-market-holds-answer-to-momentum-stocks-crash-k0eqli9d and here: https://www.zerohedge.com/markets/quant-quake-20-fallout-nomura-warns-horrific-returns-momo-stocks-ahead

7 As with the primary assets discussed above, we use ETFs to measure factor performance. Value is VLUE, growth is IWV, and momentum is MTUM.

© Grey Owl Capital Management, LLC

Read more commentaries by Grey Owl Capital Management