Financial markets have been driven largely by five factors over the recent year. Considering these drivers of recent market behavior, I see a significant possibility that the market is overly pessimistic about the outlook.

The five market drivers are:

Slowing US economic growth. Growth has been steadily slowing since the middle of 2018 as the boost from fiscal stimulus has come out of the system. Invesco Fixed Income still believes US economic growth is migrating back toward its potential rate of around 1.8%, but that stabilization has not stopped the market from being concerned about the overall slowing growth trajectory.1 Slowing US growth has been a negative headwind for other countries and contributed to the global growth slowdown across developed market (DM) and emerging market (EM) countries.

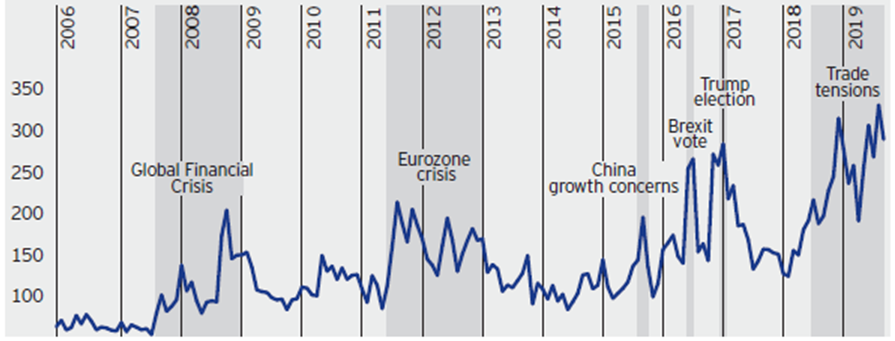

Global economic policy uncertainty. Uncertainty is high. Political trends are changing the environment for global policymakers across the globe and, in some instances, are changing their goals and reaction functions. Uncertainty about policymaker goals and objectives makes it more difficult for market participants to accurately discount prospective outcomes, and in my view, has increased volatility in markets. The Global Economic Policy Uncertainty Index has reached all-time highs over the last year (Figure 1).

Trade conflict. The escalation of trade conflict has been a direct headwind for global trade volumes, which have been steadily declining. Trade conflict has also impacted supply chains, increased uncertainty, and weighed on investment and capital expenditure plans. Companies’ natural reaction to trade uncertainty has been to hold off on longer-term investment plans.

Monetary policy interest rates. The steady increase in US policy rates in 2018 was a headwind for markets that culminated with the sharp market adjustments in the fourth quarter of 2018. Since then, the US Federal Reserve (Fed) has migrated to a more dovish stance and cut rates this year, which has been supportive of markets in 2019, offsetting some of the market headwinds from slowing growth, in our view.

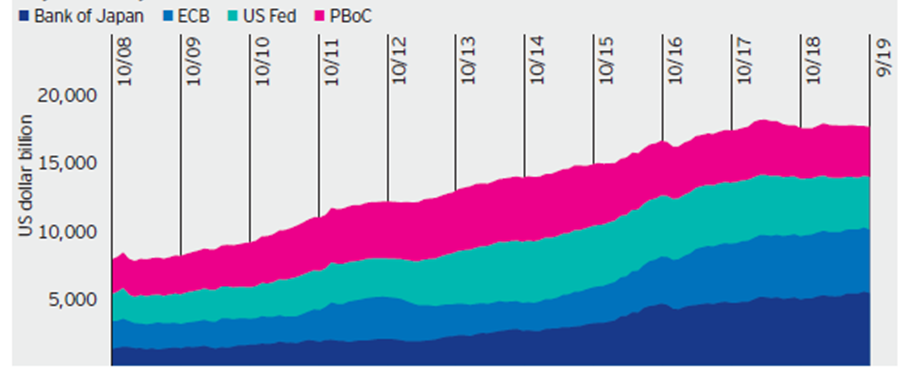

Central bank balance sheets. Central banks as a group aggressively expanded their balance sheets to support the global economy from the Global Financial Crisis up to the end of 2017. Since the end of 2017, however, the “big four” central banks, the Fed, the European Central Bank (ECB), the Bank of Japan (BoJ), and the People’s Bank of China (PBoC), have allowed the aggregate of their balance sheets to shrink (Figure 2). This has been led by the Fed and the PBoC but has not been offset by the increases at the ECB and BoJ. This shrinking aggregate balance sheet has been a headwind for the market.

Bad news is priced into the market

The market currently appears priced for slowing global growth and there are worries of a possible recession in the US. We believe the US economy will grow at a pace close to potential (we expect around 2% per year), driven by the solid labor market, wage growth, and strong consumer demand. As an indication of the market’s pessimism on global growth, the International Monetary Fund recently revised down its growth estimates for 2019 and 2020 for both EM and DM economies across the globe. Without a US recession, we do not anticipate significant further slowing in global growth.

Economic policymaker uncertainty and trade conflict is here to stay, in our view, but should be priced into the market at this point. At the margin, there is also the possibility of some good news on this front. The chances of a hard Brexit are falling, and both the US and China have incentive to look for some potential wins. The recent mini-deal announced by the US and China is a good example.

Policymakers continue to ease. After tightening policy in 2018, global central banks have been easing in 2019. The Fed has cut rates, and we believe it will likely continue to cut at its meeting at the end of October. Importantly, central bank balance sheets are moving back to an expansionary trend, starting now. The ECB has announced more quantitative easing (QE), and the Fed balance sheet, which has been steadily shrinking, will likely pivot sharply to expansion going forward, in our view. The Fed has announced plans to buy $60 billion of US Treasury bills monthly for the near future to support the functioning of the US money markets. The Fed has gone to great efforts to characterize this as a technical adjustment, not QE, but a balance sheet expansion is a balance sheet expansion, regardless of what you call it.

The combination of avoiding a recession in the US, pricing in bad news globally, and a pivot toward easier monetary policy may mark a change in market behavior going forward. A reversal of some of the recent market trends is possible. This could include a steepening of the US yield curve, reversal of US dollar strength, and solid performance from risky assets globally, including EM and equities. In fixed income, longer duration assets have performed strongly year-to-date.2 This may change to favor lower duration credit assets going forward.

Figure 1: Global Economic Policy Uncertainty Index

Source: Bloomberg, L.P., data from Jan. 1, 2006 to Sept. 30, 2019.

Figure 2: Big four central bank assets

Source: Bank of Japan, European Central Bank, US Federal Reserve, People’s Bank of China, data from Oct. 31, 2008 to Sept. 20, 2019.

1 Source: Invesco, Oct. 30, 2019.

2 Source: Bloomberg L.P., Global Aggregate Total Return Index Hedged, Jan. 1, 2019, to Oct. 30, 2019.

Important Information

Blog header image: Annie Spratt / UnSplash

Quantitative easing (QE) is a monetary policy used by central banks to stimulate the economy when standard monetary policy has become ineffective.

The Global Economic Policy Uncertainty Index is a GDP-weighted average of national Economic Policy Uncertainty indices for 20 countries. The national indicies track newspaper coverage of policy-related economic uncertainty.

The International Monetary Fund is an organization of 189 countries, and its primary purpose is to ensure the stability of the international monetary system.

The opinions referenced above are those of the author as of Oct. 30, 2019. These comments should not be construed as recommendations, but as an illustration of broader themes. Forward-looking statements are not guarantees of future results. They involve risks, uncertainties and assumptions; there can be no assurance that actual results will not differ materially from expectations.

Rob Waldner is Chief Strategist and Head of Macro Research for Invesco Fixed Income (IFI). Mr. Waldner chairs the IFI Investment Strategy team (IST) and is responsible for oversight of the overall IFI investment process; he oversees portfolio risk monitoring and review for IFI portfolios. Mr. Waldner also leads the overall investment and business strategy for IFI’s quantitative strategies. He joined Invesco in 2013.

Prior to joining Invesco, Mr. Waldner worked with Franklin Templeton for 17 years, where he was a senior strategist and senior portfolio manager. He was the lead manager for the firm’s absolute return strategies and a member of the fixed income policy committee. Mr. Waldner was instrumental in the launch of a number of new strategies on the Franklin Templeton fixed income platform. Previously, Mr. Waldner was a member of the macro team at Omega Advisors and a portfolio manager with Glaxo (Bermuda) Ltd. He entered the industry in 1986.

Mr. Waldner earned a BSE degree in civil engineering from Princeton University, graduating magna cum laude in 1986. He is a Chartered Financial Analyst® (CFA) charterholder.