NewsLetter – November 2019

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsDEAR READER,

PERSPECTIVE

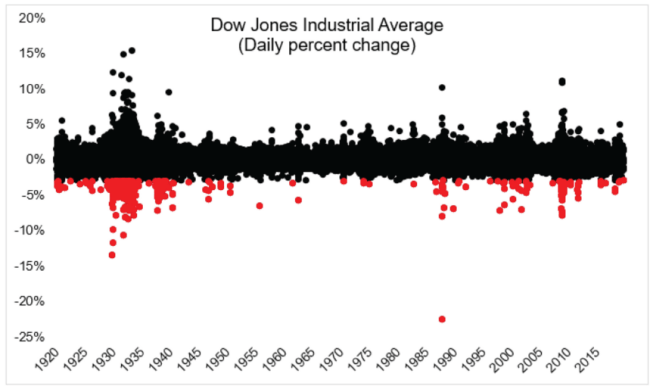

From Michael Batnick, of Ritholtz Wealth Management, via my friend Bob Veres.

Recently, the DOW fell 3% in one day. That was the 307th time the Dow has fallen 3% in a day over the last one hundred years.

OSTRICH PLANNING

Almost Half of All Americans Fear They’ll Outlive Their Savings

“This is actually a pretty big worry for many of us, with respondents to a recent survey by the financial services company Northwestern Mutual indicating that, on average, there’s a 45% chance they’ll outlive their savings. Yet despite fears about ending up a broke senior, 41% of respondents said they haven’t taken any steps to address this concern.

“There’s a very real chance many people won’t have enough money to support them through their later years—especially as the same survey found 22% of Americans have under $5,000 saved for retirement and 15% have nothing saved at all.”

Don’t let this be YOU!

https://www.fool.com/retirement/2019/09/08/almost-half-of-all-americans-fear-theyll-outlive-t.aspx

AND THE WINNER IS…

According to a recent Gallup poll, some 63% of American adults drink alcohol—and their favored beverage is beer. Some 42% of American drinkers prefer beer, compared to 34% who choose wine, and just 19% who enjoy spirits the most.

THE TEN BEST AND WORST

…states to retire in, according to WealthManagement who considered affordability, crime ranking, culture ranking, weather ranking, and wellness ranking:

BEST

- Nebraska

- Iowa

- Missouri

- South Dakota

- Florida

- Kentucky

- Kansas

- North Carolina

- Montana

- Hawaii

WORST

- Oregon

- Nevada

- Illinois

- Washington

- Maryland

- New York

- Alaska

- California

- New Jersey

- South Carolina

NO END IN SIGHT?

Cost Of Employer-Provided Health Coverage Passes $20,000 Per Year

“According to a new survey from the Kaiser Family Foundation, the average cost for an employer-provided family health insurance plan in 2019 has surpassed $20,000 per year, clocking in at $20,576 (a 5% increase from 2018), with employers bearing on average 71% of the cost … The real concern and question, though, is why costs continue to rise, especially since a recent Health Care Cost Institute study found that health care utilization declined by 0.2% from 2013 to 2017, even as average prices increased by 17.1%.”

A NEW FORM OF HIGH?

Notes from a cannabis investment fund manager:

- Investable universe. As of the end of the second quarter, approximately 350 to 400 small-, mid-, and large-cap companies around the world were engaged in the cannabis industry.

- Promising legislative developments. Canada is in the process of implementing “Cannabis 2.0,” which will provide guidance on recreational consumption of edibles, concentrates and topicals that contain cannabis. Cannabis 2.0 may be significant to companies that grow, distribute or sell these products.

- A growth trend in CBD. Biosynthesis of the cannabinoid (CBD) compounds in the cannabis plant has the potential to be crucial to long-term growth. Many companies are looking to produce cultured cannabinoids as they are seeking to perfect the consistency and purity of the CBD.

DON’T MESS WITH LITTLE KIDS

From my friend Saby:

- A little girl was talking to her teacher about whales.

The teacher said it was physically impossible for a whale to swallow a human because even though it was a very large mammal its throat was very small.

The little girl stated that Jonah was swallowed by a whale.

Irritated, the teacher reiterated that a whale could not swallow a human; it was physically impossible.

The little girl said, “When I get to heaven, I will ask Jonah.”

The teacher asked, “What if Jonah went to hell?”

The little girl replied, “Then you ask him.”

- A kindergarten teacher was observing her classroom of children while they were drawing. She would occasionally walk around to see each child’s work.

As she got to one little girl who was working diligently, she asked what the drawing was.

The girl replied, “I’m drawing God.”

The teacher paused and then said, “But no one knows what God looks like.”

Without missing a beat, or looking up from her drawing, the girl replied, “They will in a minute.”

- A Sunday school teacher was discussing the Ten Commandments with her five and six year olds.

After explaining the commandment to “honor” thy Father and thy Mother, she asked, “Is there a commandment that teaches us how to treat our brothers and sisters?”

From the back, one little boy (the oldest of a family) answered, “Thou shall not kill.”

- The children were lined up in the cafeteria of a Catholic elementary school for lunch. At the head of the table was a large pile of apples. The nun wrote a note, and posted it on the apple tray:

“Take only ONE … God is watching.”

Moving further along the lunch line, at the other end of the table was a large pile of chocolate chip cookies.

A child had written a note, “Take all you want. God is watching the apples.”

NOT MY FAVORITES

However, for those of you that like these alternatives….

Gold’s price has risen 19% so far this year to around $1,520 per ounce, as investors have reportedly been shunning risky assets and moving to safer assets such as gold.

Interestingly, bitcoin enthusiasts insist on calling the cryptocurrency a “safe haven” asset. But according to analysis from The Block’s research analyst Ryan Todd, it is not. Bitcoin has seen an average 12.4% annualized 30-day volatility over the last five years, as compared to gold’s 2.5%.

https://finance.yahoo.com/news/investors-gold-holdings-3rd-consecutive-121012323.html

OF COURSE, NOT EVERYONE AGREES, AT LEAST IN THE SHORT TERM

Forbes September 15: Gold Correction Underway

Here is a summary of the bearish influences on the metal price:

- Sentiment is too bullish.

- The weekly graph shows a hook sell signal, a sign of coming weakness.

- The monthly cycle topped on the 11th and the weekly cycle does likewise on the 17th.

- The combination of the bullish sentiment and the cycle tops point to a volatile week to the downside for gold. There is an irregular cycle that bottoms on the 20th, which has set off short-term rallies in the past. This is likely to touch off a short-term rally in the last week of the month.

- Both cycles bottom in the second week of October.

I expect gold to fall to at least $1440, the 38.2% retracement of the prior uptrend, before the uptrend resumes.

https://www.forbes.com/sites/greatspeculations/2019/09/15/gold-correction-underway/

WHAT EVER HAPPENED TO LONG TERM?

I believe kiplinger is an excellent magazine and that John Waggoner is one of the best financial writers around, but “Two Ways to Beat the S&P” was a bit disturbing.

“The Kiplinger Dividend 15, our favorite stocks for dividend income, have been riding the bull since we last checked on them in the April issue of Kiplinger’s.” It’s nice to know that it’s done well for 3 months but that seems more like dangerous noise then useful investment guidance.

Besides, focusing on dividend return and not total return can be dangerously myopic. As Jason notes in his closing, “Ideally, the companies would boost their dividend to get over our 4% threshold, but the price decline could also do the trick. Let’s hope for the former, but be prepared for the latter.” Hope doesn’t sound like a good plan, and I have no idea what “prepare for the latter” means.

SPEAKING OF “LONG TERM”

More financial pornography:

Gone to Pot: 20 ETFs That Have Had a Rough Three Months

Agriculture and international funds, including ETFMG’s Alternative Harvest ETF (MJ), posted the worst returns over the past three months.

I guess that’s better than “a rough time in the last 10 minutes.”

https://www.wealthmanagement.com/etfs/gone-pot-20-etfs-have-had-rough-three-months

20 PEOPLE WHO HELPED SHAPE THE FINANCIAL PLANNING INDUSTRY

50TH ANNIVERSARY OF FINANCIAL PLANNING: FINANCIAL PLANNING FOUNDERS STARTED A MOVEMENT — AND CREATED A PROFESSION

Cool!

Harold & Deena Evensky

GOOD NEWS FOR THE RICH

IT’S OFFICIAL

End of Era: Passive Equity Funds Surpass Active in Epic Shift

It’s official: inexpensive index funds and ETFs have finally eclipsed old-fashioned stock pickers.

Passive investing styles have been gaining ground on actively managed funds for decades. But in August, the investment industry reached one of the biggest milestones in its modern history, as assets in US index-based equity mutual funds and ETFs topped those in active stock funds for the first time.

HELP!

My passport is about to expire (or it’s lost) and I travel in a few days.

If you’re desperate and are prepared to pay $500–600, there is a reasonably convenient solution. You can visit one of FedEx Office’s 2,000 locations, or solve your problems online…

Taking care of things in person is a better option if you need to get your passport photograph taken. Any FedEx Office location offers photo services. After the photo, customers are guided to a computer area of the store and shown how to complete the transaction online.

You’ll have to pay a government fee of $170, but then rates skyrocket from there based on how quickly you need the goods. The price will depend on your timetable. Same-day service will cost you $449, while the cheapest and slowest option, 8–10 days, costs $119. Then there are shipping costs. FedEx standard overnight is $29.95, FedEx priority overnight is $39.95, and FedEx priority overnight including a Saturday is $54.95.

Note that just because you are processing it in one business day doesn’t mean you’re getting your passport back in one business day. In most cases, your passport still has to be shipped to you.

“For example, by choosing the 24-hour service option on Monday, FedEx will receive your application and begin processing Tuesday morning,” the FedEx website reads. “By Tuesday afternoon, your passport will be shipped to you for Wednesday delivery. You may be eligible to pick up your passport Tuesday afternoon or have it delivered the same day in select cities.”

WHAT YOUR ADVISOR ISN’T TELLING YOU

Excerpt from an excellent Kiplinger article:

“Ask the advisor to sign a fiduciary oath.”

Needless to say, I agree and recommend the Committee for the Fiduciary Standard “mom and pop” oath.

http://www.thefiduciarystandard.org/wp-content/uploads/2015/02/fiduciaryoath_individual.pdf

FREE MAY BE VERY EXPENSIVE

More good advice from Kiplinger:

“One of the more popular prospecting strategies for financial advisers over the last couple of decades has been the dinner seminar. While its popularity has waned recently, with new marketing strategies taking hold, there are still plenty of seminar dinners still taking place…

“In order to make these expensive presentations work from a profitable business model standpoint, these dinners can often be sales tools to sell high-commissioned products. Many presenters push products that maximize the YTB. That stands for Yield to Broker, which may not end with a good result for the client.”

So, be cautious of a “Free Steak Dinner” offer. It could end up being one of the more expensive meals of your life!

Caveat emptor.

WOE BETIDE THE HEDGE FUND MARKETER

Looks like I’m not the only hedge fund skeptic.

From Institutional Investor:

“Investor relations professionals are finding it challenging to secure clients as investors continue to pull billions of dollars out of hedge funds … Regardless of firm size or assets under management, luring investors was seen as a top challenge by survey respondents. In the hedge fund industry, these challenges are further evidenced by five consecutive quarters of outflows, amounting to $62 billion redeemed by investors on a net basis between April 2018 and June 2019, according to HFR.”

FOR YOUR BUCKET LIST

North Pole Igloos — $105,000/per night

Located in the North Pole and claiming the title of “northernmost hotel in the world,” these igloos will cost you $105,000. Thankfully, that price tag includes more than just a night in a glass dome. You will also be given two nights in Svalbard, Norway, flights between Svalbard and the North Pole, one night in the igloo itself, chef-prepared meals, security and an Arctic wilderness guide. However, you’ll still have to coordinate your flight to the isolated island of Svalbard in Norway.

If that’s a bit pricey, you might consider…

The Muraka at the Conrad Maldives — a bargain at $50,000/per night

The Muraka suite is the world’s first underwater hotel suite—and comes with a pretty price of $50,000 a night. However, there’s a four-night minimum stay required, so you’re looking at $200,000 to sleep with the fish. This suite is two stories tall, with the underwater portion being 16 feet below the Indian Ocean. What can you expect for $50k a night? You’ll enjoy a private chef, butler, boat, bar, gym, and infinity pool. In addition to all of that, you’ll automatically be upgraded to Hilton Diamond status.

https://thepointsguy.com/news/worlds-most-expensive-hotel-rooms/

GOODNESS

From my friend Mark:

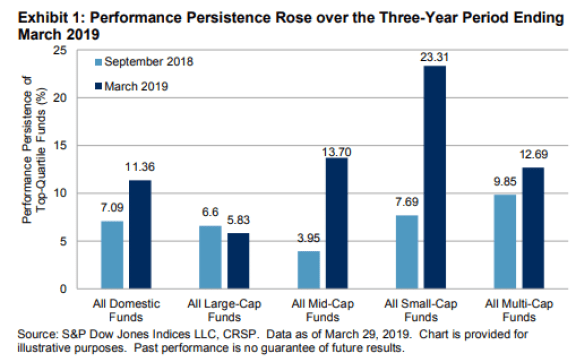

HOPE MAY SPRING ETERNAL BUT PERSISTENCE DOESN’T

From S&P Dow Jones Indices research — A REALLY IMPORTANT LESSON.

One key measure of successful active management lies in the ability of a manager or a strategy to outperform their peers repeatedly. Consistent success is the one way to differentiate a manager’s luck from skill. The S&P Persistence Scorecard shows that few funds consistently outperformed their peers:

- 4% of domestic equity funds remained a top-quartile fund over the three-year period ending March 2019.

- The ability of top-performing funds to maintain their status typically fell over longer horizons. For example, zero large-, mid-, or multi-cap funds maintained their top-quartile status at the end of the five-year measurement period.

- Top-performing funds were more likely to become the worst-performing funds than vice versa over the five-year horizon. While 15.3% of bottom-quartile domestic equity funds moved to the top quartile, a greater percentage (31.5%) of top-quartile funds moved to the bottom quartile during the same period.

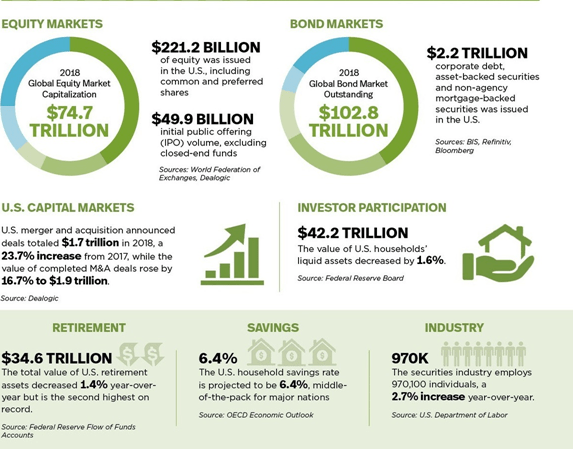

SOME INTERESTING STATISTICS

From the 2019 SIFMA Capital Markets Fact Book:

https://www.sifma.org/wp-content/uploads/2019/09/2019-Capital-Markets-Fact-Book-SIFMA.pdf

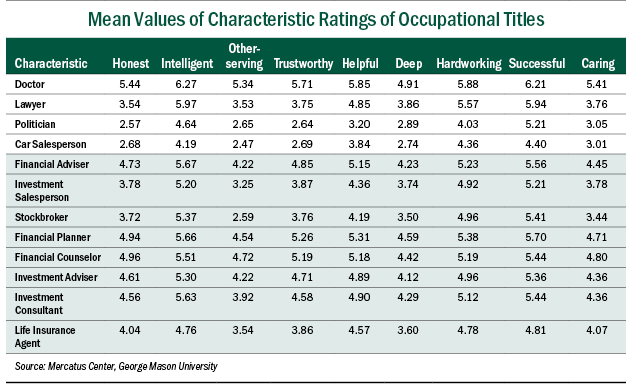

FINANCIAL PLANNERS LOOKIN’ GOOD

“Advisors” Score Highest in Intelligence While “Brokers” Score Lowest in Trustworthiness in Survey Showing Titles Matter

“Portland, Maine-based Tharp authored the “Consumer Perceptions of Financial Advisory Titles and Implications for Title Regulation” paper for the Mercatus Center at George Mason University. He is an assistant professor of finance at the University of Southern Maine.

Among the financial professional titles, ‘financial planner’ scored the highest in trustworthiness, helpfulness, depth, work ethic and success. ‘Financial advisor’ scored the highest in intelligence. ‘Financial counselor’ was on top in honesty, serving the interest of others and caring.

In contrast, ‘broker’ scored the lowest in honesty, serving the interest of others, trustworthiness, helpfulness, depth and caring. ‘Life insurance agent’ scored the lowest in intelligence, work ethic and success.”

THE BEST SONG EVER

GOOD ONES

From my #1 son:

RICH PEOPLE

Seems like there are a bunch.

At Family Office Exchange (FOX), one of the questions we hear most frequently is: “How many single family offices (SFOs) are there?”

Recently, Family Wealth Report estimated that there were about 6,000. Campden Wealth puts the figure at 7,300…

According to the Wall Street Journal, the threshold for SFOs is generally considered to be $100 million due to the costs and challenges of running such an entity. In the United States alone, there are approximately 20,407 individuals with more than $100 million in assets, as reported in the Credit Suisse 2018 Global Wealth Report.

https://www.wealthmanagement.com/high-net-worth/how-many-family-offices-are-there-united-states

THE FOX GUARDING THE HEN HOUSE

The Senate confirmed Mr. Scalia to head the agency [the Securities and Exchange Commission – SEC]. He now takes over a department whose fiduciary rule to raise investment advice standards in retirement accounts he was instrumental in killing.

Mr. Scalia, formerly a partner at Gibson Dunn & Crutcher, was the lead counsel in a lawsuit against the DOL rule. Representing financial industry opponents of the regulation, Mr. Scalia argued that the regulation was too costly and that the DOL had overstepped its authority in promulgating it.

WHAT, ME WORRY?

From planadvisor, July–August 2019:

What advisors predict will be clients’ three greatest worries for the next 12 months, and what clients say those actually are:

Advisors Investors

Increased market volatility 56% 66%

Cost of health care 27% 33%

Taxes 26% 31%

Safety of their assets 26% 27%

Inadequate savings for retirement 26% 23%

Inflation/Rising interest rates 24% 16%

Who knew there were so many things to worry about?

PERKS OF PERSEVERANCE

Also from planadvisor:

Participants who remained in their 401(k) in the decade following the Great Recession of 2008 saw their average balances soar 466%, from $52,600 in the first quarter of 2009 to $297,700 in the first quarter of 2019.

REMEMBER THIS?

From my friend Alex:

I remember them all.

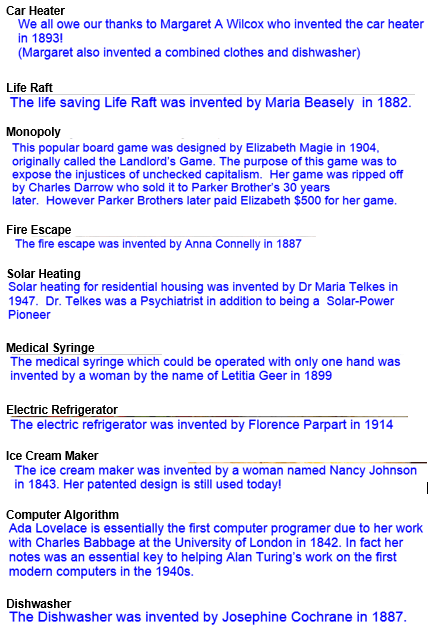

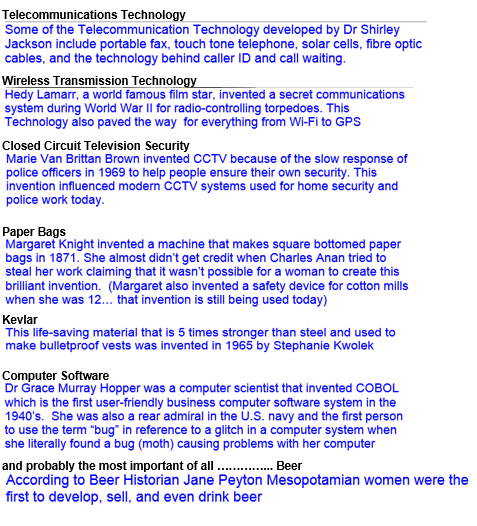

THANK YOU, WOMEN!!!

Inventions by women from my friend Judy:

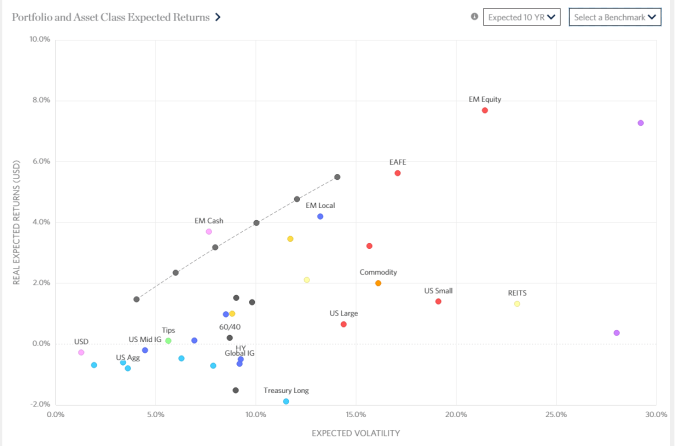

THE FUTURE ACCORDING TO RESEARCH AFFILIATES

https://interactive.researchaffiliates.com/asset-allocation

LOOKS LIKE I’M NOT ALONE

In questioning the wisdom of opening up investing in unregistered securities to unsophisticated investors:

State securities regulators are skeptical of the idea of loosening rules surrounding unregistered securities to allow ordinary investors to buy them.

“Earlier this year, the Securities and Exchange Commission issued a concept release focused on simplifying and harmonizing regulations on the sale of nonpublic investments, or private placements. Under current rules, individuals need to meet certain income and wealth thresholds to make such purchases.”

THINKING OUTSIDE OF THE BOX

Woman uses hair dryer to stop speeders

The Montana Highway Patrol awarded a grandmother with the unofficial title of “honorary state trooper” after she has attempted to slow down speeders in her neighborhood using a hair dryer.

https://www.cnn.com/videos/us/2019/09/14/montana-woman-uses-hair-dryer-to-stop-speeders-pkg-vpx.kpax

2019 TAX SEASON AT A GLANCE

Journal of Accountancy:

Total returns received $141.6 million

F-filings, by tax professionals $71.7 million

E-filings, self-prepared $56.2 million

Total refunds $101.6 million

Average refund $2,729

WHAT THE EXPERTS EXPECT

Journal of Accountancy survey of 785 CPA decision-makers, August 2019:

Portion of financial leaders who felt positive about the U.S. economic outlook in the second quarter : 57%

Portion who were positive about the global economy: 35%

Portion who cited inflation concerns: 29%

Portion who had inflation concerns at the end of 2018: 49%

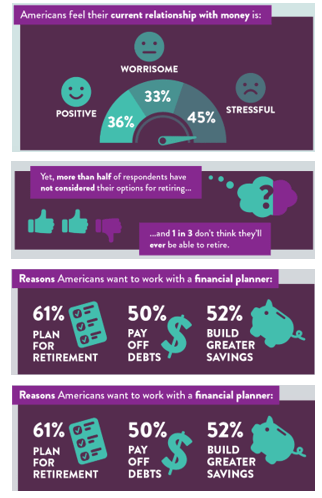

STRESSED

From my friend Taft:

The bad news from a NAPFA Survey (but the good news is financial planning can help):

https://www.napfa.org/the-state-of-financial-planning-in-america

THE FUTURE REALLY AIN’T WHAT IT USED TO BE (MAYBE)

Google Claims “Quantum Supremacy,” Marking a Major Milestone in Computing

In what may be a huge milestone in computing, Google says it has achieved “quantum supremacy,” an experimental demonstration of the superiority of a quantum computer over a traditional one.

The claim, made in a new scientific paper, is the most serious indication yet that the promise of quantum computers—an emerging but unproven type of machine—is becoming reality, including their potential to solve formerly ungraspable mathematical problems…

“While our processor takes about 200 seconds to sample one instance of the quantum circuit 1 million times, a state-of-the-art supercomputer would require approximately 10,000 years to perform the equivalent task,” the researchers said.

The researchers estimate that performing the same experiment on a Google Cloud server would take 50 trillion hours—too long to be feasible. On the quantum processor, it took only 30 seconds, they said.

https://fortune.com/2019/09/20/google-claims-quantum-supremacy/

IT’S NOT EASY

Some investors believe investing is a game easily won and the best opportunities are in exotic investments. A few tidbits from a recent story about Harvard’s Endowment might help frame that unreality.

Harvard Was “Freaking Out”: How A $270 Million Bet Tanked

“Colin Butterfield was frantic. The Harvard University endowment executive wanted to unload a disastrous $270 million investment in Brazilian farmland. But the school had no takers, and it was burning through millions of dollars…Harvard’s fear manifests itself in 2,000 pages of Brazilian court records…

“The documents, many in Portuguese, offer a window into a debacle that has contributed to the lackluster performance of the world’s largest college endowment. Part of the reason: Harvard’s backfired bet on the most exotic of investments, direct holdings of agriculture in the developing world.

“Auditors wrote down the value of the Brazil farm project by about $200 million after the endowment decided to exit the development in 2017, according to the lawsuit. Even for Harvard, which has a $39 billion endowment, that’s a steep sum, about as much as the Ivy League school spends annually on undergraduate financial aid.”

https://www.fa-mag.com/news/harvard-was–freaking-out—how-a–270-million-brazil-bet-tanked-51859.html

WELCOME TO THE FUTURE

AND MORE “I’M OLD”

- Bonanza premiered 60 years ago

- The Beatles split 50 years ago

- Lafon Premier nearly 52 years ago

- The Wizard of Oz is 80 years old

- Jimi Hendrix and Janis Joplin have been dead 49 years

- Back to the Future is 35 years old

- Saturday Night Fever is 42 years old

- The Corvette turned 66 this year

- The Mustang is 55.

INDIVIDUAL STOCK INVESTING INCREASES RISK

Before you decide to do a bit of individual stock picking, consider the following:

Larry Swedroe, one of the most thoughtful, academically practitioners I know, wrote an interesting review in Advisor Perspectives, a publication sharing ideas of experienced practitioners. Here are a few items from Larry’s contribution.

“A study in the Journal of Financial Economics, looking at overall returns from 1926 through 2015, and including all common stocks listed on the NYSE, Amex and NASDAQ exchanges. Returns are inclusive of dividends and thus assume investors reinvest dividends in the stocks that paid them. The study found that only 47.7% of all annual returns were larger than the one-month Treasury rate…

“The conclusion here is that owning stocks is not unlike playing the lottery; you need to hold a majority of the tickets in order to justify playing at all. Of course, you have a better-than-even chance of winning a stock market investment, but you need to be diversified to have a break-even chance. Most stocks have negative risk premiums…

“Yet another study covering the period 1983 through 2006 focused on the Russell 3000 index. The index produced an annualized return of 12.8% and a cumulative return over that time period of 1,694%. But the mean annualized return of the 3,000 stocks was -1.1%. 39% of stocks lost money during the period and 19% lost at least 75% of their value, before considering inflation. Just 25% of the stocks were responsible for all the market’s gains.”

https://www.advisorperspectives.com/articles/2019/09/17/individual-stock-investing-increases-risk

2.96 MILLION?! WHO KNEW?

“Passive proliferation slows, with 770,000 indexes scrapped in 2019. But the number of fixed-income indexes expanded, as did ESG indexes.”

The seemingly inexorable march of passive investing looks to have hit a roadblock.

The number of indexes around the world fell more than 20%, to 2.96 million, in 2019 as benchmark providers scrapped some of their gauges, according to a new report from the Index Industry Association.

If I’d been asked, I would have guessed a few hundred—certainly far fewer than a thousand.

BANK OF AMERICA DECLARES ‘THE END OF THE 60/40’ STANDARD PORTFOLIO

“Investors have long been told that the ideal portfolio should carry 60% of its holdings in equities and 40% in bonds, a mix that provides greater exposure to historically superior stock returns, while also granting the diversification benefits and lower risk of fixed-income investments.

But in a research note published by Bank of America Securities titled ‘The End of 60/40,’ portfolio strategists Derek Harris and Jared Woodard argue that ‘there are good reasons to reconsider the role of bonds in your portfolio,’ and to allocate a greater share toward equities…

“The future of asset allocation may look radically different from the recent past.” they wrote, “and it is time to start planning for what comes after the end of 60/40.”

The idea that any specific allocation is “ideal” for all investors is nonsense. I also hope that no one has a fixed asset allocation that is not frequently reviewed. The concept is not “buy and forget” but “buy and manage.” Although our allocations are strategic, they are constantly reviewed and do change over time.

THE REPORTS OF MY DEATH ARE GREATLY EXAGGERATED

Same song, second verse….

Some earlier headlines from my associate Marcos.

- “Why the 60/40 Asset Allocation Rule is Dead”—April 25,2013

- “Death of the 60/40 portfolio”—February 20, 2015

- “60-40 Is Dead”—October 29,2015

MORE ON THE 60/40

Also from my associate Marcos:

The 60/40 portfolio passed away on October 16, 2019, from complications of low interest rates and a bad case of Fed manipulation. This is the twenty-seventh time 60/40 has died in the past decade but enemies market timing, day traders, and alternative investments are hopeful it will stick this time around.

60/40 was 91 years old and lived a long and prosperous life, returning more than 8.1% a year. This nearly matched the return of 60/40’s best friend, the S&P 500 (9.5%), but it did so with 40% less volatility.

60/40 was such a bright light in a world often full of darkness. It was down in just 20 of its 91 years on this planet. And it was just four years old when it had its worst year in 1931 (down 27%). 60/40 finished out its life strong, returning an astonishing 10.2% per year from 1980–2018 with just five down years over the past 39 years. That was much better than the 6.9% annual return from the day the portfolio was born in 1928 through 1979.

There were some lean years when 60/40 was learning how to walk early on. After rising 27% by the time it turned one, 60/40 fell 40% over the next four years during the Great Depression.

60/40 set a good example, as it was the most popular benchmark against which other investment portfolios often compared themselves. Many were envious of the performance of the 60/40 portfolio because it was so simple. They could never wrap their heads around the fact that a mix of stocks and bonds, rebalanced periodically, could outperform so much of the professional investment universe.

I’ve shared many a conversation with 60/40 over beers about how complex so many professional investors try to make their portfolio. 60/40 would often shake its head and laugh when thinking about it. I’ll miss those conversations.

Two of 60/40’s most redeeming qualities were balance and risk mitigation. There were just four times in the portfolio’s 91-year history that both stocks and bonds fell during the same year: 1931, 1941, 1969, and most recently in 2018.

60/40 was always there for its investor friends when they needed it, but it did have a wild side that would rear its ugly head from time to time. The stock portion of its personality was down 25 years of its 91-year lifetime. The average loss for stocks during those 25 years was more than 13%. But 60/40 had a more stable, rational side of its personality that balanced out these wild times. During those 25 down years in the stock market, bonds averaged a gain of more than 5%, dampening some of the losses and allowing 60/40 to live to fight another day when things got bad.

60/40 was remarkably stable and someone you could count on over the long haul. It never had a 10-year period where it lost money. Many of you will remember that 10-year stretch from ’82 to ’91 where 60/40 went on a ridiculous run, returning nearly 350%. In five out of those 10 years, it saw returns of more than 20% and four of those years were over 30%! We all had a blast despite that wicked hangover from the Black Monday party in 1987.

But even when things were the bleakest, from 1929–1938, 60/40 still earned a respectable 20% total return, even in the face of mounting adversity.

Investors will now have to grapple with the fact that with the passing of the 60/40 portfolio, diversification is also dead. One of 60/40’s early mentors, Peter Bernstein, once said, “Diversification is the only rational deployment of our ignorance.” It’s a shame we will now have to figure out other ways to deploy our ignorance if stocks and bonds no longer offset one another.

It’s sad because 60/40 didn’t have to end this way. Investors could have simply diversified more widely across different geographies, asset classes and strategies, saved more money or adjusted their expectations.

60/40 is survived by its immediate family—wife, asset allocation, and children Vanguard, rebalancing and comprehensive investment planning. Distant relatives include crypto, pot stocks, and technology IPOs, but they were all left out of the will.

Donations can be made to your own IRA, 401k, or brokerage account on a regular basis in 60/40’s honor.

RIP, 60/40 portfolio. You will be missed. I hope to see you again someday in the big retirement portfolio in the sky, where interest rates are always 6% and stock market valuations never go above 15 times the previous 10 years’ worth of average earnings.

https://awealthofcommonsense.com/2019/10/a-eulogy-for-the-60-40-portfolio/

MY NEVER-ENDING SOAPBOX: REGULATION BEST INTEREST

I placed this at the end in case you’re in the mood for some serious stuff.

The debate over Congressional, regulatory and court activities regarding the issues related to protecting investors interest in the financial world has been going on for decades, but it has reached a fever pitch in the last year or so. The latest manifestation is the SEC’s release of what has become known as the “Best Interest Rule.”

Let me preface this with the observation that, as readers of my past NewsLetters know, I’m extremely biased on this subject.

Below are excerpts from the SECs new Rule and my thoughts noted in brackets and indented.

“SEC adopts rules and interpretations to enhance protections and preserve choice for retail investors in their relationships with financial professionals.

“With the adoption of this package, regardless of whether a retail investor chooses a broker-dealer or an investment advisor (or both), the retail investor will be entitled to a recommendation (from a broker-dealer) or advice (from an investment advisor) that is in the best interest of the retail investor and that does not place the interests of the firm or the financial professional ahead of the interest of the retail investor…”

[From the dictionary:

Recommendation – a suggestion or proposal as to the best course of action, especially one put forward by an authoritative body. Synonym : advice

Advice – guidance or recommendations offered with regard to prudent future action

Begs the question: if there is no fundamental difference between suitability (brokers) and fiduciary (registered investment advisors) as reflected below, why not just hold everyone to the fiduciary standard?]

“This rulemaking package will bring the legal requirements and mandated disclosures for broker-dealers and investment advisors in line with reasonable investor expectations…”

[As you read this, you decide if it’s in line with reasonable expectations. I’ve been practicing for over 30 years and don’t find it remotely reasonable.]

Solely Incidental Interpretation

The broker-dealer exclusion under the advisor act excludes from the definition of investment advisor – and thus from the application of the Advisers Act – a broker or dealer whose performance of advisory services is solely incidental to the conduct of his business as a broker or dealer and who receives no special compensation for those services. The interpretation confirms and clarifies the Commission’s interpretation of the “solely incidental” prong of the broker-dealer exclusion of the Advisers Act. Specifically, the final interpretation states that a broker-dealer’s advice as to the value and characteristics of securities or as to the advisability of transacting and securities falls within the “solely incidental” prong of this exclusion if the advice is provided in connection with, and is reasonably related to, the broker-dealer’s primary business of effecting securities transactions.

[This is the opening big enough to drive not just a truck through but a battleship. When you look at the ads of the major wirehouses, ask yourself if they sound like something “solely incidental” to the “business of effecting securities transactions” or comprehensive planning advice:

Merrill Lynch: It all starts with you. Your life. Your priorities. Our advice and guidance.

Morgan Stanley: Wealth Management. We help individuals reach their long-term financial goals.

Prudential: Whether you’re a DIYer or prefer a professional’s approach, our mutual funds, ETFs and personalized portfolios – delivered the way you want – can help you live the financial life you dream about. Your personalized investing solutions await.

Edward Jones: Before we can develop an investment strategy for you, we get to know you. Why are you investing? What do you want to do? This is your financial future. It shouldn’t be left to chance or some off-the-shelf plan.

Please understand, I believe these are all commendable services; however, they are not brokerage services, they are investment advisory services and should be subject to a fiduciary duty.]

“An investment advisor owes a fiduciary duty to its clients under the Advisers Act a duty that is established by an enforceable through the Advisers Act. This duty is principles-based and applies to the entire relationship between an investment advisor and its client.”

[Yep, I agree, and it should apply to ALL firms who provide investment advice.]

Reg B ban on sales contest

“… Would not prevent a BD from offering only proprietary products, placing material limitations on the menu of products or incentivizing the sale of such products through its compensation practices, so long as the incentive is not based on the sale of specific securities or types of securities within a limited period of time.”

[Wow, that really is going to protect the public.]

Standard of Conduct

If you are a broker-dealer that provides recommendations subject to regulation best interest, include [emphasis required]: “When we provide you with a recommendation, we have to act in your best interest and not put our interests ahead of yours. At the same time, the way we make money creates some conflicts with your interest.

“If you are an investment advisor, include [emphasis required]: “When we act as your investment advisor, we have to act in your best interest and not put our interest ahead of yours. At the same time, the way we make money creates some conflicts with your interest.

[Okay, can anyone really argue that this distinction is “reasonable”? Can you figure out the difference between a broker-dealer and an investment advisor? To me, they sound like two peas in a pod, both swimming in a sea of similar conflicts. Horsepucky!]

Don’t forget to ask whoever you’re getting advice from to sign the Oath.

http://www.thefiduciarystandard.org/wp-content/uploads/2015/02/fiduciaryoath_individual.pdf

https://www.sec.gov/rules/final/2019/34-86032.pdf [the full report, all 564 pages]

Hope you enjoyed this issue, and I look forward to “seeing you” again.

Harold Evensky

Chairman

Evensky & Katz / Foldes Financial Wealth Management

IMPORTANT DISCLOSURE

PLEASE REMEMBER THAT PAST PERFORMANCE MAY NOT BE INDICATIVE OF FUTURE RESULTS. DIFFERENT TYPES OF INVESTMENTS INVOLVE VARYING DEGREES OF RISK, AND THERE CAN BE NO ASSURANCE THAT THE FUTURE PERFORMANCE OF ANY SPECIFIC INVESTMENT, INVESTMENT STRATEGY, OR PRODUCT (INCLUDING THE INVESTMENTS AND/OR INVESTMENT STRATEGIES RECOMMENDED OR UNDERTAKEN BY EVENSKY & KATZ / FOLDES FINANCIAL WEALTH MANAGEMENT (“EK-FF”), OR ANY NON-INVESTMENT-RELATED CONTENT, MADE REFERENCE TO DIRECTLY OR INDIRECTLY IN THIS NEWSLETTER WILL BE PROFITABLE, EQUAL ANY CORRESPONDING INDICATED HISTORICAL PERFORMANCE LEVEL(S), BE SUITABLE FOR YOUR PORTFOLIO OR INDIVIDUAL SITUATION, OR PROVE SUCCESSFUL. DUE TO VARIOUS FACTORS, INCLUDING CHANGING MARKET CONDITIONS AND/OR APPLICABLE LAWS, THE CONTENT MAY NO LONGER BE REFLECTIVE OF CURRENT OPINIONS OR POSITIONS. MOREOVER, YOU SHOULD NOT ASSUME THAT ANY DISCUSSION OR INFORMATION CONTAINED IN THIS NEWSLETTER SERVES AS THE RECEIPT OF, OR AS A SUBSTITUTE FOR, PERSONALIZED INVESTMENT ADVICE FROM EK-FF. TO THE EXTENT THAT A READER HAS ANY QUESTIONS REGARDING THE APPLICABILITY OF ANY SPECIFIC ISSUE DISCUSSED ABOVE TO HIS/HER INDIVIDUAL SITUATION, HE/SHE IS ENCOURAGED TO CONSULT WITH THE PROFESSIONAL ADVISOR OF HIS/HER CHOOSING. EK-FF IS NEITHER A LAW FIRM, NOR A CERTIFIED PUBLIC ACCOUNTING FIRM, AND NO PORTION OF THE NEWSLETTER CONTENT SHOULD BE CONSTRUED AS LEGAL OR ACCOUNTING ADVICE. A COPY OF EK-FF’S CURRENT WRITTEN DISCLOSURE BROCHURE DISCUSSING OUR ADVISORY SERVICES AND FEES IS AVAILABLE UPON REQUEST. PLEASE NOTE: IF YOU ARE AN EK-FF CLIENT, PLEASE REMEMBER TO CONTACT EK-FF, IN WRITING, IF THERE ARE ANY CHANGES IN YOUR PERSONAL/FINANCIAL SITUATION OR INVESTMENT OBJECTIVES FOR THE PURPOSE OF REVIEWING/EVALUATING/REVISING OUR PREVIOUS RECOMMENDATIONS AND/OR SERVICES, OR IF YOU WOULD LIKE TO IMPOSE, ADD, OR TO MODIFY ANY REASONABLE RESTRICTIONS TO OUR INVESTMENT ADVISORY SERVICES. EK-FF SHALL CONTINUE TO RELY ON THE ACCURACY OF INFORMATION THAT YOU HAVE PROVIDED.

© Evensky & Katz / Foldes Financial Wealth Management

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits