Macrogram - November 2019

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsMacrogram is a chart-based newsletter, designed to provide macroeconomic insights at-a-glance.

Fed Watch

Fed Meeting October 29-30, 2019 - The Fed cut the target range for the federal funds rate by 0.25% to 1.50 - 1.75%. Fed Chair Powell expected the Fed's current policy stance 'likely to remain appropriate' amid the Fed's expectations of a sustained expansion of economic activity and inflation close to the Fed's symmetric 2 percent inflation objective. The market embraced Powell's message.

Interest Rates

10-year vs. 3-month Treasury rate - Yield curve is no longer inverted. An inverted yield curve has historically been a precursor of recessions.

Economic Activity Indicators

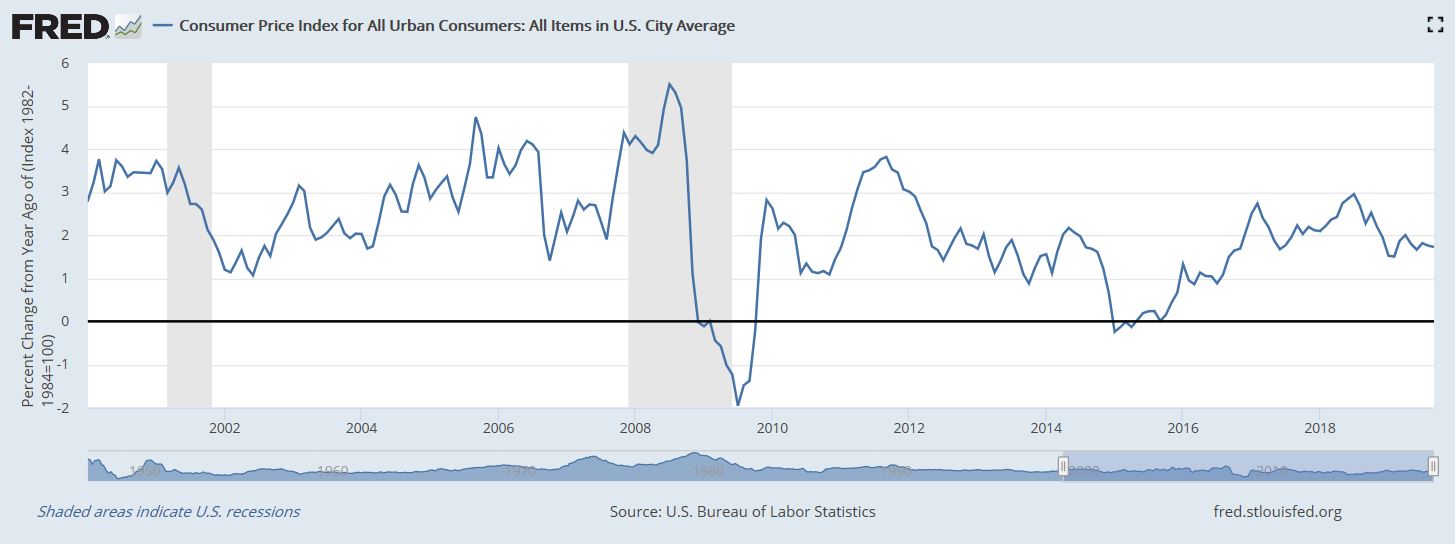

Consumer Price Index - Inflation is close to the Fed's symmetric 2 percent target rate.

Unemployment Rate - Stands at 3.6% in October, up 0.1%, just off September's 50-year low.

Initial Jobless Claims - Made a bottom in April 2019; very low initial jobless claims numbers ever since are evidence of a strong labor market.

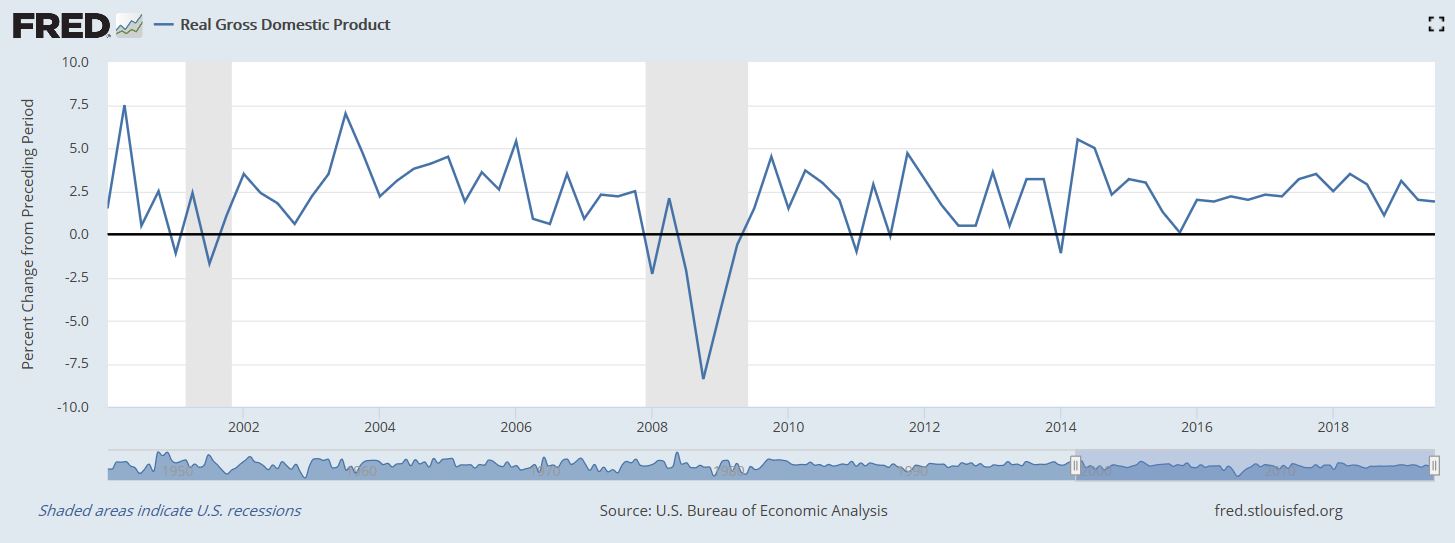

Real Gross Domestic Product - Shows a steady, albeit modest year-over-year growth rate. Clouds on the horizon: Low U.S. GDP growth forecast for Q4/2019.

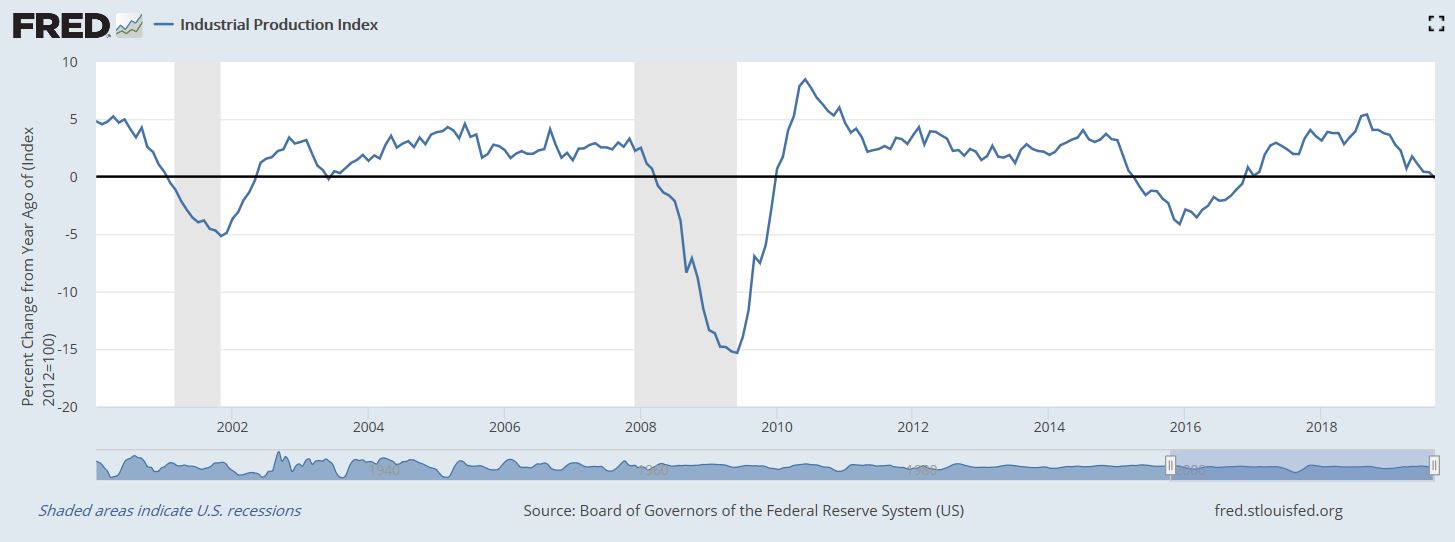

Industrial Production - Year-over-year levels show weakness. The Institute for Supply Management's (ISM's) purchasing managers index, which is widely regarded as a key U.S. manufacturing gauge, has been in contraction territory since August.

Real Household Income - Reaching for new highs. Household spending may continue to rise at a strong pace.

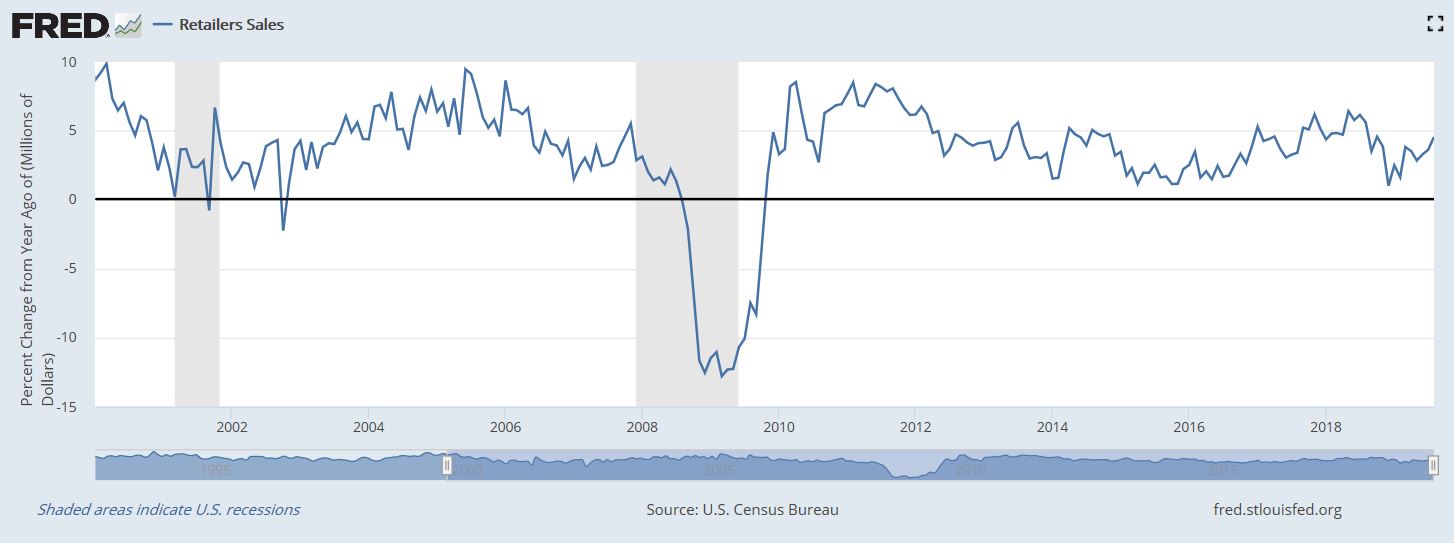

Retail Sales - Growing at a decent clip and being a main driver for the continued GDP growth in the U.S.

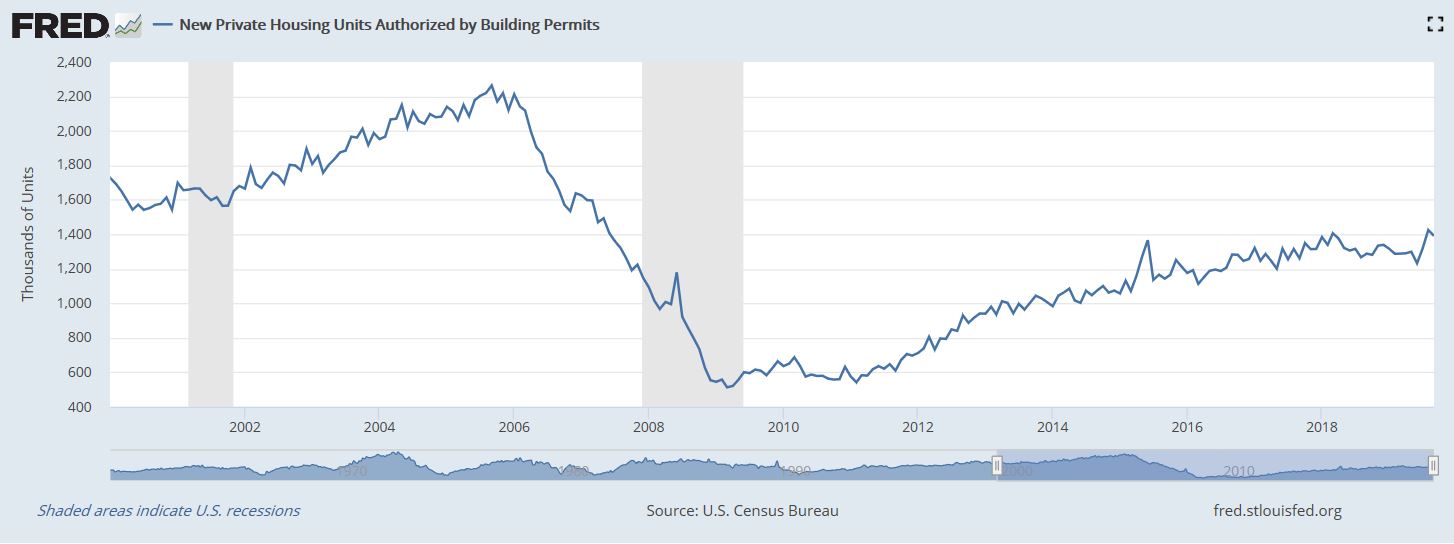

New Building Permits - Show a rebound in the housing market in response to lower interest rates.

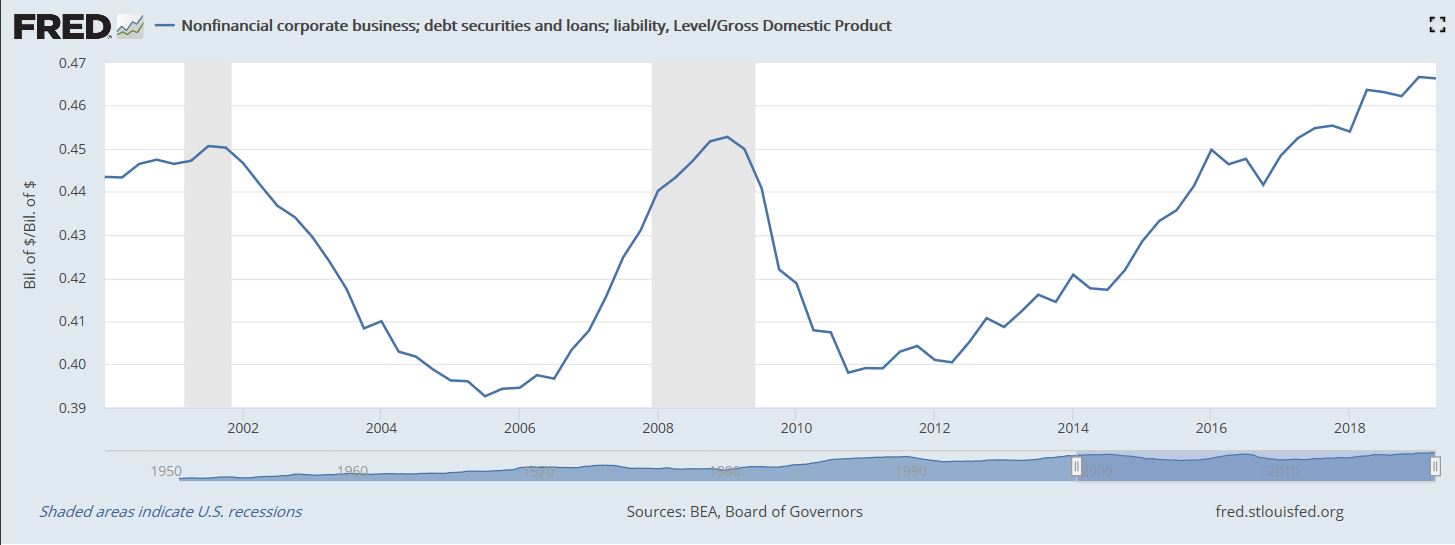

Corporate Debt/GDP Ratio - Remains at near record highs. Large percentage of leveraged loans and 'barely investment grade' debt securities give cause for concern.

Recession Watch

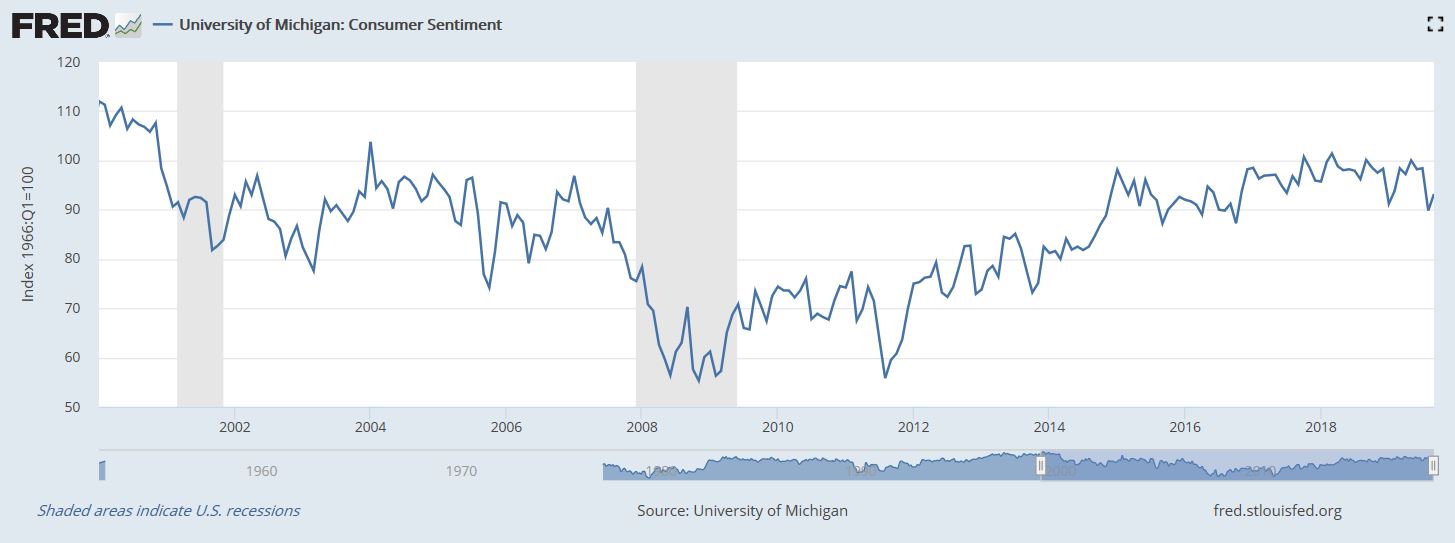

University of Michigan: Consumer Sentiment - Rises again in October amid expectations for improving incomes and lower inflation (FRED's database not yet updated as of November 1).

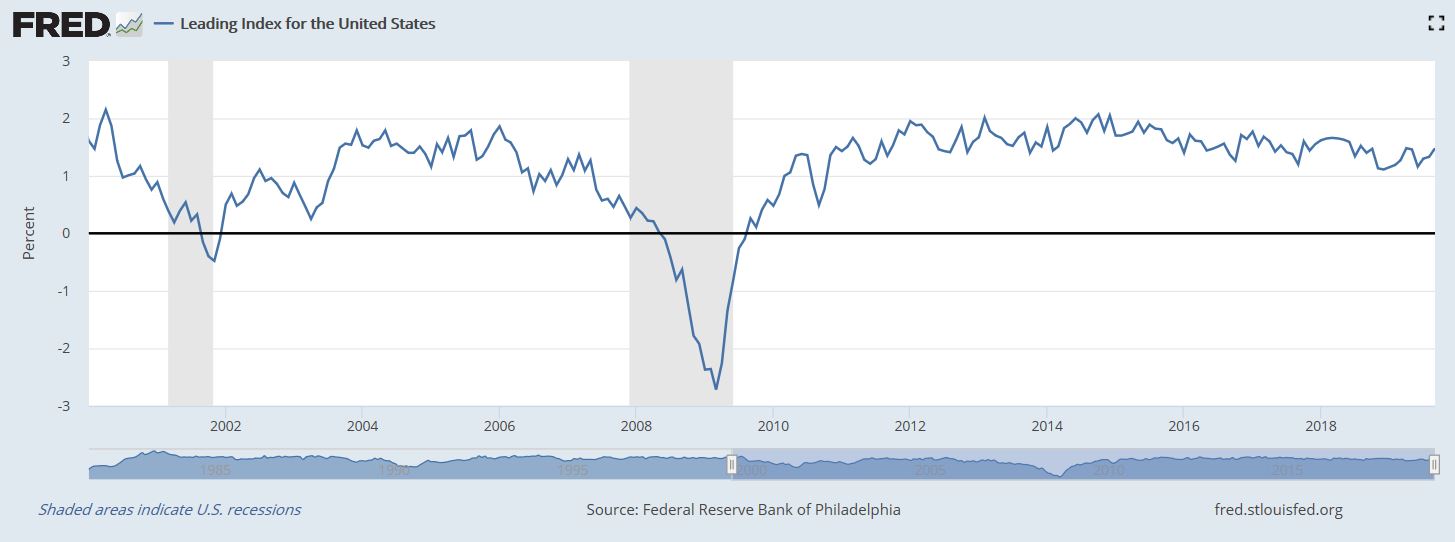

Federal Reserve Bank of Philadelphia Leading Index - Does not point to a contraction.

St. Louis Fed Financial Stress Index - Levels are not elevated.

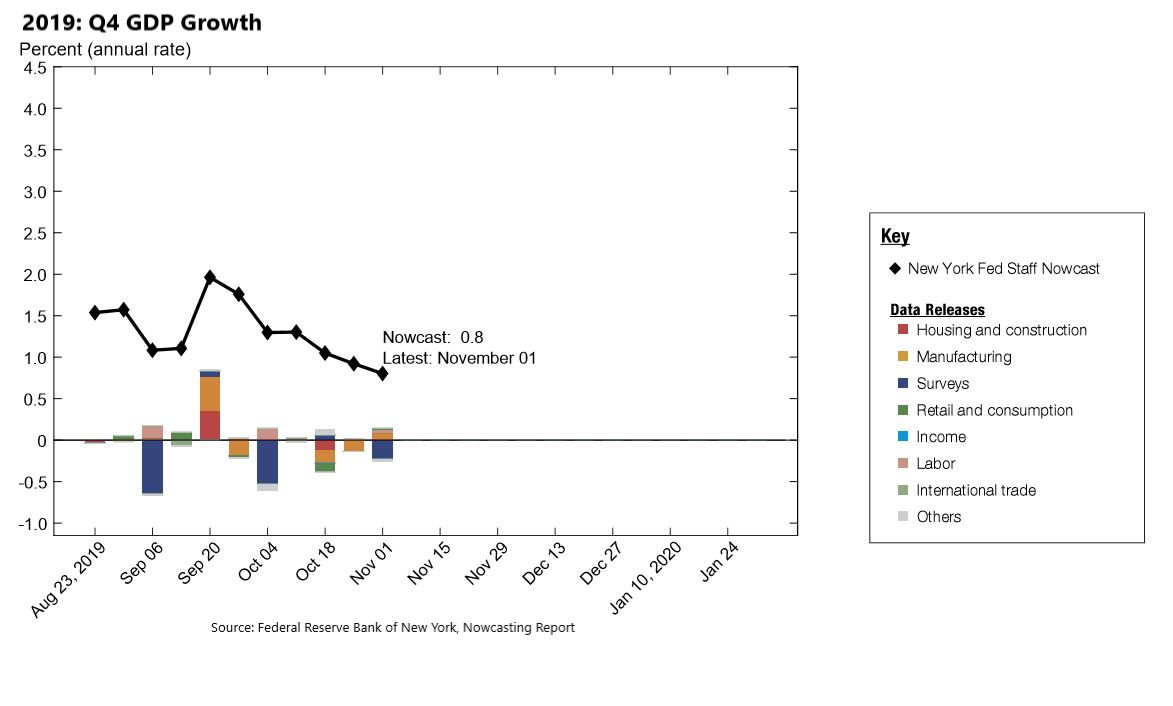

New York Fed - Forecast of Q4/2019 GDP shows anemic growth of the U.S. economy.

Maycrest Capital's Perspective

- The economic activity indicators continue to present a mixed picture. While manufacturing and business investment remain weak, consumer spending has remained firm, and employment indicators point to a strong labor market.

- The global GDP growth predictions for 2020 are at 3% based on a recent report by the Organisation for Economic Cooperation and Development. Trade tensions, the drawn-out trade war between the U.S. and China, and the fallout of Brexit continue to affect the global growth rate.

- Slow inflation and sluggish growth in the Eurozone have prompted the European Central Bank in September to cut interest rates to a negative 0.50%. The U.S. fed funds rate was also lowered in September and October by a Fed determined to extend the U.S. expansion.

- The yield curve 'un-inverted' in October. A yield curve inversion is often associated with a looming recession; however, the interest rate picture may be distorted by the unprecedented amount of negative-yielding debt in parts of the world, which entice investors to purchase long-term U.S. treasuries in search of safety and yield.

As of October 31, 2019, our BearCasting® model indicates that Maycrest Capital's equity strategy should remain invested in the U.S. stock market. Maycrest Capital invests in the U.S. stock market following its long-bias tactical equity strategy. Investment decisions are based on signals provided by our proprietary BearCasting® model, which incorporates economic, sentiment, and technical indicators.

This issue of Macrogram has been edited by Maria Davis. Please send any feedback to [email protected].

www.maycrestcapital.com

Disclosures

This is Maycrest Capital’s current assessment of the economy and the market and may be changed without notice. The visuals shown are for illustrative purposes only and do not guarantee success or a certain level of performance. This material contains projections, forecasts, estimates, beliefs and similar information (“forward looking information”). Forward looking information is subject to inherent uncertainties and qualifications and is based on numerous assumptions in each case, whether or not identified herein. This information may be taken, in part, from external sources. We believe these external sources to be reliable, but no warranty is made as to accuracy. This material is not financial advice or an offer to sell any product.

Maycrest Capital’s investment strategy may not be suitable for all investors. Before investing, consider your investment objectives and Maycrest Capital’s charges and expenses. All investment strategies have the potential for profit or loss. There is no guarantee that our investment strategy will perform as designed or that the strategy will be profitable. Investors should expect unprofitable periods. Past performance is not indicative of future performance. Maycrest Capital is a registered investment adviser. Registration does not imply a certain level of skill or training. Maycrest Capital may only conduct business in states where it is properly registered to do so. More information about Maycrest Capital including its advisory services and fee schedule can be found in Form ADV Part 2, which is available upon request.

All FRED graphs have been retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org. The Nowcasting Report has been retrieved from the Federal Reserve Bank of New York. The following data series have been used in this issue of Macrogram: Board of Governors of the Federal Reserve System (US), 10-Year Treasury Constant Maturity Rate [DGS10] Federal Reserve Bank of St. Louis, 10-Year Treasury Constant Maturity Minus 3-Month Treasury Constant Maturity [T10Y3M] U.S. Bureau of Labor Statistics, Consumer Price Index for All Urban Consumers: All Items [CPIAUCSL] U.S. Bureau of Labor Statistics, Civilian Unemployment Rate [UNRATE] U.S. Employment and Training Administration, 4-Week Moving Average of Initial Claims [IC4WSA] U.S. Bureau of Economic Analysis, Real Gross Domestic Product [A191RL1Q225SBEA] Board of Governors of the Federal Reserve System (US), Industrial Production Index [INDPRO] U.S. Bureau of Labor Statistics, Employed full time: Median usual weekly real earnings: Wage and salary workers: 16 years and over [LES1252881600Q] U.S. Census Bureau, Retailers Sales [RETAILSMSA] U.S. Census Bureau and U.S. Department of Housing and Urban Development, New Private Housing Units Authorized by Building Permits [PERMIT] Board of Governors of the Federal Reserve System (US), Nonfinancial corporate business; debt securities and loans; liability, Level [BCNSDODNS] University of Michigan, University of Michigan: Consumer Sentiment [UMCSENT] Federal Reserve Bank of Philadelphia, Leading Index for the United States [USSLIND] Federal Reserve Bank of St. Louis, St. Louis Fed Financial Stress Index [STLFSI] Federal Reserve Bank of New York, Nowcasting Report; https://www.newyorkfed.org/research/policy/nowcast.html.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits