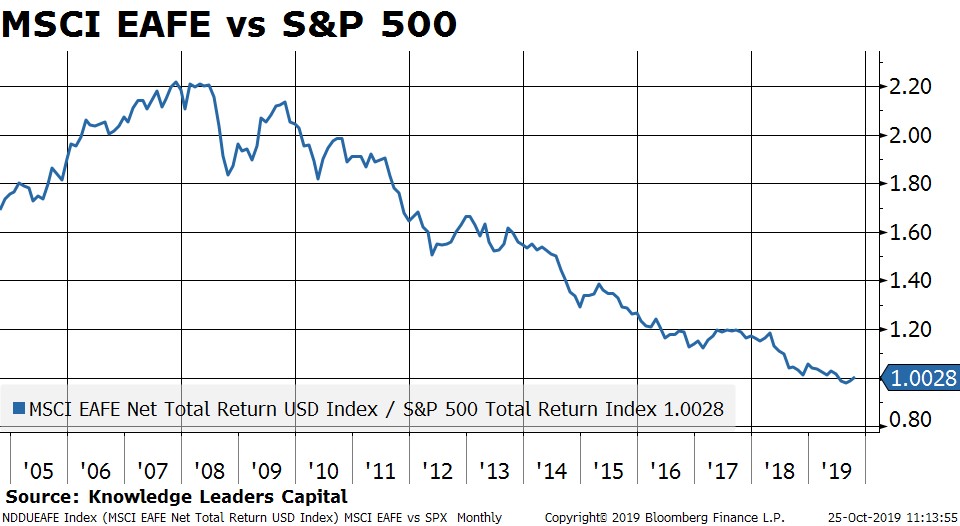

I wrote a week ago about how international equities may be finally getting the help they need to break the back of a long-term underperformance trend. It’s a trend that has caused international stocks to underperform US stocks in eight of the last eleven years. But now we have valuations and other fundamentals in the most supportive position since 2000 as well as “Not QE” that will bring up the level of bank reserves. Our work suggests that embracing those factors, and international stocks in general, would be beneficial to one’s performance. And yet, US investors are aggressively overweight US stocks and aggressively underweight international stocks. This fact would leave most portfolios in a disadvantaged position if international stocks do begin to outperform in a serious way.

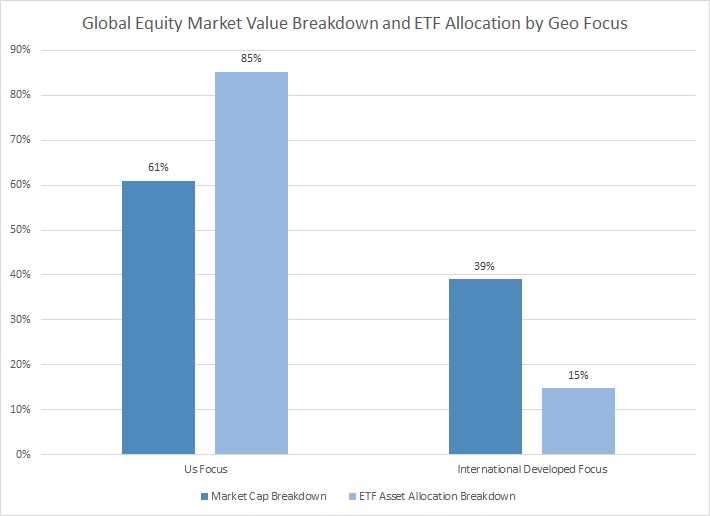

In the second chart below we highlight just how overweight the investing public is of US stocks and underweight they are of foreign stocks. The dark blue line shows the market capitalization breakdown of mid/large cap US and developed market foreign equities. Right now, the US accounts for about 61% of world equity market capitalization and foreign stocks account for the remaining 39%. However, when we add up the assets under management of US traded ETFs that have a US geographical focus we notice that those ETFs account for 85% of all mid/large cap equity ETF assets. US traded ETFs with a foreign developed market geo focus account for the remaining 15% of assets. That is to say, US investors have a US allocation that is roughly 140% above benchmark and a foreign allocation that is roughly 60% below benchamrk.

Maybe this doesn’t seem like a big deal since everyone KNOWS that US stocks ALWAYS outperform. At least, this is what US investors have been conditioned to think after such a long and healthy period of US equity dominance. But what if that isn’t true anymore? Recall that from 2002-2007 the MSCI EAFE outperformed the S&P 500 by about 50%, or 7% annualized.