When it comes to interest rates, most investors think about bonds. But interest rates also play a large role in how investors value stocks, as well as affect the relative performance of equity sectors.

For certain sectors, a change in interest rates has a relatively large impact—and that impact has increased significantly in the “new normal” environment of low interest rates. With the sharp fall in interest rates over the past year, some of these sectors saw outsize differences in performance relative to the broader market.

The lowdown on rate-sensitive sectors

Let’s first talk about that group of interest-rate-sensitive sectors. The lineup includes a few of the traditional defensive sectors, such as Utilities, Consumer Staples and Health Care. Some pro-cyclical sectors, like Real Estate and Financials, also make the list.

For stocks, there is no simple equation that can measure the likely change in price for a given change in interest rates—many factors affect stocks’ sensitivity to rates, and that sensitivity can change over time. But we can run a regression analysis and get a pretty good idea how sectors have been affected over various time periods. Some of those factors for equity sectors include their dividend yield, debt ratios, and/or how their core operations are directly affected by interest rates.

-

Financials: The Financials sector typically is highly sensitive to interest rates, as interest rates are often core to their operations. Higher interest rates usually translate into higher net interest margin—that is, the difference between the rate banks pay out on deposits and the rate they receive on loans. When the economy is bustling, interest rates usually rise at the same time loan demand is high. Because of this, there is typically a positive relationship between interest rates and relative performance of Financials compared with the broader stock market.

-

Utilities, Consumer Staples and Health Care: High-dividend-paying sectors tend to perform well as investors seek their comparatively higher dividend yield during periods when interest rates are low. Also, those sectors that are capital-intensive and carry a high level of debt, such as the traditionally defensive Utilities, Consumer Staples and Health Care, benefit from lower borrowing costs as interest rates decline.

-

Real Estate: Real Estate Investment Trusts (REITs), which make up the bulk of the Real Estate sector, are somewhat of a hybrid. REITs benefit from a growing economy, as property values, occupancy rates, and rental income all tend to rise in the good times. However, interest rates also tend to rise at the same time. Because REITs are big borrowers (in order to fund property purchases) and high-yielding (because they must pay out at least 90% of their taxable income to shareholders as dividends), higher interest rates exert downward pressure on relative performance. Typically, REITs exhibit an inverse relationship to interest rates, but there are times when the strength or weakness in the real estate market is dominant enough to offset the impact of interest rates.

What does it mean?

Having given a primer on interest-rate-sensitive sectors, let’s dive into what this all means in the current environment and how it might affect your portfolio.

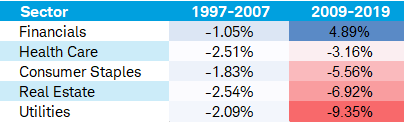

First, all the relationships that we describe above have been significantly magnified in the last 10 years, so understanding interest rate sensitivity is even more important today than at any time since 1989, when sector category data became available. The table below shows the beta, or sensitivity, of the sectors’ relative performance to a change in interest rates. A larger number, whether negative or positive, means there historically has been a bigger relative performance difference on average. In the 1997-2007 column, for example, a one percentage point rise in the 10-year Treasury yield resulted in the Utilities sector underperforming the broad market by 2.09%... and 9.35% in underperformance in the 2009-2019 period.

Sector beta to 10-year Treasury yield

Sector beta measures the percent change in sector performance relative to the S&P 500 index per a one-percentage-point change in the 10-year Treasury yield. Source: Schwab Center for Financial Research (SCFR), Bloomberg, weekly data as of 10/21/2019.

There are several hypotheses for the increase in sensitivity. For Financials, the decline that has occurred in short-term interest rates since 2009 has moved them closer to zero, limiting how much lower deposit rates can go at this point. At the same time, regulatory changes that have taken place since the 2007-2008 financial crisis have limited other sources of income, such as proprietary trading. So changes in net interest income now have a greater impact on banks’ revenues.

For the other sectors, low interest rates have increased investors’ tendency to reach for yield—that is, there’s greater demand for higher-paying securities. And as interest rates go lower, investment prices become increasingly sensitive to cash flows further and further into the future (in the bond market, this is commonly referred to as “convexity.”) Finally, if businesses respond to lower interest rates by taking on much higher debt levels, changes in interest rates will have a bigger impact on companies’ ability to refinance and service their debt.

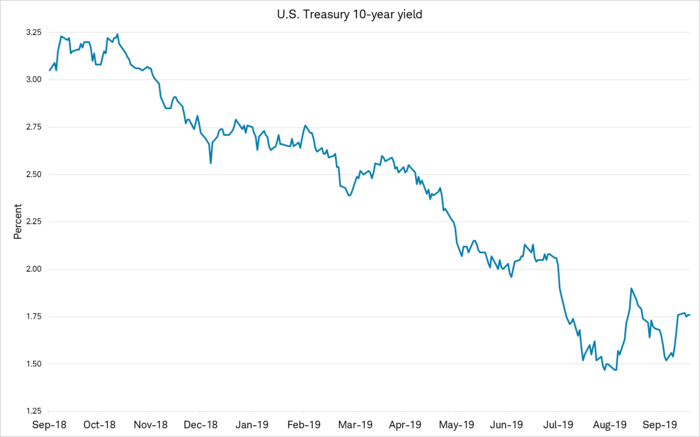

The U.S.-China trade war, uncertainty about how and when the UK will exit the EU (Brexit), Hong Kong protests and strife in the Middle East all have weighed on an already slowing global economy. The U.S. economy is not immune. The Federal Reserve cut interest rates twice in the third quarter as insurance against rising global risks, contributing to the sharp drop in the 10-year Treasury yield, to as low as 1.46% recently from more than 3% a year ago.

The yield on the 10-year Treasury bond has declined over the past year

Source: Charles Schwab, Macrobond, Federal Reserve, as of 10/21/2019.

Past performance is no guarantee of future results

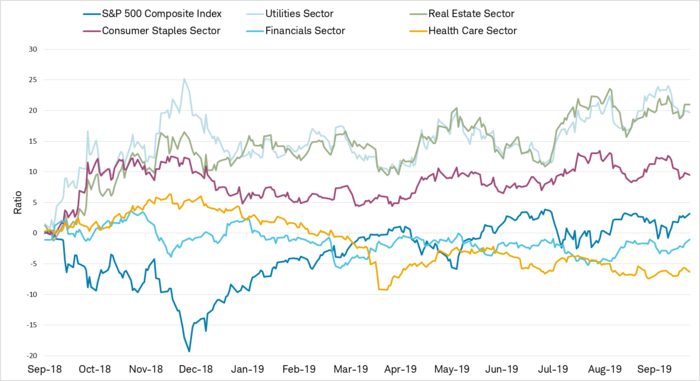

Amid this decline, we saw a big divergence in relative performance among the sectors—it has been very positive for Utilities, Consumer Staples and Real Estate, and negative for Financials. The Health Care sector has had some unique factors that have overwhelmed the interest-rate impact, which we’ll touch on later.

Utilities, Consumer Staples and Real Estate have outperformed the broader index

Ratio reflects the relative performance of each sector compared with the performance of the S&P 500® Composite Index. Sectors are represented by S&P 500 sector indices. Source: Charles Schwab, S&P Dow Jones Indices, as of 10/21/2019. Past performance is no guarantee of future results.

Where do we go from here?

The path of the economy, interest rates and overall stock market is highly uncertain … or, we should say, even more highly uncertain than usual. If the Fed’s rate cuts are not enough to stimulate economic growth, or additional geopolitical shocks tip the U.S. into recession, interest rates could close the gap with international rates, many of which are currently below zero percent. While we don’t foresee the Fed’s benchmark short-term rate, the federal funds rate, turning negative, it is currently at 1.75%, meaning it can fall another 175 basis points before reaching zero. This would argue for continued potential outperformance of those sectors with a negative relationship to interest rates (Utilities, Consumer Staples and Health Care). If the real-estate market were to dive along with the economy, it could overwhelm the interest-rate tailwind for REITs, which means the Real Estate sector potentially could underperform along with Financials.

Conversely, if we see some stabilization in the economy and continued easing in uncertainty that we’ve seen in the last couple of weeks, then rates could easily rise further. As we discussed in our previous Sector Views article, valuations in the Utilities sector in particular are very high. This opens up the risk of a sharp reversal of the strong relative performance over the past year.

Health Care may be the exception. As you can see in the chart above, it lagged the overall market and the other defensive rate-sensitive sectors, due in part to rising regulatory risk amid a presidential election filled with candidates talking about health-care system reform. However, based on current valuations, which are not far from their 20-year average, and solid fundamentals, we think the Health Care sector could outperform in the coming months. We have a marketperform rating on the other sectors mentioned above—Utilities, Consumer Staples, Financials and Real Estate—based on the highly uncertain environment for the overall market and interest rates.

A final word

Keep in mind, no matter what our view is on any of the sectors, remaining diversified is very important. Concentrating on too few sectors can dramatically affect the risk profile and performance of your portfolio. So if you do make any sector tilts in your portfolio, keeping them small is a good way to maintain appropriate diversification.

Source: Schwab Center for Financial Research, FactSet (for YTD total returns) and S&P Dow Jones Indices (for S&P 500 sector weightings). Sector performance data is based on total return for each S&P 500 sector subindex (see “Important Disclosures” for index definitions). Sector weighting data is as of 09/30/2019; data is rounded to the nearest tenth of a percent, so the aggregate weights for the index may not equal 100%.

Past performance is no guarantee of future results.

What do the ratings mean?

The sectors we analyze are from the widely recognized Global Industry Classification Standard (GICS®) groupings. After a review of risks and opportunities, we give each stock sector one of the following ratings:

- Outperform: likely to perform better than the broader stock market*

- Underperform: likely to perform worse than the broader stock market

- Marketperform: likely to track the broader stock market

*As represented by the S&P 500 index

Important Disclosures

Schwab Sector Views do not represent a personalized recommendation of a particular investment strategy to you. You should not buy or sell an investment without first considering whether it is appropriate for you and your portfolio. Additionally, you should review and consider any recent market news. Supporting documentation for any claims or statistical information is available upon request.

All expressions of opinion are subject to change without notice in reaction to shifting market or other conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Diversification and rebalancing strategies do not ensure a profit and do not protect against losses in declining markets. Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability.

In statistical modeling, regression analysis is a set of statistical processes for estimating the relationships between a dependent variable and one or more independent variables.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

International investments are subject to additional risks such as currency fluctuation, geopolitical risk and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

The Schwab Center for Financial Research (SCFR) is a division of Charles Schwab & Co., Inc.

© Charles Schwab & Co.

© Charles Schwab

More ETF Topics >