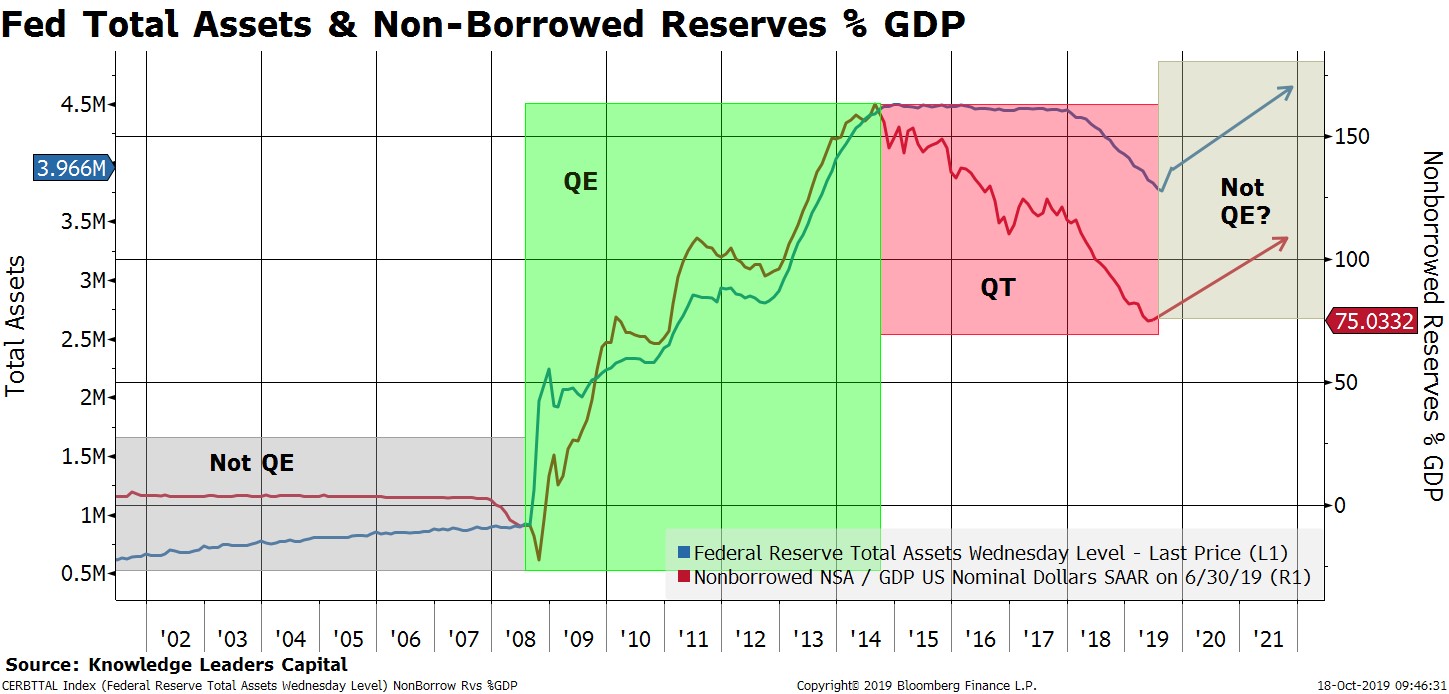

Last week the Federal Reserve announced the re-commencement of large scale asset purchases in order to alleviate funding pressures that had been bubbling for several months. Much effort has been made by Fed Chairman Powell and other missionaries to explain why this round of asset purchases, coming in at fully $60bn per month, is not the same thing as earlier rounds of quantitative easing. The two main talking points are that:

1) Bank reserves have shrunk to a level that is too low to facilitate a robust market of overnight borrowing and lending between banks.

and

2) The Fed will be buying bills, not bonds, and so these asset purchases are not as stimulative to the real economy as “QE” in that they will not pressure longer-term bond yields lower.

To these points, we would argue that:

1) Wasn’t the point of QE1 that bank reserves had shrunk to a too low level and it was causing interbank funding issues? In this respect, how is “Not QE” any different than QE1? QE1 originally consisted of $600bn in mortgage and treasury bond purchases. “Not QE” will consist of at least $360bn in bill purchases, but is open ended in nature.

and

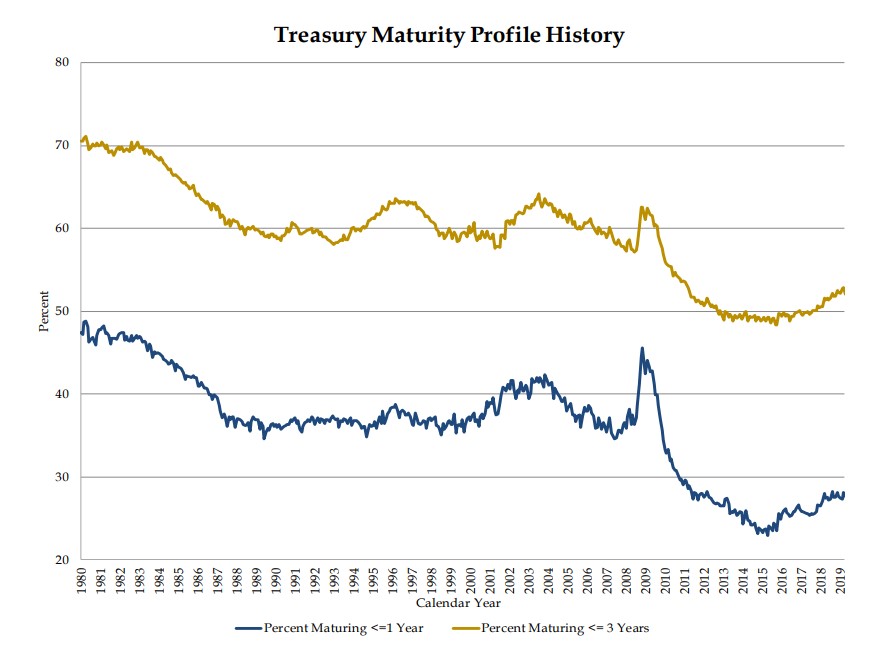

2) A main reason the Fed is buying bills and not bonds appears to be that, after a very long period of time in which bill issuance had waned as a percent of total debt issuance, bill issuance as a percent of total is now a decade high and rising.

With those simple rebuttals out of the way, we also ask ourselves whether it really matters what you call this current round of monetary support? After all, it’s not what you call it that matters for our purposes as investors, but rather the effect on asset prices. If “Not QE” acts to increase bank reserves – which appears to be the stated goal – then shouldn’t the asset price response be the same as in other periods in which bank reserves were increasing?

If so, then there is at least one big conclusion we can take from “Not QE”, which is that it could be supportive of cyclical stocks relative to all stocks. In the last chart below we simply plot the relative performance of cyclicals vs all stocks (blue line on the left axis) and overlay the 1-year difference in bank reserves held at the Federal Reserve (red line on the right axis). If “Not QE” makes the red line go strongly up and to the right, which it may, then so too could the relative performance of cyclical stocks…at least if the level of bank reserves is still a meaningful input for financial markets, which we believe would be a tough case to argue against.