United States and indeed global economic data have been weak – at least that is the unabated message from the PMI data that were released this week on both manufacturing and services. At this stage everyone knows the survey data, or “soft” data, are weak. The important question now is whether that weakness will spill over into hard economic data that admittedly comes with a lag. Indeed, for the Fed to take a much more aggressive stance they will need to see the soft data weakness bleed into the hard data.

In this respect tomorrow, Friday, October 4th, is shaping up to be one of the most important market days of the year as the September US employment report gets released. The US employment report is about as hard as the data come.

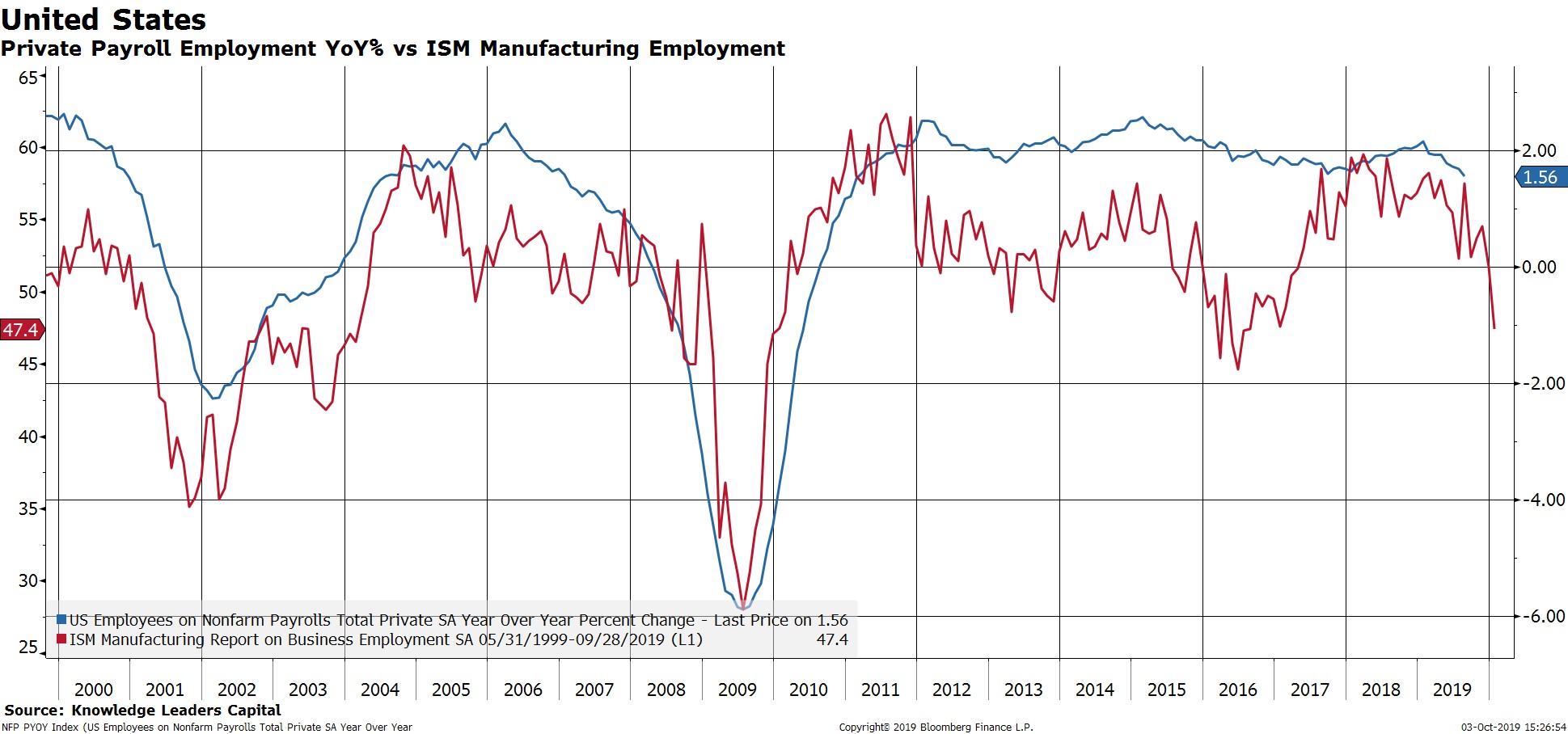

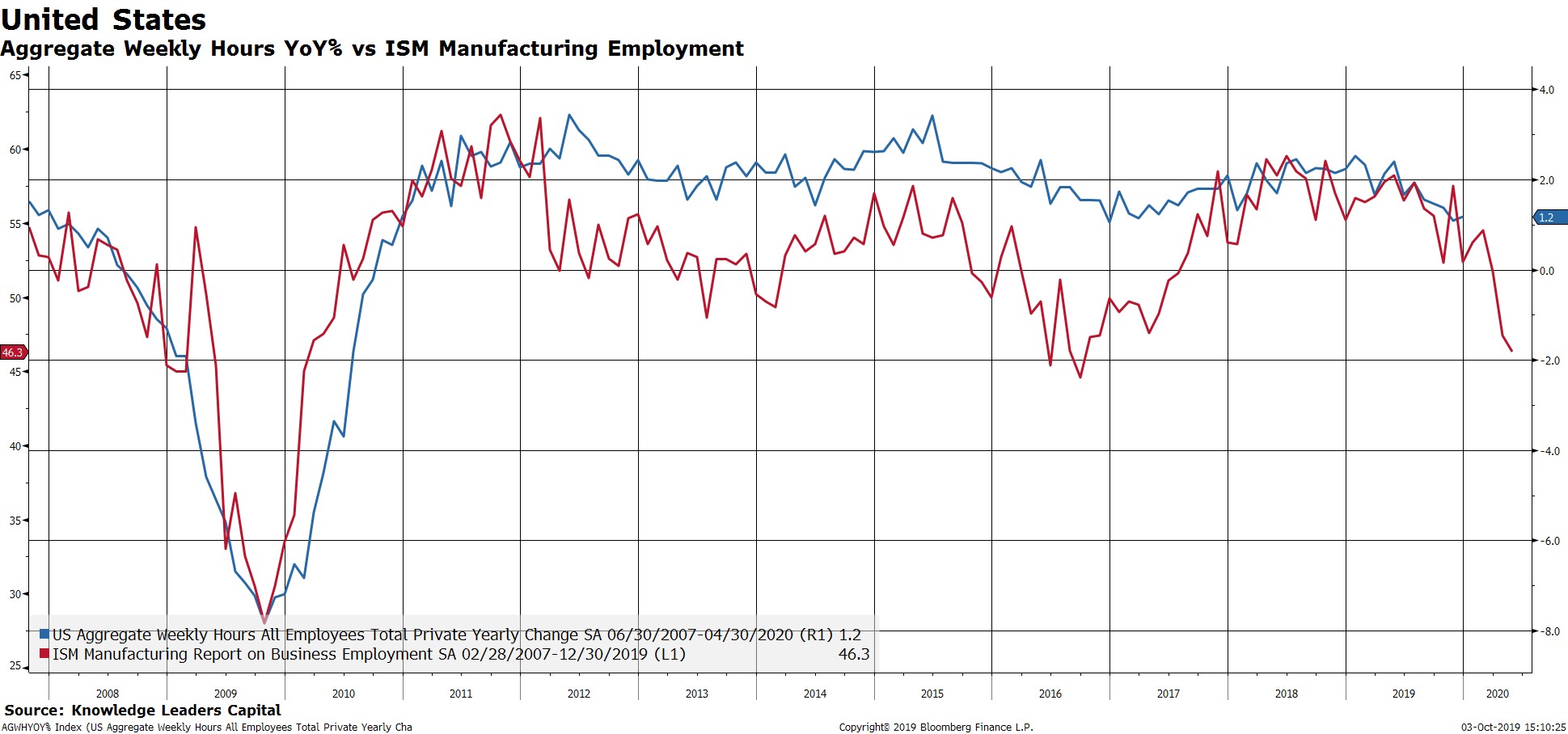

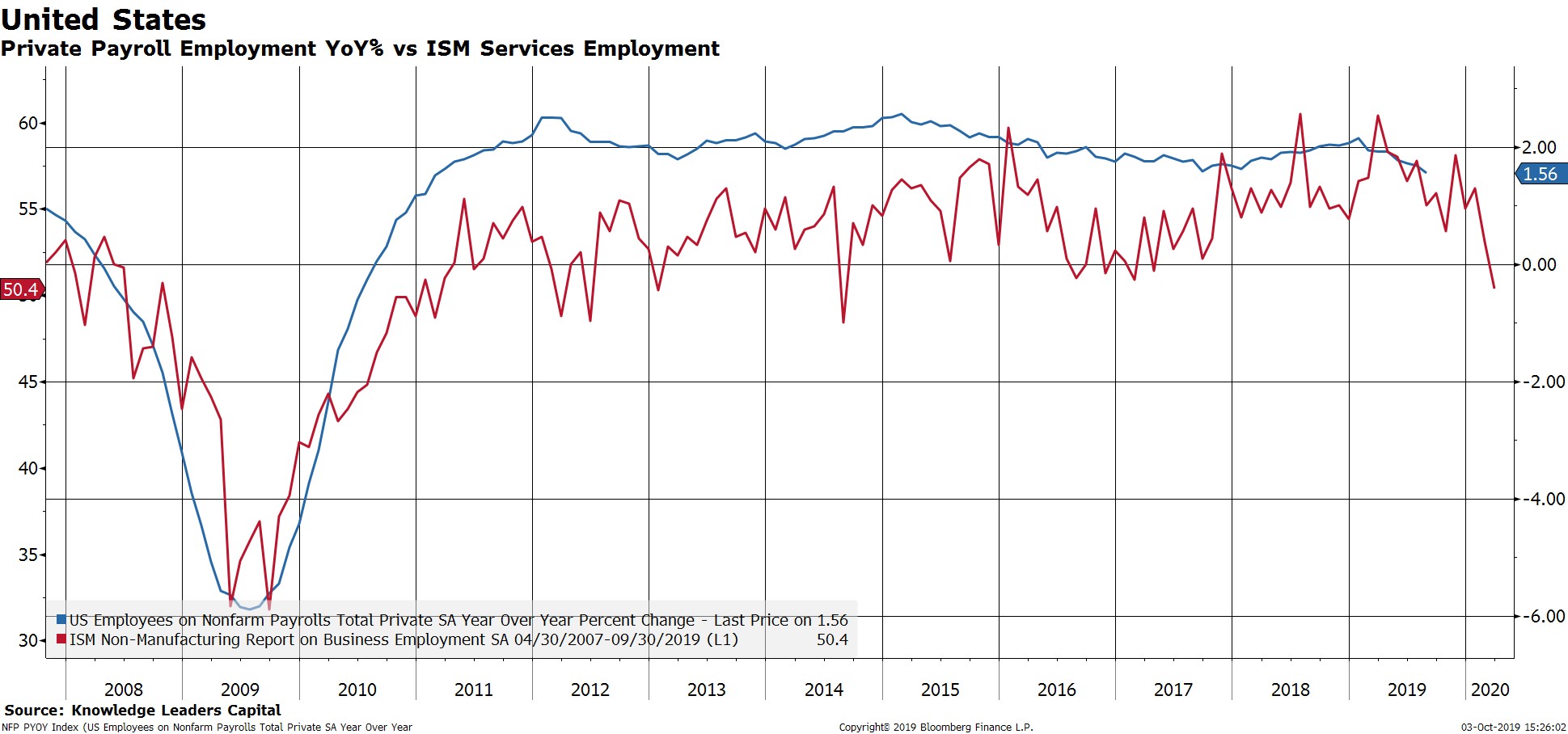

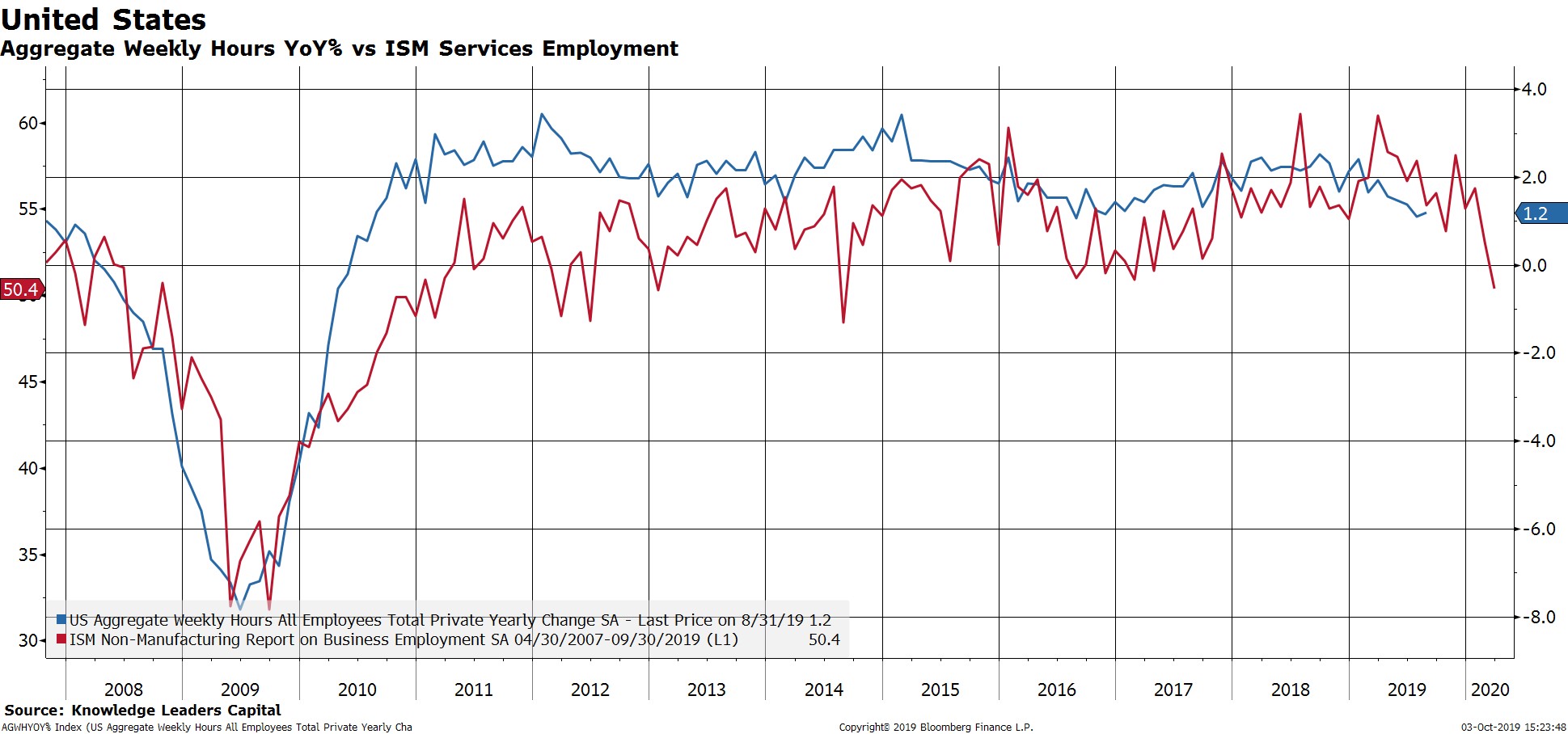

In our view, employment is challenged here and the onus is on the labor stats to pull a rabbit out of the hat. We now have leading data from both the manufacturing sector as well as the services sector that show employment in a declining trend. On the manufacturing side, the most recent ISM data showed the employment component to be in contraction with a reading of 46.3 (sub 50 readings indicate contraction). The same is almost true of the ISM services PMI, which has the employment component hanging on for dear life at just 50.4. In any case, both services and manufacturing employment surveys have turned sharply south since earlier in the year. This puts a great deal of pressure on the hard data to to show some serious resilience. We will shortly see if it is up to the challenge.

Below we show YoY payroll employment growth and YoY aggregate weekly hours growth compared to both the ISM manufacturing and services employment indices.