Emerging Markets Debt: A Case for Latin America

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsExecutive Summary

With $13 trillion of investment grade corporate and government bonds having negative yields, fixed income investors are increasingly looking at higher yielding emerging market debt.

Emerging market debt is one of the most diverse fixed income asset classes in the world with exposure to both US Dollar denominated and local currency bonds in Latin American, Asian, African and Middle Eastern economies. Latin America currently represents 33% of the total Dollar denominated debt in emerging markets. With many emerging market bonds still not included in major benchmark indices, active managers can gain an edge over their passive counterparts through security selection in their investment process.

In an ongoing effort to better understand the risks and complexities associated with emerging market investing, LM Capital has produced a three-part series to highlight the importance of regional specialization coupled with a risk minimization framework in emerging markets.

In this first part, we focus on the relatively high correlation across different regions within emerging markets and how the changing economic and demographic fundamentals make Latin America an attractive investment for the future.

Emerging market economies have evolved rapidly over the past two decades, especially in the Latin America region (LATAM). Emerging markets have decoupled from the economic cycles of developed economies and are able to withstand negative market events better than in the past. Across Latin America, the following factors are attractive for investments: improved economic fundamentals, an increasing pension industry, a young population with an expanding middle class, and cheap corporate valuations. Furthermore, a dovish Fed is putting less pressure on foreign corporations which are largely financed with US Dollars.

These trends in emerging market economies present a new opportunity for actively managed Emerging Market Debt (EMD). Although the performance of this asset class is highly correlated to systemic forces (e.g., strength of the USD/Euro/JPY, monetary policy in developed markets), the business cycles of specific EM economies have important idiosyncratic drivers. We believe risk minimization through security selection is a better approach to exploiting higher risk-adjusted returns as compared to regional diversification. At LM Capital, we attempt to identify investments that are decoupled from systematic drivers thereby harnessing diversification benefits from these idiosyncratic investments.

The Benefits of Regional Diversification Within EMD Are Largely Overstated

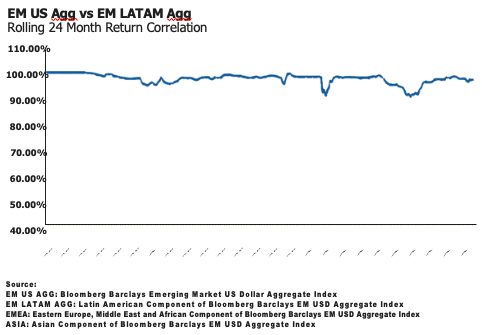

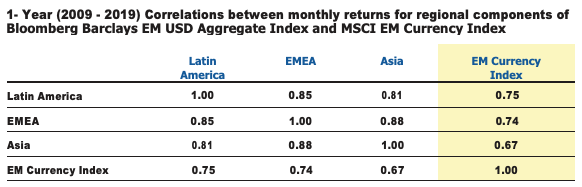

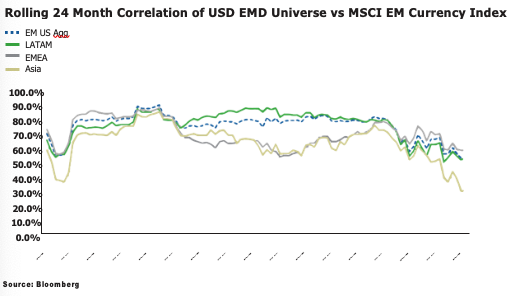

Given the inherent volatility of the EMD asset class, investors are inclined to diversify their EM exposure across geographic regions. However, we believe that in the EMD asset class, the benefits that accrue from regional diversification are largely overstated. In fact, the performance of US Dollar LATAM bonds and the broad US Dollar EMD universe are highly correlated.

The high correlation in performance is due to the fact that returns across EM regions are driven by many of the same underlying factors with US Dollar being the most prominent. The graph below shows the high correlation between the strength of the U.S. Dollar and the performance of each region in EM.

Rather than attempting to achieve diversification through regional allocations, an alternative approach is to work with an active manager who specializes in a geographic region within EM. This allows the manager to better understand the nuances of the region, better gauge specific country and company risk and therefore receive as much compensation for risk as possible while minimizing actual risk.

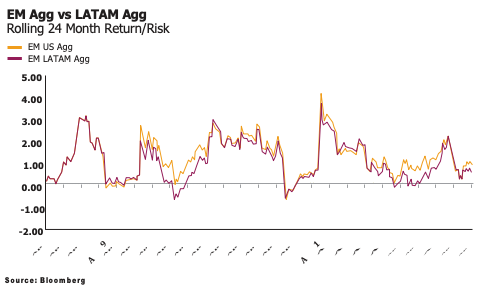

LATAM Debt, Strong Historical Performance

Latin American debt has been a strong performer over the past decade, paying higher yields than the broad EMD asset class. Latin American corporate bonds provide one of the most attractive options within emerging markets, offering particularly high yields.

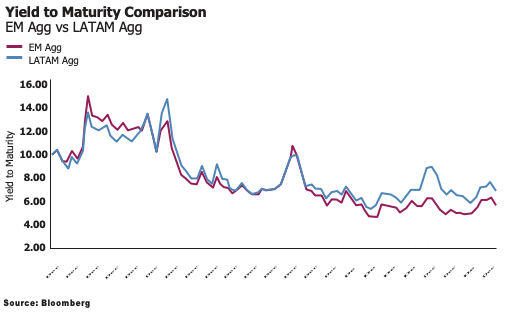

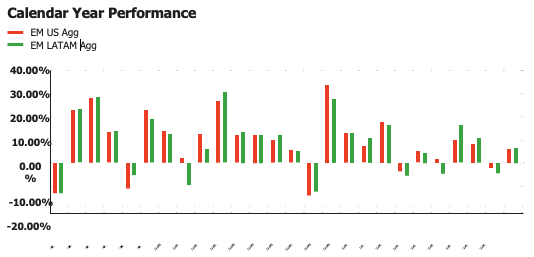

The graphs below show that in spite of the high volatility associated with Latin America, the region has consistently performed in sync with the broad EM Aggregate Index.

Source: Bloomberg

Over the last 25 years, performance for the LATAM component of Bloomberg Barclays USD EM Index has closely tracked the broad index except for three years. This can be attributed to the Argentinean default (2001), Latin American economic slowdown following Chinese slowdown (2015) and the currency crisis in Argentina caused by high inflation (2018).

Beyond its strong historical performance, the case for specialization in Latin American debt relies on economic, demographic and societal changes that bode well for the region’s future.

Turning from a historical perspective to a forward-looking analysis, we believe the region is displaying promising trends. We believe that (1) economic fundamentals are moving in a positive direction,

(2) demographic changes bode well for the region, (3) a growing pension fund industry should reduce volatility in the region’s debt markets and (4) corporations offer a particularly compelling story.

Economic Fundamentals

Stronger economic fundamentals are helping Latin America to move past its historical boom-and-bust cycle. Many Latin American countries have undergone budget and fiscal reforms, and are moving (albeit unevenly) towards fiscal responsibility. Central banks in Latin America have used inflation targeting to moderate swings in the current account and reduce the volatility of currency values and economic growth. The levels of foreign exchange reserves have increased, which helps to dampen risks in case of a financial crisis.2

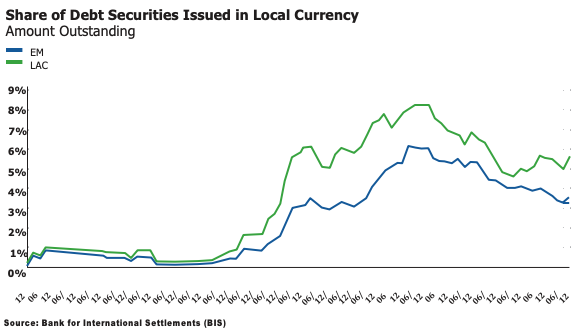

Changes in the pattern of borrowing have also helped to provide LATAM economies with additional resilience. A shift from short-term to longer-term funding has provided the region’s banking system with more stability. LATAM governments are also borrowing more in local currencies than in foreign currencies, making them less vulnerable to bank runs and currency crises. EM countries in general have seen an increase in the share of government debt denominated in local currency, yet Latin America has seen a particularly sharp increase. Peru, is a prime example. Foreign investors in Peru now hold about 40% of government debt in local currency.2

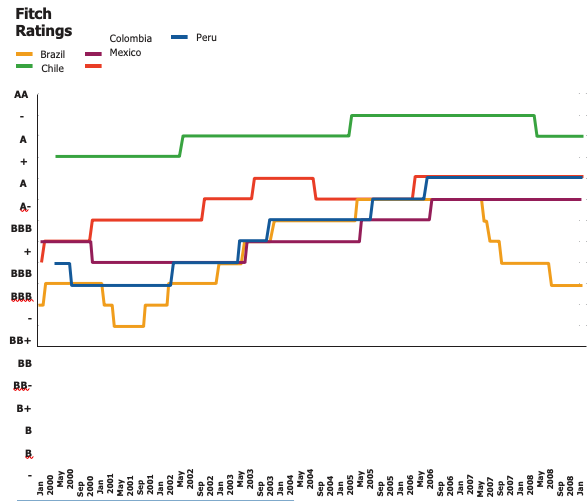

These improvements have generally been reflected in improved credit ratings. Since 2000, the sovereign credit ratings afforded by the three major credit rating agencies have been improving for four of the seven largest countries in the region: Mexico, Colombia, Peru, and Chile. Brazil’s credit rating had also been consistently improving until 2016 when internal political events interrupted stable economic policies geared to growth. These five countries accounted for over 65% of the debt issued (corporate and sovereign) by Latin America in 2018.

The graph below shows the history of sovereign credit rating provided by Fitch Ratings for these LATAM countries.

Source: Bloomberg

Demographic Change

The demographic changes that have been occurring in LATAM bode well for its future. Despite having a young population, the fertility rate has dropped to 2.1, which indicates that women are increasingly participating in the workforce. There is a growing middle class, and education rates are increasing (albeit from very low levels). The majority of progress has been seen in low- and middle-income households.4 We expect that these demographic changes will provide an internal driver of demand and are an engine for growth.

Improving fundamentals are one of the reasons why the currency crises in Argentina and Turkey in the summer of 2018 remained relatively contained and did not spread to other EM countries. We believe the poor performance of LATAM bonds in 2018 was not driven by any perceived weakness in Latin American markets as a whole, but rather due to US Dollar strength.

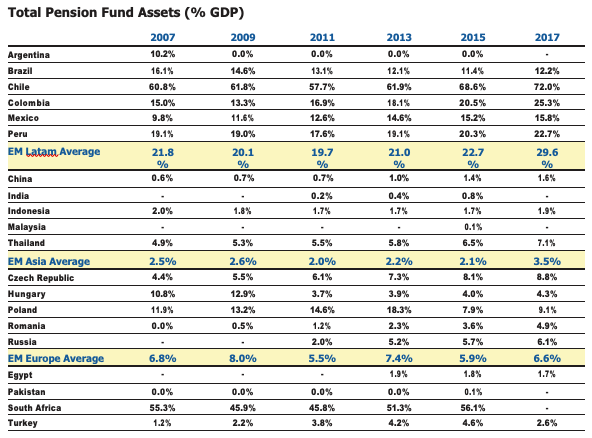

A Relatively Large Domestic Institutional Investor Base

A large domestic institutional investor base can reduce the risk of a major drawdown in the future. Local investors are less concerned about exchange rate volatility than foreign investors, making them less risk-averse, more financially resilient and more equipped to mitigate a run on a currency in turbulent times.

Latin America has one of the largest pension fund industries in EM when the size of the pension fund industry is viewed in the context of GDP. As of 2017, the highest pension fund assets in terms of GDP within EM is Chile at 72%, Columbia at 25.3%, Peru at 22.7%, Mexico at 16% and Brazil at 12%. With the pension reform bill clearing a major house hurdle, the share of pension assets in Brazil is expected to rise.7

The average value for the LATAM region at 24.7% is notably higher than for any other EM region.

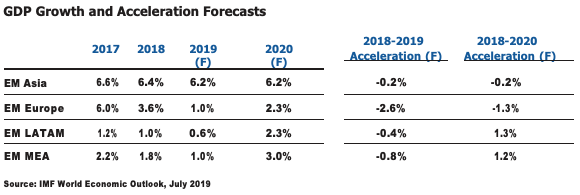

Growth Acceleration

After a difficult seven years, we expect the LATAM growth environment to improve in 2020. The economic recovery and stabilization process are expected to be slow but meaningful. Using the most recent IMF forecast numbers from July 2019, we can say that Latin America is the region within EM that is expected to show the strongest acceleration from 2018 to 2020. The prospect is strong even though Argentina is still pulling itself out of a deep recession and even as economic growth remains flat in Peru and decelerates in Chile, both being near 4%.

However, we are less enthused about Mexico’s economic prospects in the short-term. Investment has stalled due to political uncertainty, delays in the approval of USMCA, cuts in public spending, delays in construction in Mexico City due to changes in licensing requirements and uncertainty surrounding the U.S.-China trade war and US Trade and immigration policy.

However, the particularly disappointing growth in the first quarter of 2019 was largely driven by one-off factors such as a poorly managed attempt to stem fuel theft at Pemex as well as labor strikes. And prospects for the U.S.-Mexico trade relationship have improved as Mexico made major concessions regarding the role it will play in limiting immigration to the U.S.

Corporations

After the last six years, we believe that LATAM debt looks cheap relative to other regions in EM, offering a good entry point into higher quality assets. This is especially true for investment grade corporate bonds, which offer a steep credit curve, making them an alternative long-term investment. Within corporate bonds we find the financial sector to be particularly attractive. With the exception of Brazil and Argentina, the balance sheets of most banks in LATAM look strong as they have not relied heavily on external financing. Furthermore, most countries in the region are relatively underbanked, meaning that there is a large growth potential for this industry. LATAM governments generally provide an environment that is conducive to strong banking fundamentals including high interest rates and low- cost deposit financing.6,9

Expected Volatility for the Region

We expect the continuation in U.S.-China trade tensions to have an overall negative impact on the EMD asset class. The trade war will put a considerable drag on global economic growth through reduced trade volumes, supply-chain disruption and fostering uncertainty. Countries such as Malaysia that supply inputs to Chinese production of final goods ultimately sold in the U.S. might be particularly exposed to fallout from the trade war.

Yet some countries could temporarily benefit from the stand-off. Low cost manufacturing hubs that compete with China, such as Mexico and Vietnam have already taken some of the U.S. market share for manufactured goods. At the same time, China will look to source commodities such as soybeans from countries like Brazil or Argentina instead of the U.S.

As a result of the general weakening in developed markets and softening growth expectations for China, investors are likely to exhibit more risk-averse behavior. Although the valuations currently offer an opportunity to pick up higher quality assets in Latin America, we also believe that in 2019 and 2020 investors should expect a fair amount of volatility for EMD overall.

Domestic political uncertainty is likely to continue to be a source of volatility, especially for Argentina, Brazil, and Mexico. In Argentina, the October, 2019 presidential election could replace the market- friendly Mauricio Macri with a more populist president if the economy is not able to recover for out of the current high-inflation, recessionary situation. In Brazil, the conservative President Bolsanoro has increased investor confidence. However, his ability to pass a pension reform critical for the country’s fiscal health is unclear.

Mexico provides the most uncertain political panorama in the region. The current President Andres Manuel Lopez Obrador has left many investors uneasy due to his populist rhetoric as well as a number of policy missteps in the first months of 2019. These include cancelling the construction of a new airport north of Mexico City, a project which was 30% completed. An unsuccessful and poorly implemented attempt to stem massive fuel theft at PEMEX, which led to fuel shortages and contributed to a significant economic slowdown in 1Q, 2019, and the announcement of an underwhelming bailout package for the state-owned energy company, PEMEX. The bailout package was able to prevent a major sell-off but was insufficient to address PEMEX’s underlying problems - insufficient investment, excessive taxation and massive amounts of oil theft - or to prevent rating agencies from lowering PEMEX’s credit rating. Simultaneously, looming in the background is the question of whether the new NAFTA, USMCA, will be approved.

Yet President Lopez Obrador’s commitment to fiscal discipline has gone a long way to quell fears in capital markets. He has presented a balanced budget for 2019 and reduced current spending through cutbacks in wages, subsidies and transfers. Programable spending decreased 5% year-on-year in real terms in 1Q, 2019. Capital markets have responded well to the President’s commitment to fiscal austerity.

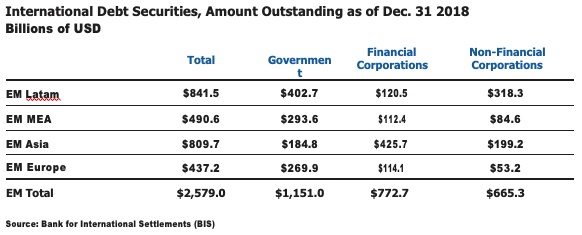

LATAM Debt Market Has Depth and Breadth Necessary for a Standalone Portfolio

LATAM debt is able to support a well-diversified standalone portfolio given its high share of EMD issuance as well as the diverse options in that issuance. Latin America and the Caribbean (LAC) presently have $841.6 billion USD in outstanding debt securities in international markets. This represents 33% of the EM debt issued in international markets, making it the largest issuer in the asset class. Latin America is followed by EM Asia at 31%, EM MEA at 19% and EM Europe at 17%. The heft of Latin America’s external bond stock is even more evident if we focus on non-financial corporations. Latin American debt represents 49% of all EM non-financial corporate debt issuance in international markets.1

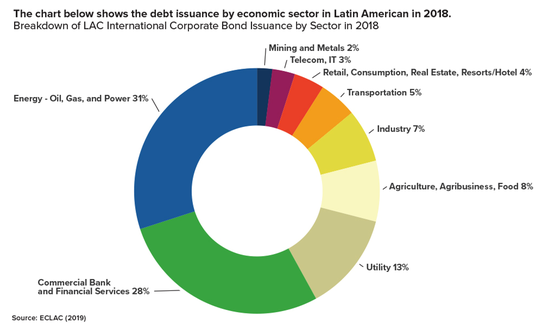

Moreover, Latin American bonds offer a wide range of choices. They are diversified across sectors, ratings, and issuers. In 2018 Mexico had the largest share of bond issuance (sovereign and corporate) within Latin America at 25.4%, followed by Brazil (20.18%) and Argentina (14.21%).10

Of the Latin America bonds issued in 2018, 40.5% were from sovereign issuers and 59.5% were corporate issuers. Within corporate debt issues, there is even more diversification. In 2018 42% of Latin America International corporate bond issuance was high-yield, while 58% was investment-grade.10 Other regions within EM offer much less diversification. Corporate bonds in Latin America also have a fair amount of variation by sector.

The underlying countries in LATAM are in and of themselves quite different. Although many LATAM countries are commodity exporters, the commodities which they produce are often affected by different underlying factors. The two largest economies in the region, Brazil and Mexico, have their fortunes tied to China in very different ways. Brazil produces what China purchases whereas Mexico produces what China makes and what the U.S. buys. Argentina is currently mired in a deep recession, and Brazil has been slowly recovering from a recession which began in 2011, while Peru and Chile are experiencing solid growth at 4%. We believe that as we enter a period of recovery for EM, the performance of individual countries will be quite varied as the underlying fundamentals will recover unevenly.

Conclusion

This decoupling of underlying fundamentals across LATAM countries offers an opportunity to construct a standalone portfolio of idiosyncratic investments. Regional specialization within LATAM harnesses these diversification benefits, thereby generating higher risk adjusted returns. An active manager who specializes in a geographic region and can better understand the regional nuances will be better equipped to exploit these opportunities while minimizing the risk of a significant drawdown.

Sources

1 Bank for International Settlements. Debt Securities Statistics, 31 Dec.

https://www.bis.org/statistics/secstats.html

2 Carstens, Agustin and Song Shin, Hyun. “Emerging Markets Aren’t Out of the Woods ” Foreign Affairs. 15 Mar. 2019.

3 Gonzalez, Pablo R. “Latin America’s $7 Billion Bond Pipeline Tests Capacity For ” Bloomberg, 23 Oct. 2018.

4 “Higher Education Expanding in Latin America and the Caribbean, but Falling Short of Potential.” World Bank, 17 May

5 International Monetary Fund (IMF). World Economic Outlook Database. April 2019

https://www.imf.org/external/pubs/ft/weo/2019/01/weodata/index.aspx

6 “Latin America Debt: A Complex Opportunity.” IPE, 1 Sept.

7 Organization for Economic Co-operation and Development (OECD). Funded Pension Indicators. 25 2019.

https://stats.oecd.org/Index.aspx?DatasetCode=PNNI_NEW

8 Papp, Zsolt. “Investing in Latin American Corporate Bonds.” JP Morgan Asset Management Global Fixed Income Blog, 17 Aug.

9 Rodriguez Valladares, Mayra. “Latin American Markets Look Promising in 2019 and Beyond.” Forbes, 10 Dec.

10 Velloso, Helvia. “Capital Flows to Latin America and the Caribbean: 2018 Year-in-Review.” Economic Commission for Latin America and the Caribbean, 11 Feb.

Disclosure: LM Capital Group, LLC is an SEC Registered Investment Advisor based in San Diego, CA. The firm specializes in active fixed income management for Institutions and High Net Worth individuals using a top-down, macroeconomic approach supported by in-depth, bottom-up research. SEC registration does not imply a certain level of skill or training.

This presentation is being delivered to, and is directed only at persons who are reasonably believed to be investment professionals, institutional investors, or other qualified investors. The presentation materials do not constitute as investment advice and should not be used as the basis for any investment decision. Any financial indices referenced as benchmarks within this presentation, are provided for informational purposes only. Materials presented are not intended as a solicitation or offer with respect to the purchase or sale of any security or other financial instrument or any investment advisory services. Reproduction of any part of this presentation without the approval of LM Capital Group, LLC is prohibited.

The data used to calculate any “model” performance was obtained from sources deemed reliable and then organized and presented by LM Capital Group. The performance calculations have not been audited by a third party. Actual performance of client portfolios may differ materially due to the timing related to the actual deployment and investment of a client portfolio, the reinvestment of dividends, length of time various positions are held, client objectives and restrictions, and fees and expenses incurred by the individual portfolio.

© 2019 LM Capital | All rights reserved

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits