“Plus ça change, plus c’est la même chose.”

(The more things change, they more they are the same)

- Jean-Baptiste Alphonse Karr

We live in a world defined by change. Anyone in doubt need only wait a few days to be reminded. Humans endeavor to measure it, describe it, and develop strategies designed to control it. Sometimes these observations persist long enough for emerging beliefs of changing paradigms or constructs. At the end of cycles, reversion to the mean gets lost as the “new normal” removes old norms from consciousness.

We are in one of those periods today, and French journalist and critic Jean-Baptiste Alphonse Karr had a vision (shared above) for keeping your head on your shoulders through these cycles. King Solomon offered additional perspective to the prevailing myopic view in Ecclesiastes 1:9, “What has been will be again, what has been done will be done again; there is nothing new under the sun.”

As contrarian value investors, we not only believe reversion is an eventuality, but that money can be made when the majority believe it to be dead. While we have no great affection for being masochistic, our discipline inherently embraces a great degree of patience in allowing the time necessary for fundamentals to win out against investor whims. Here is why:

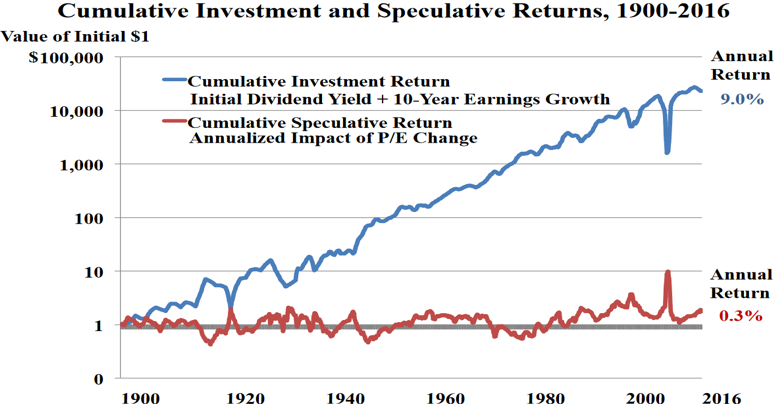

Source: http://johncbogle.com/wordpress/wp-content/uploads/2016/10/Bogleheads-15-2016.pdf

The red line above indicates the amount of money made from stock prices being revalued upwards and downwards since 1900. These changes in price-to-earnings ratios (“p/e”) have far more impact to stock-prices than business fundamentals over short or intermediate periods. Manifestations of this look like Netflix (Nasdaq: NFLX) being valued at 100x earnings, Apple’s (Nasdaq: APPL) valuation moving from 10x to 18.5x earnings over the past four years, or Tesla (Nasdaq: TSLA) garnering more market capitalization than both Ford and GM in recent years. However, fundamentals from earnings and dividends are infinitely more important and account for nearly all investment returns over long periods of time. This chart alone may explain the persistent underperformance of hedge funds or other strategies requiring a “good jockey” to game the market. Ultimately, the market can’t be gamed, but it can be weighed.

The red line today is influenced by the absolute level of interest rates and speculation of Central Bank guidance. What is lost on the market is that interest rates are not the issue for the economy. The economy is quite strong and currently rebounding. A quick look at consumer confidence, retail sales, employment, or even increased mall traffic over the past few years gives evidence of strength. Recent housing and unemployment numbers have surprised the naysayers and reinforced the blue line. The national household savings rate is the highest at 8.2% outside of recession years as it has been over the last 20 years.

Corporations are experiencing record corporate profits and plowing those dollars back into buying their own stock in historically high share quantities. These speak to the blue line, and look like NVR, Inc (NYSE: NVR) buying back 75% of its shares in the last 20 years or Amgen (Nasdaq: AMGN) buying back 53% of its shares since 2003. Amgen has also increased its dividend 420% from eight years ago and Discovery Communications (Nasdaq: DISCA) has increased its earnings nearly eight-fold in that same timeframe while doubling its free-cash flow in the last two years.

We believe it is more important than ever to maintain a long duration view in today’s markets. When the noise becomes deafening, you need discipline in order to hear the signal. Our discipline plays almost exclusively towards the blue line, which requires us to accept periods where the red line may cause temporary victory. We have never met a private business owner who gained wealth by trading in or out of their businesses as valuations ebbed or flowed—the story we consistently hear extols the value of patiently owning great businesses over long periods of time. We endeavor to do the same thing in the public markets to meet our goal of creating wealth for our trusted clients.

Warm Regards,

Tony Scherrer, CFA

The information contained in this missive represents Smead Capital Management's opinions and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Tony Scherrer, CFA, Director of Research, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

© 2019 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com

Follow us on Twitter @SmeadCap