Schwab Market Perspective: Hitting the Ceiling

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Points

-

U.S. stocks have been relatively stable in the absence of trade tension escalation, but have failed to breach their all-time highs in July.

-

Economic data has been mixed of late, and leading indicators have not yet confirmed the recent strength in economic surprises.

-

Global manufacturing weakness is beginning to spill over into confidence and employment channels, sending an ominous signal for world economies.

“Nothing ever becomes real till it is experienced.”

―John Keats

Hitting the ceiling

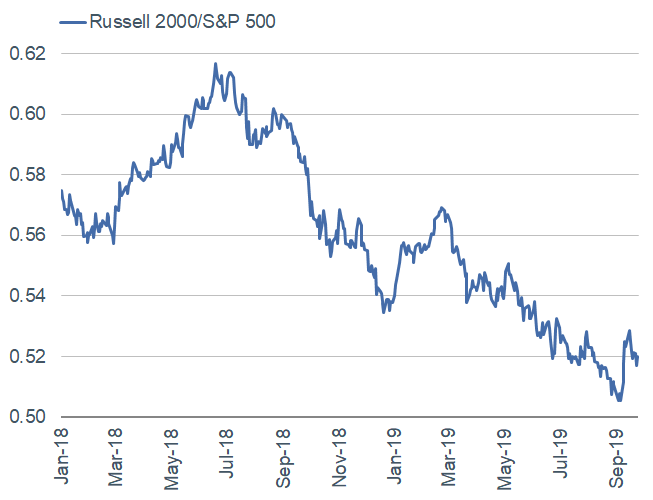

While U.S. stocks emerged out of their tight range a couple weeks ago, they have yet to surpass their July highs—as trade uncertainties remain, economic data continues to be mixed, and cloudy monetary policy and political outlooks persist. U.S. equities’ breakout to the upside was accelerated by a rapid factor reversal that favored small-cap and value stocks—strategies that have not worked for investors in the current bull market. Yet, this turned out to be a very short-lived phenomenon and we are back in an environment that tends to favor large-cap, low volatility and momentum stocks. You can see in the chart below small caps’ brief strong showing along with large caps’ subsequent outperformance over the past couple weeks; as well as large caps’ strength over the past 18 months. Larger cap companies have lower debt levels than their smaller cap brethren; are more nimble with regards to trade; and have a global presence, making it possible for them to borrow at negative rates. These fundamentals, along with the fact that a record percentage of smaller companies have soaring debt levels (as measured by the S&P 600’s debt-equity ratio of 124%), continue to support our large cap bias.

Small Caps’ Moment in the Spotlight is Over

Source: Charles Schwab, Bloomberg, as of 9/25/2019. Relative performance of Russell 2000 to S&P 500. Past performance is no guarantee of future results.

A divided economy

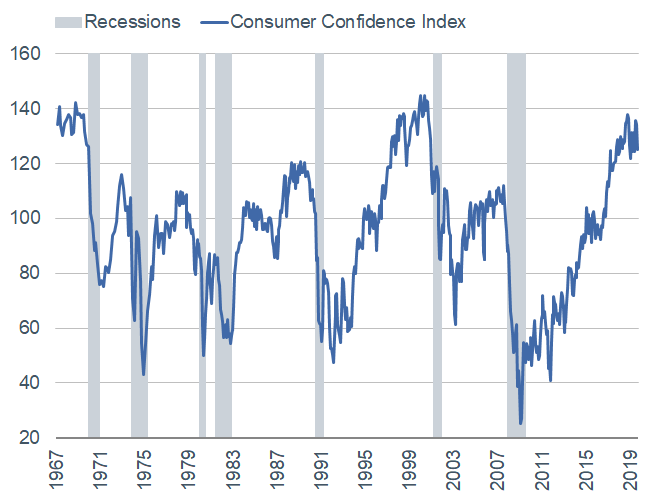

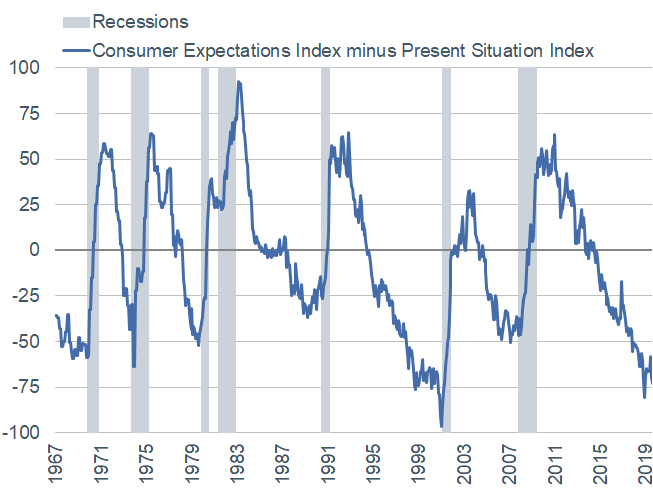

Economic data has been mixed of late, keeping firm the line that separates services/consumer strength from manufacturing’s weakness. The U.S. Census Bureau reported that retail sales rose 0.4% m/m in August, along with an increase in personal consumption of 4.6% in the second quarter (as per the Bureau of Economic Analysis). In addition to still-low jobless claims and a tight labor market, the overall picture for the consumer remains fairly bright. Yet, strength may start to wane if trade uncertainty continues to weigh on sentiment and/or the remaining tariffs kick in later this year. This may be starting to show up in consumer confidence which—as measured by The Conference Board—fell sharply in September to 125.1 from 134.2 in August. The below charts show this decline along with a drop in the difference between the Consumer Expectations Index and the Present Situation Index—which is still firmly negative. It is important to keep in mind that this index tends to trough (shortly) in advance of recessions, while consumer confidence tends to peak at the same time.

Consumer Confidence May Have Already Peaked

Source: Charles Schwab, Bloomberg, The Conference Board, as of 9/24/2019.

Source: Charles Schwab, Bloomberg, The Conference Board, as of 9/24/2019.

Conflicting data within manufacturing and services

An erosion in consumer data—which could be precipitated by the threatened October 15 and December 15 tariffs that hit consumer goods—may accompany weakness that has started to appear in the services sector. The recent Markit “flash” Purchasing Managers’ Indexes (PMIs) for September revealed a bit of an uptick in the headline numbers—with manufacturing rising to 51 and services to 50.9 (both above 50, which separates expansion from contraction). Notwithstanding manufacturing’s modest rebound, the underlying data was a bit worrisome for services this time around. Subdued demand resulted in the first employment reduction on the services side of the economy in just under 10 years. This supports our view that if the malaise in manufacturing were to bleed into services, it would most likely show up first in the employment channels.

Importantly, there have been mixed results from the regional Fed manufacturing surveys—as the Philadelphia and Empire PMIs increased in August, but the Richmond index fell sharply and the Kansas City index remained negative. Beneath the headline numbers, new orders, shipments, and employment components varied across all regions. Barring the release of the Dallas Fed’s PMI at the end of the month, the Markit PMIs and the average of the regional surveys are still elevated relative to the ISM Manufacturing Index. Considering this divergence, the September ISM release will be an important confirmation or denial of continued weakness.

Leading indicators: flattening or slowing down?

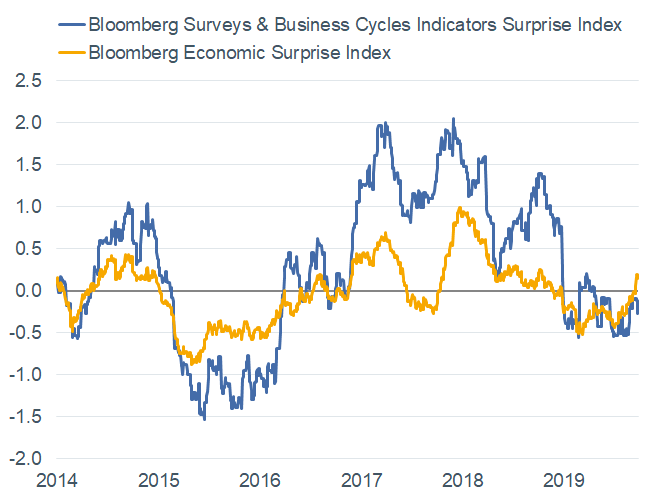

The Conference Board recently released its Leading Economic Index (LEI), which was unchanged in August and has been quite flat for most of the past year. While certain sub-components—such as ISM New Orders and the yield spread—continue to pull the index down; others like unemployment claims and building permits have been positive offsets. Thus, you can see in the following chart, a similar scenario can be seen in the recent surge in the Bloomberg Economic Surprise Index (BESI), which has shot higher courtesy of data surprising to the upside. Yet, much of that improvement has been concentrated in lagging economic indicators. The blue line represents the Bloomberg Surveys & Business Cycle Indicators Surprise Index, which is a sub-index of the BESI and measures surprises among the leading components. You can see that this has not confirmed the spike in the BESI, which leads us to believe that the excitement may be a bit premature. [Read more about what leading indicators are telling us in Take Me to Your Leader: Analyzing the Latest Leading Indicators.]

Economic Surprises Lack Confirmation

Source: Charles Schwab, Bloomberg, as of 9/25/2019. The Bloomberg Economic Surprise Index shows the degree to which economic analysts under- or over-estimate the trends in the business cycle. The surprise element is defined as the percentage (or percentage point) difference between analyst forecasts and the published value of economic data releases.

The path for interest rates is not set in stone

As expected, the Federal Open Market Committee (FOMC) cut interest rates by 25bps at its September meeting. There were three dissents—the first time since 2016—with Kansas City Fed President Esther George and Boston Fed President Eric Rosengren suggesting no cut at all, and St. Louis Fed President James Bullard in favor of a 50bps cut. Separately, the median of the FOMC’s “dots plot” signaled no change in rates for the rest of the year—which half of the members agree will be the case moving forward.

The FOMC also decided to cut interest on excess reserves (IOER) by 30bps, which exacerbated some unease amidst the New York Fed’s recent interventions in the repo market. While this has spawned chatter of quantitative easing (QE), our colleague and Chief Fixed Income Strategist, Kathy Jones, has noted that these liquidity injections represent technical fixes at this point. Because the funding market has tightened, making bond purchases difficult to finance, the Fed has engaged in repurchase agreements (“repos”) to bring the effective federal funds rate (EFFR) back into the Fed’s target band. The market gets worried when there is a shortage of liquidity, mostly because the most leveraged players can get squeezed (causing adverse reactions), but the repos do not signal that a major financial institution is in imminent trouble. [For more Fed commentary, read The Final Cut … or More to Come?]

Spillover signs?

Manufacturing has been the primary source of global economic weakness since the downturn began, with the first round of U.S.-China trade tariffs announced in early 2018. Yet, the weakness has been largely concentrated in exports and manufacturing with limited evidence of spillover to the rest of the economy. But that may be changing. The September Markit PMIs for Europe showed what may be early signs of weakness spilling over from:

- exports to domestic demand;

- manufacturing (15% of GDP per 2018 World Bank data) to services (66% of GDP);

- and production to employment.

If these spillovers become more evident, they would send an ominous signal for the global economy.

The slowdown in global manufacturing began with export demand. In recent years, overall manufacturing orders in Europe have exceeded export orders—pointing to healthier domestic demand relative to foreign demand for exports. But that changed this year, and this week’s preliminary reading for September reflected a sharp drop in domestic orders, suggesting potential spillover from weak export demand to what had been a resilient domestic economy.

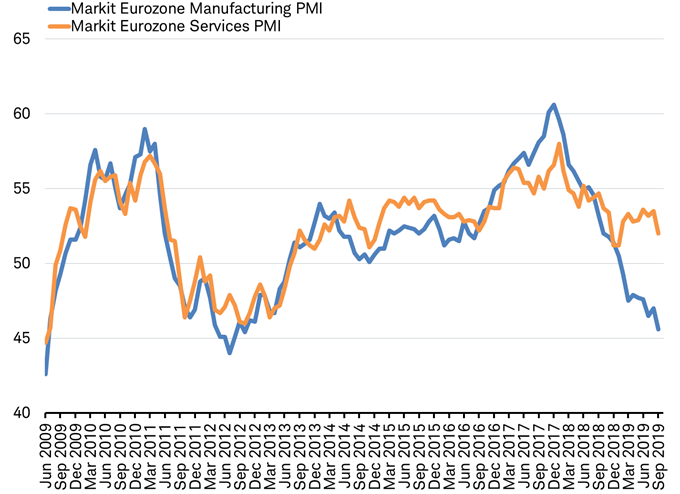

The Eurozone PMI data shows that the services sector of the economy continued to grow—as the September preliminary reading of 52 is above the 50 level and marks expansion. Yet, the yawning gap between manufacturing and the much larger services sector of the Eurozone economy is worrisome. Should services catch down to manufacturing, it may reach a level not seen since the European recession of 2012-13, as you can see in the chart below.

Gap Starting to Close?

Source: Charles Schwab, Bloomberg data as of 9/25/2019.

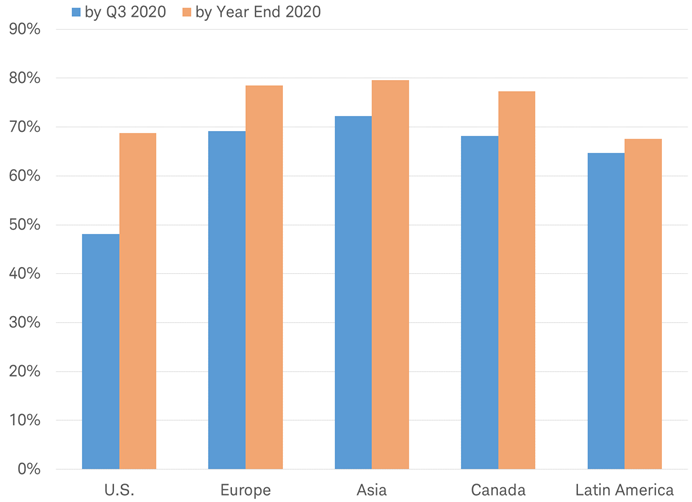

The weakness in manufacturing may also be spilling over into business leaders’ behavior and sentiment. The September CFO survey from CFO magazine and Duke University shows that nearly 70% of surveyed CFOs in the United States—and nearly 80% in Europe, Asia and Canada—expect a recession to begin sometime next year, as you can see in the chart below.

Most CFOs Expect a Recession Next Year

Source: Charles Schwab, CFO Magazine/Duke University survey cfosurvey.org data as of September 2019.

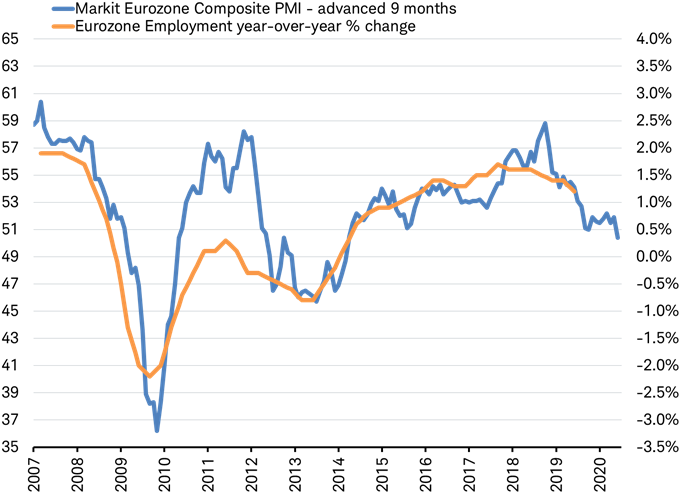

In anticipation of a recession, these executives may begin to cut back not just on equipment, but also on labor. Historically, Eurozone employment tends to follow the lead in the composite PMI (which includes both the manufacturing and services sectors) by about nine months, as you can see in the chart below. Further evidence of spillover may mean overall Eurozone employment could be headed for contraction in 2020.

Eurozone Job Growth Headed for a Slowdown?

Source: Charles Schwab, Bloomberg data as of 9/25/2019.

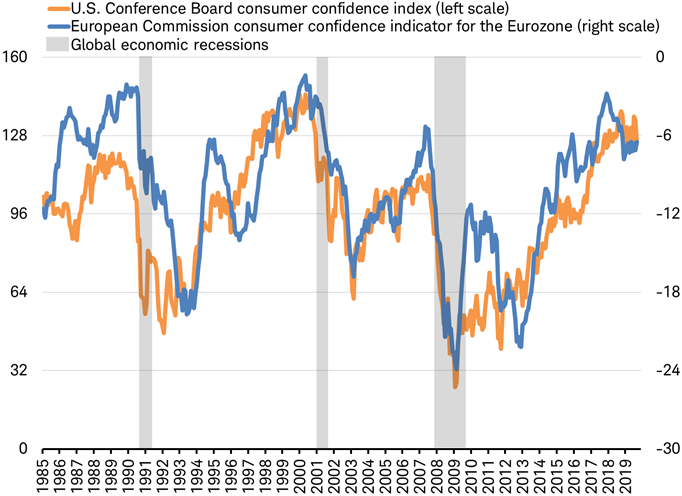

Consumers have been feeling confident in Europe, similar to their U.S. counterparts, as you can see in the chart below. But if the weakening confidence of business leaders leads to a deteriorating job market, it could further spill over into weaker consumer confidence.

Eurozone Consumer Confidence May Start to Slide

Source: Charles Schwab, Bloomberg data as of 9/25/2019.

The consumer has been the source of the remaining strength in the European economy. While this week’s report isn’t conclusive, we will be keeping an eye on the possibility of cascading spillovers of weakness from manufacturing to the rest of the economy. If increasing signs of such a spillover occur, it may lead to a retrenchment in Europe’s stock market which currently stands just 6.6% below the all-time highs set in 2000 and 2007, measured by the MSCI Europe Index.

So what?

The lack of trade news has kept volatility subdued lately, but stocks have still made limited headway over the past 20 months. Considering the potential for political headlines to change and trade tensions to escalate at any moment, we continue to believe that trading around short-term news is a treacherous exercise. As such, our recommendation continues to be that investors stay near their long-term asset allocation but use volatility to rebalance back to strategic allocations; while we continue to favor large caps relative to small caps within U.S. equities. With much uncertainty remaining with regards to trade, monetary policy, politics, and the economy, the path ahead for stocks appears no less choppy than it has been in prior months.

Important Disclosures

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. This content was created as of the specific date indicated and reflects the author’s views as of that date. Supporting documentation for any claims or statistical information is available upon request.

Diversification and rebalancing of a portfolio cannot assure a profit or protect against a loss in any given market environment. Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability

Past performance is no guarantee of future results. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data. The policy analysis provided does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

The Consumer Expectations Index is a component of the Consumer Confidence Index® (CCI), which is published each month by the Conference Board. The Expectations Index is made up of the average of the CCI components that deal with six-month outlooks for business, employment, and income.

The Present Situation Index is a sub-index that measures overall consumer sentiment regarding the present economic situation. This index is determined via survey conducted by The Conference Board, and is used to derive the Consumer Confidence Index. This is also sometimes known as the Current Situation Index.

The Markit Eurozone PMI Composite Output Index tracks business trends across both the manufacturing and service sectors, based on data collected from a representative panel of over 5,000 companies (60 percent from the manufacturing sector and 40 percent from the services sector).

The MSCI Europe Index captures large and mid cap representation across 15 Developed countries in Europe. With 448 constituents, the index covers approximately 85% of the free float-adjusted market capitalization across the European Developed Markets equity universe.

Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

©2019 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All