What sources of market returns can withstand late-cycle uncertainty? By identifying the right ingredients, we think investors can create an allocation with the potential to overcome new challenges and perform well over the long term.

Market risks are rising and returns across asset classes are likely to be moderate from here on out. Investors, meanwhile, must choose among a plethora of options, from actively managed portfolios to an increasing number of passive smart-beta portfolios, which aim to deliver performance driven by market factors. As a result, every choice creates exposure to different betas, or market returns.

But which betas are right for the tests that lie ahead? In today’s environment, we think it’s time for investors to consider the right balance between maximizing returns and protecting against future losses. That means finding investments whose returns in rising markets (upside capture) exceed their losses in falling markets (downside capture), relative to a given benchmark.

The right upside/downside capture ratio will vary, given differing risk appetites and investment horizons. But achieving it may help investors enjoy a smoother pattern of returns through volatile markets. This is important for two reasons. First, it can help investors avoid a classic investing mistake by panicking and selling low when a downturn hits. Second, for baby boomers who are nearing or early into retirement, minimizing potential losses is crucial when it’s time to sell funds for spending needs.

Riding the Ups and (Especially) the Downs with Better Betas

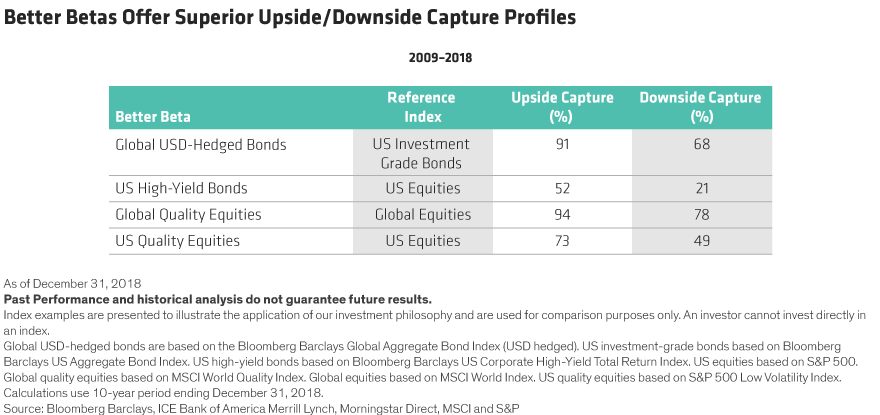

Some investments have an inherently more favorable upside/downside capture ratio than do other similar risks. We call them better betas. Most important for this late point in the economic cycle, their outperformance is often down to better downside protection.

Over a 10-year period, a global fixed-income allocation hedged to the US dollar earned 91% of what a US-only investment-grade allocation did in a rising market, while suffering just 68% of the losses. The illustrative examples below represent just a few of the many different ways investors can build portfolios to capture better betas than do standard equity and fixed-income benchmarks (Display)

Why does this better beta work? Exposure to many countries helps diversify economic cycle risks because it captures different yield curves across a range of economies—which don’t always move in lockstep. Currency-hedged government bonds of developed economies tend to perform similarly in up markets—either when coupons are simply being “clipped” and yields are generally unchanged, or in a risk-off scenario, when yields of developed-market bonds tend to fall in unison. However, during rate-tightening cycles, when bond performance struggles, monetary policies tend to be a bit less “synced.” Indeed, in 2008, yields fell throughout the developed world, but during the subsequent recovery, the tightening of monetary policy was more mixed.

High-yield bonds can often provide better betas than some passive large-cap equity exposures. Even though they may have a lower upside capture than stocks, they also tend to have a very low downside capture. On balance, that makes for a winning combination over the long term.

In equities, high-quality stocks—such as those with high free-cash-flow yields and profitability, and low leverage ratios—are better betas. Higher-quality companies don’t perform much worse than their peers when markets are going up, but investors flock to the relative stability they provide when markets are falling.

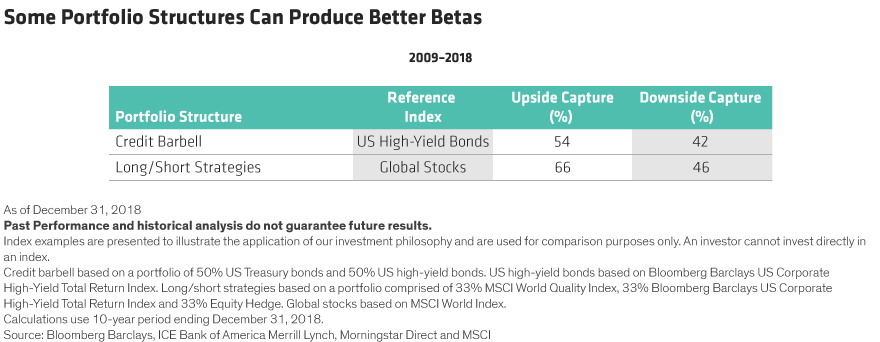

When Beta Plus Beta Equals Better Beta

Combining several types of investments can also create better upside/downside capture ratios for an overall portfolio. A credit barbell is a perfect example. While high yield is often a better beta than a naïve exposure to large-cap equities, investing in both high-quality bonds and high-yield bonds resulted in a favorable upside/downside capture profile versus investing in high yield alone over the past decade. Long/short equity strategies can similarly deliver a more resilient upside/downside capture profile (Display).

Active Choices for a Complex Future

Over the past decade, investors could be excused for being less discriminating about their beta choices. As central banks were flooding markets with cheap money, investment funds of all types prospered as markets rose broadly, in what we call the Great Beta Trade. But as growth moderates, the global debt burden balloons, baby boomers begin to retire and geopolitical tensions mount, the Great Beta Trade is great no more.

Now, the quality of assets, strategies and managers matter once again, and every investment is an active choice. Better betas can be sourced in many different ways—from active portfolios, passive exchange-traded funds and factor-oriented solutions. But every source of beta has its pros and cons.

The devil is in the details. For example, a passive allocation to quality stocks may not be as resilient as expected, depending on how the investment solution defines quality and sources it. And the number of choices can be overwhelming, with huge performance differentials between similar funds in the same categories. That’s why it’s more important than ever for investors to know exactly what they own, and why. Some betas are clearly better than are others for investing in a late-cycle market environment, but finding them requires careful and informed shopping.

Richard Brink is a Market Strategist in the Client Group at AB

Walt Czaicki is a Senior Portfolio Manager for Equities at AB

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams, and are subject to revision over time.

© AllianceBernstein L.P.

© AllianceBernstein

More Active Management Topics >