Amid the ongoing volatility of equity prices, underlying midstream fundamentals continue to be healthy. Midstream throughput, as measured by the production of oil, natural gas, and natural gas liquids (NGLs), continues to increase. Midstream capital needs and balance sheets also continue to improve.

Despite this constructive fundamental backdrop, midstream equity prices, as measured by the Alerian MLP Index (AMZ), have recently retraced to levels close to the lows of 2016, when crude oil prices were near $40 per barrel and the trajectory of US production appeared less clear.

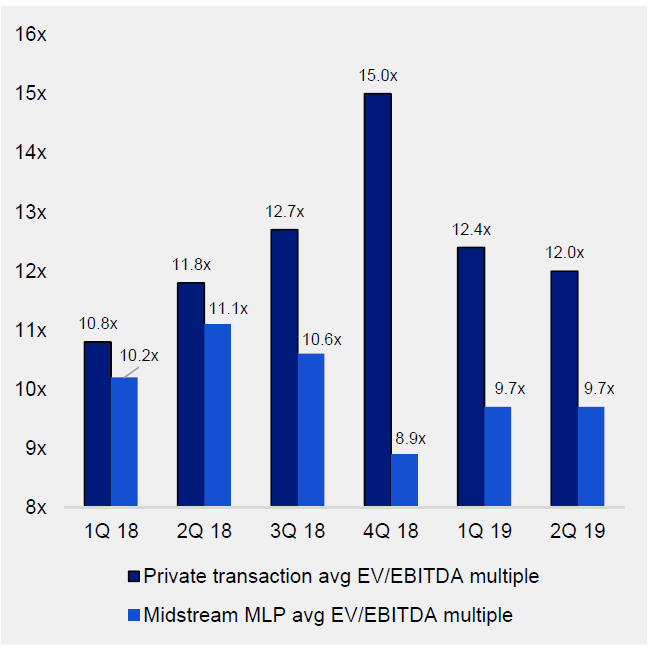

Unsurprisingly, private equity companies have seen the pricing dislocations between midstream asset and equity valuations and have been opportunistically acquiring midstream assets as well as entire companies at multiples above current public market multiples. In the latest instance, Blackstone Infrastructure Partners announced on Aug. 27 an offer to take Tallgrass Energy (NYSE: TGE) private, at an approximate 35.9% premium over TGE’s closing price on the date of the offer.

Private equity ramping up investment in midstream at higher valuations than where public MLPs are trading

Source: Morgan Stanley and company press releases as of 6/30/19.Source: Wells Fargo Research as of 6/30/19.

Operating performance has been strong

Counterintuitively, the recent weakness in midstream equities followed healthy second-quarter earnings. For the quarter, 71% of sector participants reported results that were in-line or better than consensus and sector EBITDA was up over 17% from the same period last year. Further, many sector participants have continued to capture new growth opportunities, particularly related to the Permian basin and export demand.

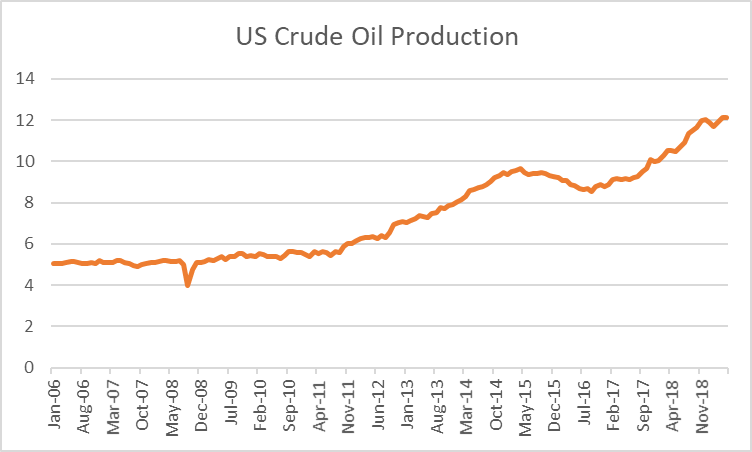

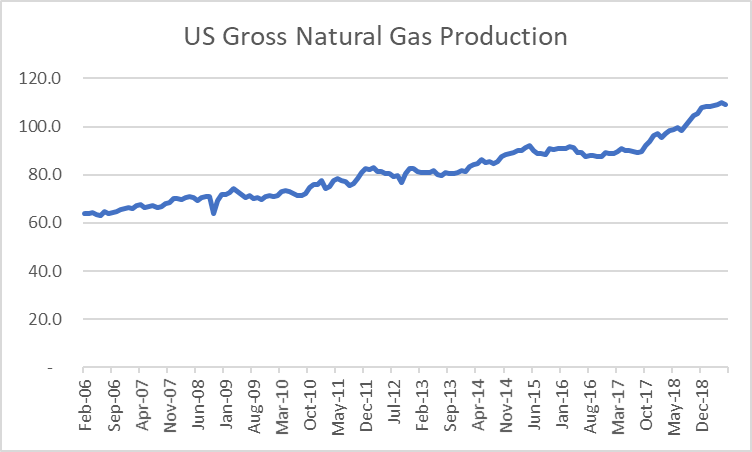

Driving this healthy fundamental backdrop is the steady pace of US production growth and global demand. Despite commodity prices that remain well below cyclical highs, improved drilling and completion techniques and cost control measures are allowing producers to achieve well economics today that rival results prior to the 2014 crude oil price collapse. Though producers have recently begun to focus on delivering free cash flows to investors rather than quick production growth, absolute volume growth is still likely to be healthy.

For example, the US Energy Information Administration, in its most recent Short-term Energy Outlook,1 projects US crude oil production will average 12.3 million barrels per day (MM bpd) in 2019 and 13.3 MM bpd in 2020, both of which would be record levels.

Source: US Energy Information AdministrationSource: US Energy Information Administration

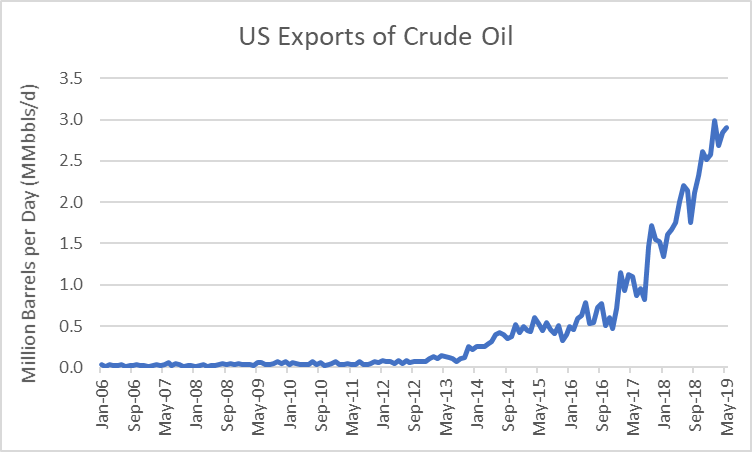

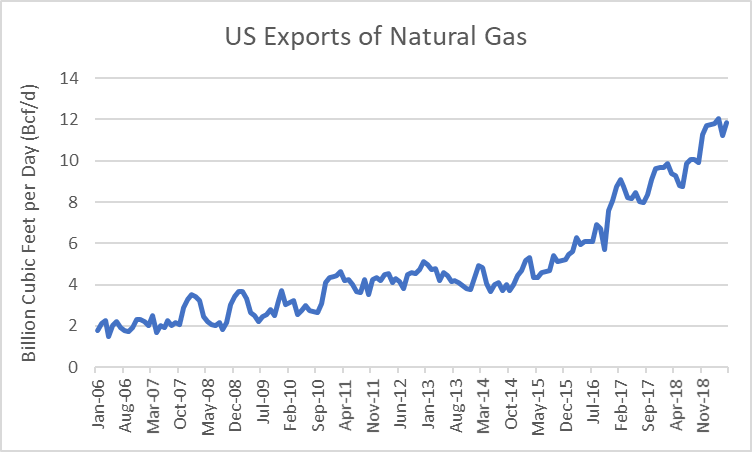

Supply growth driving export business

As production growth of crude oil, natural gas, and natural gas liquids in the US have exceeded domestic demand growth, export volumes have increased materially.

Source: US Energy Information AdministrationSource: US Energy Information Administration

Obviously, energy infrastructure, or midstream, assets are also required to meet the logistical challenge of bringing these volumes to export locations and loading these volumes on internationally bound vessels. Notably, a number of midstream operators — such as Enterprise Products Partners (NYSE: EPD), Energy Transfer (NYSE: ET), Targa Resources (NYSE: TRGP), Magellan Midstream Partners (NYSE: MMP), Buckeye Partners (NYSE: BPL) and NuStar Energy LP (NYSE: NS), amongst others — operate major export facilities and are continuing to expand their presence.

What about demand?

While demand for crude oil has been strong over the past few years, global economic activity does appear to be slowing. Importantly, regardless of whether a recession is coming or not, demand for crude oil has proven to be inelastic through the business cycle, and instances of radical oil demand retracement are rare. In the last 30 years, global oil demand has turned negative only three times. The first occurred amid the collapse of the Soviet Union in 1993; the second two took place during the two years (2008 and 2009) of the global financial crisis. During all other periods of economic slowdown, defined as periods where global gross domestic product (GDP) grew by 2.5% or less, global oil demand growth averaged 0.9%.

Additionally, the topic of electric vehicles (EVs) has moved heavily into the energy market conversation and has led to some market participants questioning demand for crude-derived transportation fuels. While the adoption of EVs is an attention-grabbing, long-term theme, even the most aggressive EV sales forecasts, if realized, would create only a slow and marginal impact on worldwide oil demand over the next decade. (In future blogs, our team will provide more context and further insight on the potential impact of EVs and renewables on energy market fundamentals.)

Outlook

As noted above, we believe industry fundamentals remain strong. Further, many operators have reached or are nearing a level of retained cash flow (cash flow available after paying dividends or distributions), to self-fund growth projects. In fact, the sector average distribution coverage ratio now sits at 1.5x versus a historical average of 1.1x.2 Over time, the sector’s strong coverage metrics may also begin to improve dividend- or yield-focused investor interest in the sector. Sector valuations are attractive relative to historic ranges, and sector yields are substantially higher than they are for other yielding equity classes. We believe the fundamental disconnect between current market valuations and underlying business health is likely to continue to attract private equity investment until this disconnect is normalized.

1 Source: EIA, Short-Term Energy Outlook, Aug. 6, 2019

2 Source: Wells Fargo Research, May 2019

Important Information

Blog header image: AvigatorPhotographer / iStockPhoto.com

The mention of specific companies does not constitute a recommendation by Invesco Distributors, Inc. Certain Invesco funds may hold the securities of the companies mentioned.

Investing in MLPs involves additional risks as compared to the risks of investing in common stock, including risks related to cash flow, dilution and voting rights. Each fund’s investments are concentrated in the energy infrastructure industry with an emphasis on securities issued by MLPs, which may increase volatility. Energy infrastructure companies are subject to risks specific to the industry such as fluctuations in commodity prices, reduced volumes of natural gas or other energy commodities, environmental hazards, changes in the macroeconomic or the regulatory environment or extreme weather. MLPs may trade less frequently than larger companies due to their smaller capitalizations which may result in erratic price movement or difficulty in buying or selling. Additional management fees and other expenses are associated with investing in MLP funds. Diversification does not guarantee profit or protect against loss.

The opinions expressed are those of Invesco SteelPath, are based on market conditions as of the date of publication and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

Brian Watson serves as a Senior Portfolio Manager for the Invesco SteelPath strategies.

Prior to joining SteelPath in 2009, Brian was a Portfolio Manager and led the MLP research effort at Swank Capital LLC, in Dallas, Texas. He also covered the MLP and Diversified Energy sectors for RBC Capital Markets in the firm’s Equity Research Division from 2002 to 2005. Prior to this, Brian worked for Prudential Capital Group, helping to analyze, structure, and invest in debt private placements issued primarily by companies involved in the energy industry including those involved in oil field services, midstream services, and oil and gas exploration and production.

Brian holds a B.B.A. from the University of Texas at Austin and an M.B.A. from the McCombs School of Business at the University of Texas at Austin. He is a CFA® charterholder.