Weighing the Week Ahead: Is Falling Confidence a Threat to Markets?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar is more important than usual. There is an emphasis on housing data as well as reports on leading indicators, industrial production, and regional Fed surveys. The most important story of the week will be the Fed’s Wednesday rate decision. Market prices imply a high probability of a 25 basis point rate cut. Many market participants are counting on the Fed, but the real question is broader. Pundits should be asking:

Is falling confidence a threat to markets?

Last Week Recap

In last week’s installment of WTWA, I asked whether it was time to worry about crowded trades. That was indeed the question on financial news to start the week. Hunting for Cheap Stocks is Back in Favor. A massive market rotation called into question much of the “wisdom” of the last few months. Interest rates rose, the yield curve steepened, and value stocks rebounded versus momentum. Now, of course, the popular question is whether this “has legs.”

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring the Investing.com version. It is static in this report, but if you go to the site you can use a number of interactive features. For those who want to explore the effect of specific events, there are news callouts.

The market gained 0.9% for the week. The trading range was 1.8%. The index chart conceals the biggest story – a massive rotation reflected by big sector moves.

News You Can Use

Dr. Brett Steenbarger’s new book is now available! Radical Renewal: Tools for Leading a Meaningful Life is innovative in both form and content. While he emphasizes traders, his work has implications for everyone. The format makes it especially user-friendly. When I finish reading, I’ll do a more complete review, but what I have seen so far is great. Dr. Brett has begun a series of regular blog posts on topics from his new book. It is an easy way to get started.

Noteworthy

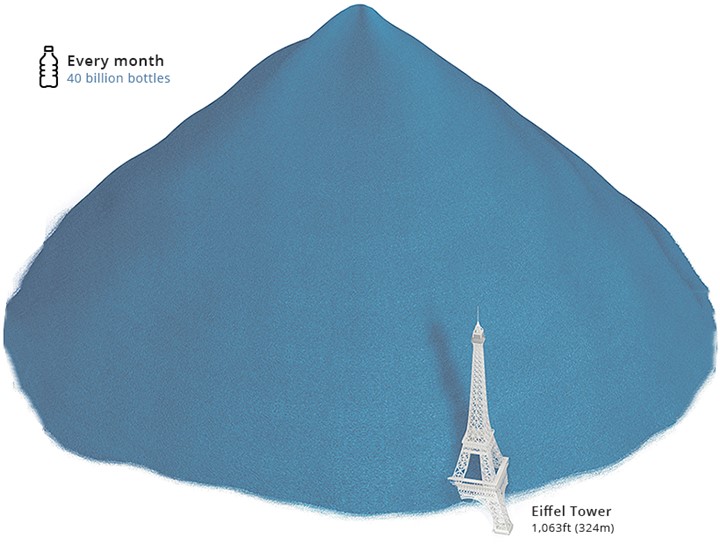

The Visual Capitalist has several striking images of plastic bottle waste compared to major landmarks. The whole post is dramatic, and the final chart demonstrates the floundering efforts toward plastic recycling. This is a good example.

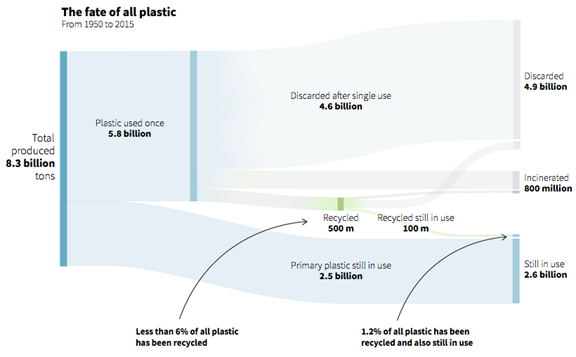

OK, I cannot resist including this image as well.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators are an important part of our regular research. The results remain positive in all three of the time frames, with improving readings. NDD notes that the long leading indicators are still “very positive.” His chief concern now is possible softness in Q3 earnings.

The Good

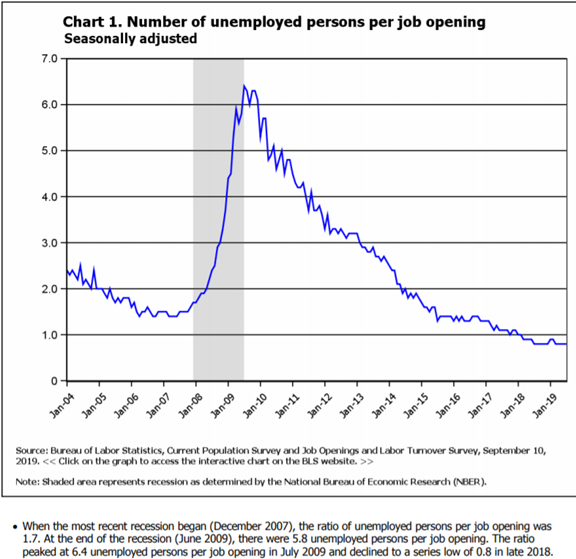

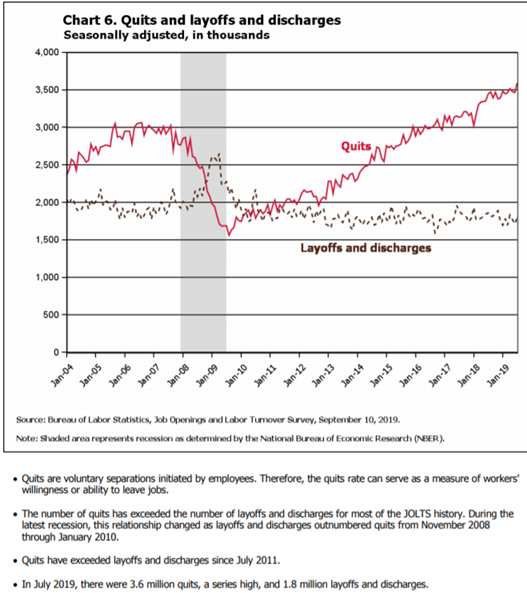

- JOLTs showed continuing labor market strength, but the market is tightening. Some analysts look only at the total number of job openings. More important is the ratio of openings to job seekers and the quit rate. Both charts are from the excellent BLS collection.

- Mortgage applications were up 2.0% versus the prior week decline of 3.1%

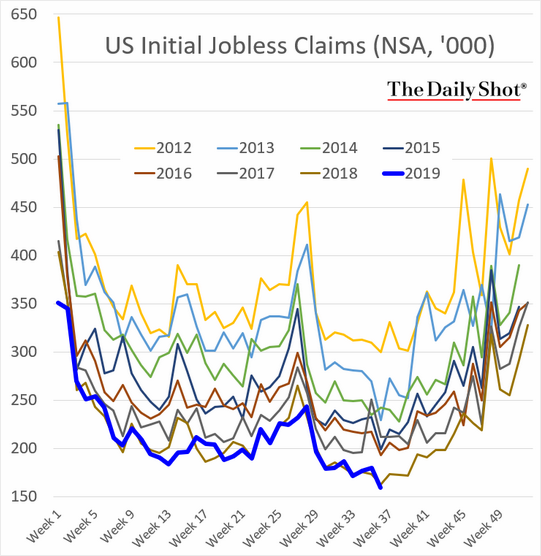

- Initial jobless claims moved even lower, to 204K. This compares with the prior week’s 219K and expectations of 218K.0

-

Trade tensions

- China halted the tariffs on pork and soybeans and resumed buying some pork.

- The US delayed for two weeks the latest round of tariff increases. (Time).

- Talks have resumed.

-

Retail sales Brian Wesbury

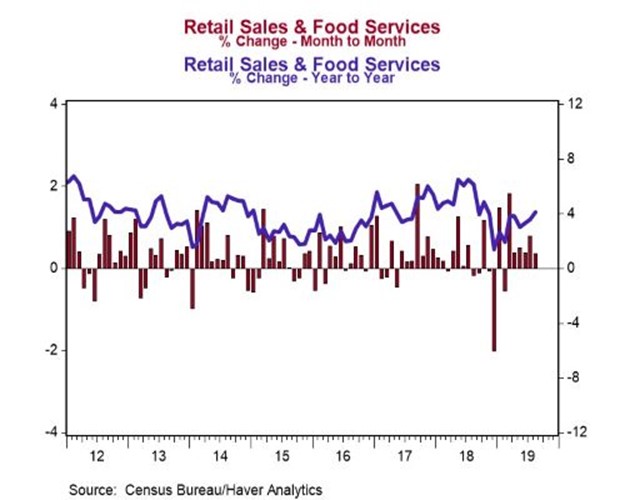

Autos and non-store retailers (think internet & mail order), led the way rising 1.8% and 1.6% in August respectively. Non-store sales are up 16.0% from a year ago, sit at record highs, and now make up 12.8% of overall retail sales, also a record. The largest decline in sales in August was for restaurants & bars, which had a 1.2% decline, the largest drop since September of last year. This drop may have been due to the approach of Hurricane Dorian late in the month, in which case they should rebound in the months ahead. “Core” sales, which exclude autos, building materials, and gas stations (the most volatile sectors) were unchanged in August, but are up 4.5% from a year ago. And even with the flat reading in August, “core” sales are up 9.4% at an annualized rate since the start of 2019, the fastest eight-month pace of growth we have seen since record keeping began in 1992!

- University of Michigan Sentiment (Sept. preliminary reading) increased to 92.0, beating expectations of 90.2 and August’s 89.8.

The Bad

-

Producer prices increased only 0.1% in August, in line with expectations, but the core reading was up 0.3% after a decline of 0.1% in July.

-

Rail traffic continues to weaken, especially in Steven Hansen’s (GEI) economically intuitive sectors. (See the Barron’s cover story in the “Watch Out” section below).

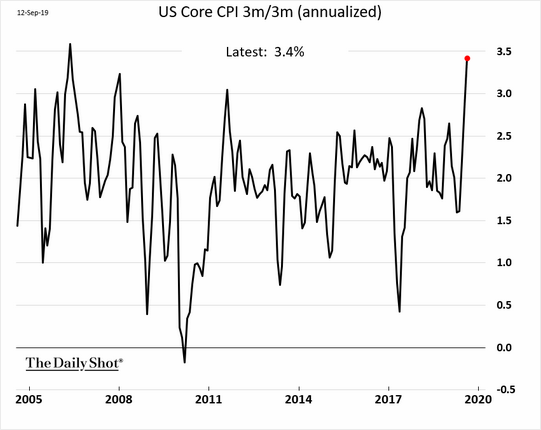

- Consumer prices for August also showed a tame 0.1% increase, down from July’s 0.3%. Core CPI, however, increased 0.3% matching July’s result and above expectations of 0.2%. Some observers view this as good news because of the Fed’s announced 2% target. This is mistaken. What we really want is solid growth without inflation. While there is a long-term correlation, inflation is a poor growth indicator. Brian Wesbury describes the concern. The Daily Shot charts the series.

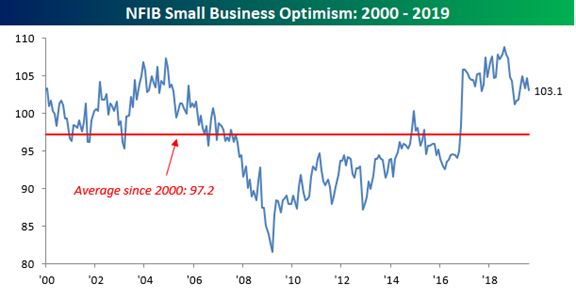

- NFIB’s Optimism Index declined to 103.1 from 104.7. There are no official expectations for this report, but small business has maintained a high confidence level since Trump’s election. Bespoke describes the overall index changes as well as elements of biggest concern – quality of labor, taxes and government red tape.

The Ugly

Refinery attacks. The drone strikes knocked out half of the Saudi oil capacity, about 5% of daily global consumption. This action reflects the continuing escalation of the regional conflict which threatens to expand as well. There is also a direct economic impact, although the refineries are expected to resume production “within days.” (CNN, Reuters)

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

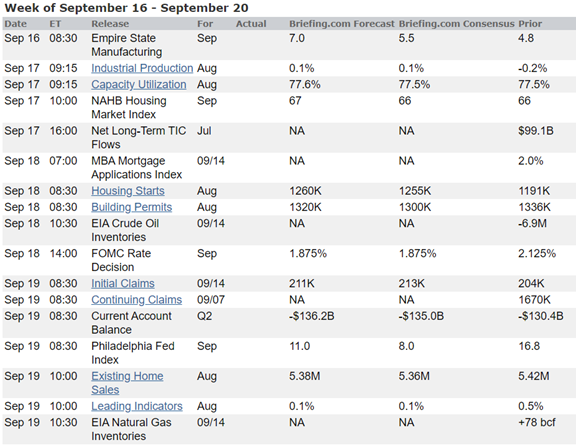

The Calendar

The calendar is bigger than usual, with an emphasis on housing data. Fans of the leading indicators will have that news on Friday. The highlight for everyone will be Wednesday’s FOMC decision.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

Traders currently believe that the Fed is supportive, but the question has become a broader one:

Is falling confidence now a threat to markets?

Background

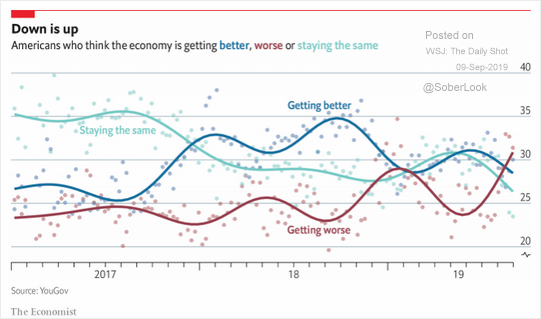

On several occasions I have mentioned my concern about declining consumer and business confidence. When people are worried, it is easy to defer spending and investment. “Let’s delay the refrigerator replacement.” Or “We’ll have a better handle on future needs in a few months. We can hold off on starting the plant expansion until then.” It is so natural; not a function of economic reality, but perceptions.

Once again, I will describe the evidence on this topic, taking up the key points which may help us reach a logical conclusion.

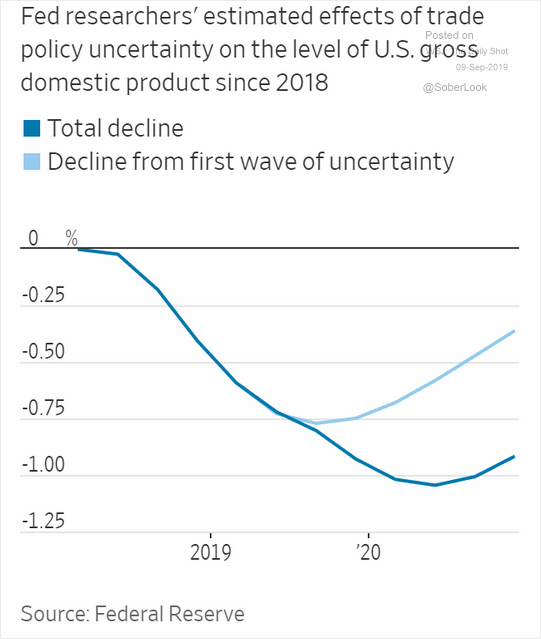

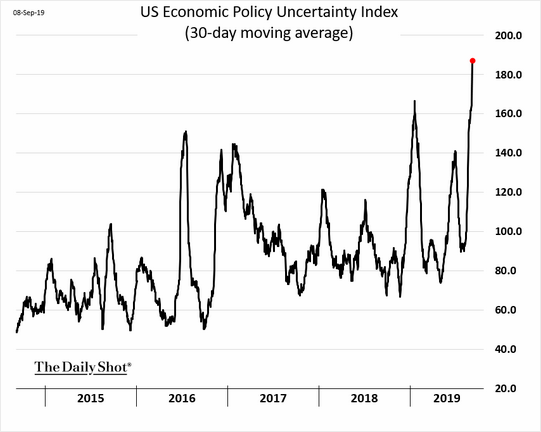

Uncertainty has Increased

Specifically, the rapidly shifting news on trade is weakening the economy because of uncertainty. This is in addition to the direct policy effects.

The uncertainty extends to all economic policy – not just trade.

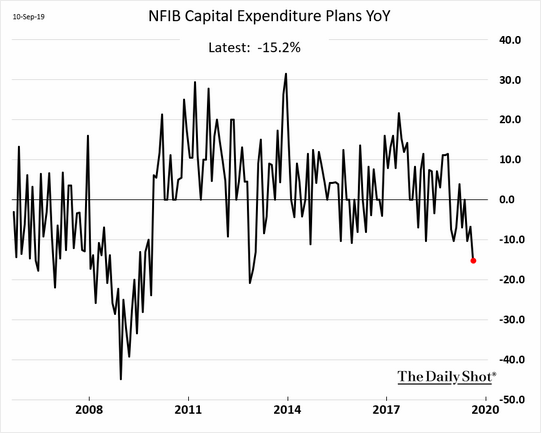

Impact on Business

The effect is showing up in small business capital expenditures.

Effect on Individuals

56% of Americans rate the economy as “excellent or good.” But 60% expect a recession in the next year. (Washington Post-ABC poll)

Perceptions Can Spark a Recession

Robert Shiller draws upon past recessions to conclude that we should look to popular narratives about the economy in identifying the risk. What People Say About the Economy Can Set Off a Recession

New crises that shake up the economy often surprise economists because no exogenous cause appears to be a sufficient explanation for a downturn. People begin to suddenly frame current events in the context of stories they had heard many times before.

This may seem puzzling until we realize that an old narrative has renewed itself in an epidemic, and people have begun to respond reflexively in their day-to-day decisions. If enough people begin to act fearfully, their anxiety can become self-fulfilling, and a recession, sometimes a big one, may follow.

I’ll have my own observations in today’s Final Thought.

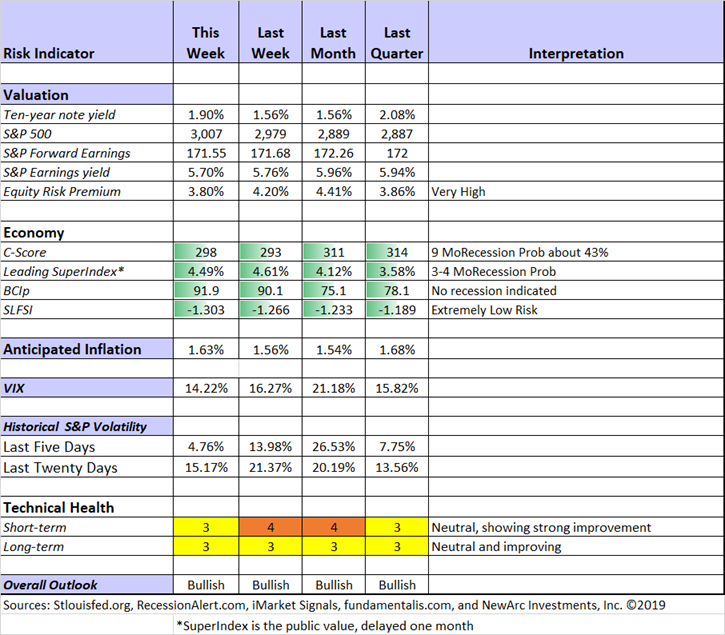

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

Short-term technicals have improved to neutral. Long-term technicals have also stabilized at neutral. Recession risk is still in the “watchful” area with the odds down a notch. We will probably see a higher C-Score next week, reflecting a steepening yield curve. We are seeing little confirmation for the risk signals, which we have been monitoring since May.

Considering all factors, my overall outlook for investors remains bullish.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

RecessionAlert: Strong quantitative indicators for both economic and market analysis

Georg Vrba: Business cycle indicator and market timing tools. The most recent update of Georg’s business cycle index does not signal recession.

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies. This week he provides a good update of the 4-quarter forward estimate – mostly unchanged at 11% growth. He finds this a bit discouraging, but it is better than many expect. That explains why the forward multiple will be so low. I am going to miss the regular lunches with my friend. I hope we can discuss this news before I move away.

Guest Sources

Paul Schatz provides a technical analysis, pointing out that the change in upside and downside volume from August to September.

August saw a number of days where 90% of the volume was on the downside. So close to all-time highs, that’s unusual behavior and signals very little patience among investors and the desire to sell first and ask questions later. In other words, it creates the negativity needed for a market low much sooner than later.

He continues by noting the 80% upside volume days from last week.

David Templeton (HORAN) studies two reports from this week—NFIB and JOLTs – and observes that the recession talk is impacting expectations and sentiment. After a deeper look at the data, he concludes:

This data around the job market represents current activity and not expectations. Based on the JOLTS and the NFIB Survey, it seems the job market is certainly tight/strong. It is difficult to image an economy tipping into a recession with this kind of survey data around the job market. I believe much of the angst for the U.S. economy is being influenced by the commentary or headlines around a potential recession.

“Davidson” (via Todd Sullivan) summarizes the key data from the last ten days, concluding “With economic data like this, there is simply no recession in sight.”

Insight for Traders

Our weekly “Stock Exchange” series is written for traders. I try to separate this from the regular investor advice in WTWA. There is often something interesting for investors, but keep in mind that the trades described are certainly not suitable for everyone.

This week’s edition discusses a crucial topic for both traders and investors—how long to let your winners run. As always, we share some picks including ideas from our new member, Emerald Bay. Pulling it all together and providing counterpoint drawn from fundamental analysis is our regular series editor, Blue Harbinger.

Insight for Investors

Investors should understand and embrace volatility. They should join my delight in a well-documented list of worries. As the worries are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely.

Best of the Week

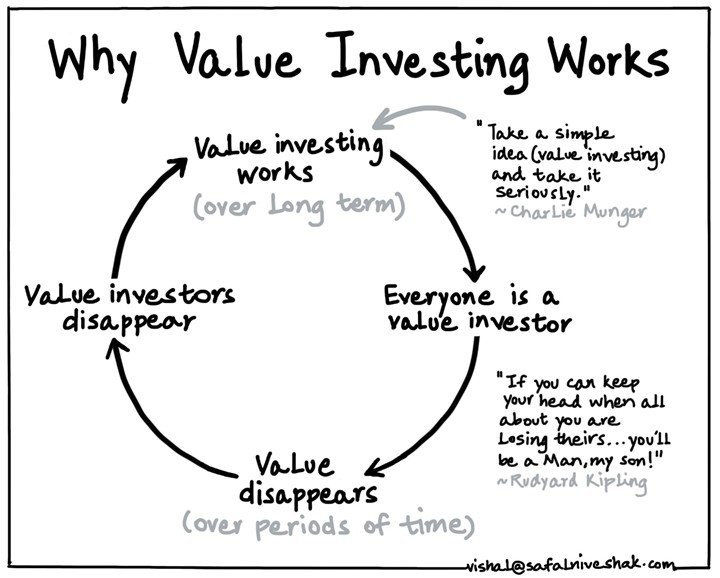

If I had to recommend a single, must-read article for this week, it would be Safal Niveshak’s Why Value Investing Works. The article, drawing upon ideas from famous value practitioners, includes key arguments embracing this theme: The fact that the value approach doesn’t work over periods of time is precisely the reason why it continues to work over the long term.

He then quotes Joel Greenblatt (via Jack Schwager).

It is very difficult to follow a value approach unless you have sufficient confidence in it. In my books and in my classes, I spend a lot of time trying to get people to understand that in aggregate we are buying above-average companies at below-average prices. If that approach makes sense to you, then you will have the confidence to stick with the strategy over the long-term, even when it’s not working. You will give it a chance to work. But the only way you will stick with something that is not working is by understanding what you are doing.

Few have the understanding required. This is not the approach taught in business schools, and it is not instinctive. As I wrote last week, “Investors are an impatient lot. Even when they do not plan to sell assets in the near future, they want the comfort of Mr. Market’s continuing endorsement of their current holdings.”

See today’s Final Thought for more about what to expect when the value approach kicks in.

Stock Ideas

Bank of America’s (BAC) stock is out of favor. Barron’s opines that it is worth betting on.

Chuck Carnevale analyzes two mREITs, finding them unsuitable for retirement accounts. (ANL and DX).

Andrew Hecht analyzes demand factors and the Aramco IPO, concluding that oil services companies are worth a look.

Contrasting takes on AT&T – Positive from Daniel Jones. Not so positive from Stone Fox Capital. With activist Elliott Management involved, will the company adopt a new plan?

Why Home Depot and Lowe’s Can Both Keep Rising Into 2020

Valuation guru Aswath Damodaran provides another great lesson with his analysis of the WeWork IPO.

Personal Finance

Abnormal Returns is the go-to source for anyone serious about the investment business. The Wednesday edition has a special focus on personal finance, with plenty of ideas for the individual investor. As always there are many good links. My favorite this week is Nick Maggiulli’s The Financial Turing Test. Most readers are familiar with the Turing Test, designed to determine whether artificial intelligence has been invented. In this variation your mission is to determine whether someone is a financial expert. He reports some of the 600 Twitter responses he got when asking the one question you would ask to make this determination. The answers range from inquiries about net worth to those about market timing. Maggiulli’s own approach has a Rawlsian quality:

Imagine we could simulate the universe where each time you are born to different set of parents with a different genetic makeup. Sometimes you are born a man. Sometimes you are born a woman. Sometimes black. Sometimes white. Sometimes smart. Sometimes not. Etcetera etcetera. What would you do to have the highest probability of becoming financially secure regardless of your background?

You will enjoy the full post, especially if you think about what your own question might be.

Watch out for…

Anthony Isola continues his hard-hitting analysis of annuities. In The Antonio Brown of Annuities he compares the indexed annuity with the timeshare.

Chesapeake Energy. Daniel Jones describes the warning signs.

Railroads. Barron’s cover story analyzes the tension between declining loads and improving efficiency.

Final Thought

Faced with the typical long list of worries, we rely upon leadership to maintain public confidence.

Confidence is difficult to measure and nearly impossible to predict. Especially in the era of modern communications, news (real or not) can spread rapidly. Compelling narratives go viral. In statistical terms the confidence indicators are mostly coincident. At the moment I sense more of a leading quality in these measures, so I am watching them closely. When we consider the list of institutions we rely upon, the fragility is apparent. How many of these inspire confidence for you?

- President Trump

- Congress

- The Fed

- Business leaders

- British Parliament and PM

- European Central Bankers

- Leaders of “hot spot” countries

- Leaders of countries with nuclear weapons

Whether or not you agree with their specific decisions, leaders need to command respect and support.

Leaders are important, but individuals also have self-confidence. People often worry about major issues while still believing in their own business and prospects. That explains some of the divergences in confidence data.

Rotation Potential

A key investment question, probably a theme coming to this space soon, is whether last week’s rotation can be expected to continue. A few months ago I featured JP Morgan’s ace quantitative strategist. Marko Kolanovic reports that the “flight from momentum is just starting.” (Bloomberg and CNBC).

Kolanovic sees this as the opportunity of the decade, concluding as follows:

“Yesterday’s move was only started by discretionary” portfolio managers, “and will continue with equity quants (that typically operate at lower frequency, e.g. month-end) and fundamental investors,” he wrote. “We believe that the value rotation can continue and the broad market could move higher going into October negotiations, and if real progress is made, continue into a more sustained rally.”

Investment Implications

Investors wanting to profit from the great rotation can do so in simple ways by buying a value or small-cap index. Those wanting to do even better should work harder to isolate the key stocks and sectors within these indexes. There are several pockets of opportunity which I am exploring.

Understanding the market helps in recognizing the future prospects. With comparative valuations so extreme, this “chance of the decade” will not disappear right away. It is not too late to act.

Confidence is the fuel for the economy.

[If your portfolio is loaded with crowded trades, it might be a signal for a checkup. How you did last week is one sign. Write for my free paper, Market Highs. You will get some ideas about replacing over-valued stocks with those showing great potential. We also have a few remaining spots for portfolio consultations – complimentary and without obligation. Just send an email request to info at inclineia dot com].

Some other items on my radar

I’m more worried about:

- Iran confrontations and the chance for an accident.

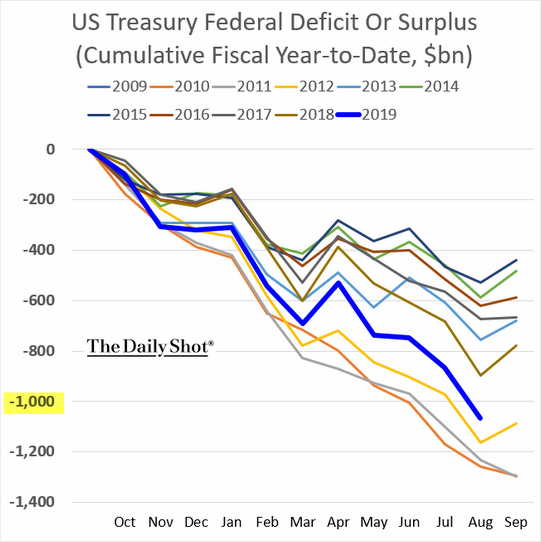

- Federal deficit. Is it time for 50-year bonds? (NYT).

I’m less worried about

- Technical market reactions. Another week of improvement has helped a lot, potentially swinging some active traders to be more bullish.

- Corporate debt. Most of the reliable purveyors of fear speak only of the aggregate amount of debt. EconoFact has a good explanation, acknowledging the basis for the concern as well as factors supporting the increase.

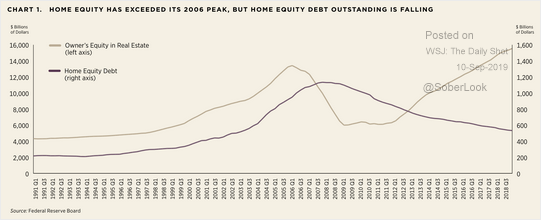

- Home equity debt. Once again, the debt totals alone are often deceptive.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits