Is the Bond Rally Over or is This a Correction in a Downtrend in Treasury Yields?

With interest rates on the 10-year US treasury bond having moved nearly 50bps higher over the last 10 days it is certainly worth asking the question if we’ve seen the low in interest rates or whether this is more of a correction in an ongoing downtrend in rates. In other words, have economic fundamentals been fixed over the last 10 days or is this correction technical in nature? From our perspective, this backup in interest rates appears to be much more the latter than the former. Granted, over the last 10 days or so we’ve seen the beginnings of a deescalation in US-Sino trade relations, the ECB come out all guns blazing with QEfinity, China introduced a few easing measures, and some modestly better US economic data. At the same time, however, it’s important to remember that 1) 2020 will see actual fiscal contraction of about 0.7% of GDP, 2) the impact of announced tariffs will continue to bite in terms of both measurable costs as well as via policy uncertainty, and 3) the US economy is still digesting the lagged effects of monetary tightening from 2016-2018. Those are all items we’ve talked about ad nauseam over the last 12 months as reasons why 10-year treasury yields should work lower until through at least 1Q20.

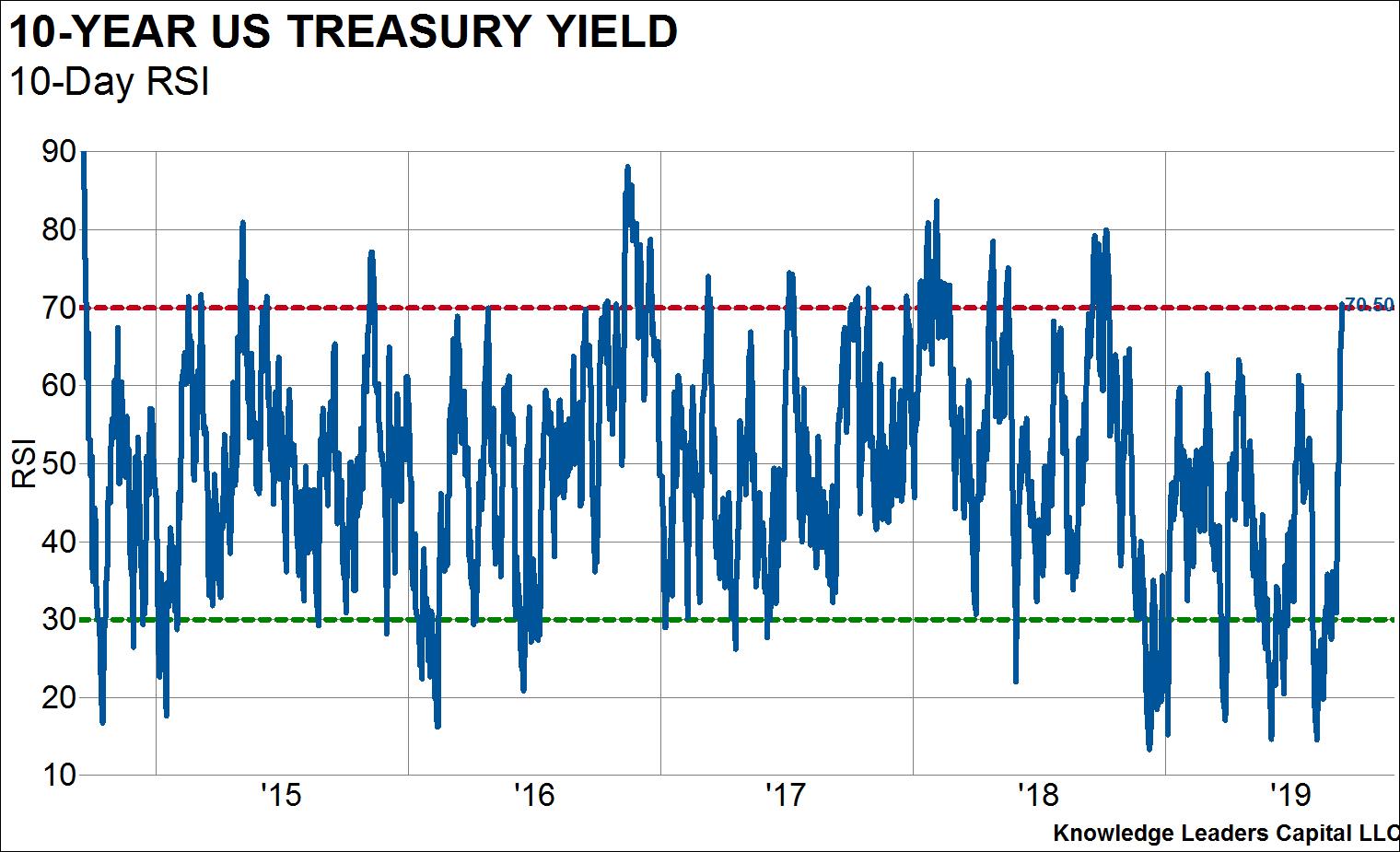

With the fundamentals for lower rates still as much of a “thing” as they were two weeks ago, we are left considering if this aggressive move higher in rates is a technical correction within a longer-term downtrend. After all, interest rates moved extremely fast to the downside once risks for the 2020 outlook became more apparent. The 10-day RSI, a measure of a security’s momentum, reached levels in the teens on multiple occasions during 2019 so far, most recently just a few weeks ago – extreme levels to be sure. But, the RSI for the 10-year treasury bond has since moved to an extreme level in the other direction. As the chart below shows, extreme levels on the RSI are never sustained for a very long period of time.

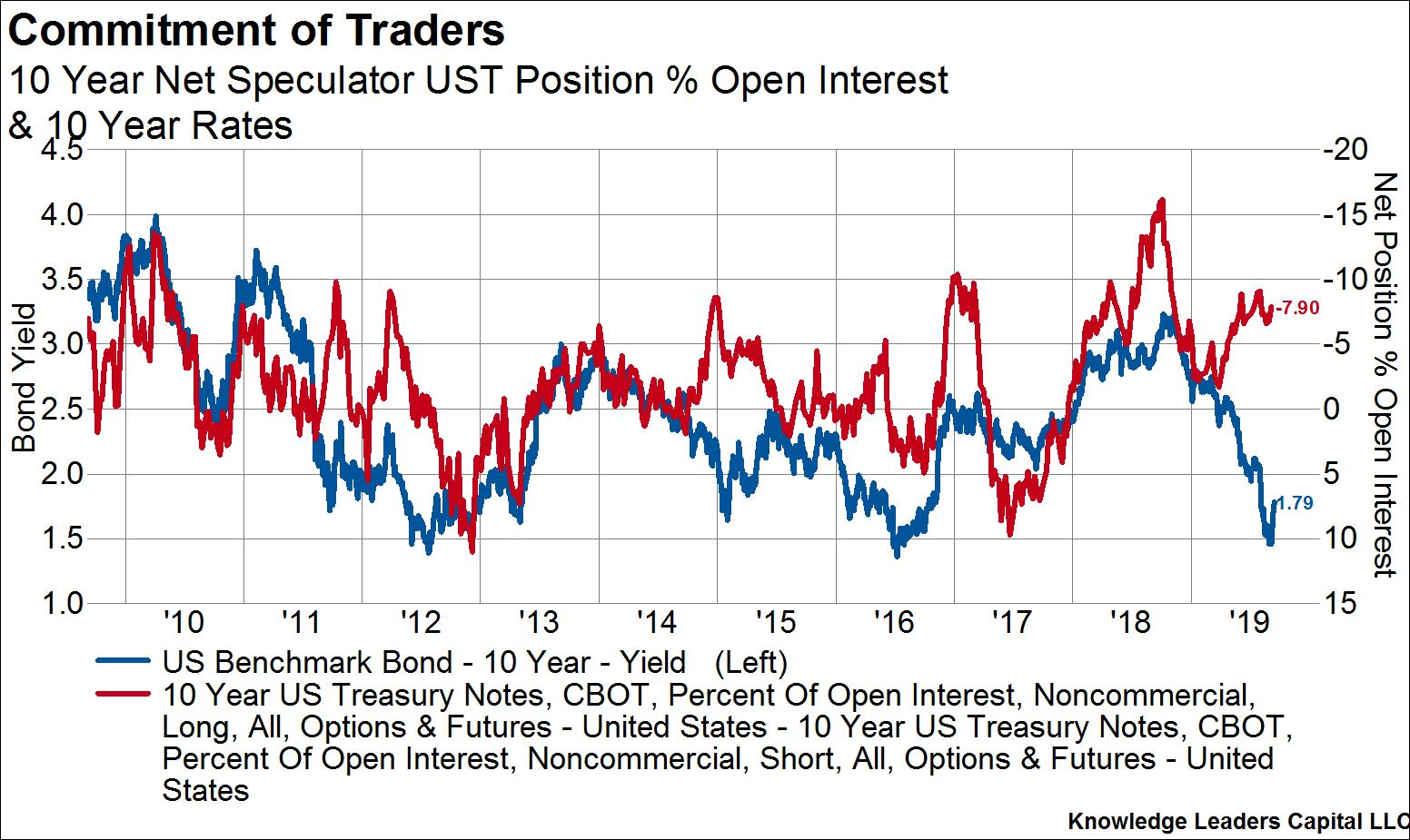

Furthermore, speculative positioning in bonds hasn’t yet gotten to an extreme level. Speculators are typically positioned to benefit from a security’s trend, and thus extreme speculative positioning tends to occur at the late stages of a rally or selloff. For the 10-year bond, lows in yields typically are not hit until speculators become net long in their options and futures bets (see 2010, 2011, 2012, 2013, & 2016). Speculators are still net short of the 10-year bond.