NewsLetter – September 2019

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsNOT SO GOOD NEWS

Financial Literacy Skills Have Taken a Nose Dive Since the Great Recession

“Younger people had the sharpest drop in their ability to answer four of five financial literacy questions correctly…

It’s been a decade since the Great Recession’s upheaval, and while some measures of Americans’ economic well-being have recovered like the unemployment rate, their financial literacy isn’t one of them.

Between 2009 and 2018, there was an 8% slip in the amount of people who could correctly answer most questions about interest rates, inflation, bond prices, financial risk and mortgage rates — from 42% to 34%.

That “clear trend of declining financial literacy” is one of the worrying signals in a three-year study from the FINRA Investor Education Foundation, the educational arm of the nonprofit organization regulating the brokerage industry.”

ARE YOU GOD’S WIFE? A FEW ITEMS TO MAKE YOU SMILE

From Lee

Teacher Debbie Moon’s first graders were discussing a picture of a family One little boy in the picture had a different hair color than the other members. One of her students suggested that he was adopted.

A little girl said, “I know all about adoption — I was adopted …”

“What does it mean to be adopted?” asked another child.

“It means,” said the girl, “that you grew in your mommy’s heart instead of her “tummy !”

************************ *********************

On my way home one day, I stopped to watch a Little League baseball game that was being played in a park near my home. As I sat down behind the bench on the first-base line, I asked one of the boys what the score was.

“We’re behind 14 to nothing,” he answered with a smile.

“Really?” I said. “I have to say, you don’t look very discouraged.”

“Discouraged?” the boy asked with a puzzled look on his face.

“Why should we be discouraged? We haven’t been up to bat yet.”

************************ *********************

An eye witness account from New York City, on a cold day in December some years ago: A little boy, about 10 years old, was standing before a shoe store on the roadway, barefooted, peering through the window, and shivering with cold.

A lady approached the young boy and said, “My, but you’re in such deep thought staring in that window!”

“I was asking God to give me a pair of shoes,” was the boy’s reply.

The lady took him by the hand, went into the store, and asked the clerk to get half a dozen pairs of socks for the boy. She then asked if he could give her a basin of water and a towel. He quickly brought them to her.

She took the little fellow to the back part of the store and, removing her gloves, knelt down, washed his little feet, and dried them with the towel.

By this time, the clerk had returned with the socks. Placing a pair upon the boy’s feet, she purchased him a pair of shoes.

She tied up the remaining pairs of socks and gave them to him. She patted him on the head and said, “No doubt, you will be more comfortable now.”

As she turned to go, the astonished kid caught her by the hand and, looking up into her face with tears in his eyes, asked her:

“Are you God’s wife?”

OH NO!

Lubbock Avalanche-Journal

“What, me worry?”

MAD Magazine leaving the newsstands after 67-year run.

CANNABIS: THE INVESTMENT OF THE FUTURE?

Journal of Financial Planning FPA Survey

22%……….Respondents who say they plan to decrease their use/recommendation of individual stocks over the next 12 months

44% ……. Respondents who say they plan to increase their use/recommendation of ETFs over the next 12 months

55%……… Respondents who say clients have asked about investing in marijuana or cannabis stocks/companies in the past six months.

10……….. Number of states, plus Washington, D.C., that have legalized recreational marijuana over the last few years.

$50 billion. Estimated worth of legal marijuana in the U.S. today.

CAUTIOUS CEOs

Journal of Accountancy

5%………. Portion of CEOs in 2018 who said they expected a drop in the growth of global GDP.

29%…….. Portion who said so in 2019

2012…… The last time they were so pessimistic

OUTLOOK BLEAK FOR US RETIREMENT SAVINGS

InvestmentNews

“Most Americans aren’t financially prepared for retirement.

About 44% of Americans said their retirement savings are not on track, versus 36% who said they are, according to the Federal Reserve Board’s six annual survey of household economics. The rest of Americans aren’t sure whether their plan is on track or not and one-quarter have no retirement savings or pension whatsoever.

RETIREMENT MONEY

Less Than $10,000……. 19%

$10,000-$99,999………. 31%

$100,000-$499,999…… 24%

Over $500,000…………. 12%

Don’t Know ……………. 14%

THE PROBLEM WITH PLUS LOANS

Kiplinger’s Personal Finance

New student loan rates are lower, but parent loans are still no bargain.

COST OF A $31,000 LOAN

FEDERAL STUDENT LOAN…. 4.529% Total Cost…. $38,606

PARENTS PLUS LOAN … 7.079% Total Cost…. $43,344

GOOD LIFE LESSON

One day a school teacher wrote on the board the following:

9×1 = 7

9×2 = 18

9×3 = 27

9×4 = 36

9×5 = 45

9×6 = 54

9×7 = 63

9×8 = 72

9×9 = 81

9×10 = 90

When she was done, she looked to the students and they were all laughing at her because of the first equation, which was wrong, and the teacher said the following”

“I wrote that first one wrong on purpose, because I wanted you to learn something important this was for you to know how the world out there will treat you. You can see that I wrote the RIGHT thing nine times but none of you congratulated me for it but you all laughed and criticize me because of one wrong thing I did.”

So this is the lesson:

The world will never appreciate the good you do a million times but will criticize the one wrong thing you do…. DON’T GET DISCOURAGED. ALWAYS RISE ABOVE ALL THE LAUGHTER AND CRTICISM. STAY STRONG.

SPACE

Texas Monthly

CLIENTS CURIOUS, BUT PLANNERS WARY OF CRYPTO

Journal of Financial Planning – FPA Survey

34%……………… An interesting concept to keep an eye on, but not invest in yet

32%……………… Not a viable investment option

18%……………… A fad that is best avoided

15%……………… A gamble; only worth investing money you can stand to lose

1%………………. A viable investment option that has a place in a portfolio

EYES OF THE BEHOLDER

Planners may not be too fond of crypto but volatility junkies seem pleased. Of course, planners are focused on long-term financial health and it seems many crypto investors are more into entertainment.

Crypto Conference Shows Bitcoin Getting Whole Lot More Fun Again

As little as six months ago, Bitcoin was moribund, with prices languishing at a fifth of their record high, disappointing a mass of cryptocurrency enthusiasts who had grown used to extreme — and often upwards — moves in the virtual currency.

But this week’s Asia Blockchain Summit in Taipei highlighted how volatility is back, reviving the excitement around crypto trading.

“Bitcoin is fun, but it’s a hell of a lot more fun at 100 times leverage,” said Arthur Hayes, the founder and chief executive officer of the exchange BitMEX. “That’s what people want to see in crypto, they want that high volatility,” he said. “At the end of the day, we’re all in the entertainment business of traders.”

HERE’S HOW MUCH YOU NEED TO EARN TO BE IN THE TOP 1%. HINT: IT’S A LOT

USA Today

“The Economic Policy Institute (EPI) published a study that looked at income inequality based on 2017 reported wages, and the results may be surprising. While the top 1% obviously outearn the bottom 90% by a considerable margin, you don’t need to make millions each year to join them. And if you consider yourself relatively well-to-do, you may be in the top 5% or 10% already.

Currently, you need to make a minimum of $421,926 per year to be considered in the top 1%, according to the EPI study. But in this crowd, that’s just scraping by. The average annual income among the top 1% is $718,766, and the top 0.1% earn an average of $2,756,865. By contrast, the bottom 90% make an average of just $36,182…

The 1% income threshold varies by state. In New Mexico, you only need to earn $255,429 to join this elite group, while Connecticut residents need a minimum of $700,800. You can view statistics for every state and region, and the country as a whole, on the EPI website…

While most of us – by definition – will never join the top 1%, joining the top 10% (or even the top 5%) is attainable for those in well-paying fields. You need to make $118,400 to join the top 10% and $195,070 for the top 5%. Again, these figures don’t include investment income, but they give you a baseline.”

https://www.usatoday.com/story/money/2019/07/10/what-you-need-to-earn-to-be-in-the-top-1/39659489/

AH WELL

BRAIN PILLS ARE A BUST – AARP BULLETIN

One in four Americans 50 and older take a supplement for brain health. They are likely flushing dollars down the drain, says a new report by AARP global counsel on brain health…

The study, “The Real Deal On Brain Health Supplements,” says more than $3 billion was spent on memory supplements in 2016, a number that is expected to nearly double by 2023.

“Despite adults’ widespread use of brain health supplements, there appears to be little reason for it,” the study says. “It’s a massive waste of money.”

TRUST ME, THE CHECK IS IN THE MAIL

The fiduciary/suitability debate continues. Having lost to big $$ in the national arena, the fight now moves to state regulation. Recently Massachusetts considered a proposal to apply a state-based common law fiduciary standard to broker-dealers’ and investment advisers’ advisory activities. A consortium of organizations including my Committee for the Fiduciary Standard sent a letter to the state in support of the proposal. Below is an excerpt from the letter highlighting the issue:

Here are just a few examples of firms’ marketing materials supporting the conclusion they function as “trusted advisors.”

- A. Davidson states: “Trust is the cornerstone of the relationship between you, as an investor, and the D.A. Davidson & Co. financial professionals working for you. Your needs should always come first.”

- Mass Mutual states: “Join millions of people who place their confidence and trust in us.”

- Raymond James states: “[I]t’s developing a long-term relationship built on understanding and trust. Your advisor is there for you throughout the planning and investing process, giving you objective and unbiased advice along the way.”

- Schwab states: “A relationship you can trust, close to home.”

- UBS states: “The UBS Wealth Management Americas approach is based on the trusted relationship of our Financial Advisors and their clients. Our experienced Advisors are committed to understanding clients’ needs and delivering insightful, informed advice to help them realize their dreams.”

The harm to investors is immense when they reasonably, but mistakenly, believe they are getting advice that’s in their best interest based on a trusted relationship with their financial professional. In addition to paying higher costs, investors who rely on biased sales recommendations as if they constituted unbiased advice can end up facing unnecessary risks or receiving substandard returns. Cumulatively, these industry practices drain tens of billions of dollars every year out of investors’ pockets and into the pockets of firms and their financial professionals. According to one study, Massachusetts IRA investors alone lose approximately $491 million a year as a result of conflicted advice. The losses are even larger when considering all types of accounts (retirement and non-retirement) and the full range of products sold within these accounts.

Given how broker-dealers advertise and function as advisers in position of trust and confidence with their customers, it is entirely appropriate to apply a common law fiduciary duty to their advisory activities.

If you’d like to see the entire letter, please let me know.

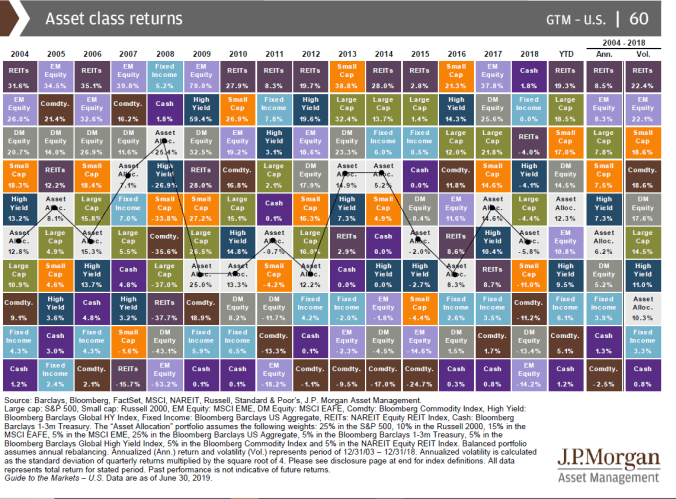

ASSET ALOCATION — SMART, NOT BRILLIANT

From JP Morgan’s most excellent Guide to the Markets 3Q 2019

SOMEONE MUST BE DEADLY AT SCRABBLE

What happens if you rearrange the letters

From my friend Leon

PRESBYTERIAN: BEST IN PRAYER

ASTRONOMER: MOON STARER

DESPERATION: A ROPE ENDS IT

THE EYES: THEY SEE

THE MORSE CODE: HERE COME DOTS

DORMITORY: DIRTY ROOM

ELECTION RESULTS: LIES — LET’S RECOUNT

SNOOZE ALARMS: ALAS! NO MORE Z’S

PICTURES FOR ‘SENIOR’ PEOPLE

From my #1 son. I think he’s trying to rub it in …

WARNING: If you are not a senior, you cannot look at these pictures because you will not understand!

PROTECTING THE LITTLE GUY

InvestmentNews

I sure am pleased to see the government protecting the opportunity for the little guy to invest in private placements. The following are excerpts from two articles in the same issue ofInvestmentNews:

SEC Wants More Access to Private Placements

“The Securities and Exchange Commission is looking for ways to allow more investors to buy unregistered securities and enable emerging companies more easily to raise capital….SEC Chairman J Clayton has pushed open private markets more widely to ordinary investors so they can be in on the ground floor of the launch of breakthrough companies.”

“Alternative investment advocates assert that such products diversify portfolios and offer investors a way to hedge against general market downturns. Investor advocates warned private placements can be highly risky and often harm investors.”

GPB Reports Huge Value Declines

“In a blow to investors, GPB Capital last Friday reported significant losses in the value of its investment funds which are in the form of private partnerships…The two largest GPB Holdings II and GPB Automotive Portfolio, have seen declines in value, respectively, of 25.4% and 39%….GPB’s five other smaller funds reported declines in estimated value of 25% to 73%, according to GPB.

Having served as an expert witness for decades, I’ve seen all too often how investors, particularly smaller investors, have been devastated by investments in exciting sounding private placements that the neither understood nor appreciated the risk. I vote on the side of investor advocates and believe the SEC should also.

MORE PROTECTING THE LITTLE GUY

“In a letter Tuesday, the American Securities Association accused the CFP Board of subverting the authority of the Security and Exchange Commission by holding certification designees to a standard of service beyond what is required by law.”

https://www.wealthmanagement.com/industry/cfp-boards-private-standards-raise-concerns

How awful and presumptuous of the CFP Board to require higher standards of professionals than the abdominally low ones currently required by law. What are regulators thinking of? If I didn’t know better, I’d think it was a joke. Unfortunately, I do know better and it’s not a joke. If you haven’t yet asked your advisor to sign the Committee for Fiduciary Standards Oath, now’s the time.

https://www.advisorperspectives.com/articles/2012/04/17/harold-evensky-s-fiduciary-oath

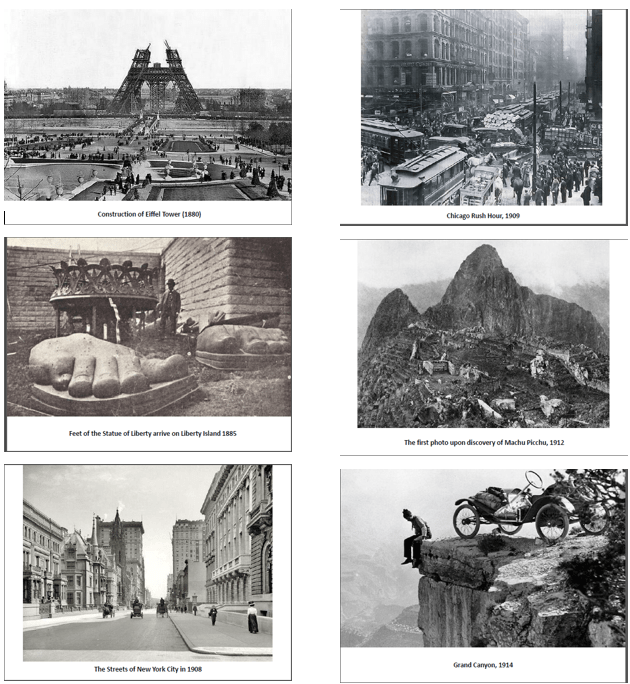

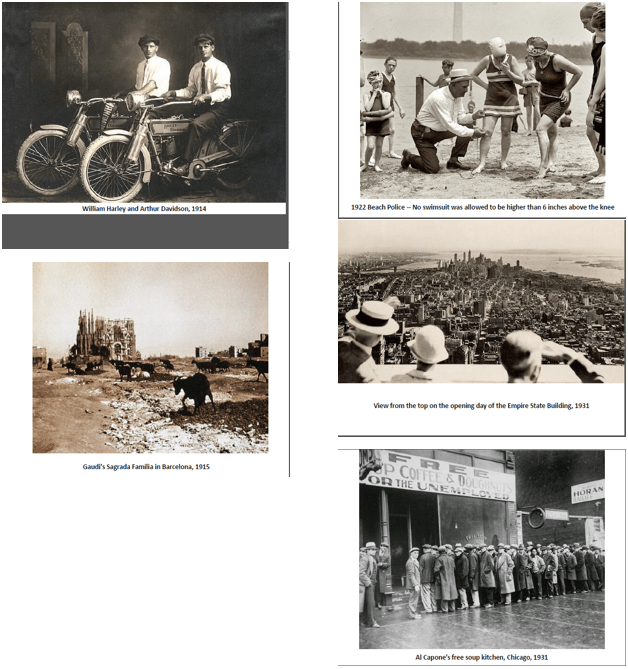

MORE GREAT HISTORICAL PICTURES (AND A FEW REPEATS)

From my friend Judy

WHAT IS THE SIZE OF THE AVERAGE RETIREMENT NEST EGG?

2019 analysis of more than 30 million retirement accounts by Fidelity Investments found that the average balance in corporate-sponsored 401(k) plans at the end of 2018 was $95,600.

https://finance.yahoo.com/m/d84dcdd6-f54b-3db9-ad85-b7b9d3919510/what-is-the-size-of-the.html

TRAGIC NEWS WITH A HAPPY ENDING

Lubbock Avalanche-Journal

“When announcers last July declared Joey Chestnut the winter of Nathan’s Famous hot dog eating contest, spectators had little reason to doubt the score: 64 dogs and 10 minutes.

But the judges, unable to clearly view the contestants’ plates amid all the cups on the table and overwhelmed by the eater’s ability to scarf two or three frankfurters at a time, had undercounted Chestnut by 10 dogs, briefly robbing him of a new world record.

Although judges quickly corrected the score and handed Chestnut his world record, the error caused a small scandal. And it sent organizers of the annual Fourth of July contest scrambling for solutions to avoid a repeat.”

I LOVE LUBBOCK

This was a posting on our neighborhood website around July 4th.

“Ziggy ran from our house. Currently wearing a unicorn costume and an American flag.”

I’ll bet I know why Ziggy ran away. Should be easy to find.

BITCOIN RESEARCHERS WARN OVER POTENTIAL SUDDEN, SHORT PRICE SURGE

Now, new research has found that national holidays and family gatherings could drive interest in buying bitcoin and other cryptocurrencies when the market is already doing well or improving — suggesting we could be set for a new bitcoin boost this Independence Day weekend, but it might not last.

As families and friends gather for Fourth of July celebrations across the U.S., many will be asked the question: “Have you heard of bitcoin?”

Bitcoin and cryptocurrency awareness, something that was harder to measure before bitcoin’s epic 2017 bull run sent the bitcoin price from under $1,000 per bitcoin to almost $20,000 in fewer than 12 months, appears to be closely tied to the bitcoin price, which gets pushed on by so-called fear of missing out (FOMO), according to bitcoin and crypto prime dealer SFOX’s research team.

“Part of the narrative surrounding [the 2017] unprecedented bull run was that many people were hearing about bitcoin for the first time,” the researchers wrote in a blog post. “Over Thanksgiving dinner, the story goes, Luddites in the family would ask the more tech-savvy among them about this ‘bitcoin’ they’d seen in mainstream news — and how could they purchase some ‘bitcoin coins’ for themselves?”

A SOBERING CONCLUSION

For investors who want to pick individual stocks.

“Research from Vanguard, the fund house that invented passive funds, showed investors would capture the best returns in the American stock market by owning more than 500 companies.

The firm tested nine separate portfolios made up of varying numbers of shares: one, five, 10, 15, 30, 50, 100, 200, 500, and found the higher number of shares, the better returns.”

https://www.telegraph.co.uk/investing/funds/perfect-number-stocks-hold-portfolio-think/

HOW TO BE A HIT ON THE BEACH

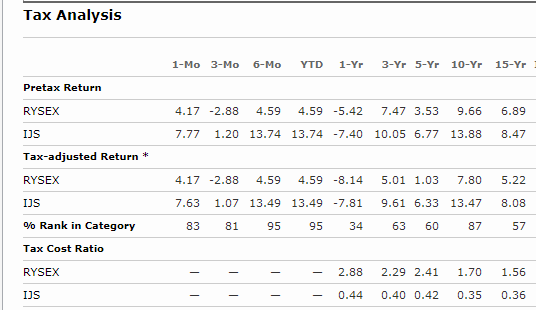

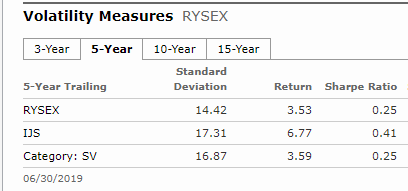

CAVEAT EMPTOR

As much as I like and respect Kiplinger, I remind you that investing based on headlines and good stories is a dangerous strategy. Here’s an example:

Kiplinger Mutual Fund Spotlight

WINNING BY LOSING LESS

“A hefty chunk of cash has helped this small-company fund’s performance.

Cash is always king at Royce Special Equity. Charles Dreifus and Steve Mc Boyle want to have ample funds to snap up shares when they see opportunities. The small-company stock mutual fund typically holds 8% to 10% of its assets and ready money — more than its peers (funds that invest in value-priced small-stocks), which maintain a roughly 3% cash position.”

The article goes on to say, “Overall, the fund’s strategy of winning over time by losing less has earned mixed results. Special equities five-, 10-and 15-year annualized returns, for instance, lag its typical peer and the Russell 2000 index. But the fund has been roughly 15% to 20% less volatile than its peers over those stretches.”

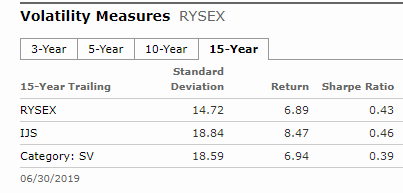

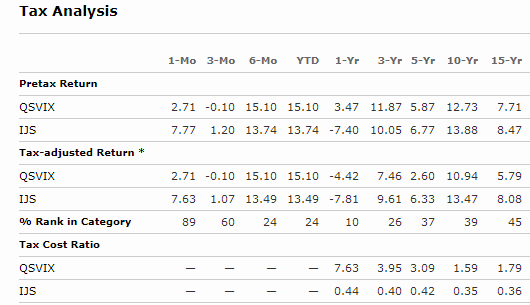

Sounds good, and indeed in 2018 the fund lost about 40% less than its peer universe. However, how did it look over the long term compared to an ETF alternative? For that purpose, I used the iShares S&P Small-Cap 600 Value ETF (IJS), and the answer is, “not so good.”

ROYCE SPECIAL EQUITY INVESTMENT

When taxes are factored in, the results are even more depressing.

How about the risk-adjusted argument? Another “not so good.”

I then looked at the fund ranked number one in the story by Kiplinger for one-year returns. Again, the “winning by losing” rationale was a failure. Add to that the fact that the tenure of the three fund managers was just a shade over a year and a half when the article was published highlights my warning of “buyer beware.”

QUAKER SMALL/MEDIUM IMPACT VALUE

And how about when we factor in taxes?

And of course, all of these statistics are not very meaningful as all of the managers are fairly new.

MANAGER TENURE

Andrew Cowen – 1/12/2018

Thomas Lott – 1/12/2018

Andy Kaufman – 2/01/2019

I’M DEFINITELY GETTING TOO OLD FOR THIS NEW AGE

From American Way Magazine

“Goat yoga is so 2017 … A new class in England’s bucolic Lake district pairs wellness with…lemurs.”

I THOUGHT I WAS AN OPTIMIST

Massachusetts police ask residents to refrain from crime until after the heat wave passes

https://www.cnn.com/2019/07/20/us/police-department-heat-wave-stop-crime-trnd/

POORLY CORRELATED? NOT SO MUCH

JP Morgan’s Guide to the Markets 3Q 2019

Limited correlation benefits with hedge funds and private equity.

OVER CONFIDENCE — BUY LOW, SELL HIGH

From The NBER Digest “How Strongly Do Expectations About Returns Affect Portfolio Choice?”

Based on a study of Vanguard customers (average age 58.7 with and an average of $467,000 invested with Vanguard). “The survey data show that there is a positive relationship between an investor’s expectation of the return in the next year on the stock portfolio and that investor’s portfolio composition… On average, an investor expecting a 1 percentage point increase in return over the next year increases portfolio equity holdings by about 0.7 percentage points.”

REALLY GOOD NEWS!!

“Want to live longer? Drink alcohol, new study says” | USA TODAY

“A recent study of nearly 8,000 men and women aged 78 to 88 suggests that drinking alcohol at an advanced age might actually increase longevity….

Now, in contrast, a paper titled “Alcohol Consumption in Later Life and Mortality in the United States,” just published in the journal Alcoholism: Clinical and Experimental Research, reports that researchers have found consistent associations between occasional and moderate drinking and lower mortality rates, compared to lifetime abstainers.

Occasional drinkers are those who consume alcohol less than one day a week and who, when they do drink, limit intake to three drinks daily for men, two drinks for women. Moderate male drinkers, indulging on one or more days per week, imbibe one to three drinks while females have one to two.”

MOVE OVER MEDITATION

If alcohol doesn’t work, try rage…

“Meditating is one way to reduce stress, pulverizing a porcelain toilet is another — or at least that’s the thinking behind the rise of rage rooms. In the past few years, more than 50 of these facilities have opened around the world, inviting pent-up patrons to pay a fee, put on safety goggles and vandalize their way back to their happy place…”

American Way magazine

CHARTS WORTH PONDERING

From JP Morgan’s always fascinating Guide to the Markets 3Q 2019

WHERE DOES THE TIME GO?

According to the Pew Research Center, which has analyzed the ATU surveys [Bureau of Labor Statistics and its American Time Use Surveys], Americans age 60 and older sleep just over 8½ hours a day, on average. About seven hours are spent on leisure; three hours on chores and errands; a little more than one hour on eating; about one hour on personal activities, such as grooming and health care; and just under an hour on unpaid caregiving and volunteering.

Work remains part of the equation, as well. Men age 60-plus spend two hours a day, on average, on paid work; women age 60-plus spend one hour and 12 minutes.

Looking more closely at leisure, the average person age 60-plus spends the bulk of their leisure time — about 4¼ hours each day — in front of a television, computer, tablet or other electronic device. (That’s an increase of almost 30 minutes in the past decade.) The balance of leisure time is spent, among other activities, on socializing, reading, listening to music, attending events, etc.

https://www.wsj.com/articles/what-people-do-in-retirement-hour-by-hour-11562338744

MORE OLDER THAN DIRT

I have a little “nostalgia” book with “Remember When” for my birthday year — 1942

World News: Lieutenant Cornel Doolittle leads a bombing group over Tokyo.

National News: The Manhattan Project begins; zoot suits are a fashion statement for men; Kellogg’s Raisin Bran and instant coffee introduced.

Life Expectancy: 62.9 years

Cost of Living: New house: $3,775; new car: $920; average income: $1,885/year; movie ticket: 30 cents; gas: 15 cents; bread: 9 cents/loaf

1942 Birthdays: Wayne Newton, Annette Funicello, Harrison Ford, Muhammad Ali, Aretha Franklin, Sandra Dee, Barbara Streisand, Tammy Wynette

Movies: Casablanca, Bambi, Mrs. Miniver

Music: Jingle, Jangle, Jingle; White Christmas; Deep in the Heart of Texas [Yes!]

INVESTORS IMPERILED?

AARP says new SEC rule fails to protect retirees. AARP BULLETIN

“Investing for retirement will be less safe and more confusing under a new Securities and Exchange Commission regulation governing the actions of stockbrokers and investment advisors, AARP and others say… . The new regulation best interest rule, adopted 3-1 in June by the SEC commissioners, doesn’t protect investors, critics say. Under the rule, no one is required to offer advice or recommendations that put the interest of investors first, AARP and other critics say. ‘As a result, conflicts will continue to taint the advice American investors received from brokers,’ says SEC Commissioner Robert Jackson Junior, the dissenting vote.

AARP agrees. ‘This rule will have a negative impact on the ability of Americans to save and invest for retirement,’ says Nancy LeaMond, AARP’s Executive Vice President and Chief Advocacy and engagement officer.”

Seems I have good company with my frustration regarding the new SEC regulation.

THE PENSION CRISIS AT CONGRESS’ DOOR

AARP BULLETIN

Pensions that have been cut or approved for cuts……………………………………..…… 90,000

Workers and retirees whose plans are expected to run out of money…………..1,300,000

POLICE HUMOR

From my friend Alex

ONE MORE ‘DIG DEEPER’

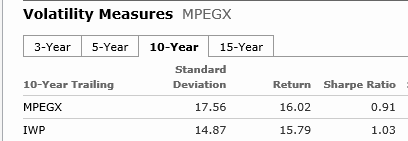

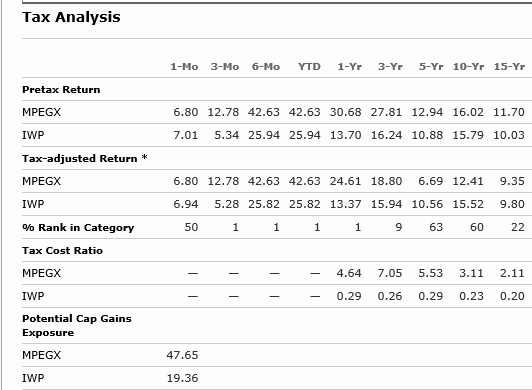

AND THE NO. 1 STOCK FUND MANAGER IS…

Wall Street Journal

“The winner: Dennis Lynch, head of the Counterpoint Global team at Morgan Stanley Investment Management and manager of Morgan Stanley Institutional Discovery Portfolio (MPEGX) — which romped across the finish line with a 30.8% return for the trailing 12 months ended June 30.”

https://www.wsj.com/articles/and-the-no-1-stock-fund-manager-is-11562638561?mod=flipboard

IWP is the iShare Russell Mid Cap Growth

A WORD OF WARNING FROM KIPLINGER’S

Although I’m a user of Angie’s List, Kiplinger’s says to take the recommendations with a grain of salt.

“Angie’s List was founded in 1995 to help consumers pick reliable home-service providers. But in 2017 when it was bought by the same company that owns homeadvisor.com, it changed the way it does business. Now, instead of charging an annual fee, Angie’s List is free — it’s funded almost entirely by advertising and referral fees from the companies it evaluates. A recent report from the nonprofit Consumer Federation of America (www.consumerfed.org) explains how that arrangement undermines the usefulness of the ratings and the ‘short list of top-rated pros’ users receive.

CFA recommends that if you use Angie’s List read the detailed consumer comments for A-rated businesses with at least 25 comments, and pay extra attention to comments that are negative…. Always double-check a pro’s reputation with the Better Business Bureau (www.bbb.org), ask to see proof of licensing and insurance, and check references.”

PONDERISMS

From my special friend Patti

- Why do peanuts float in a regular Coke and sink in a Diet Coke? Go ahead and try it.

- Why do you have to “put your two cents in” but it’s only a “penny for your thoughts?” Where’s that extra penny going?

- What disease did cured ham actually have?

- How is it that we put man on the moon before we figured out it would be a good idea to put wheels on luggage?

- Why is it that people say they “slept like a baby” when babies wake up like every two hours?

- Why are you IN a movie, but you’re ON TV?

- Why do toasters always have a setting that burns the toast to a horrible crisp, which no decent human being would eat?

- Why do the Alphabet song and Twinkle, Twinkle Little Star have the same tune?

- Why did you just try singing the two songs above?

- How did the man who made the first clock know what time it was?

POT CALLING THE KETTLE BLACK?

Don’t Listen to Your Market Guru

In his Real Money column Tuesday morning, Cramer had some advice for investors who are listening to market pundits and basing their stock picks or trades off of them. Cramer’s take? Make up your own mind.

Here’s a snippet of what Cramer has to say about those who are following the words of a market pundit. “I am simply saying that once again we listened to a guru — a word I hate — and the guru was full of sound and fury but signifying nothing having to do with the stock market.”

UNCLE HAROLD’S BARN GOOD CHIPS

They’re not just good, they’re GREAT! (sorry, no sample)

UPSIDE DOWN

A Danish bank is offering mortgages at a 0.5% negative interest rate — meaning it is basically paying people to borrow money

“Jyske Bank, Denmark’s third-largest bank, said this week that customers would now be able to take out a 10-year fixed-rate mortgage with an interest rate of -0.5%, meaning customers will pay back less than the amount they borrowed…Many investors fear a substantial crash in the near future. As such, some banks are willing to lend money at negative rates, accepting a small loss rather than risking a bigger loss by lending money at higher rates that customers cannot meet.”

https://www.businessinsider.com/danish-bank-offers-mortgages-at-negative-interest-rates-2019-8

MORE OLD PICTURES

If you’re old enough to remember who these people are – from Peter

Hope you enjoyed this issue, and I look forward to “seeing you” again.

Harold Evensky

Chairman

Evensky & Katz / Foldes Financial Wealth Management

IMPORTANT DISCLOSURE

PLEASE REMEMBER THAT PAST PERFORMANCE MAY NOT BE INDICATIVE OF FUTURE RESULTS. DIFFERENT TYPES OF INVESTMENTS INVOLVE VARYING DEGREES OF RISK, AND THERE CAN BE NO ASSURANCE THAT THE FUTURE PERFORMANCE OF ANY SPECIFIC INVESTMENT, INVESTMENT STRATEGY, OR PRODUCT (INCLUDING THE INVESTMENTS AND/OR INVESTMENT STRATEGIES RECOMMENDED OR UNDERTAKEN BY EVENSKY & KATZ / FOLDES FINANCIAL WEALTH MANAGEMENT (“EK-FF”), OR ANY NON-INVESTMENT-RELATED CONTENT, MADE REFERENCE TO DIRECTLY OR INDIRECTLY IN THIS NEWSLETTER WILL BE PROFITABLE, EQUAL ANY CORRESPONDING INDICATED HISTORICAL PERFORMANCE LEVEL(S), BE SUITABLE FOR YOUR PORTFOLIO OR INDIVIDUAL SITUATION, OR PROVE SUCCESSFUL. DUE TO VARIOUS FACTORS, INCLUDING CHANGING MARKET CONDITIONS AND/OR APPLICABLE LAWS, THE CONTENT MAY NO LONGER BE REFLECTIVE OF CURRENT OPINIONS OR POSITIONS. MOREOVER, YOU SHOULD NOT ASSUME THAT ANY DISCUSSION OR INFORMATION CONTAINED IN THIS NEWSLETTER SERVES AS THE RECEIPT OF, OR AS A SUBSTITUTE FOR, PERSONALIZED INVESTMENT ADVICE FROM EK-FF. TO THE EXTENT THAT A READER HAS ANY QUESTIONS REGARDING THE APPLICABILITY OF ANY SPECIFIC ISSUE DISCUSSED ABOVE TO HIS/HER INDIVIDUAL SITUATION, HE/SHE IS ENCOURAGED TO CONSULT WITH THE PROFESSIONAL ADVISOR OF HIS/HER CHOOSING. EK-FF IS NEITHER A LAW FIRM, NOR A CERTIFIED PUBLIC ACCOUNTING FIRM, AND NO PORTION OF THE NEWSLETTER CONTENT SHOULD BE CONSTRUED AS LEGAL OR ACCOUNTING ADVICE. A COPY OF EK-FF’S CURRENT WRITTEN DISCLOSURE BROCHURE DISCUSSING OUR ADVISORY SERVICES AND FEES IS AVAILABLE UPON REQUEST. PLEASE NOTE: IF YOU ARE AN EK-FF CLIENT, PLEASE REMEMBER TO CONTACT EK-FF, IN WRITING, IF THERE ARE ANY CHANGES IN YOUR PERSONAL/FINANCIAL SITUATION OR INVESTMENT OBJECTIVES FOR THE PURPOSE OF REVIEWING/EVALUATING/REVISING OUR PREVIOUS RECOMMENDATIONS AND/OR SERVICES, OR IF YOU WOULD LIKE TO IMPOSE, ADD, OR TO MODIFY ANY REASONABLE RESTRICTIONS TO OUR INVESTMENT ADVISORY SERVICES. EK-FF SHALL CONTINUE TO RELY ON THE ACCURACY OF INFORMATION THAT YOU HAVE PROVIDED.

© Evensky & Katz / Foldes Financial Wealth Management

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits