Over the last few days investors have been given a good amount of information to digest from incoming economic data, Federal Reserve meting minutes, and Fed speakers opining about monetary policy at the annual Jackson Hole conference. Even still, everyone is waiting on THE speech from Fed Chairman Powell tomorrow to set to the expectations for the Fed’s upcoming meeting in mid-September. It’s clear from both the Fed meeting minutes as well as recent comments by Fed officials that there is no consensus for additional easing in September, let alone a 50 basis point cut in rates. Indeed, below are excerpts from three Fed speakers over the last few days, all suggesting no keen desire for more rate cuts.

Fed Rosengren: “We’re likely to have a second half of the year that’s much closer to 2% growth…I’m not saying there are not circumstances in which I’d be willing to ease. I just want to see evidence we are going into something that is more a slowdown.”

Fed Harker: “We’re roughly where neutral is. It’s hard to know exactly where neutral is, but I think we’re roughly where neutral is right now. And I think we should stay here for a while and see how things play out.”

Fed George: “We’re at a sort of equilibrium right now and I’d be happy to leave rates here absent seeing either some weakness or some strengthening, some kind of upside risk that would cause me to think rates should be somewhere else…I don’t yet see the signal that suggests it is time to get worried about a downturn…[a rate cut] is not required in my view.”

The market, on the other hand, continues to price in a 100% probability of easing in September, a two in three chance of more easing still at the October meeting, and a better than even chance of a third cut by January, 2020. Clearly there is a disconnect – a disconnect that in our view is getting harder and harder for the Fed to justify based on incoming data.

Indeed, over the last week or so we’ve seen:

- Aggregate US corporate profits revised lower by $200bn

- Payroll employment revised down by 500K from April 2018-March 2019

- Industrial production decline MoM and miss expectations

- Capacity utilization decline MoM and miss expectations

- Consumer sentiment decline MoM and miss expectations

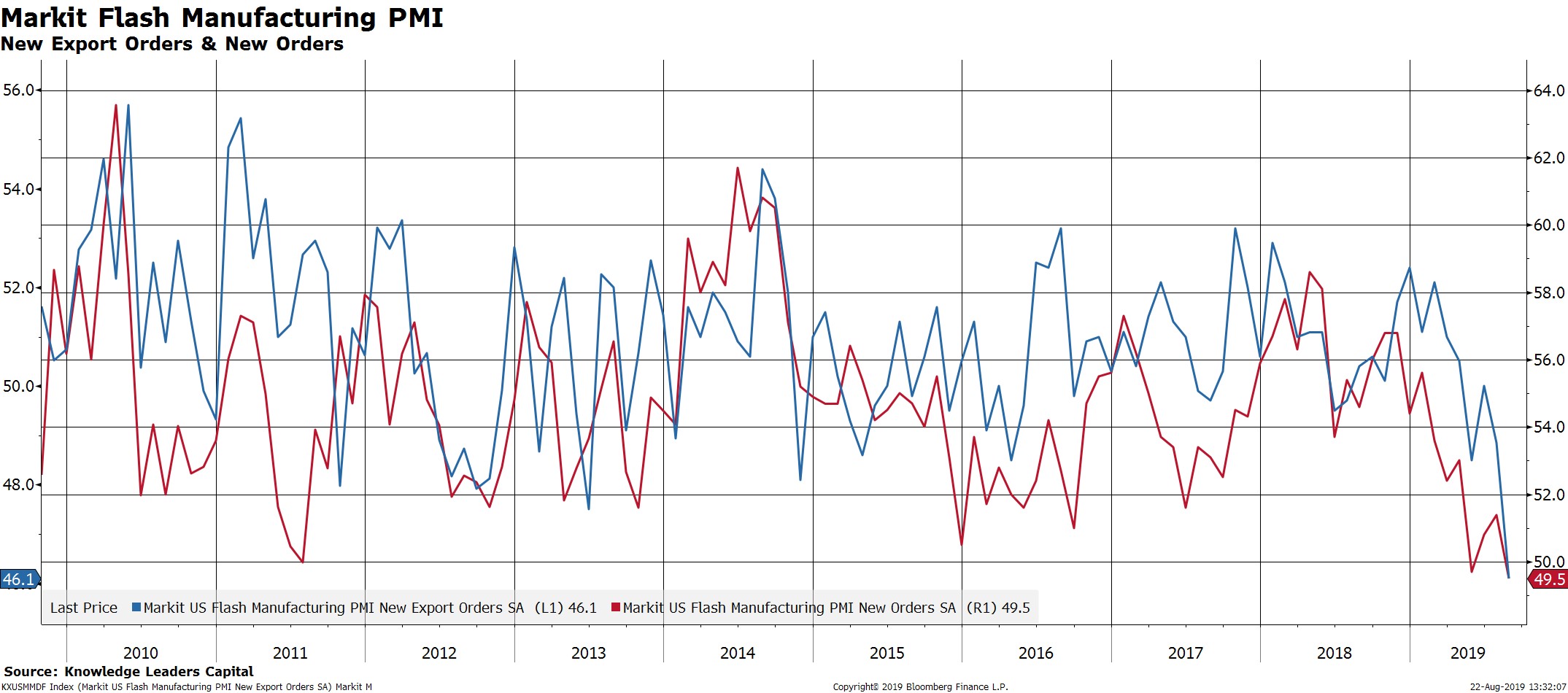

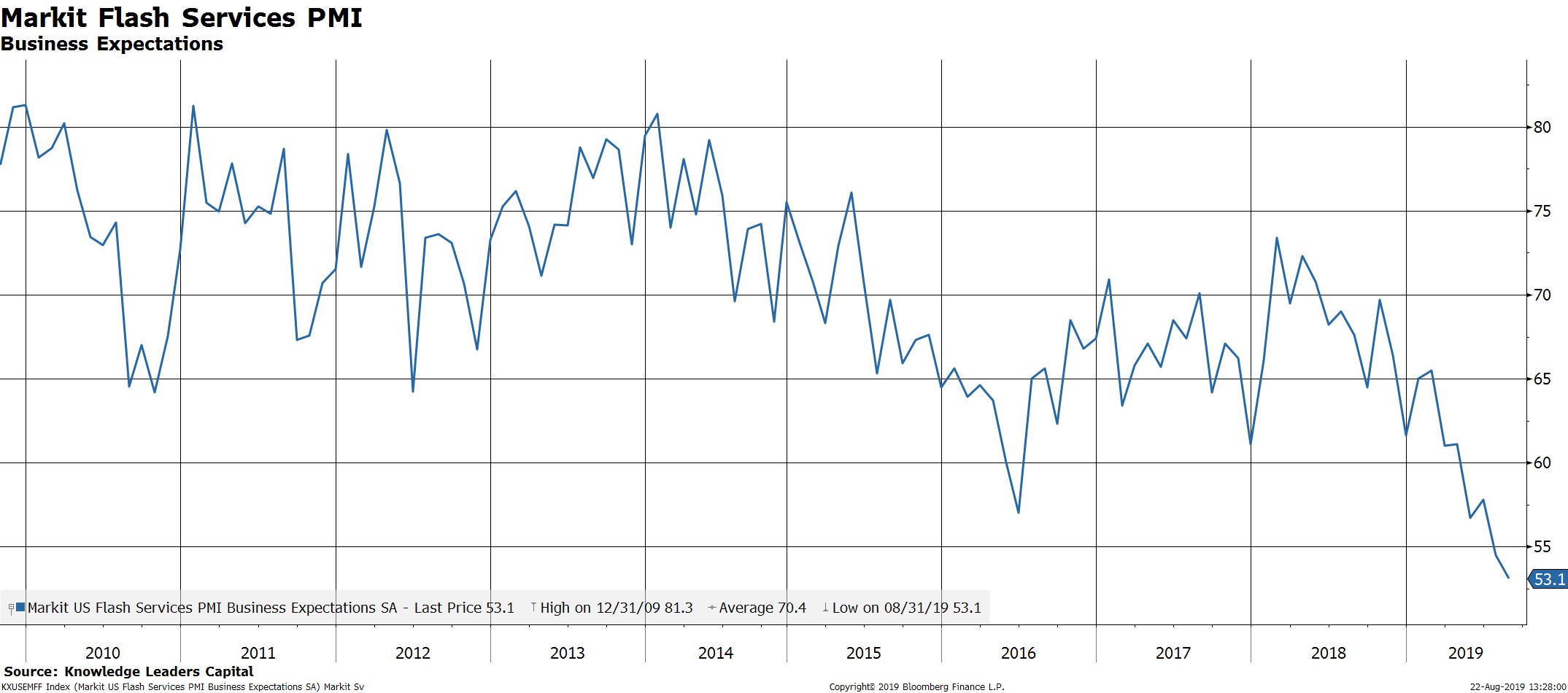

- Markit manufacturing and service sector PMIs decline MoM and miss expectations

It’s true that not all the econ data is coming in on the weak side. Importantly, retail sales came in higher than expectations thanks to Prime Day, housing data is mixed and initial unemployment claims have remained low. But we must remember that those data tend to be lagging in nature. More concerning is how the leading components of business surveys like the Markit survey are coming in at the lowest levels on record. On the manufacturing side, new export orders and new orders are in contraction and plunging. Worryingly, the weakness in manufacturing appears to be bleeding into services as service business expectations are also at new historic lows and plunging.

No wonder the market is pricing in three more 25bps rate cuts over the next five months. And regardless of Fed speakers so far this week, logic points to the Fed being more rather than less aggressive. After all, as we see it the Fed basically has two high probability options at this point. Option A is to sit tight, perhaps dribble in another “mid-cycle” cut over the next several months and see how the data evolve. This is the option that George, Harker and Rosengren would most likely support. Option B is to cut rates in September and signal at least two additional 25bps cuts by January, thereby meeting the market’s expectations.

The relative downside of Option A looks increasingly large compared to Option B. If the hawks win out and Option A prevails, the risks to a further slowdown/recession would increase in our view given the message from the leading economic data. This case would all but guarantee the eventuality of a 0% Fed Funds rate and possibly more quantitative easing. If they opt for Option B then perhaps a deeper slowdown/recession is avoided, which would allow the Fed to hold the policy rate at a relatively higher level. The worst case for Option B is that they end up in the same place as the Option A, with a policy rate of 0% and QE on the table, except that the lags from the easing campaign would have been less.

Of course, there are risks to option A including inflating a financial asset bubble, but the opposite is also true as we saw last December when Chair Powell told the world the Fed’s balance sheet was on “auto pilot”. Regardless, no matter how you slice it either policy option would seem to support bonds and gold, while only one option (Option B) would also support equities.

In our view, Option A would tend to result in lower inflation and growth expectations, bringing down the long end of the Treasury curve while pinning down the short end of the curve, thereby exacerbating the 10Y-3M and 10Y-2Y inversions. Falling long-term real rates would likely put a floor on gold prices even if the US dollar broke to new highs. Equities would likely struggle on the back of falling growth and inflation expectations.

Options B would tend to steepen the curve in our view by bringing down the short end faster than the long end. Long-term rates would face relatively limited upside thanks to falling term premiums that result from policy easing, and possibly significantly more downside. Still negative real rates would support gold prices and relative policy easing would tend to weaken the US dollar. Equities would be supported if inflation and/or growth expectations rose.

Given the circumstances outlined above of clear economic slowing with downside risks, the case for aggressive Fed easing has become quite a bit easier to make while the relative risks of the “mid-cycle” status quo have become greater. Either option is likely to be eventually quite supportive of bonds and gold while only the dovish option is likely to support stock prices.

© Knowledge Leaders Capital

© Knowledge Leaders Capital

More Factor-Based Investing Topics >