Protect Your Wealth Against the Law of Unintended Consequences

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Friendship. Liberty. Hope.

These are among the cruelly ironic names given to ships involved in the transatlantic slave trade, if you can believe it. Giving the vessels agreeable names helped obscure the terrible truth of slavery and no doubt eased the consciences of captains and crewmembers alike.

Today, lawmakers often follow the same tactic when they give cute names to legislation that was well-intentioned but had unintended consequences.

Think of the “Patient Protection and Affordable Care Act.” Or the “U.S.A. PATRIOT Act.”

The word “patriot” carries such strong connotations for Americans. Who would deny being a patriot?

And yet the PATRIOT Act, signed into law following the September 11 terrorist attacks, has a decidedly rocky past. Intended to strengthen national security, it’s been criticized for having a number of negative repercussions, including serious privacy violations, guilt by association and much more.

“A rose by any other name would smell as sweet,” Shakespeare writes. Conversely, a law with a great name doesn’t hide that it may not have been carefully considered.

The law may perhaps be even more suspect when it’s given a boring, almost clinical name. The Department of Labor’s (DOL) “Fiduciary Rule” and the “Recourse Rule” both come to mind.

The Law of Unintended Consequences

I called the Fiduciary Rule one of the costliest financial regulations of the past 20 years. Meant to protect investors from nosebleed fees and advisors’ conflicts of interest, the rule may end up costing investors in the long run. A “cheaper is always better” attitude will surely exclude many smaller funds, ultimately giving retail investors fewer choices. Although the rule died in court last year, the DOL is expected to unveil a new version by the end of the year.

And then there’s the Recourse Rule. The little-known rule, enacted in 2001, is now widely believed to be partly responsible for the financial crisis that began in August 2007. I won’t get into the full details of what the rule did. In short, it changed banks’ capital requirements. Holding individual mortgages was given a greater risk-weight than highly-rated mortgage-backed securities (MBS), and so banks, trying to sidestep the additional capital requirements, securitized the loans—many of them “non-prime”—to which rating agencies gave the coveted AA- or AAA rating.

Those who’ve read Michael Lewis’ fabulous account of the housing bubble, The Big Short, or seen the Academy Award-winning film of the same name, know how this turned out for lenders—and, consequently, the world economy.

Over-regulation, then—as opposed to under-regulation—may have been the root cause of the worst economic crisis since the Great Depression.

“They’re Not Sending Their Best”

Adding insult to injury, it appears that some of these well-intentioned but ill-conceived rules and laws were imported directly from other parts of the world, particularly the European Union (EU). The Fiduciary Rule is a near-exact replica of the EU’s Markets in Financial Instruments Directive (MiFID II). The Recourse Rule was basically an addendum to Basel I, 1988’s series of banking regulations agreed upon by central bankers from around the world.

“Harmonization” is the word used to describe the process of normalizing regulations across country borders. Even this is sweetly named and well-intentioned—it’s meant to reduce redundancies and conflicting standards—but it has the chilly effect of placing domestic affairs under the purview of socialist bureaucrats in Brussels.

This is precisely the reason why some people vehemently oppose globalization. It’s precisely why the United Kingdom voted to leave the EU, why the American people elected Donald J. Trump.

“They’re not sending their best,” Trump famously said four years ago when he launched his presidential run. Of course he was referring to illegal immigrants, but he may as well have been speaking of the socialist policies the U.S. has adopted from the international community in past years.

Inflation Is Starting to Pick Up

My reason for bringing all of this up is to stress the importance of protecting your wealth, and your family’s wealth, against the law of unintended consequences. That’s why I have for years recommended that investors follow the 10 Percent Golden Rule. Gold has little to no correlation with stocks, making it an exceptional, time-tested diversifier when there’s market uncertainty. A 10 percent allocation, split between physical gold and gold mining stocks, is a rational way to the hedge against multiple headwinds right now, many of them sparked by poor government policies.

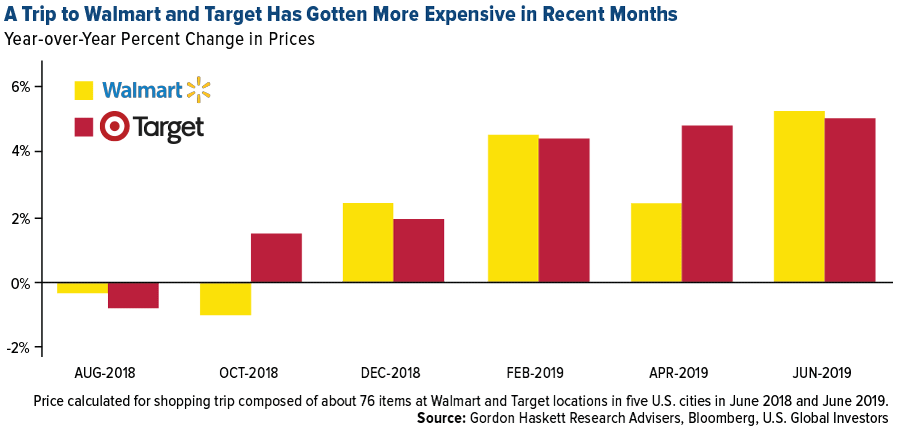

And yes, that includes trade tariffs. More than a year after the start of the U.S.-China trade war, we’re starting to see consumer prices increase. Tariffs are like taxes. Core inflation, which excludes food and energy, rose to a six-month high of 2.2 percent year-over-year in July. In the chart below, you can see that average inflation since the trade war started in March 2018 is higher than it was in the months prior.

This data becomes more tangible when you look at changes in price at specific stores. According to Gordon Haskett Research Advisers, a trip to Walmart or Target in June was nearly 5 percent more expensive than it was a year ago. That might not sound like much, but because of Walmart’s reputation of having low prices, even a slight bump up could be enough to prompt some shoppers to turn to deep-discount retailers like Dollar General, Gordon Haskett analysts say.

Pool of Negative-Yielding Debt Hits $16 Trillion

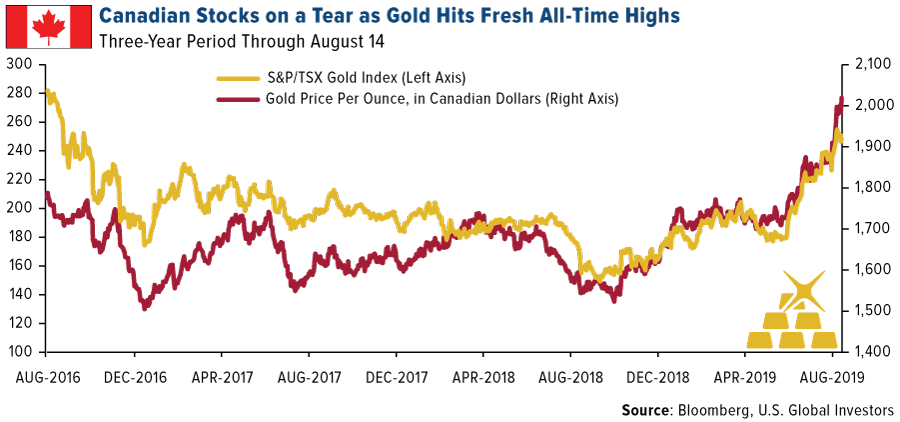

As I’ve pointed out before, inflation has been very constructive for the price of gold. With yields around the world falling deeper and deeper into negative territory, the yellow metal has hit new all-time highs in a number of currencies.

That includes the Canadian dollar, which is incredible news for the country’s massive metals and mining industry. Canada is the number five gold producer in the world behind the U.S., and nearly 60 percent of all global mining financings are done on either the Toronto Stock Exchange (TSX) or TSV Venture Exchange. In 2017, about 56 billion mining shares were traded in Canada, for a total value of C$206 billion. Last month, I highlighted several junior, mostly-Canadian miners that have made some monster moves lately thanks to higher metal prices in the local currency.

So will gold hit an all-time high in U.S. dollars? Already some analysts are making forecasts for $2,000 an ounce gold.

Speaking to CNBC this week, Daniel Ghali, a TD Securities commodities trader, said that as the pool of negative-yielding debt expands, “I could see a case for gold at $2,000.”

I could see this happening as well, especially if nominal Treasury yields turned negative. That’s no longer an absurd notion, says PIMCO’s global economic advisor, Joachim Fels. This week former Federal Reserve Chairman Alan Greenspan echoed that sentiment, telling Bloomberg that there’s “no barrier for U.S. Treasury yields going below zero. Zero has no meaning, besides being a certain level.”

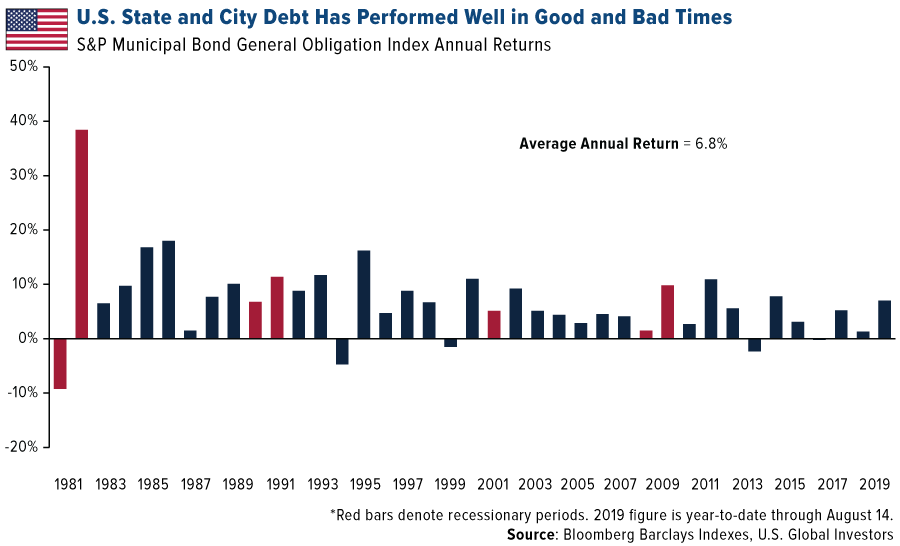

Municipal Bond Investors Won Big in Last Downturn

Besides gold, municipal bonds are highly sought by investors right now due to their history of steady performance in good as well as bad times. Look at the chart below. State and local debt was up in most years going back to 1981, when during recessional years. Over the past 38 years, munis have delivered an impressive average annual return of 6.8 percent.

It’s no surprise, then, that inflows into muni bond mutual funds have done so well this year.

Investments were up 58 percent in the week ended August 7, for the 31st straight week of positive flows, according to the Investment Company Institute (ICI). Year-to-date, investors have added a whopping $58.3 billion to funds that invest in munis. Remember to follow the money!

Curious to know what’s next for gold? Check out my latest Frank Talk Live! episode by clicking here!

Gold Market

This week spot gold closed at $1,513.38, up $21.07 per ounce, or 1.41 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 3.18 percent. The S&P/TSX Venture Index came in off 3.78 percent. The U.S. Trade-Weighted Dollar rose 0.73 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Aug-13 | Germany CPI YoY | 1.7% | 1.7% | 1.7% |

| Aug-13 | Germany ZEW Survey Current Situation | -6.3 | -13.5 | -1.1 |

| Aug-13 | Germany ZEW Survey Expectations | -28.0 | -44.1 | -24.5 |

| Aug-13 | CPI YoY | 1.7% | 1.8% | 1.6% |

| Aug-13 | China Retails Sales YoY | 8.6% | 7.6% | 9.8% |

| Aug-15 | Initial Jobless Claims | 212k | 220k | 211k |

| Aug-16 | Housing Starts | 1256k | 1191k | 1241k |

| Aug-19 | Eurozone CPI Core YoY | 0.9% | -- | 0.9% |

| Aug-22 | Initial Jobless Claims | 216k | -- | 220k |

| Aug-23 | New Home Sales | 644k | -- | 646 |

Strengths

- The best performing metal this week was palladium, up 1.88 percent, despite hedge funds cutting their net bullish positions to a 10-week low. Gold bulls outnumbered the bears in the weekly Bloomberg survey of traders and analysts for a second week as the metal notches a third weekly gain. Bullish respondents say the turmoil in global equity and bond markets is strengthening the investment case for gold. Silver is also rallying alongside gold on recession fears. The core consumer price index (CPI) rose 0.3 percent in July from the prior month, which is historically positive for the yellow metal.

- A growing number of data points support another rate cut from the Federal Reserve next month as insurance against a global slowdown, writes Bloomberg’s Steve Matthews. Deutche Bank analyst Benjamin Fisher says that positioning is not stretched in gold equities, which means that there is alpha opportunity.

- As the U.S.-China trade war moves into a currency war as well, demand for gold is skyrocketing as a perceived safe haven asset. Whitney George, president of Sprott Inc., says “gold is a currency, but it’s nobody’s obligation, so it will stand tallest when everyone else is trying to debase their currency to be competitive globally.”

Weaknesses

- The worst performing metal this week was platinum, down 1.31 percent. Friday marked the seven-year mark since the Marikana Massacre when 34 miners were shot dead by police during a protest at Lonmin’s Markikana platinum mine. Retailers jumped, and gold plunged, after the Trump administration announced a delay until mid-December for the 10 percent tariff on some Chinese goods. Demand for gold as a safe haven was dampened on the news, but then recovered later in the week. According to data compiled by Bloomberg, the SPDR Gold Shares ETF saw almost $523 million of outflows on Tuesday after the news, the biggest one-day decrease since 2016.

- Morgan Stanley says that gold stocks have run harder than warranted and are overbought as investors flock to safe haven assets. Barrick Gold is looking for buyers for Australia’s Kalgoorlie super-pit mine that was once the country’s largest and says that Northern Star has potential interest. Northern Star’s share price tumbled 8 percent on the news. This raises doubts about the potential purchaser of the mine that was once seen as a massive opportunity.

- Anglo American Platinum Ltd, the world’s top platinum and palladium supplier, is looking to invent a new battery to counter the long-term threat of the electric car boom. Bloomberg writes that EV demand is a threat to demand for automobile catalysts, which use the two precious metals to clean toxic emissions. However, these two metals are heavier and more expensive than what is currently used in EV batteries.

Opportunities

- Gold equities are cheap and have room to continue running relative to the gold price, as they are lagging their historical relationship. The chart below compares the price of the senior gold miners to the price of gold 10-years ago. The miners have taken a much bigger drop than the gold price. TD Securities writes in a note that it expects a further rotation from producers down to the junior miners and eventually to the emerging producers to developers, which will be catalyzed by high profile M&A activity. Jeff Currie, global head of commodities research at Goldman Sachs, says that central banks are buying gold because they don’t want to own dollars with sanction, geopolitical and trade-war risks. UBS raised its gold price forecast in 2020 to $1,550 per ounce as their economists believe a U.S.-China deal is looking increasingly unlikely, reports Bloomberg.

- Former Federal Reserve Chairman Alan Greenspan said this week that he wouldn’t be surprised if U.S. bond yields turn negative and that if they do, it won’t be that big of a deal. Greenspan said in a Bloomberg interview that “there is no barrier for U.S. Treasury yields going below zero. Zero has no meaning, besides being a certain level.” This comes as 10-year TIPS were negative for two days this week. Negative yields have historically been positive for the price of gold.

- South Africa’s Public Investment Corp., the continent’s largest money manager, sees big investment opportunities in West Africa to drive the next gold mining boom. Mining research analyst Lebohang Sekhokoane says “when you look at the gold sector in West Africa, that’s where the sun is rising.” The firm highlights Ghana, where AngloGold Ashanti and Gold Fields are shifting more production to and away from South Africa. Cardinal Resources also has its 5.1 million ounce shovel-ready reserve in Ghana and could be a takeover target.

Threats

- An 18 percent surge in bullion over three months is great news for mining companies, writes Bloomberg, but has spurred a burst of illegal prospecting that has helped fuel organized crime within some of the world’s top gold-producing regions. This is bad news for natives in these mining areas, leading to suffering caused by threats, danger and even mercury poising. In fact, a third of the gold imported from Latin America in 2013 was mined illegally – meaning proper permits were not obtained, areas were not environmentally protected or heavy machinery was used without oversight.

- According to Morgan Stanley analysts, a supply gap for palladium, rhodium and platinum is seen persisting over the next four years, reports Bloomberg, as tighter vehicle emissions standards drive demand. Tighter emissions for heavy-duty vehicles could boost platinum use in China and India in particular, the article continues.

- According to industry sources, China has severely restricted imports of gold since May, reports Reuters, in a move that could be aimed at curbing outflows of dollars and bolstering its yuan currency as economic growth slows. Shipments have been cut by around 300-500 tonnes compared with last year – worth $15-25 billion at current prices, the article continues. China is the world’s biggest gold importer, accumulating what is equivalent to one-third of the world’s total supply.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.53 percent. The S&P 500 Stock Index fell 0.94 percent, while the Nasdaq Composite fell 0.79 percent. The Russell 2000 small capitalization index lost 1.26 percent this week.

- The Hang Seng Composite lost 0.96 percent this week; while Taiwan was down 0.70 percent and the KOSPI fell 0.55 percent.

- The 10-year Treasury bond yield fell 18 basis points to 1.56 percent.

Domestic Equity Market

Strengths

- Consumer staples was the best performing sector of the week, increasing 1.57 percent compared to an overall decrease of 1.00 percent for the S&P 500 Index.

- Walmart was the best performing stock for the week, increasing 5.32 percent.

- Nvidia rallied on Friday after the semiconductor company reported second-quarter results that beat expectations. Strength in the quarter was driven by growth in its gaming chips, where sales were up 24 percent on a sequential basis. Analysts also touted the unexpectedly rapid increase in gross margins, which helped to offset a revenue outlook that was a little lighter than consensus estimates, as well as ongoing softness in its data-center division. Shares rose as much as 8.3 percent in its biggest one-day percentage gain since October.

Weaknesses

- Energy was the worst performing sector for the week, decreasing 3.88 percent compared to an overall decrease of 1.00 percent for the S&P 500.

- Tapestry was the worst performing stock for the week, falling 27.13 percent.

- General Electric’s biggest plunge in 11 years came on Thursday when Harry Markopolos, who rose to prominence by blowing the whistle on Bernie Madoff, accused GE of “accounting fraud.” The stock fell 14 percent on the day.

Opportunities

- Health Catalyst is expected to receive initiations from analysts as soon as Monday when a quiet period expires at banks that underwrote its initial public offering. This has been a stellar year for digital health IPOs with Change Healthcare and Phreesia paving the way for Health’s July 15 offering, which was upsized and above-priced. Shares are up nearly 60 percent from its offer to date. Initiations from analysts at bookrunner banks tend to be favorable and could catalyze another move up, based on Change and Phreesia’s example.

- CyrusOne may be worth $85 a share in a takeover, Cowen analyst Colby Synesael writes after Bloomberg earlier reported the Dallas-based real estate investment trust (REIT) is exploring a takeout after getting interest. With private investors still interested in data center managers and most larger, private companies already acquired, it’s only natural that at this point in the cycle attention is moving to public companies. Cowen said in a July 23 note that it sees CONE as the likeliest takeout target in the sector, especially due to a “stark difference” in multiples being paid in the private market vs multiples of public.

- Coworking space startup WeWork unveiled its IPO filing Wednesday. The company was valued at $47 billion in its most recent private funding round in January and has raised $10 billion in funding since 2011.

Threats

- President Donald Trump is reportedly planning an attempt to regulate Facebook and Twitter over alleged anti-conservative bias. According to CNN, Trump is planning an executive order that could have significant implications for how internet companies moderate content.

- Global banks are cutting 30,000 jobs this year. It's a sign the banking crisis is only getting worse. Citigroup, Barclays and Deutsche Bank have all announced cuts this year.

- The U.S. Justice Department is preparing to sue to block travel technology company Sabre Corp.’s proposed acquisition of Farelogix over concerns the deal will harm competition, according to a person familiar with the matter. The department’s antitrust division is set to file a lawsuit as soon as Monday, said the person. Sabre announced plans Wednesday to close the deal next week. Sabre agreed to buy Farelogix in November for $360 million. Both companies provide information technology systems that enable airlines to sell tickets. The Justice Department challenge would follow concerns raised by the U.K.’s antitrust regulator on Friday. The Competition and Markets Authority said its initial investigation of the takeover found Farelogix is a competitive threat to Sabre.

The Economy and Bond Market

Strengths

- Data released by the U.S. Census Bureau on Thursday, shows that U.S. retail sales increased by 0.7 percent on a monthly basis in July, beating the market expectation of 0.3 percent. The latest number shows that consumer spending continues to be a pillar of growth domestically.

- The headline General Business Conditions Index of the Federal Reserve Bank of New York's Empire State Manufacturing Survey came in at 4.8 in August, reports FXStreet.com, following July's reading of 4.3 and surpassed analysts' estimate of 3. "New orders increased after declining for the prior two months, and shipments continued to expand," the New York Fed said in its publication.

- Former Fed chair Janet Yellen told Fox Business News that she doesn’t think the U.S. economy is headed toward a recession. “I think the answer is most likely no,” Yellen said on WSJ at Large Opens a New Window on Wednesday. “I think the U.S. economy has enough strength to avoid that. But the odds have clearly risen and they are higher than I’m frankly comfortable with.”

Weaknesses

- The U.S. fiscal deficit has already exceeded the full-year figure for last year, writes Bloomberg, as spending growth outpaces revenue. The gap grew to $866.8 billion in the first 10 months of the fiscal year, up 27 percent from the same period a year earlier, the Treasury Department said. That’s wider than last fiscal year’s shortfall of $779 billion — which was the largest federal deficit since 2012, the article continues.

- Initial claims for state unemployment benefits increased more than expected by 9,000 to a seasonally adjusted 220,000 for the week ended August 10, the Labor Department said Thursday. Economists polled by Reuters had forecast claims would rise to 214,000 in the latest week.

- Germany's economy just shrank, meaning Europe's biggest economy is 'teetering on the edge of recession,’ reads one Business Insider headline. The economy contracted by 0.1 percent in the three months to June, fueling the country’s slowest first-half growth rate in six years.

Opportunities

- The focal point next week will be the Federal Reserve and the path of monetary policy in the United States as the FOMC minutes are due to be published on Wednesday and Fed Chairman Jerome Powell will speak on the second day of the Jackson Hole conference on August 23. Traders will be seeking to get more clarity from Powell following his much-criticized press conference from the July meeting. If Powell and other FOMC members suggest the worsening U.S.-China trade war warrants a deeper rate-cutting cycle than hinted at during the July meeting, markets will likely be appeased.

- Just as the Fed’s economic symposium comes to an end on August 24, the leaders of the world’s seven largest industrialized nations will meet in France for the 2019 G7 summit. With US-China trade tensions running high and given the recent flare-up in the Middle East with Iran, it’s unclear whether the summit will produce any thaw in relations between the key nations. But should any progress be made, the recent flare up in global turmoil could hit a much needed reprieve.

- National security adviser John Bolton stressed to British officials on Monday that Washington will support a U.S.-U.K. free trade agreement.

Threats

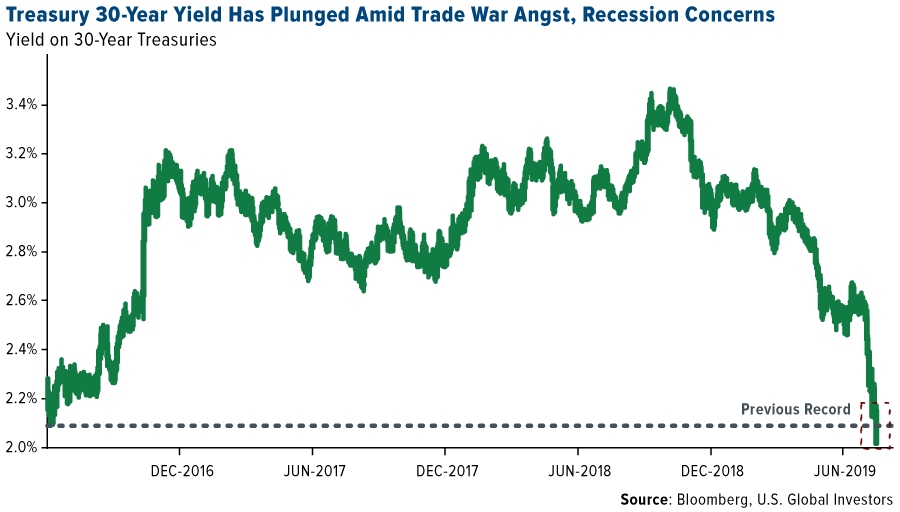

- The yield on the 30-year Treasury bond fell to its lowest level on record as concerns mount over the potential impact of the U.S-China trade war on the world economy. China reported the weakest growth in industrial output since 2002, Germany’s economy shrank as exports slumped, and euro-area production plunged the most in more than three years as the overall expansion cooled. Meanwhile, the stream of investors into the safest parts of the market drove the 10-year Treasury yield below the two-year for the first time since the financial crisis.

- U.S. consumer sentiment plummeted to a seven- month low in August on growing concerns about the economy, writes Bloomberg. The University of Michigan’s preliminary sentiment index slumped to 92.1 from July’s 98.4, missing all forecasts in Bloomberg’s survey of economists. The gauge of current conditions decreased to 107.4 while the expectations index dropped to 82.3, bringing both readings to the lowest levels since early this year.

- U.S. homebuilding fell for a third straight month in July amid a steep decline in the construction of multi-family housing units, reports Reuters. Housing starts dropped 4.0 percent to a seasonally adjusted annual rate of 1.191 million units last month, the Commerce Department said on Friday.

Energy and Natural Resources Market

Strengths

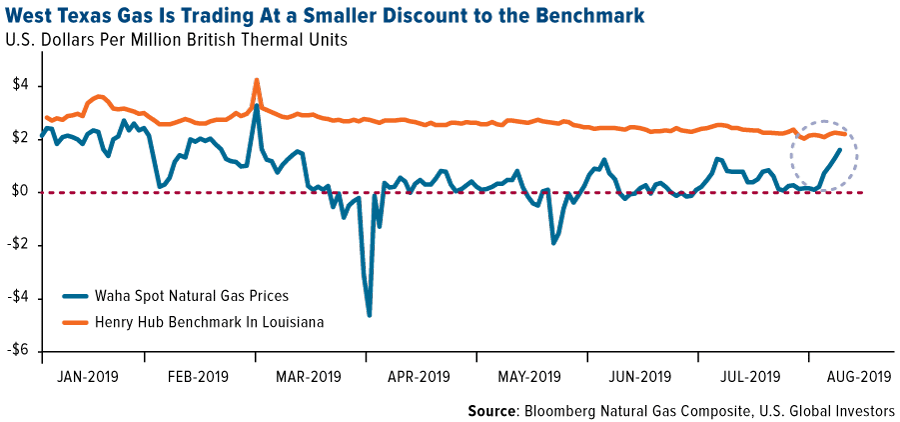

- The best performing major commodity for the week was nickel, which gained 5.01 percent as the Indonesian government said it will move forward a plan to ban raw mineral ore shipments. Bloomberg reports that natural gas prices in the Permian Basin surged 16-fold this week after a key pipeline began initial flows. The Kinder Morgan Gulf Coast Express Line will carry 2 billion cubic feet a day from the Permian and will serve as a key interconnection point in the region. Oil is headed for a weekly gain, with West Texas Intermediate (WTI) futures gaining 0.6 percent on Friday morning, as hopes increase that the U.S. and China will resume trade negotiations.

- Cobalt is working its way back up as Glencore released a plan to slash one fifth of global output. Glencore, the world’s top producer of the metal, will close its biggest mine by the end of the year and help the market, which has suffered from severe over supply. Cobalt has now gained 20 percent in the month of August after hitting its lowest level since 2016 at the end of July.

- According to the Energy Information Administration (EIA), U.S. solar imports in May hit their highest level since October 2017. Duties have decreased this year to 25 percent, down from an initial 30 percent, while panel costs continue to decline. Bloomberg reports that solar installations reached a record in the first quarter of this year.

Weaknesses

- The worst performing major commodity for the week was corn, which fell 9.57 percent as government estimates for crop plantings and yields came in higher than estimated. In addition, China noted that African swine fever will cut their feed demand. On Monday Texas became the most expensive place to buy power in all of America’s major markets. Bloomberg reports that electricity prices jumped 36,000 percent to average $6,537.45 a megawatt-hour (Mwh). The Texas power market has become highly volatile as coal-fire powered plants continue to close due to shrinking profits.

- Bank of American Merrill Lynch cut its recommendations on six miners, saying that China’s economy is likely to get worse before it gets better. The bank cut its ratings on BHP and Glencore, saying that miners are unlikely to rebound until China acts with rate cuts and other stimulus to help the economy.

- According to BloombergNEF, an effort to lobby the Democratic Republic of Congo to renegotiate its mining code that increases royalties on cobalt is unlikely to succeed. Codelco, the world’s largest copper miner is raising debt to secure funding for upgrade projects just four months after saying that it didn’t need to raise money either this year or next.

Opportunities

- Bloomberg reports that China National Chemical is gearing up for a listing of Syngenta AG, a Swiss pesticide producer that it acquired for $43 billion. This would be the world’s biggest chemical IPO and could come as soon as mid-2020.

- Goldman Sachs came out with a few forecasts this week. They say iron ore will recover from a steep sell-off and rise back above $100 ton within three months and hit $115 per ton. The group said iron’s recent collapse is “temporary relief from a structural deficit rather than a lasting price collapse.” Goldman also says that hedge funds’ overly pessimistic outlook on global economic prospects has fueled bearish bets against copper, but that it leaves potential for the price to rebound.

- A new development in wind power took flight this week. Alphabet-subsidiary Makani completed a test of its flying wind power turbine off the coast of Norway. Bloomberg’s William Mathis writes that the new device looks like a sleek airplane and that it has eight rotors attached to spin in the wind to generate electricity. The benefits of this new technology is that it requires less steel and concrete to install and would be a fraction of the cost of floating platforms.

Threats

- According to law firm Haynes and Boone, shale bankruptcies are on track to surge past the number set last year. The firm’s data shows that so far in 2019 there have been 36 drillers, frackers and other oilfield-service providers that have filled for bankruptcy, compared to 30 at the same point in 2018.

- The Trump Administration’s Environmental Protection Agency (EPA) is drafting a proposal that would end direct federal regulation of methane leaks from oil and gas facilities. This comes as several oil companies have made voluntary pledges to keep methane in check. Bloomberg writes that some have warned the administration that federal regulation is essential for natural gas to maintain its reputation of being a more climate-friendly source of electricity.

- Jeff Currie, global head of commodities research, said in a Bloomberg interview this week that crude markets are trading on sentiment, not fundamentals, and that oil is unlikely to reach $75 per barrel.

August 14, 2019"No Longer Just a Science Project": David Fessler on Renewable Energy and EVs |

August 12, 2019What's Next for Gold After $1,500? |

August 12, 2019With Yields Sinking Everywhere, Gold Just Hit New All-Time Highs... |

|||

Emerging Europe

Strengths

- Czech Republic was the best performing country this week, gaining 1.25 percent.

- The Czech crown was the best performing currency this week, down 45 basis points against the U.S. dollar. The Czech National Bank (CNB), unlike the European Central Bank, will not ease monetary policy anytime soon.

- Information technology was the best performing sector among eastern European markets this week

Weaknesses

- Greece was the worst performing country this week, losing 5.74 percent.

- The Russian ruble was the worst performing currency in the region this week, losing 1.86 percent against the U.S. dollar. The ruble fell to its weakest level since May as crude oil declined and fears of a global economic slowdown weighed on emerging market assets.

- Financials was the worst performing sector among eastern European markets this week.

Opportunities

- The Bank of Russia’s total stockpile of cash, gold and other securities is about to surpass Saudi Arabia’s. Russia has tightened its budged and is running a surplus, while Saudi Arabia spends money that has been stockpiled when oil prices are higher. Russia’s reserves have increased by 45 percent in the past four years to a total of $518 billion in June, while the reserves of the other oil dependent country, Saudi Arabia, fell to $527 billion. Russia still needs to implement reforms that will stimulate growth and with high reserves, it may finally happen.

- Emerging market assets could be back on investors’ minds as President Donald Trump delayed tariffs on certain consumer items until December 15, while other products were removed from the new China tariff list altogether. Quarter-to-date, Greece and Poland sold off the most among central emerging Europe, and could both rebound strongly on lower trade tensions between the U.S. and China.

- Alrosa, a Russian diamond producer, is preparing to sell the Spirit of the Rose diamond, which could be among the world’s most valuable gems. Discovered in 2017 in the far east of Russia, the prized stone could be worth between $60 million to $65 million. Pink diamonds are rare and are about to become even rarer after Rio Tinto Group confirmed earlier this year that it is shutting its giant Argyle operation in Australia, the mine producing about 90 percent of the world’s pink gems.

Threats

- According to a Gallup poll in Russia, 20 percent of the population wants to leave the country. The figure is even higher among younger populations. In the 15 to 29 year old group, 44 percent indicated that they would like to migrate. President Vladimir Putin came to power 20 years ago, but his popularity is declining, as people are demanding reforms that would improve their quality of life. The population is also demanding more democracy. Protests on streets of Moscow are growing, as local elections are approaching and Moscow authorities refuse to register opposition candidates.

- Expectations for the German economy have slumped to the lowest level since the eurozone debt crisis eight years ago due to U.S.-China trade tensions and worries over the U.K.’s exit from the European Union. The ZEW Survey Expectations indicator has dropped to minus 44.1, much lower the estimate in a Reuter’s poll of minus 28.5.

- Gross domestic product (GDP) in Germany shrank in the second quarter. GDP fell 0.1 percent from the previous period, as expected. In the whole eurozone area, second quarter growth was confirmed at 0.2 percent, while industrial output plunged to 1.6 percent in June. Central European countries are growing at a faster pace with Hungary reporting 1.1 percent growth in the first quarter and Poland with 0.8 percent.

China Region

Strengths

- The best performing index in the region for the week was China’s Shanghai Composite, which jumped 1.81 percent on the week amid some trade war reprieve on tariff escalation.

- The best performing sector in Hong Kong’s Hang Seng Composite Index was Telecom, which gained 0.80 percent as a safer haven in a mildly down week.

- Malaysia’s second quarter year-over-year GDP reading clocked in at 4.9 percent, beating expectations for a 4.7 percent print and rising from a prior reading of 4.5 percent.

Weaknesses

- The worst performing index in the region for the week was Singapore’s FTSE Straits Times Total Return Index, which fell 1.16 percent since last Thursday (Singapore was closed for National Day and Hari Raya Haji holidays on Friday and Monday last and this week, respectively). Thailand’s SET Index was also down, falling 1.09 percent this week.

- The worst performing sector in Hong Kong’s Hang Seng Composite Index this week was Materials, which declined by 2.89 percent.

- China’s Industrial Production, Retail Sales and Fixed Assets Investment all missed estimates this week, gaining for the July periods, respectively, and year over year, only 4.8 percent, 7.6 percent and 5.7 percent.

Opportunities

- As was observed could be possible, we did indeed see a bit of reprieve on the trade war front as President Donald Trump is planning to delay implementation of some new tariffs until December (or even beyond?) in order to spare the U.S. consumer through the holiday season (for domestic consumers do indeed bear some costs of a trade war inasmuch as they purchase imported, tariffed goods at higher prices or face higher prices from the boosted pricing power of other producers or sellers of similar but non-tariffed goods). Presidents Trump and Xi Jinping are reportedly scheduled to talk sometime “very soon.”

- Indonesia’s Joko Widodo suggested that the economy is now set to expand at the fastest pace in seven years, announcing that the Southeast Asian island nation’s GDP is forecast to grow at 5.3 percent next year.

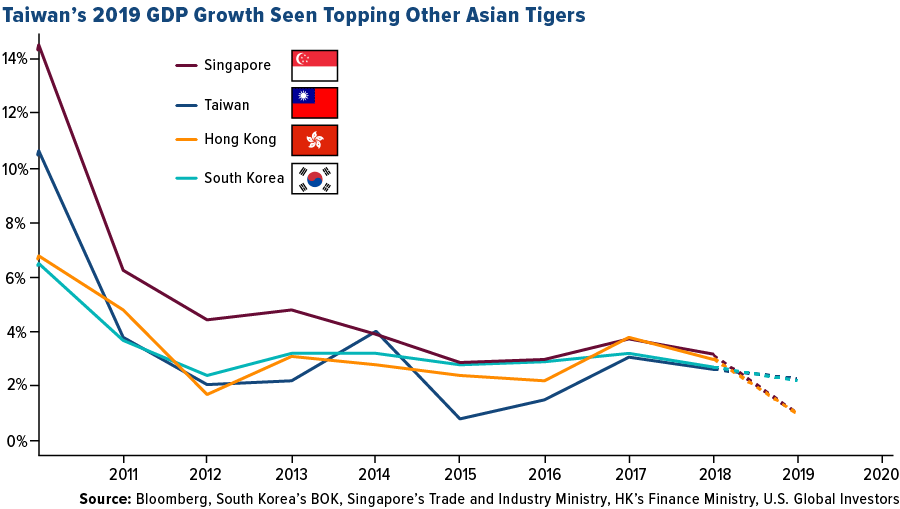

- Taiwan looks set to top the three other traditional so-called “Asian Tiger” economies, with full-year economic growth projected to clock in at just under 2.5 percent, likely outperforming South Korea, Singapore and Hong Kong, according to a recent Bloomberg News report.

Threats

- In keeping with what remains a very real threat, we again reiterate that trade war escalation remains a threat until it isn’t. Even though we saw a bit of a reprieve this week, so too we also witnessed China announce it is preparing countermeasures to any U.S. tariffs and very much play down upcoming “talks’, which may well be telephone only.

- Once again, unrest continues in Hong Kong, which may be perpetuating negative sentiment. Media reports are also granting more attention to international stands and campus support for Hong Kong around the world, while Beijing appears in no rush to rush anything related to the SAR.

- Hong Kong’s economy contracted further than expected for the second quarter, shrinking 0.4 percent, and Financial Secretary Paul Chan, who has advised that the city faces significant economic disruption amid the protests, indicated that GDP is now expected to be between 0 percent and 1.0 percent, lowering expectations from a previous range of two to three percent. The Hong Kong government did announce some fiscally-supportive measures at the same time, given the current headwinds.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended August 16 was BitBall, up 6,435.72 percent.

- In a 28-page packet of slides titled “The Charts That Matter Next Week,” an introductory note cautions that the views within are not “an official view of Goldman Sachs,” reports Bloomberg. They do, however, represent the views of one Goldman analyst Sheba Jafari, who believes that bitcoin could go up by 23 percent in the short term, and that later the coin could go even higher.

- Walmart has reasserted its interest in blockchain-backed drones with a recent patent application, reports CoinDesk. The application entitled “Cloning Drones Using Blockchain” isn’t the retail giant’s first foray into blockchain-backed drone technology, the article continues. In 2017 it sought a patent for a package delivery system using the same tech, among other applications.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended August 16 was Boltt Coin, down 97.27 percent.

- The Securities and Exchange Commission (SEC) has again postponed decisions on three bitcoin ETF proposals, according to documents released by the regulatory agency on Monday. Wilshire Phoenix Funds joined the waitlist with Bitwise Asset Management and VanEck/SolidX when it proposed a find that hedges bitcoin with Treasury bills in June. The new deadline for a decision from the SEC, reports CoinDesk, is September 29 for Wilshire Phoenix and various dates in October for Bitwise and VanEck/SolidX.

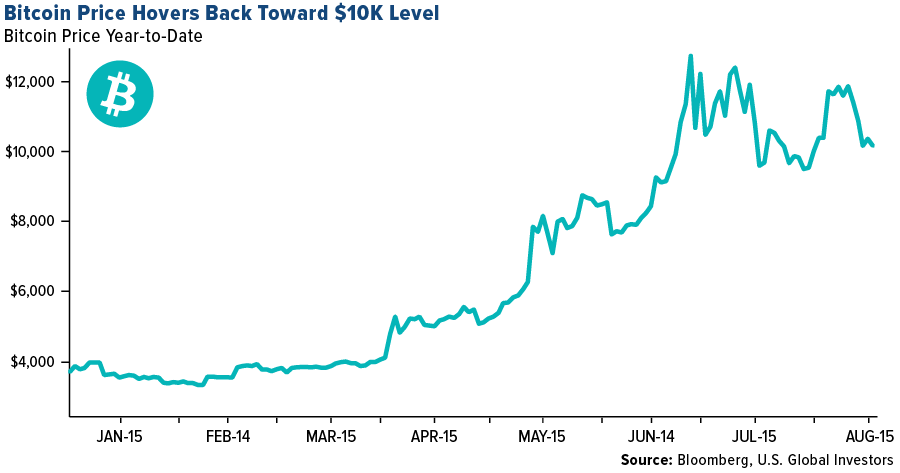

- After enduring its worse single-day loss in a month, bitcoin continues to tumble from temporary support levels at $10,000, reports CoinDesk. The popular digital currency dipped beneath its 100-day moving average, which could open the doors to support near $8,500 if the bulls can’t keep prices above the MA. As of Friday, however, bitcoin seemed to defend its price support, hovering around the $10K (despite the bear case still being intact).

Opportunities

- The People’s Bank of China (PBOC) is “close” to issuing its own cryptocurrency, according to deputy director of the bank’s payments department Mu Changchun. As reported by Bloomberg, the PBOC’s intention is that the digital currency would replace M0, or cash in circulation, rather than M2, which would generate credit and impact monetary policy.

- Finally Samsung has added bitcoin functionality on its blockchain-enabled smartphones, writes CoinDesk. Back in March the Galaxy S10 range was launched with a “Blockchain Keystore” offering cryptocurrency storage and transactions for ether (ETH) and related ERC-20 tokens, but had notably excluded the number-one crypto by market cap.

- Turmoil in Argentina and Hong Kong is prompting local investors to pay a premium for bitcoin, writes Bloomberg, with the leading digital currency proving to be less of a refuge for everyone than advertised. In fact, in Argentina where the peso fell on election uncertainty, bitcoin traded for as much as $12,000 on LocalBitcoins.com (a peer-to-peer platform).

Threats

- “The most prestigious banking relationship in crypto has ended,” reads one article from CoinDesk this week. According to industry sources, London-based Barclays is no longer working with cryptocurrency exchange Coinbase. Despite Coinbase finding a replacement in ClearBank, the change has inconvenienced the exchanges’ users, the article continues. Although nobody knows for certain, some sources claim that Barclays’ risk appetite has contracted a little.

- A new round of warning letters from the U.S. Internal Revenue Service (IRS) to cryptocurrency users is being sent out, reports CoinDesk, and this time it is to taxpayers believed to have misreported income from exchange transactions. According to one letter shared with CoinDesk, a taxpayer owed nearly $4,000 for the 2017 tax year. “This taxpayer owed more than $3,600 in taxes alone, with another $200 or so in interest accrued,” the article goes on to explain.

- Despite many loans being made in cryptocurrency, lenders have not reaped a lot of profit, writes CoinDesk. This is according to a new report released by Graychain, which is a startup aiming to bring credit assessment to the crypto space. The report estimates that while $4.7 billion has been lent out over the history of the sector, only $86 million has been earned back in interest.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits