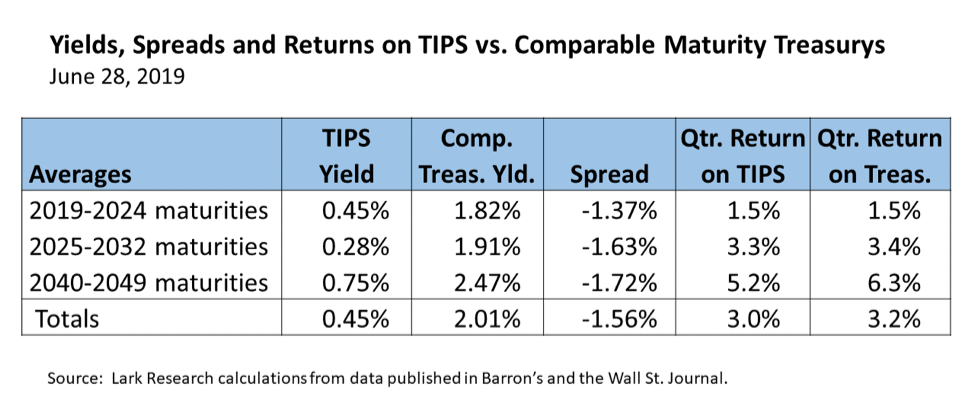

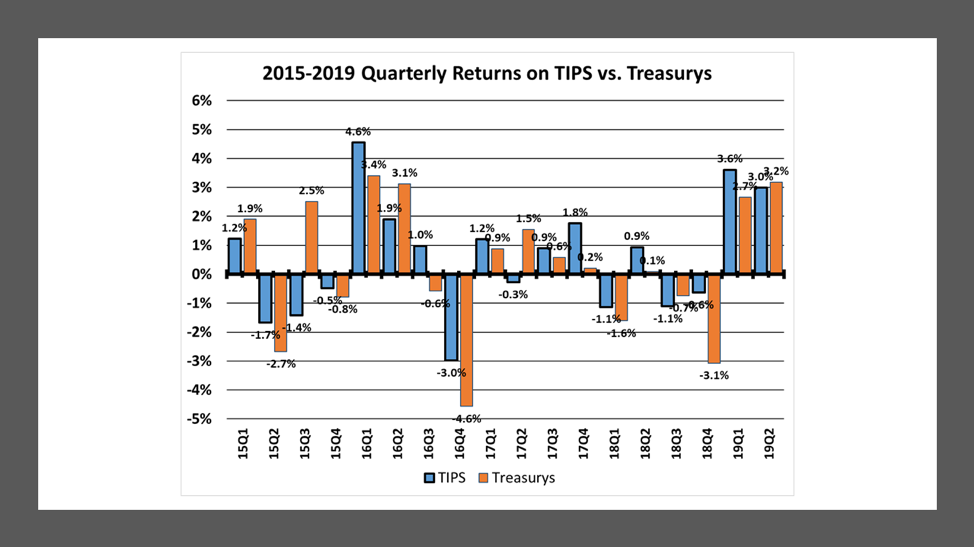

Comparable maturity straight Treasurys outperformed Treasury Inflation-Protected Securities (TIPS) in the 2019 second quarter, but only slightly. On average, Treasurys earned a return of 3.2% in the quarter, better than the 3.0% return on TIPS.

On a price basis (excluding the inflation adjustment), Treasurys significantly outperformed TIPS. The average TIPS yield rose 5 basis points (bp) in the quarter to 0.45%, while average Treasury yields fell 44 bp to 2.01%. Most of the shortfall in price return on TIPS was therefore made up by the CPI inflation adjustment, which averaged 152 bp in the quarter.

While the average yield on TIPS bonds rose by 5 bp to 0.45%, there were meaningful differences in yield changes across maturities. Short-term TIPS experienced the greatest bump up in yield, increasing from -0.01% to 0.45%. Yields on intermediate-term TIPS dropped by 22 bp to 0.28% and long-term TIPS yields declined by 14 bp to 0.75%.

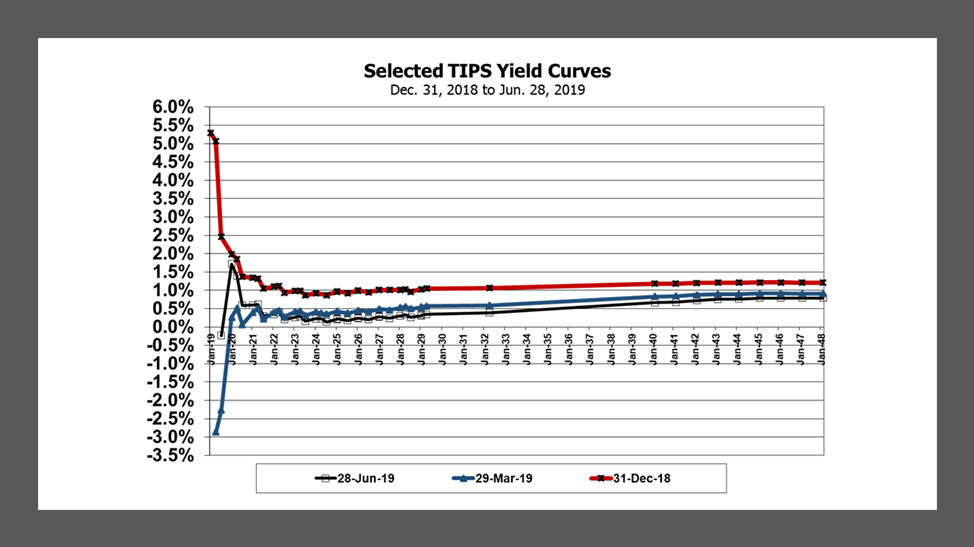

The chart below shows the shifts in the TIPS yield curve by quarter for 2019. At the short end of the curve, small changes in price typically have a big impact on yield. Accordingly, the shortest maturity TIPS have swung wildly from positive in 18Q4 to negative in 19Q1 and then back to positive in 19Q2. The swings suggest that investors routinely chase returns on short maturity TIPS based upon expected changes in the inflation adjustment. They are willing to accept negative yields on short-term TIPS when they anticipate a solidly positive CPI adjustment, but require positive yields when the CPI adjustment will be small or perhaps even negative.

Moving out on the TIPS yield curve, TIPS yields have shifted lower with each passing quarter, essentially following the performance of straight Treasurys. Those moderate downshifts in yield have produced solid returns on intermediate- and long-term TIPS so far this year.

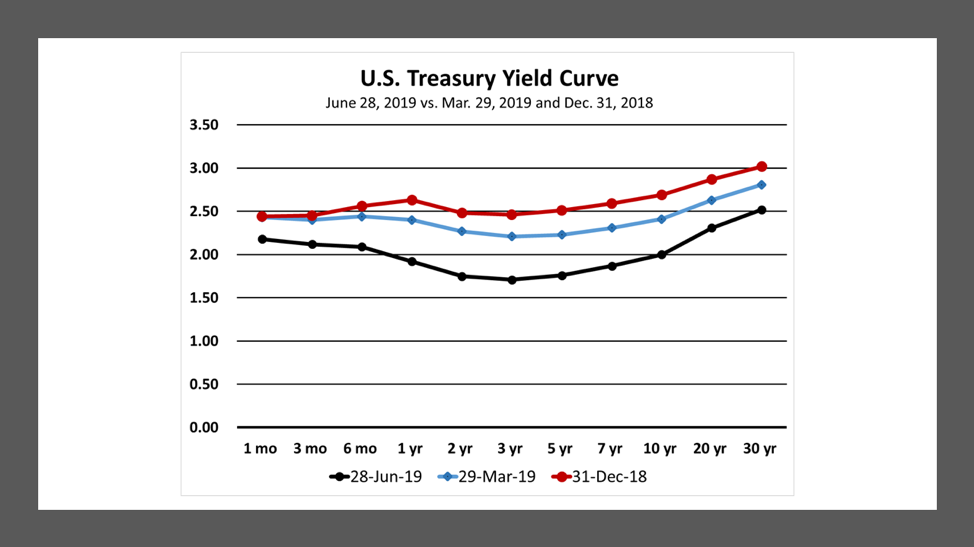

The decline in straight Treasury yields was more significant in 19Q2. The average Treasury yield across all maturities fell 44 bp to 2.01%. Short-term Treasury yields fell 52 bp to 1.82%, apparently anticipating a significant easing of Federal Reserve policy. Intermediate-term Treasury yields declined 47 bp to 1.91%; while long-term Treasury yields declined 31 bp to 2.47%.

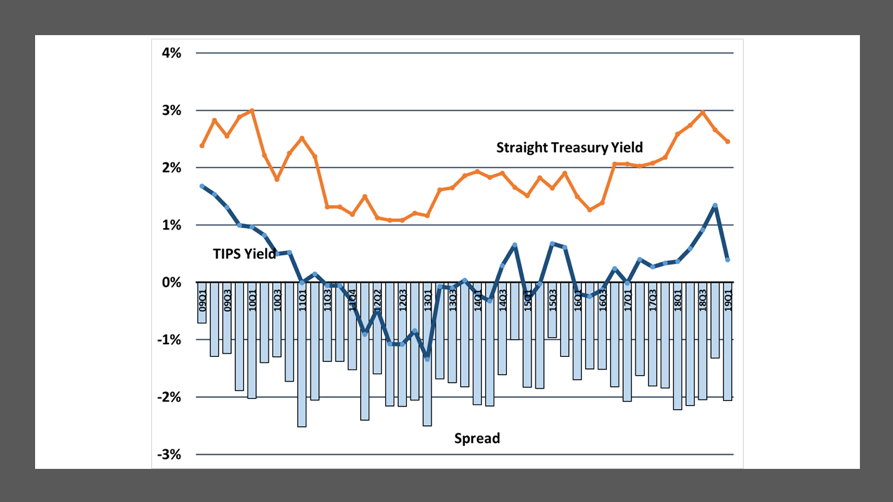

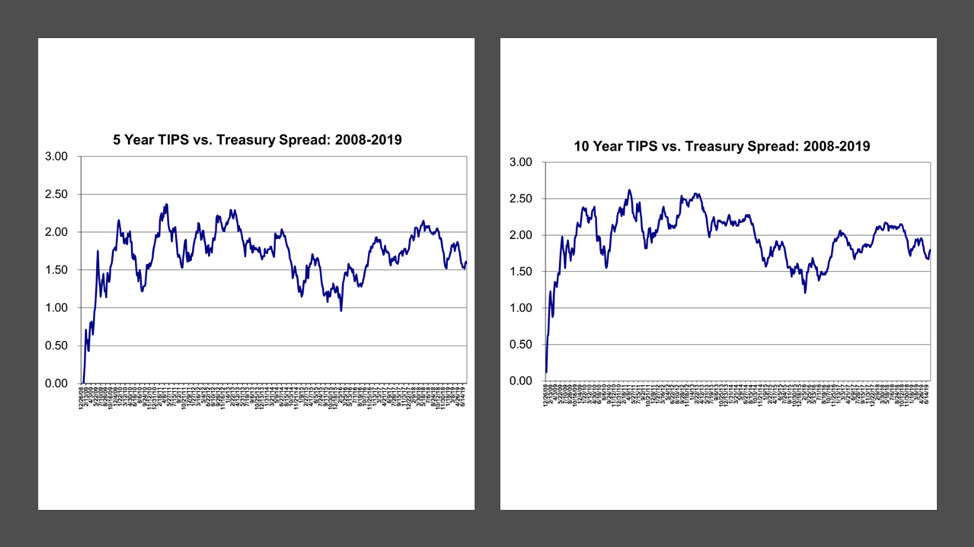

The greater decline in Treasury yields caused the spread between TIPS yields and Treasury yields to fall by 50 bp from 206 bp in the 2019 first quarter to 156 bp in the 2019 second quarter. The spread measures the average expected inflation rate. It is also called the breakeven inflation rate that would make investors indifferent to owning TIPS or straight Treasurys. If an investor believes that actual inflation will be higher than the breakeven spread, she would prefer to own TIPS (because she would get a greater total return with a higher inflation adjustment). On the other hand, if she thinks that actual inflation will be lower than the spread, she would prefer to own straight Treasurys.

Since 2009, the TIPS-Treasury spread has averaged 175 bp and the quarterly change in the spread has averaged 38 bp. So far this year, the quarterly change in the spread has averaged 66 bp, nearly twice the historic average. This volatility has coincided with the changes in inflation adjustment on TIPS (which is determined by the change in the benchmark headline CPI).

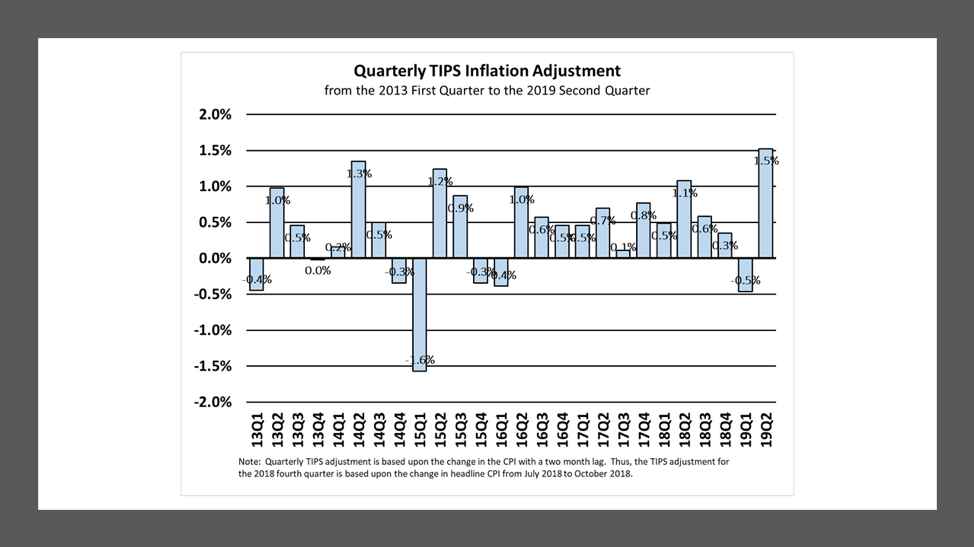

The inflation adjustment is determined by the quarterly change in the non-seasonally adjusted headline CPI with a two-month lag, so investors get an advance read on the upcoming inflation adjustment. Most recently, the inflation adjustment has fluctuated from an increase of 0.58% for the 2018 fourth quarter to a decline of 0.49% in the 2019 first quarter to an increase of 1.52% in the 2019 second quarter. Based upon the May and June CPI figures and my forecast for the CPI for July, I estimate that the inflation adjustment will be between 0.25% and 0.35% for the 2019 third quarter. Thus, investors have sold short-maturity TIPS, which has increased their average yield, to compensate for the expected drop in the inflation adjustment.

The recent gyrations in the inflation adjustment have been due primarily to the impact of changing energy prices (most notably gasoline) on inflation. Since the end of 19Q2, the price of West Texas Intermediate crude oil has declined 6.5% from $58.50 to $54.70 on Aug. 5. Similarly, the continuous near-term contract for gasoline futures has fallen 9.5% from $1.90 to $1.72 per gallon over the same period. This is the key driver behind my estimate for July CPI and the 19Q3 inflation adjustment.

The 19Q2 outperformance of Treasurys vs. TIPS and the decline in the breakeven spread to 156 bp (to below the long-term average of 175 bp) make TIPS more attractive than straight Treasurys to my eye at this time. If the spread returns to its long-term average in the next few quarters, it will most likely be accomplished by a greater increase in Treasury yields vs. TIPS.

Yet, it is difficult to predict when and how that will happen. The market seems to be worried that a looming slowdown in the economy will bring inflation well below the Fed’s long-term target of 2%. Thus, the decline in the spread may merely be anticipating this change in the economic environment. It is possible, therefore, that the spread could go lower before it moves higher.

That, in fact, is what has happened in the past five weeks. Since the end of 19Q2, the average TIPS yield has slipped 4 bp to 0.41% and the average yield on comparable maturity Treasurys has fallen another 25 bp to 1.76%. Thus, TIPS have earned 1.3% on average over the past five weeks (with the inflation adjustment) while straight Treasurys have delivered a 2.1% total return. The greater drop in Treasury yields has pushed the breakeven spread to 136 bp, which is approaching the low end of its range over the past decade.

August 6, 2019

Stephen P. Percoco

Lark Research

839 Dewitt Street

Linden, New Jersey 07036

908) 448-2246

[email protected]

www.larkresearch.com

Lark Research is an independent investment research provider founded by Stephen P. Percoco in 1991. Research coverage includes stocks and bond in industries such as real estate, utilities, oil & gas, telecommunications, industrials, consumer goods and materials. Prior to founding Lark Research, Steve served as Vice President in High Yield Corporate Bond Research at Salomon Brothers and as an investment officer at Bank of Boston. He is a graduate of Bowdoin College and Harvard Business School.

© Lark Research

More Energy Topics >