3 Reasons Why More Tariffs are Bullish for Government Bonds

Today’s news of 10% tariffs on a the remaining $300bn of imports from China took markets by storm today with US stocks moving from a 1% gain to almost a 1% loss on the day. Meanwhile, gold closed at a 6-year high of $1445. But the most important move, in our view, was the action in government bonds. The 10-year treasury note shattered the July low to finish at 1.89% – the lowest level since late-2016. The action came as markets were already trying to digest more evidence of a further slowdown in manufacturing activity as ISM manufacturing PMI declined by half a point to 51.2 vs expectations of a rise to 52. Even with the large moves today, especially in government bonds, the additional tariffs foreshadow still more downside for yields for at least three reasons.

Manufacturing activity is being affected by tariffs and it is slowing markedly – bond yields track manufacturing activity. Manufacturing activity peaked coincident with tariffs being announced on Chinese-made solar panels and washer machines in early 2018. As the impact of trade policy has affected actual business decisions, business conditions have deteriorated. More tariffs are likely to exacerbate this trend in manufacturing activity and bring down rates as a result.

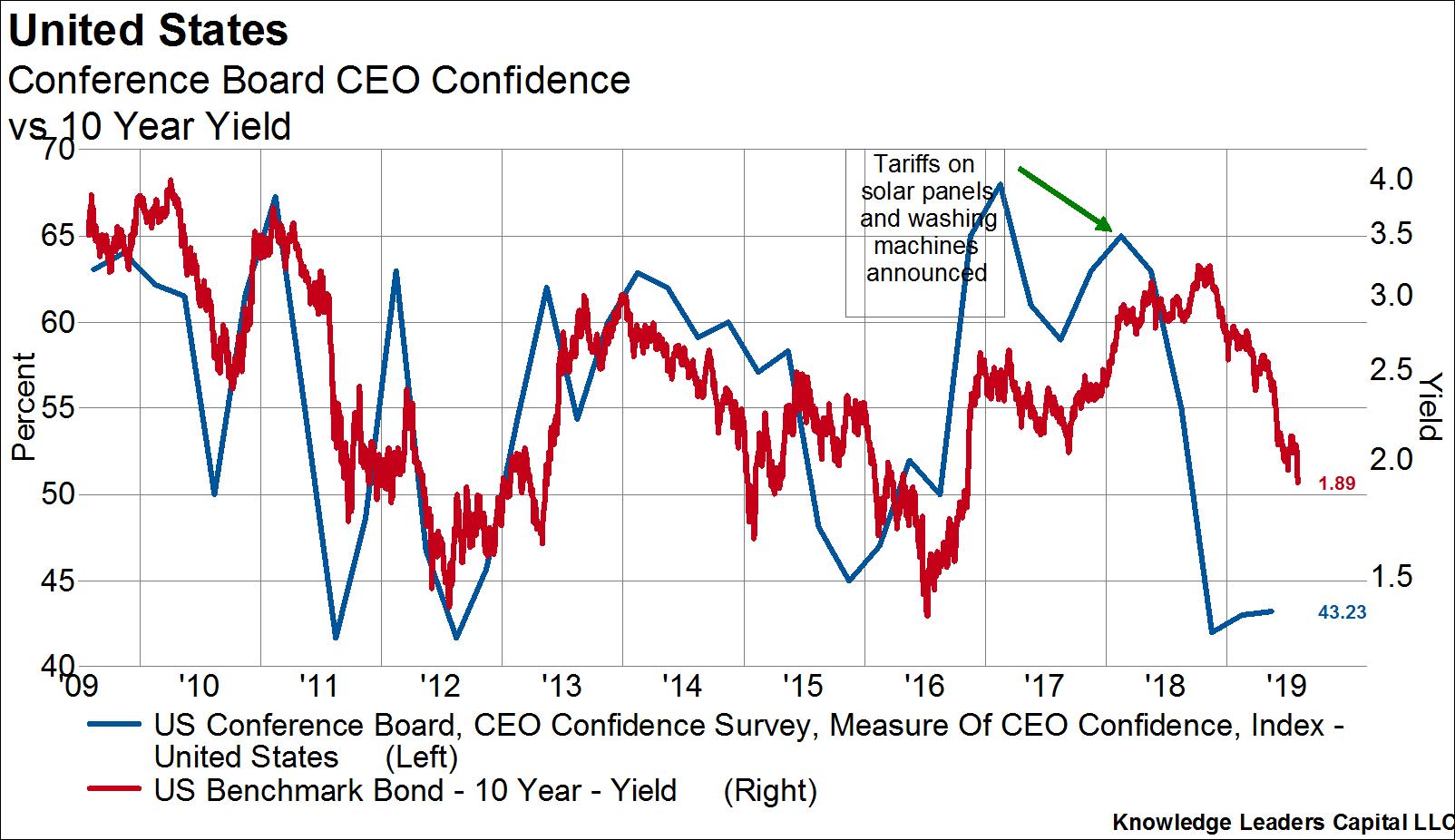

Business confidence is being affected by tariffs and is falling markedly – bond yields track business confidence. Public policy affects business confidence insofar as policy uncertainty makes it more difficult for business leaders to make decisions about capex and hiring. Business confidence peaked in early 2018 coincident with the imposition of tariffs on Chinese-made solar panels and washer machines. Confidence has since fallen sharply. More tariffs are likely to exacerbate this trend in business confidence and bring down rates as a result.

The Federal Reserve is likely to be much more accommodating than they let on yesterday as a result of more tariffs. More trade policy uncertainty seems likely to kick the Fed into action and meet the bond market’s expectations for two more rate cuts in 2019 and possibly more still in 2020. Moreover, the 10-year to Fed Funds yield spread is still inverted by 35 basis points. In other words, the likelihood of a full on rate cutting cycle has increased and that of a “mid-cycle adjustment” has decreased. This is bullish for short-term as well as long-term government bond yields.