It was just over six months ago that we penned a piece about the then market sell-off, cautioning against knee-jerk reactions to short-term headlines such as “Worst December Since 1937” amongst others. Well, it did not take long. At 4:01 ET on Friday, June 28, a headline flashed across the Bloomberg terminal: “S&P 500 Has Best First Half of Year Since 1997.” This time around, we again urge calm, in this case against the fear of missing out, or FOMO. We often write about why we choose to be strategic investors, and will not rehash it all here, but there are reasons why these quarterly letters are littered with examples of failed short-term market predictions and “hot dot” chasing. They often miss the mark. The latest “hot dot” is an oldy but a goody, Initial Public Offerings (IPOs).

We are often asked by clients if they should invest in a given IPO and the question has come up a bit more often with the recent spate of high-profile debuts. First, a quick disclaimer. We are not saying IPOs are inherently bad. A lot of the negative pieces written about IPOs center around the tech bubble and associated frenzy, and while there is some of that happening today, the brush frequently paints too broadly. Equity markets need new names to evolve and grow. Ultimately, a fraction of these companies become part of the fabric of the public equity markets and a select few even go on to become the mega cap blue chips we all know and love today. But, and this is an important but, it’s a small fraction and rarely does that happen in a straight line.

We typically have very little actionable insight to a particular company, but we would offer the following thought experiment: what do Amazon, Twitter, Facebook, Uber, Snap, Apple, Spotify, Tesla, Dropbox, and Etsy all have in common? They ALL traded below their IPO price at some point, and by an average of 36%! For roughly the last 25 years, a full 85% of IPOs greater than $500mm have at some point traded below their IPO price. This is not a tech-only factoid. Household names like Nike, Coca-Cola, and Lockheed Martin (and hundreds of others) went through a similar post-IPO dry spell. Yes, Beyond Meat’s meteoric rise from its May 1, 2019 IPO is impressive, and it may be that exceptional, but it has been an outlier. Looking deeper at the data helps us see a clearer picture. From 1980 through 2016, IPOs on average underperformed the market over their first three years. That does not mean they go on to underperform into perpetuity, but the initial fervor of the IPO has been, more often than not, unwarranted. Aforementioned Twitter is a good case-in-point. It went public in late 2013 at $26, and after some initial success, traded well below its IPO price until early 2018.

As we look at IPO dynamics today, there are some unfortunate parallels to past follies, in particular, that nearly 80% of companies going public today have negative earnings. There have been more reasonable periods in the mid-2000s and 2010s where the numbers were not so skewed. FOMO is still concerning when companies with no earnings capture investor imaginations, but at least for right now, it’s on a somewhat smaller scale than the Tech Bubble era.

All this comes back to how we approach investing, which often translates to avoiding “hot dot” chasing and headline creep into portfolios. In short, we would counsel sticking with your financial plan and not chasing performance. It is probably a good time to reaffirm with your Advisor your risk profile, and to remind yourself of what a realistic good market scenario, and more importantly, a bad market scenario may look like.

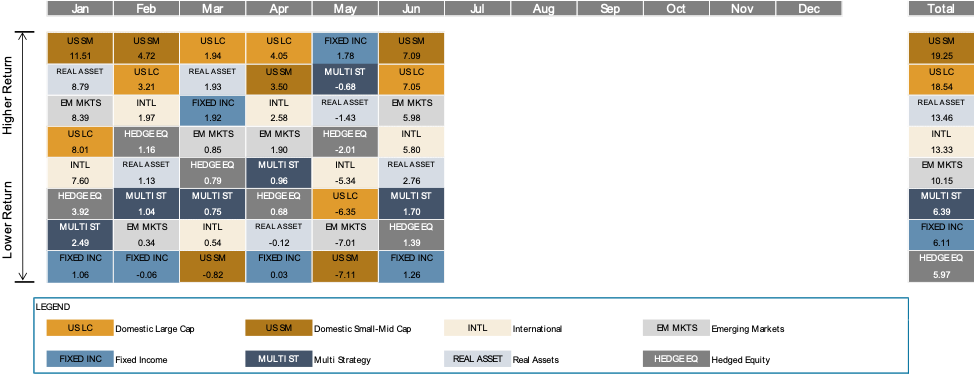

Markets

US large cap stocks were joined by small caps and international equity indices in returning +10% to +20% for the first half of 2019. Not to be left out, fixed income indices also registered robust gains, with the Barclays US Aggregate Index performing its best Jan 1- June 30 since 1995 at +6.1% and the Barclays Municipal Bond 1-12 year index returning +3.6%.

Alternative investments have generally kept up with fixed income in the first half of the year, but have broadly lagged the torrid pace of equities, particularly in the US. The major nuances come from underlying implementation, where strategies with significant exposure to higher yielding debt (both in the US and abroad) tended to outperform.

Other Notes and Takeaways

- The US consumer and economy seem like they continue to be relatively unscathed by the tariff noise and other geopolitical concerns. In its Regional Survey of Business Activity, published on June 25, 2019, the Richmond Fed indicated that “…manufacturing activity changed little” and “most firms reported some improvement in local business conditions, and they were optimistic that they would see growth in the next six months.”1 As you get further from the US consumer, however, data seems more worrisome, with slowing growth in many parts of the world. Chinese recent releases show more slowing than the US, highlighting that, at least in the data, the tariff spat seems to be impacting China more than the US.

- For the first time since the financial crisis, major Central Banks have been net shrinking their balance sheets. However, this period of policy normalization will likely come to end soon as the Federal Reserve ends shrinking its balance sheet and the Bank of Japan continues expanding theirs.

- The US household sector shows remarkable health, with debt payment as a % of disposable income the lowest since before 1980.

- Statistical Insignificance. Not all rate hike cycles look the same - in the last 5 cycles (1990, 95, 98, 01, 07) prior to the latest, the stock markets were up a year later three times and were noticeably lower two times.

- For all the recent IPO fervor the number of publicly traded companies is still nearly half of what it was in 1996 (4,336 vs. 8,090)

- The average Beyond Meat shareholder held the stock for less than 85 hours.

Bronfman E.L. Rothschild, LP is a registered investment advisor (dba Bronfman Rothschild) and wholly owned subsidiary of NFP Corp. Securities, when offered, are offered through an affiliate, Bronfman E.L. Rothschild Capital, LLC (dba BELR Capital, LLC), member FINRA/SIPC.

This information should not be construed as a recommendation, offer to sell, or solicitation of an offer to buy a particular security or investment strategy. The commentary provided is for informational purposes only and should not be relied upon for accounting, legal, or tax advice. While the information is deemed reliable, Bronfman Rothschild cannot guarantee its accuracy, completeness, or suitability for any purpose, and makes no warranties with regard to the results to be obtained from its use. Past performance does not guarantee future results.

© 2019 Bronfman Rothschild

1https://www.richmondfed.org/-/media/richmondfedorg/research/regional_economy/surveys_of_business_conditions/manufacturing/2019/pdf/mfg_06_25_19.pdf

Read more commentaries by Sontag Advisory