Weighing the Week Ahead: Are You Part of the Dumb Money?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar is light but includes some home sales data and the (old news) Q2 GDP first estimates. Fed speakers will be on the sidelines for the pre-meeting quiet period. Earnings reports remain the most important fresh data for both traders and investors. And of course, there is always the chance of a tweet or two.

In quiet times the punditry loves to look at the markets through the prism of a bull-bear debate. I am seeing some new takes on both sides, but the most colorful is the question:

Are you part of the “Dumb Money?”

Last Week Recap

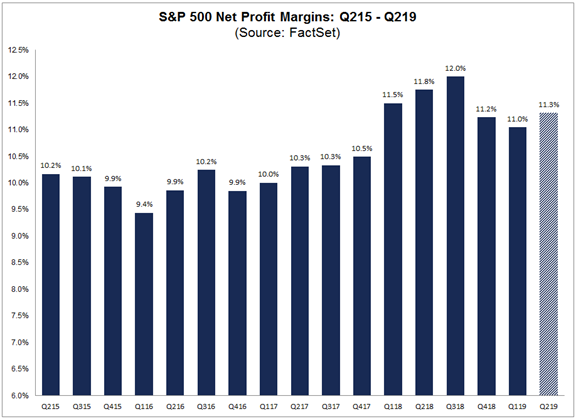

In last week’s installment of WTWA, I asked how much global economic weakness was affecting corporate earnings. We still don’t have a definitive answer to that question, but it certainly was a hot topic. FactSet’s John Butters reports that earnings are down -1.9% year-over-year but revenues are up 3.8%. This raises concerns about declining net profit margins, a long-time market worry.

Stay tuned!

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski’s version, which combines a lot of information in one picture. The full article also includes several other interesting takes on price movement.

The market declined 1.2%. The chart looks choppy, but the trading range was only 1.5%. Those watching closely were treated to breathless media commentary about moves of less than 1%. Friday’s trading was influenced by a clarification (walking back?) of NY Fed President John Williams, whose need to “act quickly” comment was clarified as an inference from academic research, not a hint of policy actions. My weekly Quant Corner translates this into a volatility calculation which you can compare both to VIX and to past readings.

Noteworthy

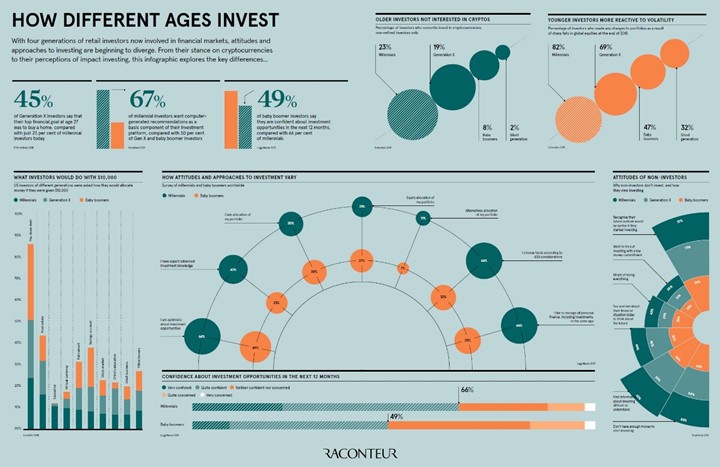

The Visual Capitalist looks at how four generations of retail investors differ in their perceptions.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators are an important part of our regular research. There are three different groups corresponding to different time frames. It has been a long time since all three groups have been positive. The long-term forecast has been seeing improvement for many reports, but NDD warns about the volatility in the short-term indicators.

The Good

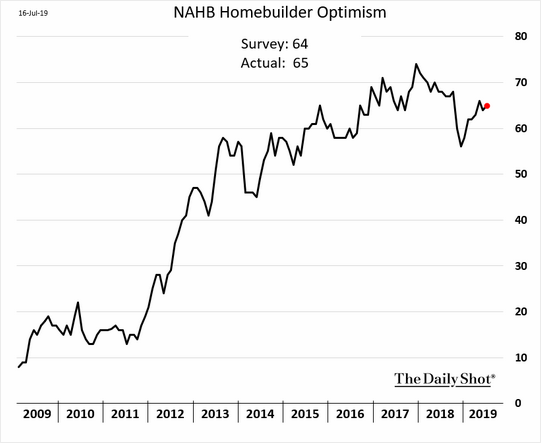

- The NAHB housing market index registered 65, up a tick from June and beating expectations of 62.

- Retail sales increased 0.4%, equaling May’s gain and beating expectations of 0.2%. Ex-auto the results were the same.

The Bad

-

Industrial production showed no gain versus expectations of 0.2% and May’s 0.4%.

-

U.S. – China trade talks are “stuck in a rut over Huawei.” (WSJ)

-

Mortgage applications declined -1.1% versus last week’s -2.4%.

-

Rail traffic continues in deep contraction in Steven Hansen’s (GEI) economically intuitive sectors. Rail earnings were somewhat mixed with CSX earnings missing and UNP beating.

-

Leading economic indicators declined -0.3%

in June. Prior and expectations were both for 0.0%.

-

Housing starts for June were 1253K (SAAR) versus expectations of 1270K and last month’s 1265K. Barron’s sees the combination of lower rates and lower prices as the cause for an end to the home building downturn. Brian Wesbury writes, “…the details in the report continue to signal life in homebuilding.” And of course, Calculated Risk, now looking for better starts in 2019 than in 2018.

-

Building permits were only 1220K (SAAR), significantly lower than expectations and the May report of 1300K. Eric Basmajian emphasizes permits over starts and notes that lower interest rates did not help in June.

The Ugly

Ebola, now designated as a public health emergency of international concern by the World Health Organization. Drug companies are donating vaccine doses, but the potential recipients do not trust providers. The crisis has turned into a political cause for many. (Council on Foreign Relations).

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

The economic calendar is light, featuring data on home sales. The first estimate of Q2 GDP will make headlines, but it is “old news” that will be revised as more data come in. Fed participants are in the quiet period before the next meeting, so those seeking commentary from public officials must depend upon Congress and the President. The biggest news will come from the continuing earnings reports.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

In quiet times the punditry fills the news vacuum with provocative questions. A favorite is a bull/bear debate. These have taken on a new edge. Despite the earnings news, many of the A players are in the Hamptons. This might not be the only question in the debate, but it will be popping up in thinly disguised form. Expect pundits to be asking:

Are you part of the dumb money?

Background

There has been a slight change in pundit tone. There is a broader acknowledgement that the apocalyptic predictions are overdone. I was wondering if I had imagined this, until I read others on the same track.

-

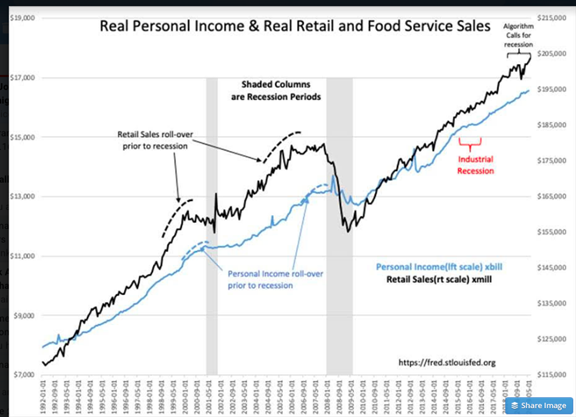

Gradually those voices urging investors to ‘do something’ to avoid the ravages of recession have faded away. There are still a few loud voices, but far fewer than 6mos ago. Real Retail and Food Service Sales reported this morning include several upward revisions and are the highest on record. Real Personal Income for May 2019 is a record high. CNBC continues to focus on economic weakness when very little weakness exists in data.

- Barron’s!! The Up and Down Wall Street column is a long-term home for “reliably bearish comments.” Andrew Bary suggests, Why Stocks Are Still the Best Investment, Even After a 10-Year Run.

You must read it to believe it.

How is this playing out? Here are a few examples.

Some Bears

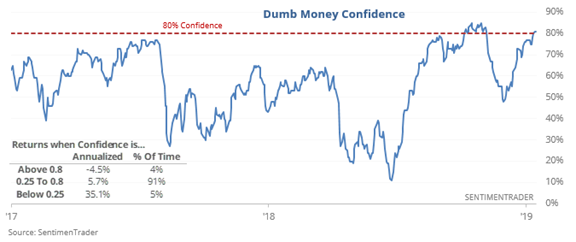

Inspiring today’s theme is Jason Goepfert, who writes The Dumb Money Is Nearing Maximum Confidence.

This is a clever name, but the indicator does not identify any group of bad investors and create a testable hypothesis. It does some back fitting of indicators.

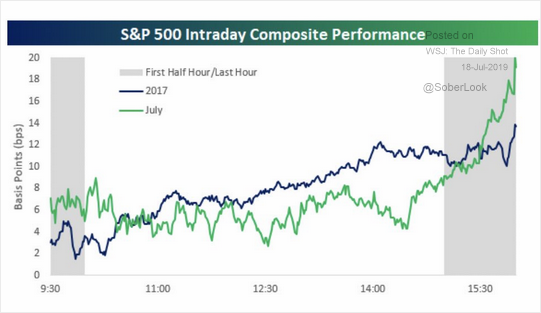

Another recently popular indicator was the “smart money” version. The idea for this one is that “dumb money” represented by individual investors trades at the start of the day while the pros trade late. Here is a good explanation citing the Bloomberg calculation.

But something has changed! Those early-day traders are doing better.

Instead of including a few more such links, I’ll just refer you to John Mauldin. He cites a number of his friends showing that a recession may have already started or will very soon, the yield curve is worse than you think, earnings and productivity are terrible, Mr. Buffett does not know how to interpret his own indicator, global weakness has made us vulnerable, and the Fed has blundered by not following Mauldin’s advice months ago. (Methinks Mr. Mauldin needs some friends who are more bullish. Everyone he cites has earned a place on my Twitter list of “reliably bearish commentators.”

Some Bulls

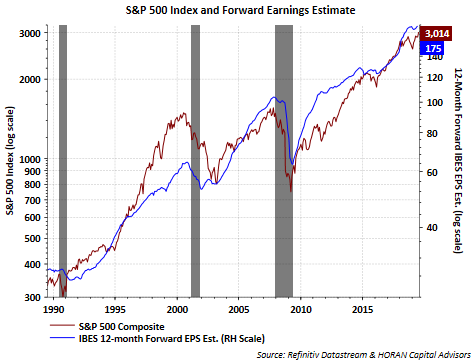

David Templeton (HORAN) sees a continuing rally led by growth in expected earnings.

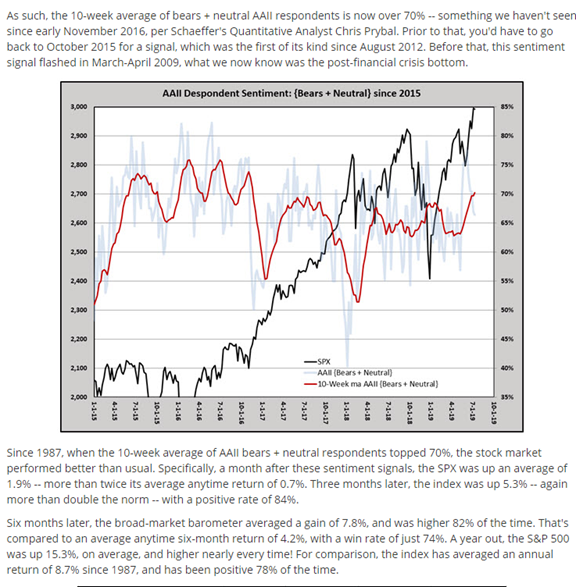

Brian Gilmartin reports on Bernie Schaeffer’s “Despondent Survey,” drawing a bullish conclusion from the extraordinary reading.

The Market reaction

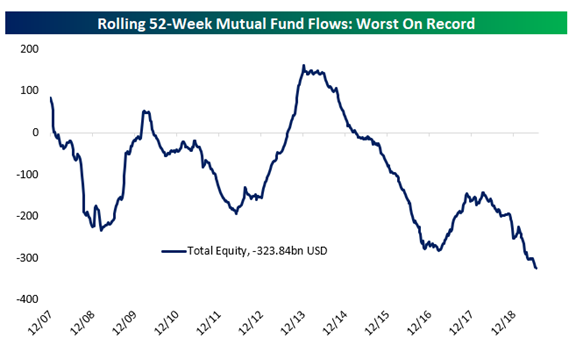

Investors are selling stocks. Bespoke writes that there are Record Outflows from Equity Mutual Funds.

David Templeton notes, Investors Are Selling Equities: Not A Typical Behavior At Market Tops.

I’ll cover my own conclusions in today’s Final Thought.

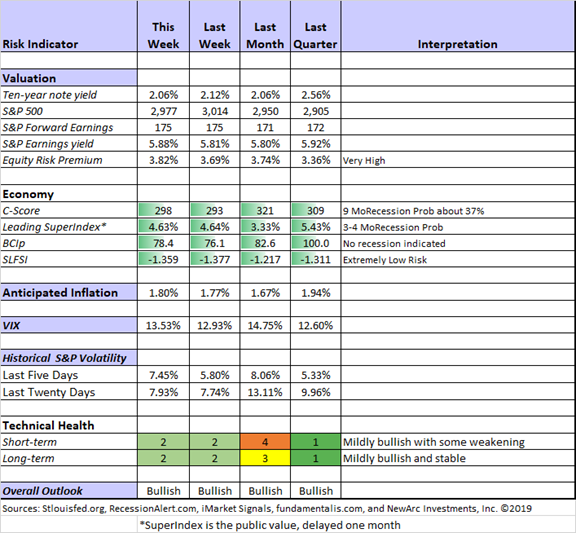

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

Our technical market indicators, both long and short term, remain mildly bullish.

Recession risk is still in the “watchful” area.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

RecessionAlert: Strong quantitative indicators for both economic and market analysis

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis.

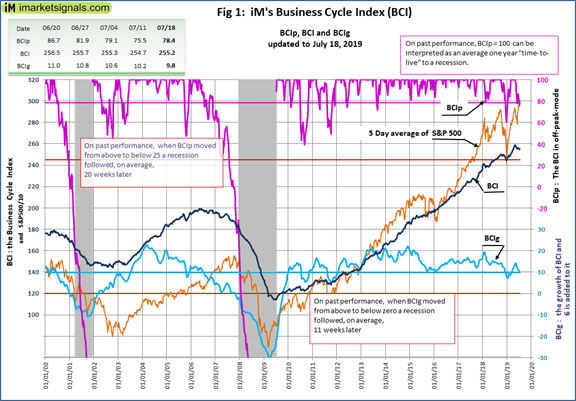

Georg Vrba: Business cycle indicator and market timing tools. The most recent update of Georg’s business cycle index does not signal recession.

Guest Sources

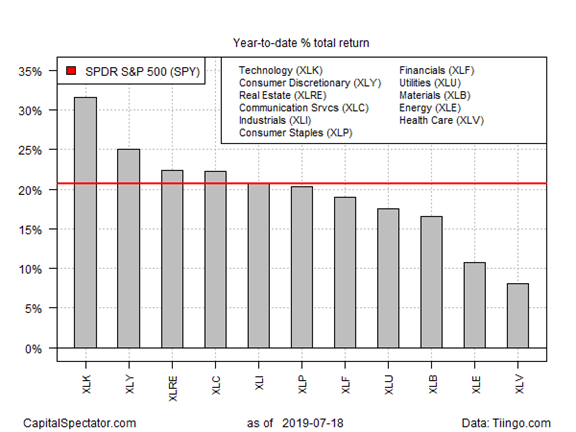

James Picerno reports on tech leadership in the 2019 rally. This is a crucial point for those choosing stocks and sectors.

Insight for Traders

Our weekly “Stock Exchange” series is shifting to a publication date earlier in the week. I am doing this to create more separation between the stocks discussed and our own adjustments. While we warn investors that these are just ideas. They are not intended for readers to follow without research or determining the suitability for their portfolios. We also warn that we may trade out of positions without notice. Even with all of that in mind, a little more separation between publication and trading would be better. Regular readers can look for a new installment on Tuesday.

Insight for Investors

Investors should understand and embrace volatility. They should join my delight in a well-documented list of worries. As the worries are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely.

Best of the Week

If I had to recommend a single, must-read article for this week, it would be Marc Gerstein’s Finding Stocks Worth Evaluating, The Most Important And Typically Overlooked Task. I like to highlight great ideas that are often overlooked. Marc’s experience shows in this analysis.

“Before we decide whether a stock is good, bad or in between, we need to decide which stocks to look at. This is a critical and typically under-appreciated step. If you squander your time and resources looking at stocks that aren’t worthy of being considered, you’re setting yourself up for failure before you even start. On the other hand, if you can focus your efforts on a collection of stocks that has been sensibly pre-qualified much the way a successful salesperson tries to pre-qualify leads rather than calling on every name that pops up at random, you’re much better positioned for success.”

Then he quotes the legendary Peter Lynch who wrote, “If I could avoid a single stock, it would be the hottest stock in the hottest industry, the one that gets the most favorable publicity, the one that every investor hears about in the carpool or on the commuter train—and succumbing to the social pressure, often buys.” Marc observes that this mistake is made by investors who get their ideas from financial television.

He follows this with some great examples and his own approach to narrowing your universe. There is a lot of value here, so don’t skimp. Read the full post.

Stock Ideas

Chuck Carnevale has an excellent update of his principles for managing an investment portfolio. As always, he combines great lessons, strong data, and helpful ideas.

Lyn Alden Schwartzer concludes, It’s Time to Take a Look at Invesco. As usual, she has a careful, data-driven explanation. It includes good comparisons with other asset managers.

Want to bet on Europe? James Henshaw highlights an interesting choice, Ashted Group (ASHTF). This is not trading on a major US exchange, which does not carry the stigma it once did. The company is a major participant in the US equipment rental business.

Eddy Elfenbein, who has the most transparent and frequently updated portfolio, analyzes some earnings results in his stock. He adjusts buy prices and targets as needed. Everyone is free to peruse his list, or you can simply join me in owning his ETF (CWS).

Bhavneesh Sharma tempts us with Fate. Fate Therapeutics, that is. He has a knack for explanation of key points. Here you can learn about induced pluripotent stem cells (iPSCs) as well as the potential for the stock. Bhavneesh covers the pipeline possibilities, current burn rate, and cash on hand.

William Stamm makes the case for Johnson and Johnson, a defensive name with growing earnings. He sees the impact from current lawsuits as overdone.

Jon C. Ogg (24/7 Wall Street) analyzes 10 Dividends That Can See Double-Digit Growth for 5 Years or Longer.

Personal Finance

Abnormal Returns is the go-to source for anyone serious about the investment business. The Wednesday edition has a special focus on personal finance, with plenty of ideas for the individual investor. I especially enjoyed Patrick Runyen’s advice about retiring to a low tax state, perhaps because that is on my personal agenda. There is plenty of practical advice about what you need to do to establish residence and how to do research.

John Yeigh’s discussion of stock options affects fewer people, but it is crucial for many. This topic is often neglected until it is too late. If you leave a company and you are loaded up with options, you should think about hedging alternatives. You might be surprised at the choices available.

Readers may also have a special interest in the Saturday edition, which covers an array of topics you have probably not seen elsewhere. I must use care to stay and my writing task and save these interesting links for later!

Watch out for…

Netflix (NFLX). Barron’s opines that the company’s troubles have just begun. Reasons: Subscriber loss and new competition.

Annuities. Karen Hube (Barron’s) describes the improvements in this product, but also provides a guide about what to watch for.

Final Thought

No one should be worried about name calling, a staple of certain web sites. I understand that “sheeple” and “bag holder” are other popular terms used by those who have missed all or most of the market rally. Many of those thought to be part of the “smart money” are lagging badly this year.

The Reasoning

I agree about one aspect of this. Beating the market right now might not be such a good idea. For one thing, it shows that you are violating Peter Lynch’s advice in our best of the week investment commentary (above). For more detail, check out my post on what you should be watching. You can have great market returns, but you must gear the results to your personal needs. The return for solid choices does not work like a railroad schedule.

Alan Steel has a gift for explaining this in a colorful and entertaining fashion. Check out his leading quotations. Among his many excellent points, I especially liked these two drawn from Benjamin Graham.

- In a 1963 lecture “he expressed concern over the excessive share prices of some “hot” stocks in the US, predicting a sharp return to “reality.”

- And “…It’s possible for investors to get significantly better returns than the average. But two conditions are necessary. One, they must follow sound principles of selection related to the value of the securities and not their market price action. The other is to cut themselves (emotionally) off from the general public…. thinking differently from the crowd.”

The Errors

These raise my blood pressure because I know that some people take them seriously.

- The strong early 2019 rally, and why this is a cause for worry. This is the old tactic of choosing the best starting point for your argument, helped this time by the calendar. The bogus recession concerns of last December are surely part of this story. What would we expect after the worst December in 85 years?

- The claim that “we might already be in recession.” This is supported by the popular notion that “the government did not recognize the 2007 recession until it was over.” Or it might be the Fed cited as the offender. These statements all reveal either complete ignorance of how recession dating works or a willingness to deceive for profit.

- The ever-rotating indicators, finding whatever proves the point right now.

- The argument that good news is bad news.

The Potential

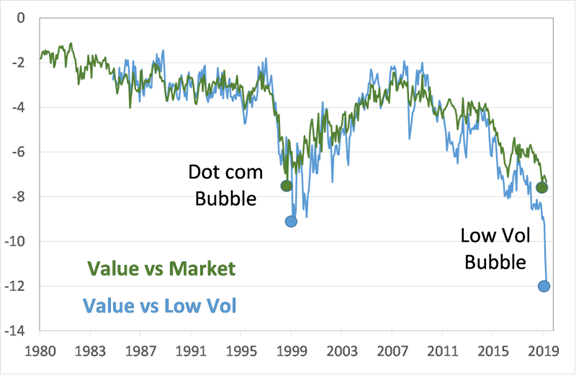

I have frequently written about the concept of “upside risk.” Now there are influential voices joining in. JP Morgan’s influential Marko Kolanovic calls the right investment strategy a “once in a decade opportunity.” What is that strategy? Playing for the record gap between value/cyclical stocks and low volatility/defensive stocks to do some mean reversion. He sees this gap as wider than the dot-com bubble overshoot.

The Buy and Hold “Dummies”

I personally believe in reducing risk when objective indicators flash a warning. Headline news is just the opposite. But what about buy and hold? Sarah Ponczek (Bloomberg explains). Investors Trading to Prep for the Big One Should’ve Stayed Still.

Investors lose whether they retreat to defensive sectors, try to time the market, or buy protection. The “strategy of buying bearish index options has a ‘pathetic’ record of effectiveness.” (Quoting a paper from AQR Capital Management).

Healthy debate about the market is normal. The number of completely inaccurate statements from prestigious sources is on the rise. The ability to correct these is declining.

Some other items on my radar

I’m more worried about:

- The July Fed meeting. Everyone sees a cut as 100%, but everyone has consistently been more pessimistic on the economy than the Fed. See “Davidson’s” take, The Fed Could Do Nothing.

- The debt ceiling increase. It is still supposedly needed by September. This would occur before Congress returns from its summer recess. Meanwhile, legislative cooperation is in short supply. The parties have switched sides on this issue. Expect plenty of efforts to tack on unrelated matters and creative ways to stretch the deadline. Let us hope there is not another shutdown.

I’m less worried about

- Fundamental economic factors. Baseline growth is a bit lower, but still looks like over 2% for the year.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits