Gold Heats Up and Silver Joins the Race

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Now that gold has broken through the $1,450 an ounce level, a six-high year high, the next big test is $1,500. And as I’ve said before, it can do this in the blink of an eye under the right conditions.

We may end up seeing those conditions emerge sooner rather than later.

On Thursday, Federal Reserve Bank of New York President John Williams seemed to indicate that a rate cut could be expected later this month, saying that central bankers need to “act quickly” as economic growth cools. Although he later clarified his comment, claiming he was simply citing research and not forecasting central bank action, the price of gold jumped as much as 2 percent on the news before closing above $1,440 for the first time since May 2013.

Investors took some profits on Friday, knocking the price down around 1 percent after gold started to look overbought a day earlier. The metal was up two standard deviations over the past 60 trading days, its highest level since April 2016. I would consider each pullback such as this a buying opportunity, though, because I believe the best is yet to come for the metal.

Ray Dalio seems to agree. In a lengthy post on LinkedIn—Dalio’s favorite platform for getting the word out—the billionaire hedge fund manager writes that he thinks we’re on the verge of a new economic paradigm shift and that central banks’ accommodative policies, from low rates to quantitative easing (QE), are unsustainable. To hedge against this, Dalio says, “I believe that it would be both risk-reducing and return-enhancing to consider adding gold to one’s portfolio.” Most investors are underweighted in gold, “meaning that if they just wanted to have a better balanced portfolio to reduce risk, they would have more of this sort of asset,” he writes.

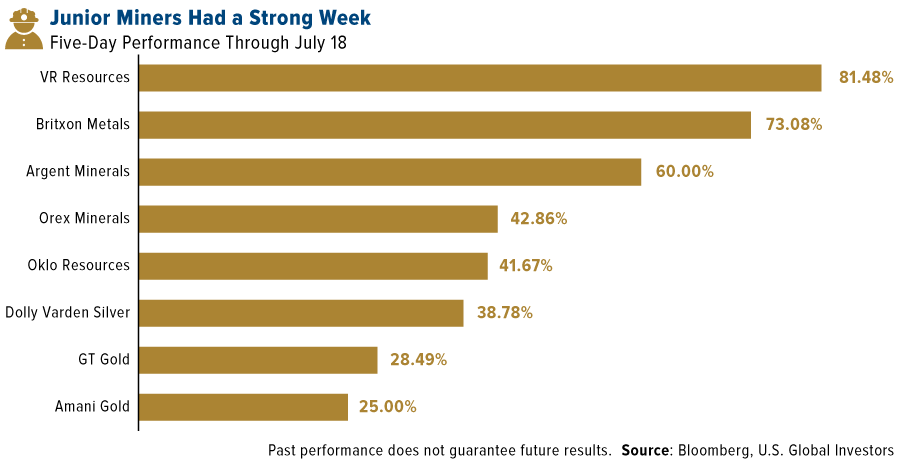

A Monster Rally for Juniors

Select junior and micro-cap gold and precious metal miners also posted very strong growth over the past week, mostly on positive drilling results. In a press release dated July 15, Brixton Metals announced encouraging results at its wholly owned Thorn Gold-Copper-Silver Project in British Columbia. Gary Thompson, chairman and CEO of the Vancouver-based explorer and developer, said that Brixton “continues to unlock a mountain of value” at the property, which exhibits even greater mineralization than was previously thought.

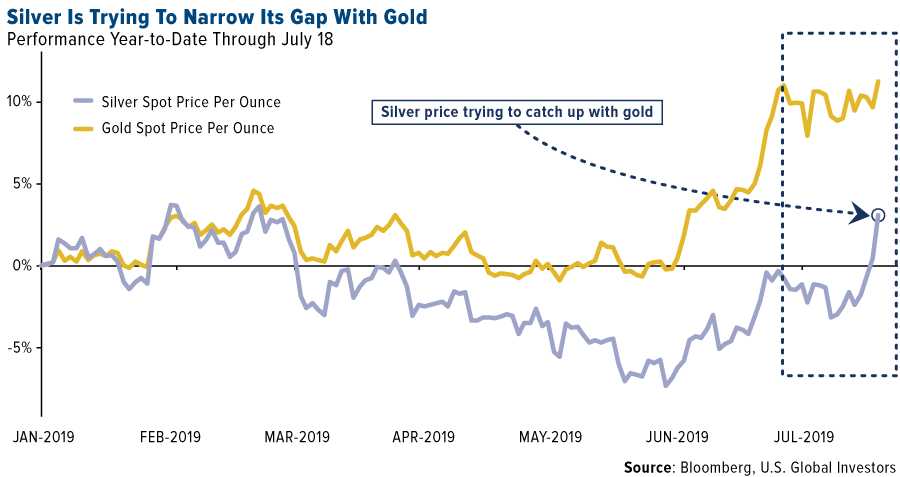

As for silver, I’m pleased to see that it’s finally playing “catch up” to gold, its price having hit a 52-week high after an incredible six straight days of gains.

The Bullish Calls on Gold Continue

With gold having already broken out of its five-year trading range, is the best still yet to come? I believe it is. And I’m not alone. Read what some analysts and strategists have to say:

Alpine Macro

“The Fed is getting ready to cut interest rates, which should set in motion a multi-year bear market in the dollar,” write analysts at Alpine Macro in a research note dated June 28. A weaker U.S. dollar is one of three “key ingredients” for a bull market, according to Alpine Macro, the other two being a more accommodative Fed and rising geopolitical risks.

“The technical break above $1,400 an ounce is a positive sign,” the firm adds. “New all-time highs for gold should be seen in the coming years.”

World Gold Council (WGC)

“The prospect of lower interest rates should support gold investment demand,” the World Gold Council (WGC) says in its mid-year outlook. “Our research indicates that the gold price was higher in the 12 months following the end of a tightening cycle. Moreover, historical gold returns are more than twice their long-term average during periods of negative real rates—like the one we are likely to see later this year.”

Canadian Imperial Bank of Commerce (CIBC)

“We continue to see no signs of rate hikes on the horizon over the next several years, and historically have seen gold continue on an upward trajectory beyond the last rate cut,” writes CIBC in a note dated July 14.

The bank points out that in two previous gold bull market cycles—in the 1970s and 2000s—negative real rates were the main contributing factor.

“During the last two major periods when real rates stayed below the 2 percent level and actually ticked into negative territory, the gold price moved over 320 percent in the 1970s… and approximately 400 percent from 2004 to peak in 2011.”

Looking to make sense of the markets? Subscribe to my award-winning Frank Talk CEO blog! Click here to sign up!

Gold Market

This week spot gold closed at $1,425.37, up $9.62 per ounce, or 0.68 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 6.94 percent. The S&P/TSX Venture Index came in up just 2.77 percent. The U.S. Trade-Weighted Dollar rose 0.33 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jul-16 | Germany ZEW Survey Current Situation | 5.0 | -1.1 | 7.8 |

| Jul-16 | Germany ZEW Survey Expectations | -22.0 | -24.5 | -21.1 |

| Jul-17 | Eurozone CPI Core YoY | 1.1% | 1.1% | 1.1% |

| Jul-17 | Housing Starts | 1260k | 1253k | 1265k |

| Jul-18 | Initial Jobless Claims | 216k | 216k | 208k |

| Jul-24 | New Home Sales | 658k | -- | 626k |

| Jul-25 | Hong Kong Exports YoY | -2.3 | -- | -2.4% |

| Jul-25 | ECB Main Refinancing Rate | 0.000% | -- | 0.000% |

| Jul-25 | Durable Goods Orders | 0.8% | -- | -1.3% |

| Jul-25 | Initial Jobless Claims | 220k | -- | 216k |

| Jul-26 | GDP Annualized QoQ | 1.8% | -- | 3.1% |

Strengths

- The best performing metal this week was silver, up 6.40 percent on perhaps a paradigm shift as the investors poured $133 million into silver bullion ETFs on Wednesday, the single biggest inflow in six and a half years. The weekly Bloomberg survey of gold traders and analysts shows that most are bullish on the yellow metal as prices broke through a five-year high and touched $1,453 per ounce on Friday morning. Traders seem to be set on an interest rate cut from the Federal Reserve this month, which is helping gold, even as some better-than-expected economic data was released on Tuesday. Turkey, which often sells its gold, saw its reserves rise by $71 million this week compared to last.

- The Perth Mint left a $45 million gold coin on display in Manhattan on Tuesday. The coin, which measures 32 inches in diameter and is almost five inches thick, weighs 2,200 pounds. Perth Mint CEO Richard Hayes says that the rise in U.S. sovereign debt has been a big and largely overlooked factor in surging gold prices, reports the Financial Review.

- After a long spat, Acacia Mining and Barrick Gold have reached a deal for Barrick to buy the roughly 36 percent stake in Acacia that it didn’t already own, reports Bloomberg. The offer is a 24 percent premium to the company’s closing price on Thursday. Now that this dispute has been resolved, hopefully Acacia and the Tanzanian government can mend their relationship.

Weaknesses

- The worst performing metal this week was palladium, down 2.49 percent as hedge funds cut their net bullish position, perhaps rolling some of the proceeds to silver. Gold exports from Europe’s major refining hub, Switzerland, fell a whopping 55 percent in June to the lowest since at least 2011. This is due to smaller shipments to China and India, the world’s two largest consumers of gold, on the back of higher gold prices.

- Venezuela is defying sanctions once again and selling off its gold reserves. The troubled South American nation sold $40 million in reserves last week, nearly one ton, lowering its dollar reserves to a near three-decade low of $8.1 billion. President Maduro has sold approximately 24 tons of gold to places such as the United Arab Emirates and Turkey since April, according to Bloomberg.

- Even as gold is soaring to multi-year highs, investments into gold-backed ETFs don’t seem to be going anywhere. Looking at the SPDR Gold Shares ETF, cumulative demand since the start of 2018 doesn’t show a big rush to own bullion yet. Additionally, investors are selling out of gold miner ETFs which have underperformed their rivals; mutual fund asset managers in the precious metal miners sector have significantly outperformed the ETF products.

Opportunities

- In an essay posted on LinkedIn this week, billionaire investor Ray Dalio writes that he believes “it would be both risk-reducing and return-enhancing to consider adding gold to one’s portfolio.” Dalio adds that he sees a “paradigm shift” coming in the next few years as a huge amount of debt and non-debt liabilities come due and can’t be funded with assets. SkyBridge Capital said it is considering investing in gold for the first time since exiting in 2011 due to Fed interest rate cuts. Bloomberg published a piece this week saying that sub-zero real yields are boosting the rush into gold – since gold’s lack of yield doesn’t matter when the pile of negative-yielding bonds continues to grow. Lastly, Deutsche Bank says that should U.S. foreign exchange policy start a currency conflict, the best option is to hold gold.

- According to a survey of central banks conducted by the World Gold Council (WGC) and YouGov, 54 percent of respondents expect global holdings of gold to climb in the next 12 months due to concerns about risks in other reserve assets. WGC said that “this year’s survey signals another healthy year of central bank gold demand” after central banks bought the most gold in 2018 since 1971.

- Silver finally got some attention from investors this week. Bloomberg’s Eddie van der Walt writes that silver has been in gold’s shadow for eight years now and that the price ratio between the two rose above 93 this month – a level not seen since 1992. National Bank Financial analysts Don DeMarco said that when the ratio falls below 90, which it did on Tuesday, the average one-year return for silver is 22 percent and 10 percent for gold. The silver spot rose about 6.40 percent this week. Exploration stocks and silver miners also saw exceptionally strong price performance throughout the week.

Threats

- Venezuela continues to attempt to evade U.S. sanctions. According to sources familiar with the matter, Venezuela is mulling over using a Russian-operated international payments messaging systems as an alternative to SWIFT.

- De Beers, the world’s largest diamond producer, continues to see demand fall and is cutting production. Bloomberg reports that the company plans to mine 31 million carats in 2019 – at the bottom end of a previous forecast range. Diamond sales from January to June have fallen for four consecutive years.

- President Trump said this week that his administration will “take a look” at Peter Thiel’s allegations that Google’s work with China is “seemingly treasonous,” writes Bloomberg’s Terrance Dopp. Thiel is a board member of Facebook. More investigations into the big tech companies could spell trouble for the markets overall.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.65 percent. The S&P 500 Stock Index fell 1.23 percent, while the Nasdaq Composite fell 1.18 percent. The Russell 2000 small capitalization index lost 1.41 percent this week.

- The Hang Seng Composite gained 1.06 percent this week; while Taiwan was up 0.45 percent and the KOSPI rose 0.37 percent.

- The 10-year Treasury bond yield fell 7 basis points to 2.047 percent.

Domestic Equity Market

Strengths

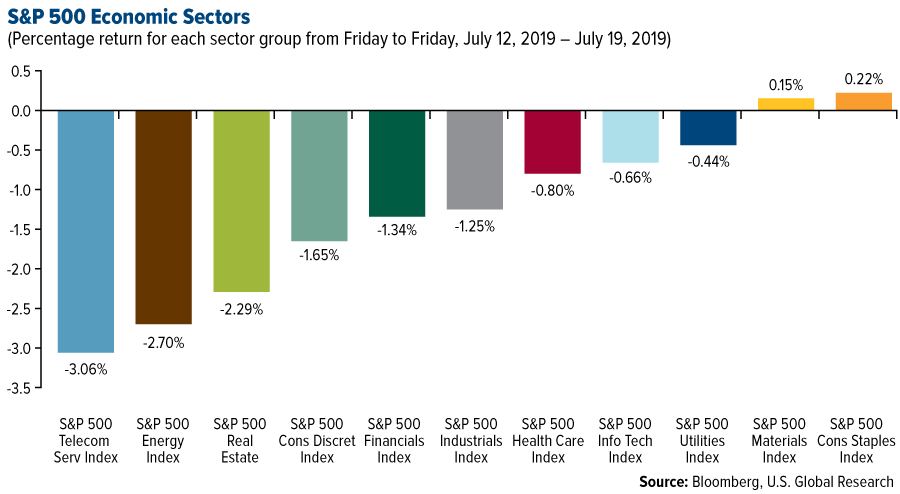

- Consumer staples was the best performing sector of the week, increasing by 0.22 percent versus an overall decrease of 1.17 percent for the S&P 500.

- Hunt (JB) Transport Services was the best performing stock for the week, increasing 11.62 percent.

- Microsoft blew away Wall Street estimates in its most recent quarter, growing its revenue by 12 percent from last year.

Weaknesses

- Health care was the worst performing sector for the week, decreasing by 1.43 percent versus an overall decrease of 1.17 percent for the S&P 500.

- Netflix was the worst performing stock for the week, falling 15.58 percent.

- Netflix lost more than $15 billion of its market cap after suffering a decline in U.S. subscribers, the first since 2011.

Opportunities

- PepsiCo is planning to acquire South Africa's Pioneer Food Group for around $1.7 billion, reports Business Insider, as it targets expansion in Africa. The company said the move would boost manufacturing and go-to market capabilities in Sub-Saharan Africa, as well as "enable scale and distribution."

- Beyond Meat is just the beginning of food substitutions. According to Business Insider, dairy alternatives are set to boom to a $38 billion market. Dairy-free cheese sales rose 20 percent in the year to April to $160 million in the U.S., and yogurt sales grew almost double that, by 39 percent to $230 million.

- Bayer rallied after a judge slashed a payout over its cancer-linked Roundup weed killer by $55 million. Bayer's stock climbed as much as 3 percent on Tuesday, after the original ruling of $75 million was cut to $20 million.

Threats

- If President Trump intervenes in the $10 billion JEDI cloud contract, both Amazon and Microsoft could end up as losers. The Pentagon looked set to announce the winner of the $10 billion JEDI cloud contract in late August, with Amazon Web Services widely expected to walk away the winner.

- Stocks are dropping as traders worry about the US-China trade war, Iran tensions and weak earnings. "We have a long way to go as far as tariffs where China is concerned," President Donald Trump said on Wednesday, adding his administration was willing to extend tariffs to another $325 billion worth of Chinese goods.

- The European Union (EU) launched a big anti-trust probe into Amazon, which could lead to a fine of up to $23 billion. The investigation is set to examine whether Amazon's use of data from the independent retailers that sell on its marketplace is in breach of EU competition rules.

The Economy and Bond Market

Strengths

- U.S. retail sales increased more than expected in June, writes Reuters, pointing to strong consumer spending. The Commerce Department said on Tuesday retail sales rose 0.4 percent last month. Economists polled by Reuters had forecast retail sales edging up 0.1 percent in June.

- Even in the face of rising economic headwinds that are likely to spur the Federal Reserve to cut interest rates in a few weeks, the consumer sentiment survey rose to 98.4 this month, reports MarketWatch. That is up from 98.2 in June, according to a preliminary reading from the University of Michigan.

- The Philadelphia Fed Manufacturing Business Outlook Survey rebounded 21.5 points in July, crushing the 4.5 consensus forecast.

Weaknesses

- The leading economic index fell 0.3 percent in June to mark the biggest decline in three years, reports MarketWatch, suggesting U.S. growth is likely to be softer in the months ahead. "As the U.S. economy enters its 11th year of expansion, the longest in U.S. history, the LEI suggests growth is likely to remain slow in the second half of the year," said Ataman Ozyildirim, director of business cycles research at the board.

- U.S. mortgage applications decreased last week as some home borrowing costs climbed to their highest level in a month, the Mortgage Bankers Association said on Wednesday. The seasonally adjusted index fell 1.1 percent to 500.2 from 505.8 in the week ended July 12. The group’s barometer on loan applications for home purchases, which is seen as a proxy on future housing activity, decreased 3.8 percent to 265.1, reports Reuters.

- U.S. industrial output was flat in June, writes the Wall St. Journal, as increases for the manufacturing and mining sectors were offset by a decline in utilities output. That fell short of economists’ expectations for a seasonally adjusted 0.2 percent increase last month.

Opportunities

- The advance GDP report for the second quarter will be the focal point next week as investors are split on the likelihood of a 50 basis point rate cut by the Fed at the next meeting. Following the stronger-than-expected retail sales figures earlier this week, a beat in second quarter growth forecasts is possible.

- IHS Markit will release flash PMIs for the month of July on Wednesday, along with durable goods orders. Durable goods orders are forecast to have increased by 0.5 percent month-on-month in June, recovering partially from the 1.3 percent drop the prior month.

- The European Central Bank (ECB) is expected to keep monetary policy unchanged on Thursday but is widely anticipated to update its forward guidance to signal some form of easing at its next meeting in September. Futures markets are predicting there are more than even odds that the ECB will trim rates by 10 basis points next week, while a reduction in September is fully priced in. Many analysts think the ECB will also restart its QE program to fight persistently low inflation and a deteriorating economic outlook.

Threats

- China’s portfolio of U.S. bonds, notes and bills fell by $2.8 billion to $1.11 trillion in May, according to Treasury Department data released Tuesday in Washington. As Bloomberg reports, this marks the third straight month of declines, leaving the nation’s holdings at the smallest since May 2017 amid an escalation of the trade war between the world’s two largest economies. China is still the largest creditor to the U.S., followed by Japan.

- The housing market will fall under the spotlight next week amid signs of renewed weakness in the sector. Starting on Tuesday are the monthly home price index (May) and existing home sales (June), followed by new home sales (June) on Wednesday.

- The flash eurozone PMIs for July will be grabbing the headlines on Wednesday amid mixed signals about the euro-area economy.

Energy and Natural Resources Market

Strengths

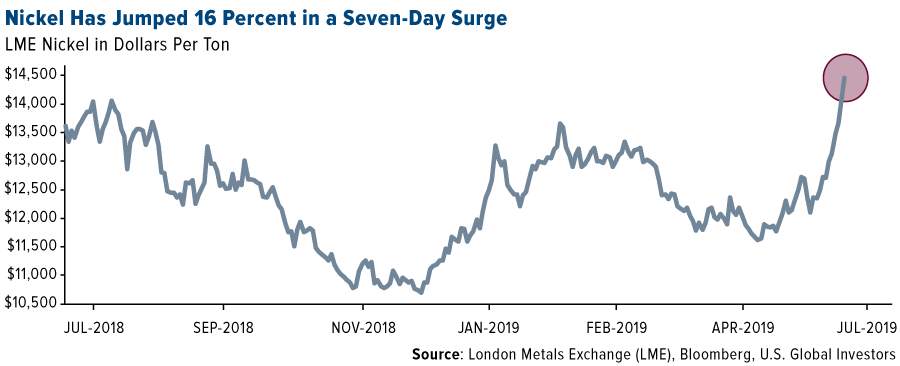

- The best performing major commodity for the week was nickel, gaining 10.50 percent on strong demand out of China. On Thursday, nickel climbed as much as 4.20 percent to $15,000 a tonne on the London Metals Exchange. The metal even jumped 16 percent in seven days, as of Thursday, although it backed down slightly Friday morning.

- Iron ore also had a good week, jumping to a five-year high on supply worries and record output of steel in China. President Trump signed an order requiring that 95 percent of steel and iron used in government contracts be American sourced, which should be positive for domestic demand.

- Bloomberg reports that Barrick Gold Corp and Antofagasta Plc were awarded $5.8 billion in damages from Pakistan over a disputed mining license for a copper and gold project dating back to 2011. A feasibility study showed that the Reko Diq project is one of the largest undeveloped copper and gold deposits in the world. Although there are questions surrounding who will begin to build out the project and when, the settlement is positive for both companies and the mining industry.

Weaknesses

- The worst performing major commodity for the week was natural gas, which fell 7.95 percent as anticipated milder weather will cut short the staying power of the current heat wave. On Wednesday, President Trump said there’s “a long way to go” for a trade deal with China and that he could impose more tariffs on Chinese imports if he wanted to. Bloomberg reports that copper led most metals lower following the comments. Metals also came under pressure after China reported increases in copper, lead and zinc output. According to Panama Canal Authority CEO Jorge Luis Quijano, cargo from the U.S. to China through the canal has fallen this year due to China cutting its imports. Japan is now the canal’s second-biggest user, with the U.S. at number one.

- De Beers, the world’s largest diamond producer, continues to see demand fall and is cutting production. Bloomberg reports that the company plans to mine 31 million carats in 2019 – at the bottom end of a previous forecast range. Diamond sales from January to June have fallen for four consecutive years.

- The world’s biggest oil processor, China Petroleum & Chemical Corp. known as Sinopec, has been hit by the growing fuel glut in Asia. Bloomberg reports that the company plans to process less crude into fuels in the third quarter of this year due to ample supplies weighing on margins. Meanwhile, crude output from the Permian Basin is starting to wane. Oil flows are set to increase by less than 1 percent in August from July, and in 2019 the monthly rate has only exceeded 2 percent once, versus six times in 2018.

Opportunities

- American Electric Power Co. is seeking approval to buy three wind farms in Oklahoma from Invenergy LLC for around $2 billion. Once completed, the wind farms will have 1,485 megawatts of capacity, reports Bloomberg. This deal is another sign that utilities are increasingly buying projects rather than entering long-term contracts for electricity. On Thursday, New York State signed the biggest ever deals for offshore wind power in U.S. history, awarding contracts to Equinor and Eversource Energy for two projects that will total 1,700 megawatts in capacity.

- Zambia’s new finance minister wants to restart talks with the International Monetary Fund about a bailout loan, reports Bloomberg. Bwalya Ng’andu said the government might also delay the start of a controversial sales tax. The Zambian economy is growing at the slowest pace in more than 20 years due to weaker copper prices – the country’s main export – and numerous disputes with miners. Investors responded positively to the news with Zambia’s Eurobonds rising 5.2 percent – the most in more than three years.

- America’s largest steelmaker, Nucor Corp., sees a bottom in steel prices due to strong demand after hot-rolled coil steel has fallen around 25 percent this year. CEO John Ferriola said in the company’s second-quarter earnings statement that “real demand for our products remains strong in key end-use markets” and that the company is “cautiously optimistic that pricing has bottomed for most products.”

Threats

- According to the National Weather Service, a “dangerous and widespread” heat wave is expected for two-thirds of the U.S. this weekend. Bloomberg reports that the heat will stress Midwest crops and boost energy demand for air conditioning. A July 16 report from the Union of Concerned Scientists says that with little or no action to cut climate change, the country’s hottest weather could see up to a fourfold increase by mid-century.

- More trade tensions continue, but this time between the U.S. and Europe. Bloomberg reports that Europe is expecting the World Trade Organization to allow the U.S. to place tariffs on EU products valued between $5 billion and $7 billion, as part of a 14-year dispute over illegal aircraft subsidies to Airbus. According to two European government officials, the tariffs could also be aimed at goods such as cheese, olives, pasta and whiskey.

- New York lawmakers are calling for a probe into Consolidated Edison Inc. after a power outage left part of Manhattan without power for most of Saturday evening, reports Bloomberg. Investors largely shrugged off the blackout with shares of the utility only falling as much as 1.1 percent on Monday.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 4.89 percent. Trump said he is not looking at economic sanctions against Turkey “right now” over its decision to begin receiving parts of a Russian missile-defense system may have supported Turkey’s stocks this week. However, the Trump administration has suspended the country’s participation in the F-35 program.

- The Turkish lira was the best performing currency this week, gaining 1.16 percent against the U.S. dollar.

- Industrials was the best performing sector among eastern European markets this week.

Weaknesses

- Russia was the worst performing country this week, losing 2.77 percent.

- The Romanian leu was the worst performing currency in the region this week, losing 35 basis points against the U.S. dollar.

- Energy was the worst performing sector among eastern European markets this week.

Opportunities

- U.K. wages grew at the fastest pace in 11 years in the three months through May, with average earnings excluding bonuses rising 3.6 percent. The figure was up from 3.4 percent in the previous period. The number of people in work rose 28,000 to a record high, leaving the jobless rate at a 44-year low of 3.8 percent.

- A spike in wages and government subsidies for cleaner- running cars has helped Lithuania and Romania buck the trend of falling car sales in the EU in the first half of the year. While the double-digit growth in Lithuania go a boost from resales to other countries, in Romania the government is doling out grants of as much as 10,000 euros for new cars to retire one of the oldest fleets in Europe.

- Cornerstone analysts expect the European Central Bank (ECB) to cut the deposit rate further into negative territory, accompanied by a tiering system, which should reduce the impact of negative rates on bank profitability. Bank stocks have underperformed the broad market for years. Since ECB President Mario Draghi’s speech in Sintra last month, bank stocks have outperformed the market. Draghi said depending on the specifics of a likely tiering system, outperformance could continue.

Threats

- The population of central, eastern and southeastern Europe, excluding Turkey, will decline by 12 percent by 2050 due to aging and migration, according to Tao Zhang, deputy managing director of the International Monetary Fund (IMF). Labor forces may also be reduced by 25 percent at the end of the same period, says Zhang citing new IMF research. This means that the working population will have to support more than twice the number of elderly people than it currently does. These demographic challenges could significantly slow economic growth. A shrinking labor supply and lower productivity of older workers, together with greater pressure on public finances, could cost countries about 1 percent of GDP per year according to the IMF.

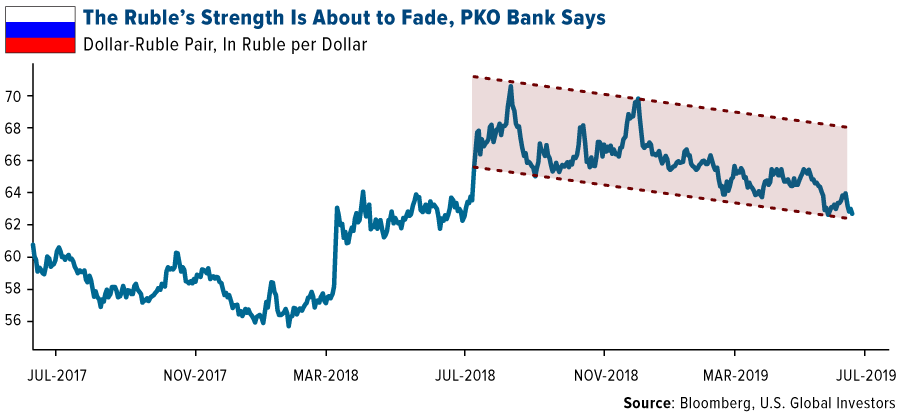

- The analyst who most accurately predicted the Russian ruble’s rally in the second quarter is now its most pessimistic forecaster. The Bank of Russia’s switch to monetary easing is the reason Jaroslaw Kosaty, a currency strategist at Poland’s PKO bank, sees the currency sinking about 9 percent against the U.S. dollar by the end of the year. Foreign investors who piled into local OFZ bonds in anticipation of the cuts are largely done staking out their positions, and the Bank of Russia says it expects the non-resident flows to fade, exposing the currency to further interest rate reductions.

- Germany’s ZEW survey recorded further declines in sentiment on both the current assessment and expectations balance. The July survey showed expectations fell to -24.5 from -21.1 in June. A gauge for the current situation dropped below zero for the first time since 2010. Elevated risks from U.S. protectionism, souring sentiment and a turn in the global investment cycle are likely to keep a lid on growth in the second half of this year.

China Region

Strengths

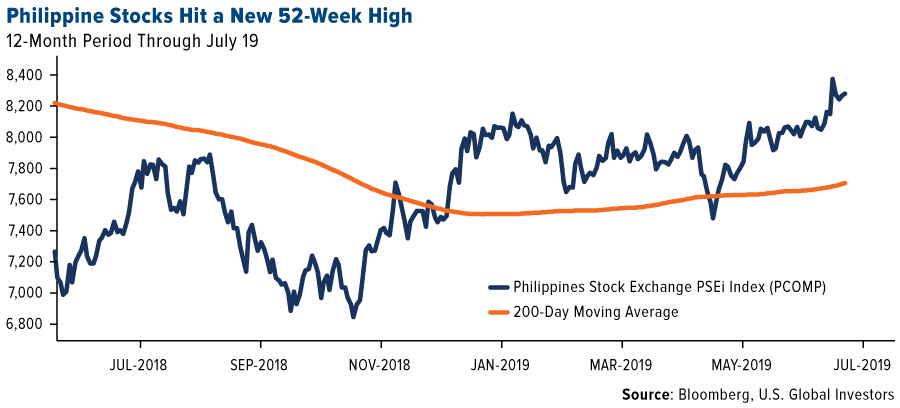

- The best performing index in the region for the week was the Philippines’ PCOMP Index, which rose 1.58 percent, while the Jakarta Composite climbed 1.31 percent. Hong Kong’s Hang Seng Composite rose 1.06 percent on the week.

- The best-performing sector in Hong Kong’s Hang Seng Composite Index since last Friday was consumer goods, which climbed 2.75 percent.

- The Philippines’ PCOMP Index jumped to 52-week highs this week.

Weaknesses

- The worst-performing indices in the region for the week were India’s NIFTY and SENSEX Indices, which declined by 1.04 and 0.91 percent respectively. The Shanghai Composite closed the week down very slightly, while Malaysia’s FTSE Bursa Malaysia KLCI closed down 67 basis points.

- The worst-performing sector in Hong Kong’s Hang Seng Composite Index this week was once again energy, which declined 0.77 percent.

- China’s second quarter GDP clocked in at a 6.2 percent, in line with consensus but nonetheless falling to the country’s slowest pace of growth since data were recorded in 1992; the reading was also down from the prior reading of 6.4 percent. A 6.2 percent pace remains within the expected governmental range of 6.0-6.5 percent for 2019.

Opportunities

- U.S.-China trade talks continue, with tariff escalation on hold but also without any clear progress. The framework for the current round of talks remains somewhat vague—will the framework be whatever was ninety percent done before the current round of talks? Or something new entirely? And so on. There is conspicuous absence of optimistic press releases, which, while not bad, may well mean some of the tough issues yet remain before us before some deal can be reached. But still, given the overhang on global markets that a trade spat between the world’s two largest economies can have, it is a definite positive that talks remain ongoing and there is a chance of some breakthrough or success; in the meantime, of course, tariff escalation is staved off, which is also a positive.

- Indonesia and Korea joined the global easing party this week, and with slow inflation in Indonesia in particular, that central bank has indicated they have more room to work as needed.

- A star is born? The Shanghai Stock Exchange’s new science and technology innovation venue—the STAR Market—begins trading on Monday with 25 debut IPOs expected to begin trading at an average price-to-earnings ratio of around 50. The new listing venue is designed to aid earlier-stage and/or even money-losing companies to go public in China rather than losing out on those listings to venue in New York, Hong Kong or elsewhere, and allows for greater freedom in terms of regulations around going public than does China’s traditional A-share market. The first five trading days will reportedly have no price limits for the newly-listed stocks, so there may be some Wild West-like swings over the first week, but the longer-term goal remains a set of domestic Chinese markets that can better imitate global developed markets and provide more opportunities for Chinese companies raise funds at home even while integrating global standards (and thus internationalizing China’s economy).

Threats

- The threat of U.S.-China trade war escalation must remain a threat until resolved with more certainty. And in the meantime, however positive it is that talks remain ongoing, the inherent uncertainty may be considered an inherent threat.

- Bloomberg reported that Beijing will withhold the final $4.9 billion needed to complete the Kenyan leg of a Chinese-built Belt and Road Initiative railway across East Africa. The high-profile nature of the Mombasa-Nairobi Standard Gauge Railway project—a showcase of President Xi Jinping’s ambitious BRI—has received some pushback and, since the profits from the railway, which would presumably be used to repay the debt, looks unlikely to come soon and with growing accusations that China is allegedly drowning its Belt and Road partners with debt obligations, the whole eastern portion of the project ground to a halt. China is already Kenya’s largest external creditor, at 22 percent. It is not the first BRI project to be shelved or walked back in scale.

- Monetary policy missteps remain a possibility, with market sentiment possibly swinging around easing expectations that can always run the risk of disappointing.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended July 19 was Tarush, up 609.59 percent.

- The company that launched the first U.S. bitcoin ATM, known as LibertyX, is expanding into 90 retail locations in Arizona and Nevada, reports CoinDesk. In a statement released on Wednesday, the company explained that it will now operate over 1,000 so-called bitcoin ATMs across the country, with the latest additions set up in ARCO and Chevron gas stations and even select Family Dollar locations.

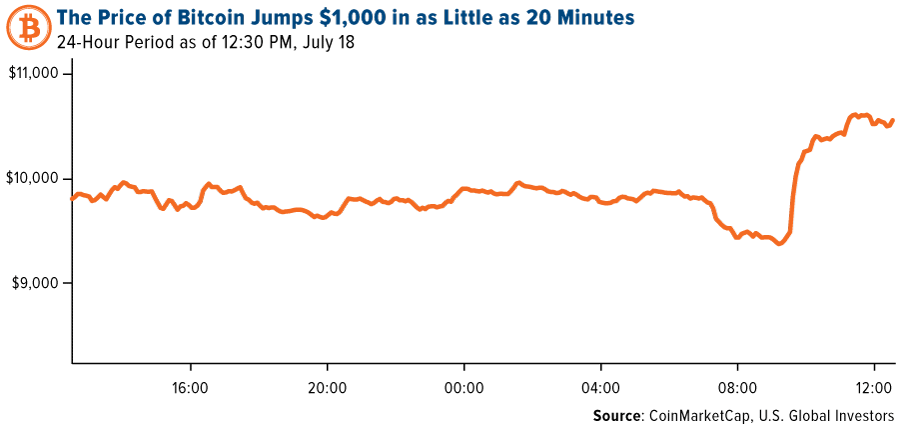

- On Thursday, bitcoin surged by $1,000 in as little as 20 minutes during U.S. trading, reports CoinDesk. The move pushed the leading digital currency from $9,335 to a high of $10,400.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended July 19 was Big Bang Game Coin, down 82.62 percent.

- Bitcoin lost nearly a third of its value this week after trading above $13,000, with much of the blame falling on Congress’ scrutiny over Facebook’s proposed Libra coin, according to the Wall Street Journal. The world’s largest crypto fell as much as 13 percent on Tuesday, its worst one-day drop of 2019. Enthusiasm about Libra drove much of bitcoin’s earlier rally, the hope being that it would usher in widespread adoption of cryptocurrencies. Since Facebook made the announcement, however, the criticism has been pointed and varied, coming from high-ranking members of Congress, the Federal Reserve chairman, the Treasury secretary and even the president himself. In a press conference on Monday, Treasury secretary Steven Mnuchin went so far as to call cryptocurrencies a “national security issue.”

- Cryptocurrency exchange BitMEX is reportedly being probed by the U.S. Commodity Futures Trading Commission (CFTC), reports CoinDesk. Bloomberg cited sources in a report saying that the regulator is investigating whether the exchange has allowed U.S. traders to use its platform. “The CFTC considers cryptocurrencies like bitcoin commodities and has jurisdiction over derivatives such as futures based on cryptos,” Coindesk writes. “As such, BitMEX would need to be registered with the agency to allow Americans to trade such products in the U.S.”

Opportunities

- In a new paper titled “The Rise of Digital Money,” the International Monetary Fund (IMF) suggests that cash and bank deposits could be left behind as digital money and fiat-pegged cryptocurrencies see greater adoption, reports CoinDesk. In the introduction, the author’s write that “digital forms of money are increasingly in the wallets of consumers as well as in the minds of policymakers.”

- Think the price of bitcoin will surpass $100,000 by the end of 2020? There’s now a call option for that. After winning approval in June from the Commodity Futures Trading Commission (CFTC), derivatives exchange LedgerX officially unveiled an option that pays off if the crypto hits a whopping $100,000 by December 2020—a tenfold increase from this Tuesday’s price, according to Bloomberg.

- As announced on Friday, the Jersey arm of Binance has listed the cryptocurrency exchange’s own British pound-backed stablecoin, reports CoinDesk. The Binance GBP (BGBP) is being offered on the fiat-to-crypto platform due to trader demand for more stablecoin options.

Threats

- An analysis by Coinfirm can now show the movement of the bitcoin stolen from Binance into various wallets, reports Coindesk. The hack happened on May 7, 2019 and netted 7,000 BTC, the article explains, and the hackers have been moving stolen bitcoin from wallet to wallet. Most recently, it’s been discovered that the hacker has begun liquidating the BTC on various exchanges.

- Last weekend’s “fat finger” error involving the Tether stablecoin exposes a huge vulnerability in the still-early market infrastructure for trading cryptocurrencies, the Wall Street Journal reports. On Saturday, the company behind Tether accidentally created some $5 billion of the digital coin in an instant, more than doubling the amount in circulation, according to the WSJ. “The sudden flood spooked the market and drove down the price of bitcoin, the most actively traded cryptocurrency, by about 12 percent,” the article reads. “The error shows how easy it is to muck up the cryptocurrency market, a decade after bitcoin’s birth.”

- A review by Reuters of 33 blockchain projects at large companies—including major banks, exchanges and tech firms—shows that the technology “has yet to deliver on its promise.” Despite some projects having been announced four years ago, at least a dozen of them have not even gone beyond the testing phase, and those that have “are yet to see extensive usage.” Many executives interviewed by Reuters suggest that “regulatory hurdles” have impeded adoption. “The euphoria that surrounded the early days of Wall Street’s interest in blockchain is giving way to pragmatism, as companies realize that it will likely take years before it takes off in a substantial way,” Reuters reports.

© US Global Investments

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All