Weighing the Week Ahead: How Much Has Economic Weakness Hurt Corporate Earnings?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar is normal and includes several important reports. I am especially interested in the housing data and retail sales. More important than the economic data is the start of earnings season. With everyone convinced about economic deterioration, expect the pundits to be asking:

How much has the weak global economy affected corporate earnings?

Last Week Recap

In last week’s installment of WTWA, I asked who was really running the Fed. That was a good forecast for the week’s theme. CNBC led with similar stories at the start of the week, and the discussion continued through Thursday’s Powell testimony. Bloomberg and online financial publications also featured the issue of Fed independence. This was also a question during the hearings, as Powell was asked what he would do if the President tried to fire him. (Fill out his term as Chair, he said).

Paul Schatz, finding nothing in the Fed mandate to support a rate cut, makes the score Trump 1 – Powell 0.

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski’s version, which combines a lot of information in one picture. The full article also includes several other interesting takes on price movement.

The market posted a quiet, 0.8% gain for the week, with a trading range was only 1.7%. It felt bigger to most market participants because of the early weakness on the return from the long weekend and the spike when Fed Chair Powell’s written testimony was released. My weekly Quant Corner translates this into a volatility calculation which you can compare both to VIX and to past readings.

Noteworthy

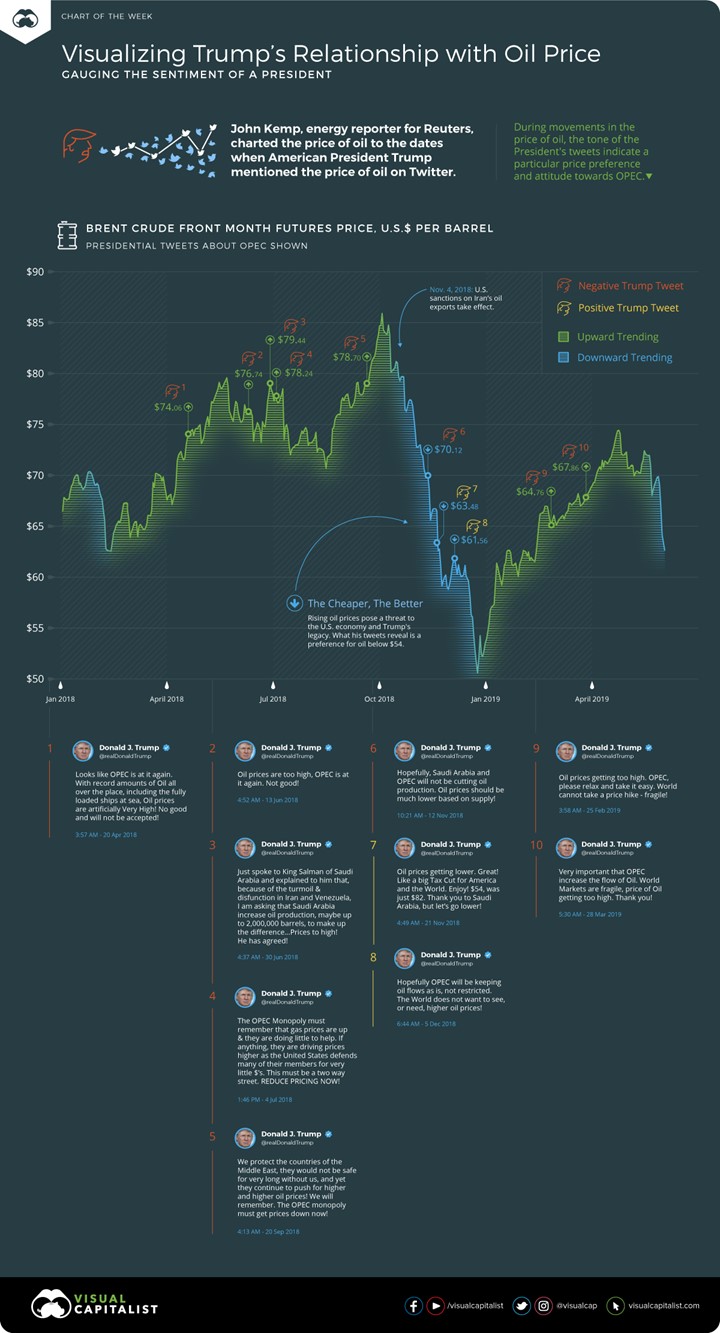

The Visual Capitalist enlightens us about the Tweeter-in-Chief and his implied views on oil prices.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators are an important part of our regular research. There are three different groups. Long-term indicators and the nowcast remain positive, helped by a dovish Fed. The short-term message has improved to neutral. NDD remains concerned about trade wars.

The Good

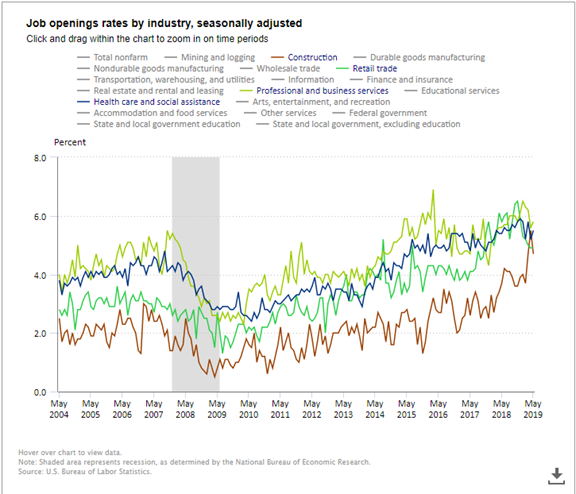

- The JOLTS report showed continuing labor market strength. Most observers characterized the data as a miss of expectations because they look only at the absolute number of job openings. Growth in jobs is much better measured by the data in the monthly employment situation report. JOLTS is about labor market structure, which continues to look very good. I explained what we really should be watching in this brief post. You can review much more at the BLS site, including some great interactive charts. Here is one example.

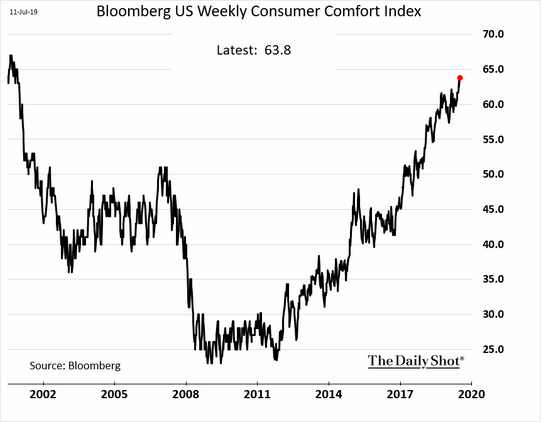

- Bloomberg’s consumer comfort index continues to rise, approaching levels last seen in 2000.

- Hotel occupancy is tracking near last year’s record highs. (Calculated Risk).

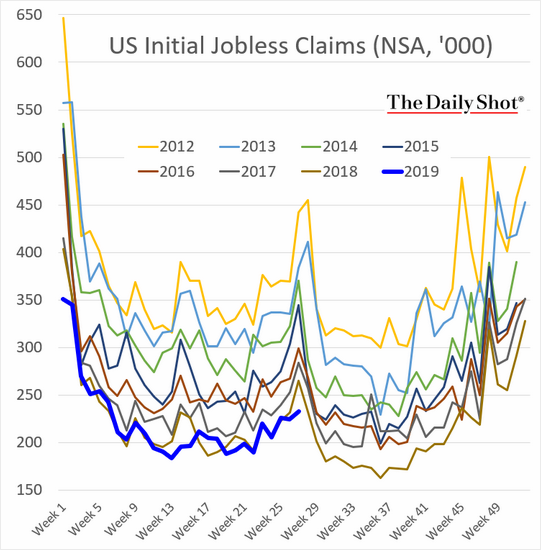

- Initial jobless claims declined to 209K, better than both the prior week and also expectations of 222K. The Daily Shot has an interesting comparison of 2019 to prior years.

-

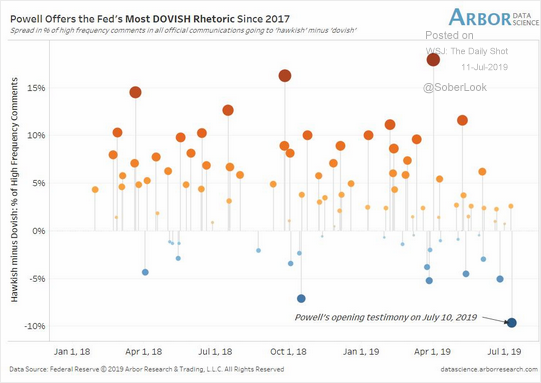

Chairman Powell

What pushed them over the edge to a rate cut was the potential disruption triggered by President Trump’s repeated use of tariffs as a negotiating club. The uncertainty caused by the actions was sapping business confidence and threatening to force force to endure the costly process of reworking current global supply chains. The Fed felt they had little choice but the respond with lower rates just as they would with any adverse economic shock.

In other words, Trump got the Fed to cut rates, but had to damage the economy to do it.

Here is a graphic comparison with past communications from The Daily Shot.

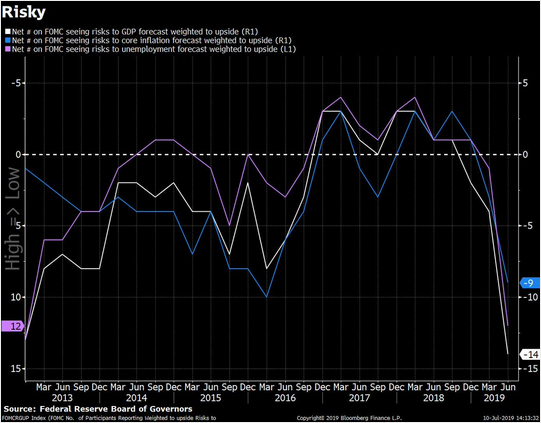

The minutes from the June meeting confirmed the more cautious read on the economy. These are the net positions of Fed participants on the economy, core inflation, and unemployment. All have dropped significantly in the last few months.

The Bad

-

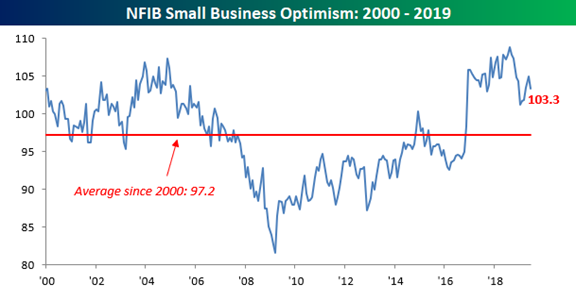

Small business optimism down ticked, but still beat expectations. Bespoke analyzes the data, noting that this is still the fourth highest reading on record. That said, there are concerns about rising uncertainty.

-

Mortgage applications declined -2.4% versus the prior week’s -0.1%. (Calculated Risk).

-

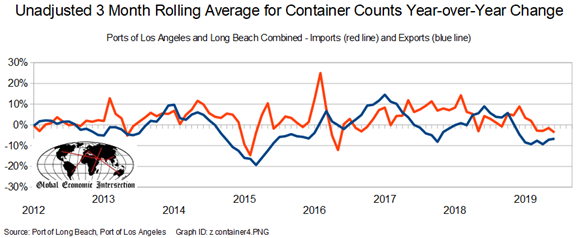

Sea container counts showed a one-month gain, but Steven Hansen (GEI) shows results after smoothing out the noise.

-

Core CPI increased 0.3% above expectations of 0.2%. Headline CPI was up 0.1% above an expected 0.0%.

-

PPI increases mirrored the CPI, 0.3% core and 0.1% headline, both a touch higher than expectations.

-

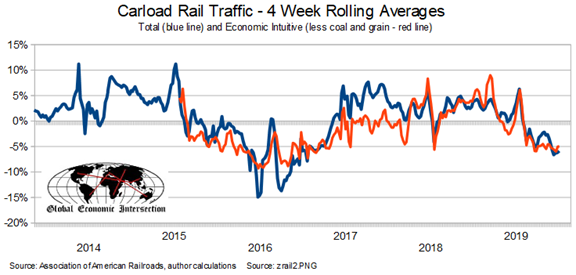

Rail traffic remains in deep contraction using Steven Hansen’s (GEI) four week rolling averages. This is true both for total carloads and his “economically intuitive sectors.”

The Ugly

Chicago area property taxes – how assessments are done, how they are appealed, and the conflicting roles of public officials.

Assessments are too high and have excessive variation. Taxpayers with the means hire attorneys to appeal the assessment. Some Chicago Alderman are attorneys whose firms specialize in these cases. Why is something that has gone on for decades now in the news?

- Cubs co-owner Todd Rickets has been paying taxes on a 100-year old house despite replacing it nearly ten years ago with a “5,000-square-foot North Shore house nestled on a meticulously landscaped lot complete with a Japanese-style garden”. (Chicago Tribune)

- New Illinois Governor JB Pritzker removed toilets in a North Shore mansion to get it classified as “uninhabitable.” He has repaid the $330,000 he saved and asserts that he followed all of the rules. (Chicago Tribune)

- Property tax bills in some areas are increasing dramatically. It was an 87% increase in two years for one resident (NBC 5).

There is a larger and more general public policy story in all of this.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

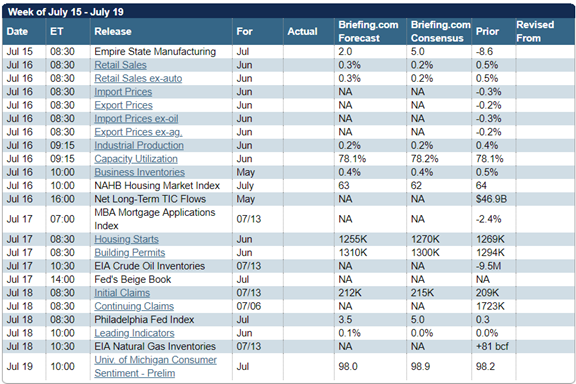

The Calendar

The economic calendar is normal including important reports on housing, retail sales, industrial production, and Michigan sentiment. Some are believers in the leading indicators and the Philly Fed and Empire state reports earn attention as the first data for the new month. I’m still looking for a turn in the housing starts data, but we might not be there quite yet.

China’s GDP will also be closely followed, especially if it falls to a 5-handle.

More important than the regular reports will be the start of earnings season. Citibank tees off Monday, before the opening, and the rest of the big banks follow.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

Opinions about the economy draw a lot debate, but the translation to market impact is loose. The transmission goes through corporate earnings, which command attention four times a year. With a current consensus about a weakening global economy, expect the punditry to be asking:

How much has the weak global economy affected corporate earnings?

Background

Four times a year earnings season provides a chance to verify (or not) economic data with the impact on actual corporate results. Many think this is too often, pushing executives to think in the short-term. The usefulness of the reports varies widely. The conference calls add color, but often seem dramatically different from the actual data. Some companies no longer provide guidance about future earnings. Those that do have widely varying track records.

In short, the earnings story is as challenging to interpret as is economic data.

There is a repeating pattern of original analyst estimates (sometimes two or more years before the quarter) being too high. The estimates fall continually until the actual quarter. With this lowered bar, the “beat rate” for earnings results is usually more than 60%.

Q2 Expectations

We will pay special attention to the leading sources for earnings coverage for the next few weeks. We urge you to do the same.

- John Butters of Fact Set provides a comprehensive analysis of the macro and sector picture, the beat rates, and key trends.

- Investment manager Brian Gilmartin has closely followed earnings versus expectations for decades. He looks at key sectors, as well as analyzing individual companies. Since he lives in Chicago, we were able to get together regularly for market discussions. I was impressed with his work. It was a great opportunity for me to make a friend via my professional network.

- Seeking Alpha provides an excellent resource with transcripts of earnings calls. Years ago we all spent hours monitoring these calls, and sometimes they are still worth hearings. A printed, searchable transcript may not help a trader who needs to make a fast decision, but it is an excellent resource for investors.

Market expectations range widely, from those who see a major decline and the start of an earnings recession, to those who see only transitory weakness. No one is looking for major gains, so the expectations bar is set low.

Brian provides a preview of week one, focusing on the financials and comparisons with other sectors. He always provides data you will not find in other sources and adds his own spreadsheets and analysis. Here is another example which draws upon the excellent JP Morgan Guide to the Market.

John’s work includes some shorter posts on specific topics and the weekly “Earnings Insight” publication for us wonks. Key takeaways for this week include the following:

- Despite the expected decline of -3.0% in this quarter, he sees a good chance of a modest increase. This would be consistent with the pre-announcement “underbid” of prior quarters. Most would find this result surprising.

- Key items to watch for in conference calls include trade (especially China) and currency effects.

These are valuable guides for us as we watch the results pour in.

I’ll cover my own ideas about the implications in today’s Final Thought.

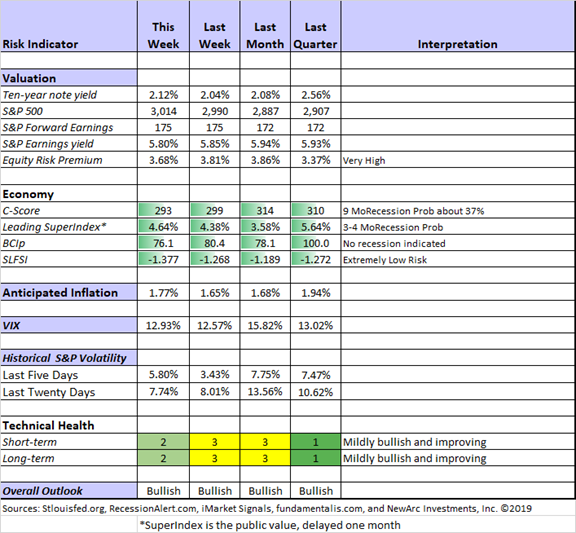

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

Our technical market indicators, both long and short term, have improved.

The C-Score yield curve effect is slightly delayed due to official reporting of government data. It will rebound a bit next week reflecting Friday’s trading. Recession risk is still in the “watchful” area.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

Georg Vrba: Business cycle indicator and market timing tools. The most recent update of Georg’s business cycle index does not signal recession.

RecessionAlert: Strong quantitative indicators for both economic and market analysis

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis.

Guest Sources

When does 30% = 100%? That was a popular theme this week, on the trading floor and on Bloomberg TV. I thought it was tweet worthy. I also liked this irrefutable forecast: Germany Sees 50% Chance for EU-U.S. Trade Deal, Possibly in 2019.

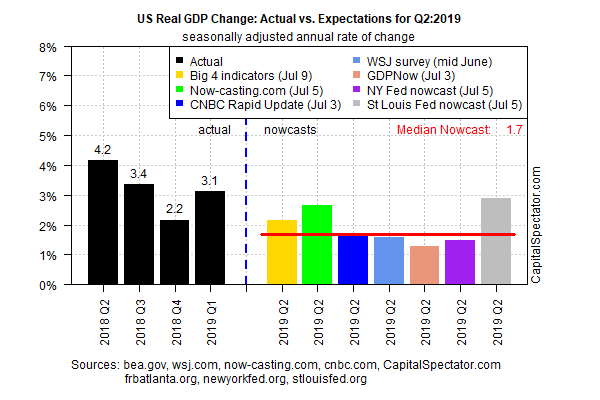

James Picerno monitors current GDP forecasts and adds valuable interpretations. The 1.7% median nowcast is a significant decline from Q1’s 3.1%, which he sees as a “warning flag for this year’s second half and beyond.”

Insight for Traders

Our weekly “Stock Exchange” series focused on how traders should react when risks increase despite the market reaching all-time highs. We also reviewed recent picks from the trading models, showing the frequent contrast with a fundamental analysis. Pulling it all together was our series editor, Blue Harbinger.

Insight for Investors

Investors should understand and embrace volatility. They should join my delight in a well-documented list of worries. As the worries are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely.

Best of the Week

If I had to recommend a single, must-read article for this week, it would be Nick Maggiulli’s The Price of Admission. He starts with a clever thought experiment and then provides the data.

Imagine there exists a market “genie” who approaches you every December 31 with information about the U.S. stock market for the next year. Unfortunately, this genie cannot tell you which individual stocks to buy or how the market will perform, but the genie does know how much the stock market will be down at its worst point (“maximum intrayear drawdown”) in the next 12 months.

My question to you is: how much would the market have to decline at its worst point in the next year for you to forgo investing in stocks (S&P 500) to invest in bonds (5-Year U.S. Treasuries)?

You may well be surprised by the result. One of the charts provides some excellent interactive choices – educational and fun to try.

The more important insight from the plot above is that the S&P 500 has had a positive return in every year since 1950 with an intrayear drawdown of 10% or less.

This, my friends, is the price of admission. Because markets won’t give you a ride without some bumps along the way. You have to experience some downside to earn your upside. And, as the plots above illustrate, avoiding these bumps can be beneficial, though knowing when they will occur is near impossible. Unfortunately, there is no magic genie.

[Jeff – I’m not convinced that this is the best criterion for allocation, but it is a great way to think about the problem].

Stock Ideas

How about Russian Stocks? Lyn Alden Schwartzer observes that they are “quietly outperforming.”

Andrew Hecht highlights Petroleo Brasileiro SA- Petrobras (PBR), which he expects to outperform price increases in oil. Investors who are bullish on oil will find this to be an attractive idea.

Or else oil services? D.M. Martins makes the case for Halliburton (HAL).

Interested in Charles Schwab (SCHW)? Brian Gilmartin provides his usual balanced assessment of the company’s prospects.

Colorado Wealth Management updates their analysis of Annaly Capital Preferred (NLY-I) shares. The idea is working well so far.

Are the Dogs of the Dow a good way to find high yield with appreciation potential? Double Dividend Stocks takes a look.

Morningstar takes a different approach to the search for dividends. Here are eleven stocks that have a good economic moat, low risk of bankruptcy, and an attractive yield.

Personal Finance

Abnormal Returns features a special week of content in July. Tadas takes a well-deserved vacation but provides interesting and fresh commentary. He invites a group of leading bloggers to provide candid answers to some interesting questions. (I am both pleased and honored to be part of the group). Check out the topics, including The Death of Value, the trend toward non-transparent ETFs in active management, the prospects for the “long-term stock exchange,” surprises from the last year, the rise of podcasting, and endorsements of favorite new things.

This provocative approach always generates ideas that you do not typically see. It is well worth reading.

Watch out for…

Bitcoin regulation. Fed Chair Powell made some observations about the role of cryptocurrencies. President Trump also cited Facebook’s Libra as suggesting the need for regulation.

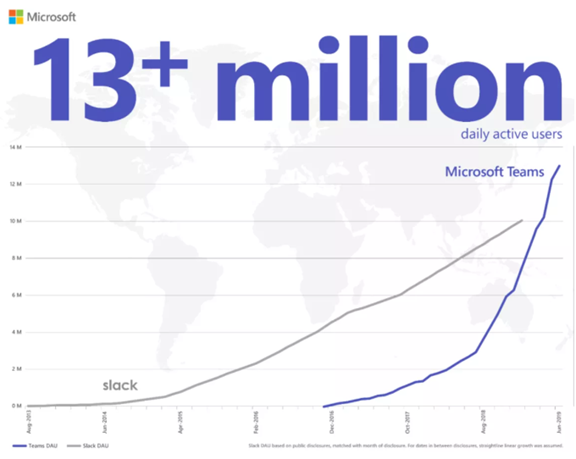

Microsoft Teams overtakes Slack with 13 million daily users.

Final Thought

The “hot money” in daily trading usually exaggerates any snippet of news. This often means expecting any current trend, no matter the length or strength, to persist until an extreme is reached. Witness this week’s repetition of the NY Fed 30% recession probability reading, quickly turned into a near certainty.

The recent trend has included some weaker economic data, but nothing that threatens what I have suggested is a current baseline – 2 to 2.5% real growth.

Fundamental Market Support

I monitor three elements in evaluating market fundamentals.

- Attractive and growing expected earnings, especially when compared to alternatives like bonds.

- Low inflation expectations and reasonable interest rates.

- Little concern about recession or high levels of financial stress.

When one or more of these elements is missing, it is time to reduce the allocation to equities.

This is definitely not a ‘bad news is good news’ viewpoint. Robust economic growth is a key element of increasing earnings. Interest rates in the 4 – 5 % range on the ten-year note are historically consistent with a healthy stock market.

Abundant Opportunities

There are plenty of attractive inexpensive stocks, but they are not the ones that have commanded popularity in the last few years. Finding companies with attractive value and earnings growth may not make you an instant winner, but it has the best long-term investing record.

Earnings Season

There has been such a negative consensus that I am optimistic about this earnings season. For Q1 it seemed obvious from the outset that the market was insisting on the most negative interpretation of any announcement. Our team was especially cautious in implementing indicated trades right before an earnings report. For me, this week has a special significance.

The most prevalent market myth? The expectation that “late cycle” means “end of cycle.” Those who missed the bulk of the market rally have over-emphasized recession odds. Any snippet of information that supports that thesis confirms their biases. How can you avoid this?

Investors should be open to all information, especially that which challenges their current viewpoint. What we all need is a “reset” button to permit a fresh start.

[Is your portfolio making a new all-time high? This might be a signal for a checkup! Write for my free paper, Market Highs. You might also enjoy Understanding Risk. Just send an email request to main at newarc dot com].

Some longer-term items on my radar

I’m more worried about:

- Potential conflict with Iran. The increase in enriched uranium violates the prior agreement but does not represent an immediate threat. The Council on Foreign Relations has several good background pieces, including one emphasizing geopolitics and one on Iran’s nuclear program.

- The debt ceiling increase is now needed by September according to Treasury Secretary Mnuchin. This would occur before Congress returns from its summer recess. Meanwhile, legislative cooperation is in short supply.

I’m less worried about

- The length of the economic and market expansion – long and slow. The Economist reviews the arguments.

- The yield curve, which steepened this week. I’m watching, but no other confirming recession signals so far.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits