Upstream

At one end of the Energy sector’s “value chain” are the “upstream” companies. The upstream segment includes exploration & production (E&P) and oil-field equipment & services companies that are engaged in the search for, and production of, crude oil and natural gas. These sub-industries account for roughly 35% of the sector by market cap, and their profits tend to be highly correlated with commodity prices.

Midstream

Midstream companies store and transport oil, natural gas, and natural gas liquids. The midstream segment includes pipelines and liquefied natural gas (LNG) exporters, as well as other companies engaged in the transportation and storage of crude oil, natural gas, and natural gas liquids. Many midstream companies have the ability to pass through changes in commodity prices to their customers and, as a result, their profitability is relatively insulated from fluctuations in the price of oil or natural gas. Midstream companies account for about 7% of the sector by market cap.

Downstream

Downstream companies refine crude oil and market the finished products, such as gasoline and jet fuel, to customers in the U.S. and abroad. Profits from downstream business also tend to be relatively well-insulated from commodity price fluctuations. Downstream companies account for about 10% of the sector by market cap.

End Users

At the other end of the energy value chain are the “end users.” These are companies that use energy products intensively in their operations, either as a fuel or a feedstock. The price of energy can have an important effect on the competitiveness of these companies.

Integrated Oil & Gas

The largest segment of the Energy sector is the Integrated Oil & Gas sub-industry, which accounts for 44% of the sector by market cap. Exxon Mobil, Chevron, and Occidental Petroleum comprise this sub-industry, with operations in all parts of the energy value chain.

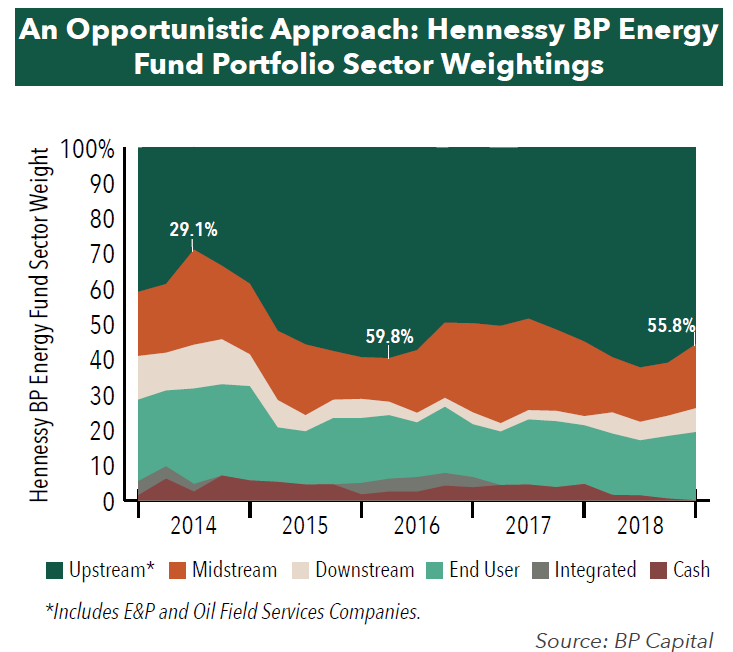

Opportunity Up and Down the Value Chain

The portfolio managers of the Hennessy BP Energy Fund have the flexibility to opportunistically move up and down this energy value chain, and, depending on the outlook for each segment, overweight the areas they believe will generate the best returns.

Over time, the percentage of the Fund invested in different segments of the value chain has fluctuated significantly. For example, in mid-2014, only 29.1% of the Fund was invested in upstream companies, whose profits are highly correlated with the price of oil. As a result, the Fund was relatively well insulated from the effects of a decline of over 60% in the price of oil over the subsequent nine months. In contrast, in March 2016, the Fund had an almost 60% weighting in upstream companies and benefited from the almost 40% increase in the price of oil over the subsequent nine months.