We’ve written many times about the difficulty—or as some would say, the futility—of using macro events to predict economic conditions and financial-market performance. That’s why instead we’ve always focused on the prospects for individual companies.

Among macro forecasts, consider the many warnings that artificially low interest rates and massive government-bond purchases (a.k.a., quantitative easing) in the aftermath of the global financial crisis (GFC) would produce runaway inflation. To the contrary, about 10 years later, we now have persistently low inflation—and even deflation in some areas of the global economy.

Moreover, despite predictions for rapidly rising interest rates, the 10-year U.S. Treasury bond yield recently fell to about 2%. Even more surprising, 10-year government-bond rates in Austria, Denmark, Germany, Japan, the Netherlands and Switzerland are actually negative. Just imagine tying up your money for 10 years and actually getting back less than you had originally invested.

Recently, perhaps the only macro force that’s been a reliable harbinger of near-term market performance has been U.S. Federal Reserve (Fed) policy. Stocks seem to be rising and falling based on actual and anticipated adjustments to the federal-funds rate. The Fed’s latest pronouncements have been about an upcoming rate cut and a revised view on neutral monetary conditions. While these pronouncements have been perceived as positive for stocks, paradoxically the Fed’s change of heart has been in response to signs of economic weakness.

The often-irrational reliance on the Fed has been in the short run, and we don’t necessarily expect such behavior by market participants to continue indefinitely. What we do expect is that our approach of concentrating on company fundamentals will continue to add value over the long run. And one element of this approach is our emphasis on innovation—whether in companies creating breakthrough technologies or in companies simply using these technologies to benefit their businesses.

DIGITALIZATION IS THE FOUNDATION

Digitalization, at its most-basic level, is a superior way of doing business. Digitalization involves the electronic storage, retrieval and distribution of information, and the ability to communicate, collaborate and be productive with the help of electronic devices. We see the rapid digitalization in the global economy as the foundation of the innovation occurring at companies in every sector and in every industry.

One key development is the ability of even non-tech companies to establish more-personalized relationships with their customers through the use of mobile-phone apps. In the U.S., many of our portfolio holdings are technology companies that directly facilitate this secular trend or are companies that have embraced technology to gain a competitive advantage in the race to source, convert and retain customers. Companies are increasingly utilizing mobile apps as critical sales tools. Today’s consumers are convenience-driven. Companies, large and small, have been finding that mobile apps help them to better engage with their customers, who are then likely to become more loyal and boost spending.

To stay ahead of the competition, an increasing number of companies—whether business-to-business or business-to-consumer—are integrating customer-facing technology into their operations. For example, we’ve invested in a company that puts digitalization to work by delivering technology solutions, including mobile apps, to customers of U.S. financial institutions like banks and credit unions. More and more customers want an app that they can use on their phone to check balances, make deposits, transfer money, pay bills and even get a loan. The financial institutions benefit because the convenience of using an app drives customer loyalty, improves efficiency and helps them stand out in a crowded field.

As another example of how mobile apps are helping companies in all sectors and industries to gain a competitive advantage, consider one of our non-tech holdings that’s embraced the digitalization trend in the United States. This company is a leading distributor of chemicals, parts and supplies to pool-maintenance businesses. The mobile app allows maintenance businesses to search for and order materials and equipment for pool owners from the field. The app also enables them to provide instant customer quotes. A pool-maintenance competitor that doesn’t have such an app may need to research prices and check availability back at the office, activities that increase the workload and delay customer service.

In India, digitalization is also the foundation of a technology revolution—allowing the country to leapfrog outmoded stages of development in the ways people communicate, the ways they live and the ways they work. Just imagine going from having no indoor plumbing or electricity to having a mobile phone and a bank account almost overnight. Beyond telecom and financial services, the Indian coastal city of Kozhikode is using a cloud-based digital solution developed by the eGovernments Foundation to get building plans approved—including site inspections—in as little as 15 days, down from as much as one year.

Similarly, an Indian driver’s license can now be obtained through a mobile-phone app, which replaces filling out paperwork and waiting in long lines at the Regional Transport Office. Moreover, the license itself is stored along with other government records in a DigiLocker, which eliminates the need for tangible documents and lessens the burden of a person’s physical presence to accomplish many tasks. Consequently, India’s government bureaucracy—which used to be a major impediment—has now been streamlined into a competitive advantage compared to other countries, even developed countries like the United States.

Below we discuss more about innovation, highlighting additional developments in the U.S. and India.

MARKETS

As mentioned, the U.S. Fed has played a dominant and positive role in financial markets recently. On the world stage, the economic slowdown in China has probably had the largest negative effect.

We often get a sense of the relative uniformity in financial-market performance by looking at the indexes shown on Morningstar.com. Of the 145 stock, bond, target and commodity indexes, 131 were positive and 14 were negative for the second quarter of 2019. Not surprisingly, of the 14 indexes that were negative, most of them were related to weakness in China and broader Asia.

During the quarter, the U.S. large-cap S&P 500® Index advanced 4.30%. The technology-heavy Nasdaq Composite Index gained 3.87%. The Russell 2000® Index of small caps rose a more-modest 2.10%. And growth-oriented small caps performed a little better, with the Russell 2000 Growth Index up 2.75%. Value-oriented small caps in the Russell 2000 Value Index were up a lesser 1.38%, as value stocks—including those across larger market capitalizations—generally trailed their growth counterparts. Investors’ preference for growth stocks over value names was a continuation of the trend we’ve seen for a number of years.

Generally speaking, international stocks also performed reasonably well in the second quarter. The MSCI World ex USA Index rose 3.79%. But the MSCI Emerging Markets Index, to some extent held back by exposure to China, gained just 0.61%.

Intermediate- and long-term bond yields fell during the quarter, which may have had something to do with disinflationary forces and extremely low rates overseas. In addition, there was probably a flight to safety as angst intensified over trade disputes. Because bond prices move in the opposite direction of yields, bond indexes posted positive returns. The Bloomberg Barclays US Aggregate Bond Index increased 3.08%. And the Bloomberg Barclays US 20+ Year Treasury Bond Index was up a solid 6.11%.

We’ve recently noted a chorus of commentators calling for a significant market correction due to a host of macro factors. From our perspective, we remember the many erroneous macro predictions and the fallen media stars who dared to go too far out on a limb with their comments and with their investment strategies. Based on such hazards in trying to predict the future, we prefer to keep an open mind.

Although we’re willing to acknowledge our lack of insight regarding some conditions in the economy and in the financial markets, we do have the courage of our convictions in other areas. We just think there’s a big difference, on the one hand, in betting on the timing of an interest-rate hike or cut, deal or no deal on trade and, on the other hand, in investing in companies based on intensive research of strong management teams that are taking advantage of technological advances to create paradigm-shifting innovations.

ECONOMY

In this section, we discuss our economic views, which do help shape our investment decisions—just not in an all-or-nothing sort of way. Perhaps the best description of our approach with respect to economic conditions is that we’re “macro-aware” rather than “macro-driven.”

Regarding the state of the economy, one of the most-striking interviews we’ve seen recently was with Stanley Druckenmiller, a very successful American investor and philanthropist—who, like us, has no qualms about saying “I don’t know” when a question is beyond the scope of his knowledge. Druckenmiller remarked that he was surprised to see policy makers and the investment community focused so minutely on the levels of economic statistics, including interest rates, inflation and economic growth.

During more-rational times—according to Druckenmiller—the Fed, for example, would hit the brake when the economy was clearly overheating and would step on the gas based on a pronounced slowdown. Today, he says, there’s a silly attention to economic statistics down to decimal values.

What’s more is that most economic statistics aren’t even accurate to such levels. For instance, there’s an obsession with tweaking the federal-funds rate in fractions of a percentage point and with targeting a U.S. inflation rate of 2%. But inflation is hard to measure because our wellbeing changes over time with different needs and preferences for goods and services. Also not taken into account is that very low inflation, or even deflation, can be good if such a condition is spurred by technology and high productivity.

Similarly, the boom in innovation—including cloud-based computing, for example—means that gross domestic product (GDP) growth has become less relevant to our standard of living. Just consider three services provided by Google: internet search, maps and storage. These services are free or are very inexpensive. Now consider how much you would have been willing to pay for these services before they even existed.

But what you would have been willing to pay for Google’s services isn’t reflected in GDP because the actual cost to consumers is so low and the improvement in productivity is difficult to ascertain. So how do you measure the economic value of the following innovations? You’ll never again have to buy an updated encyclopedia. You’ve got a virtual personal assistant to guide you with customized directions to your destination. Your photos look better than ever before, and you can access them from almost anywhere.

Now let’s consider our on-the-ground economic assessments from our research of company-specific results and our discussions with management teams, customers and suppliers. Based on these factors, a U.S. recession doesn’t seem imminent to us. Moreover, we believe the prospects for continued innovations and productivity improvements are on the rise.

When we talk about a “recession,” for the reasons outlined above, we’re less concerned about the technical definition—which is two successive quarters of declining inflation-adjusted GDP. We’re far more concerned with, for example, a condition in which company management teams say they’re seeing slack demand and are pulling in their horns.

For the most part, we haven’t witnessed a lot of such reticence in the U.S. What we have witnessed are companies investing in technological innovations—such as the move to the cloud and strong social and mobile presence—which we think are required to engage and delight customers, who are demanding convenience, ease of use and an exceptional overall experience.

In Europe and parts of Asia, however, we have heard more concerns from management teams. Some of this trepidation has to do with the uncertainty surrounding Brexit (Britain’s looming exit from the European Union). Some has to do with global trade tensions, especially related to China. And there are lingering wounds from the GFC that, relative to those in the U.S., have been slower to heal—including a still-struggling banking system. Beyond these factors, many international companies have lagged their U.S. counterparts in developing and implementing more-advanced technologies such as business-to-consumer and business-to-business applications.

Fortunately, stock valuations are somewhat less expensive internationally than in the U.S. And we’re able to find businesses that are catching up on the innovation front. This should enable us to invest in companies expanding at a healthy clip even in a slow-growth economic environment.

INDIA TODAY: SIMILAR TO THE U.S. IN THE EIGHTIES

Returning to our point about the United States seeming to hold up better economically than most other countries, we believe that—in addition to a focus on innovation—the U.S. continues to benefit from deregulation and other reforms that began in the 1980s under President Ronald Reagan. Additionally, we think the proliferation of self-funded retirement plans around that time helped create more of an “investor culture,” which has been positive for economic development.

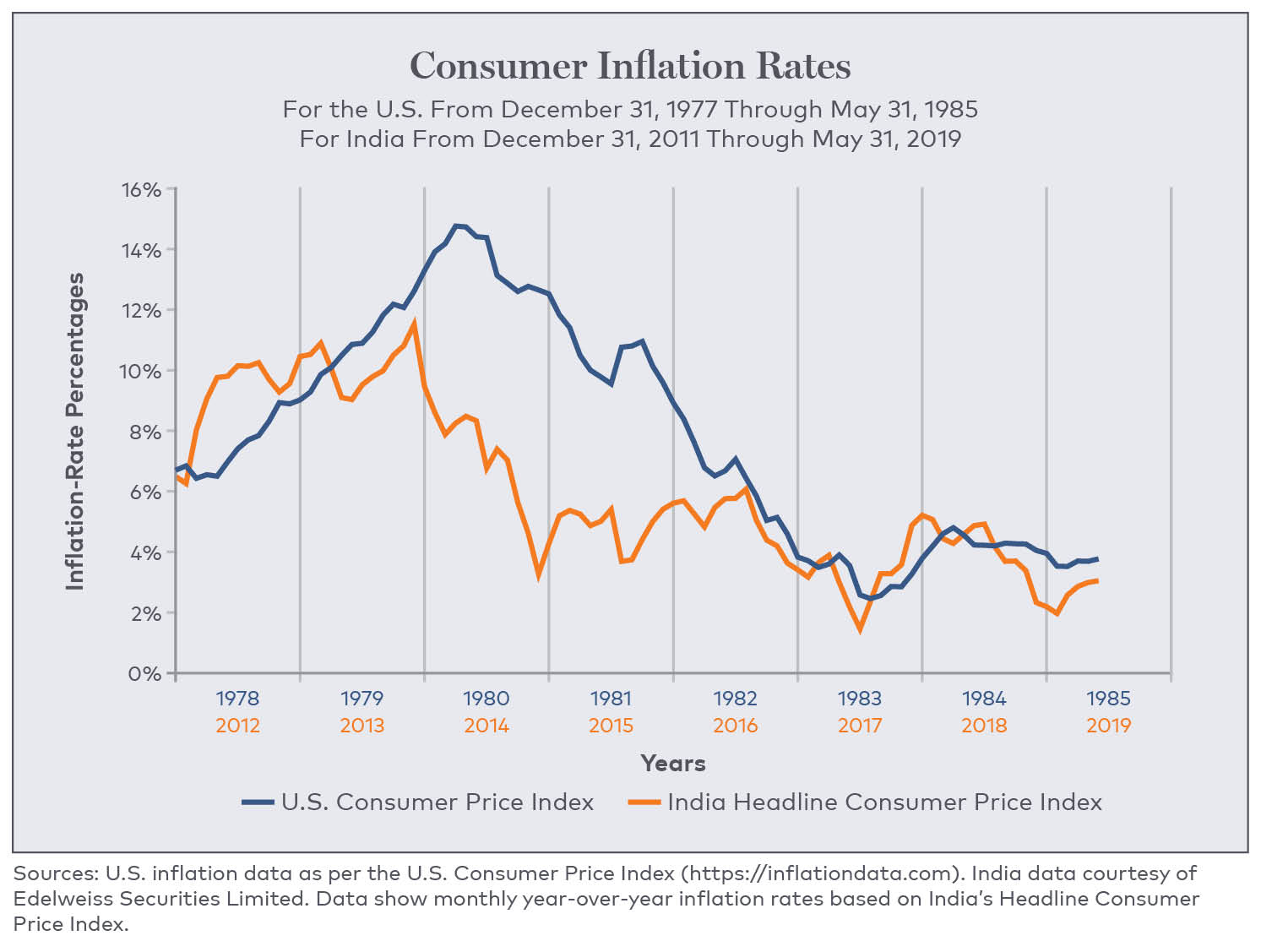

Beyond pro-growth measures during the Reagan administration, former U.S. Federal Reserve Chairman Paul Volcker led the fight to reduce inflation, which peaked at 14.8% in 1980. Volcker took the unpopular step of raising the federal-funds rate to 20% in 1981. But he was vindicated in the eyes of most economists when inflation fell to below 3% by 1983.

Like the U.S. in the 1980s, we think India is currently experiencing the long-term effects of reforms and initiatives that have been bolstered under Prime Minister Narendra Modi. India’s forward-thinking measures have helped make the country the fastest-growing major economy in the world and one of the most-fertile emerging markets for finding attractive investments.

Even India’s “investor culture” is similar to that of the United States. In the U.S., there are individual retirement accounts (IRAs), 401(k) plans and other savings vehicles. In India, there are systematic investment plans (SIPs). The goal in both countries is the same: getting people who are still relatively young to take charge of retirement planning and to benefit from the powerful force of long-term compounding, mainly through investments in assets such as stocks and bonds.

Another parallel between the U.S. and India has been a willingness to fight inflation. In 2014, under the Modi administration, former Reserve Bank of India (RBI) Governor Raghuram Rajan took a page out of Volcker’s playbook by raising the RBI’s benchmark policy rate to 8%. What followed, as indicated in the chart on page 4, was a general decline in India’s consumer price inflation—which now sits at 3%, down from over 11% around the time that Rajan became RBI Governor in 2013.

Moreover, the Reserve Bank of India Act was amended by the Finance Act of 2016, which allows the central bank to contain inflation within a specified target level. Therefore, inflation targeting has been enshrined in India’s constitution.

Also included in the chart is the pattern of U.S. consumer price inflation from the late 1970s to the mid- 1980s. Since then, U.S. inflation has never exceeded about 6% and has averaged much less than that.

THE WASATCH TAKE ON INDIA

In addition to India’s longstanding political improvements, which have been enhanced and accelerated under Prime Minister Modi, other changes are occurring based largely on digitalization. This means India is making great strides in the identification of its citizens (with data integrity and security) and in the expansion of the internet and mobile-phone services—often more progressively than developed-market counterparts. Another result is that more can get done electronically with less need for a person’s physical presence and with fewer tangible items (like handwritten paper authorizations).

Digital innovation has also accelerated the delivery of financial services to hundreds of millions of people in India. This financialization—which entails the creation and distribution of banking, investment, credit, payment and insurance services—provides the foundation for any well-functioning modern economy. To understand the speed of India’s financialization, consider that one Indian bank launched a fully digital app through which ordinary people can use a mobile phone to open an account in less than two minutes. This app helped the bank add approximately eight million new accounts in 18 months, about doubling its customer base.

At a broader level, digital innovation has helped to formalize the Indian economy. Formalization refers to the greater transparency of economic activities and a better regulatory framework. One element of formalization is a simpler and fairer tax system that reduces layers of “petty corruption” and gets tax money to where it’s intended—to building infrastructure, for example. Another element of formalization is making personal and business transactions with electronic devices, rather than with tangible currency notes. This way, transactions are conducted more honestly and equitably—and with less “regulatory cholesterol” that clogs economic systems.

From a portfolio-management perspective, what’s interesting about India versus the U.S. is that our Indian holdings are light in technology names, while we’re generally overweighted in technology among our U.S. holdings. That’s because technology companies in India tend to be more export-oriented—and we prefer to focus on the domestic Indian economy by investing in consumer and financial companies that are using technology to benefit from the digitalization, financialization and formalization trends. In the U.S., we’re investing both in companies that are simply using technological solutions and in companies that are creating these solutions.

In India, we believe digitalization, financialization and formalization are interacting to produce exponential-type growth that’s largely responsible for a virtuous circle of amazing progress. Our complete analysis of this virtuous circle will be presented in an upcoming white paper, which we look forward to sharing with you.

With sincere thanks for your continuing investment and for your trust,

Matthew Dreith and Paul Lambert

RISKS AND DISCLOSURES

Mutual-fund investing involves risks, and the loss of principal is possible. Investing in small-cap and micro-cap funds will be more volatile, and the loss of principal could be greater, than investing in large-cap or more diversified funds. Investing in foreign securities, especially in frontier and emerging markets, entails special risks, such as unstable currencies, highly volatile securities markets, and political and social instability, which are described in more detail in the prospectus.

An investor should consider investment objectives, risks, charges and expenses carefully before investing. To obtain a prospectus, containing this and other information, visit www.WasatchFunds.com or call 800.551.1700. Please read the prospectus carefully before investing.

Wasatch Advisors is the investment advisor to Wasatch Funds.

Wasatch Funds are distributed by ALPS Distributors, Inc. (ADI). ADI is not affiliated with Wasatch Advisors, Inc.

Information in this document regarding market or economic trends, or the factors influencing historical or future performance, reflects the opinions of management as of the date of this document. These statements should not be relied upon for any other purpose. Past performance is no guarantee of future results, and there is no guarantee that the market forecasts discussed will be realized.

© 2019 Wasatch Funds. All rights reserved. Wasatch Funds are distributed by ALPS Distributors, Inc. WAS004987 Exp: 10/30/2019

More ETF Topics >