Summary: We’ve hit the longest economic expansion and bull market in U.S. history, but it can continue, in our opinion. The market endured a terrible growth scare over October-December last year and again pulled back during May on concerns about tariffs. These worries were ultimately overwhelmed by a combination of ongoing strong economic conditions, and a Federal Reserve that appears willing to act to support equity prices. The possible resolution of tariffs is helping this morning. The duration of economic growth and the bull market are often cited by those predicting a downturn, but current conditions remain favorable, in our opinion.

This Time Different or Each Time Different?

“This time it’s different” are fateful words, and normally best recognized as a warning sign. Our view is that the economy is strong, the consumer is in a good place, and American companies remain very innovative. The global political situation is also relatively stable, simmering tensions between the U.S. and Iran notwithstanding. This should be a good time for companies to do well, and thus the market to perform, and that’s exactly what we’ve seen as gains in 2019 have built on previous years. Yet, we constantly read in the financial media alarmist predictions of losses and economic catastrophe. Every possible conflict or sector-specific weakness is heralded as the possible pivot point away from the current positive conditions. We have also read a lot about the average length of the economic cycle, how long a bull market is supposed to last, and attempts to predict future market moves based on the current valuation of stocks compared to historical levels. These articles normally support a cautious conclusion because we don’t have examples of elongated economic cycles or bull markets from our past. On the contrary, we are bullish and optimistic because of what we see happening right now in the economy and because U.S. companies are so innovative.

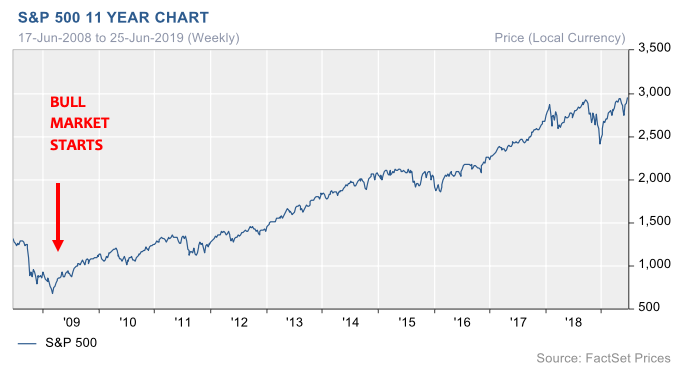

Figure 1. The longest-lived bull market since 1854. The S&P 500 has gained 331% or a 10.25 CAGR of 15%.

Are we saying this time it’s different and the economic cycle won’t turn? No. Something we’ve observed in 20 years investing in stocks, analyzing companies, and guessing about the economy is that comparisons to similar stocks, companies, or economic environments can often be misleading. The lesson for us is that rather than base investment decisions mostly on comparisons to similar scenarios (which is very tempting) it is better to approach each as if it were unique. In other words, we don’t argue that the current economic expansion and bull market should continue because this time it’s different. Rather, we argue that the best approach is to start with the assumption that each instance is different. When we look at momentum in the economy, innovation and the development of new technology and the creation of value in the U.S., the state of the world and the U.S. consumer, we see good things.

Behavioral Finance 101: Our Brains are Pattern Seeking Machines

Averages, charts, technicals, past performance, mean reversion, momentum, etc. We are not experts in behavioral finance. That caveat aside, as we understand it, behavioral finance is the idea that our brains were created by evolution in the natural world and these hardwired instincts continue to influence our behavior today, notably in making investment decisions. This manifests most frequently in emotional decisions like desire for gains and fear of losses. More importantly, it is apparent in our brains’ tendency to find patterns in information and similarities across situations even when there are none. Our brains do this because identifying patterns in the natural world conferred evolutionary advantage. For example, being able to recognize the features of rivers and streams that correlate with where it’s best to fish aided in the procurement of food. In finance and investing however, this same hardwired instinct to connect to the dots can lead us to find patterns and draw conclusions, even when the data doesn’t contain any. This brings us back to our main theme, which is a suggestion to treat each situation on its own merits.

How We are Managing Our and Client Money:

Our assumption is that our ability to forecast the overall market and macroeconomic conditions is highly limited. Accordingly, while we try to understand current conditions and trends, we try to make investment selections based on a long-term view and look for companies we can own throughout the economic cycle. The stocks of the best companies will still go down in a recession, but these businesses oftentimes benefit from challenging economic conditions as weaker competitors fail and cede share.

Selection from our model portfolio: Our approach is to own high-quality companies, bought opportunistically, and own them long-term with the intention to minimize trading costs and taxes. Our portfolio is concentrated (~20 positions) and generally we are favorably inclined towards companies we know or at least find easy to understand.

When NOT to Sell…

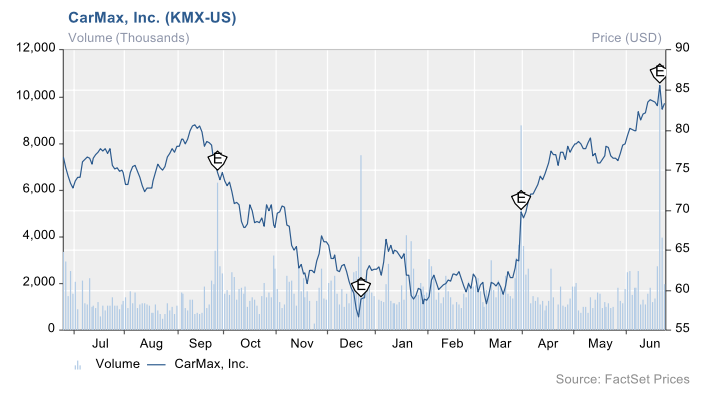

CarMax (KMX): More difficult than making the decision to buy a stock, is figuring out when to sell it, in our opinion. One can buy a stock for many reasons, but among them is always included the idea/ hope/ desire that it will be worth more in the future. Selling is a lot more complicated because things like taxes come into play, and a broader set of emotions get involved. We’re only going to talk about a winner today, CarMax, which is a stock we wrote about KMX in our April and December newsletters. You can read those write-ups here. Two weeks ago, on Friday morning, KMX reported very strong sales growth, exceeding analyst estimates, and shares have since risen to a new all-time high of $87 per share. You can see the chart below. Simultaneously, the market is also at an all-time high. Thus, we have an individual stock at an all-time high and a market at an all-time high. This is normally when you may hear your broker calling you to take some money “off the table” and “lock in gains”. Leaving aside the tax implication, and acknowledging that anything can happen, our point is that the stock’s recent performance and the market’s performance are the wrong consideration set to use in making a buy or sell decision. Rather, you should continue to own a stock as long as the fundamental case for investing in the business is intact and you should sell when something has changed unfavorably (assuming you don’t need the money and haven’t found an alternative, more attractive investment elsewhere). In KMX’s case, the company is reporting accelerating sales growth, driven partially by the development of a new sales channel for its business, which is to sell used cars entirely online with delivery to the customer’s home. (Previously, the company only transacted at its stores.) It’s the company’s early success with this initiative, and investor anticipation of continued sales gains, that have produced the big move in the shares (up >36% YTD). Our view is that KMX is an excellent company, that leads with technology, offers a better experience to its customers vs. competition, is financially strong, and has a very large long-term opportunity for growth. Layer on top of this an innovative new sales channel that leverages the core business, and we have the making of a great stock. This is not a name to sell based on the chart or risk of short-term pullback.

Figure 2. KMX shares have had a nice move YTD, up >36%.

John Zolidis,

President & Founder

Quo Vadis Capital, Inc.

[email protected]

www.quovadiscapita.com

General Disclosures:

Quo Vadis Capital, Inc. (“Quo Vadis”) is an independent research provider offering research and consulting services. The research products are for institutional investors only.

The price target, if any, contained in this report represents the analyst’s application of a formula to certain metrics derived from actual and estimated future performance of the company. Analysts may use various formulas tailored to the facts and circumstances surrounding a specific company to arrive at the price target. Various risk factors may impede the company’s securities from achieving the analyst’s price target, such as an unfavorable macroeconomic environment, a failure of the company to perform as expected, the departure of key personnel or other events or circumstances that cannot be reasonably anticipated at the time the price target is calculated. Quo Vadis may change the price target on this company without notice. Additional information on the securities mentioned in this report is available upon request. This report is based on data obtained from sources Quo Vadis believes to be reliable; however, Quo Vadis does not guarantee its accuracy and does not purport to be complete. Opinion is as of the date of the report unless labeled otherwise and is subject to change without notice. Updates may be provided based on developments and events and as otherwise appropriate. Updates may be restricted based on regulatory requirements or other considerations. Consequently, there should be no assumption that updates will be made. Quo Vadis disclaims any warranty of any kind, whether express or implied, as to any matter whatsoever relating to this research report and any analysis, discussion or trade ideas contained herein. This research report is provided on an "as is" basis for use at your own risk, and neither Quo Vadis nor its affiliates are liable for any damages or injury resulting from use of this information. This report should not be construed as advice designed to meet the particular investment needs of any investor or as an offer or solicitation to buy or sell the securities or financial instruments mentioned herein. This report is provided for information purposes only and does not represent an offer or solicitation in any jurisdiction where such offer would be prohibited. Commentary regarding the future direction of financial markets is illustrative and is not intended to predict actual results, which may differ substantially from the opinions expressed herein. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur.

The analyst who is the author of this report has a long position in CarMax, Inc. (KMX). Quo Vadis prohibits analysts from trading in a way that is inconsistent with opinions expressed in reports [subject to exceptions for unanticipated significant changes in the personal financial circumstances of the analyst].

Permission is hereby granted to reproduce or redistribute this report. Please cite Quo Vadis Capital, Inc. in any reproduction.

SEC Reg AC Certification:

All of the views expressed in this research report accurately reflect the research analyst's personal views about any and all of the subject securities or issuers. No part of the research analyst's compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed by the research analyst in the subject company of this research report.

© Quo Vadis Capital, Inc.

Read more commentaries by Quo Vadis Capital